Meritage Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

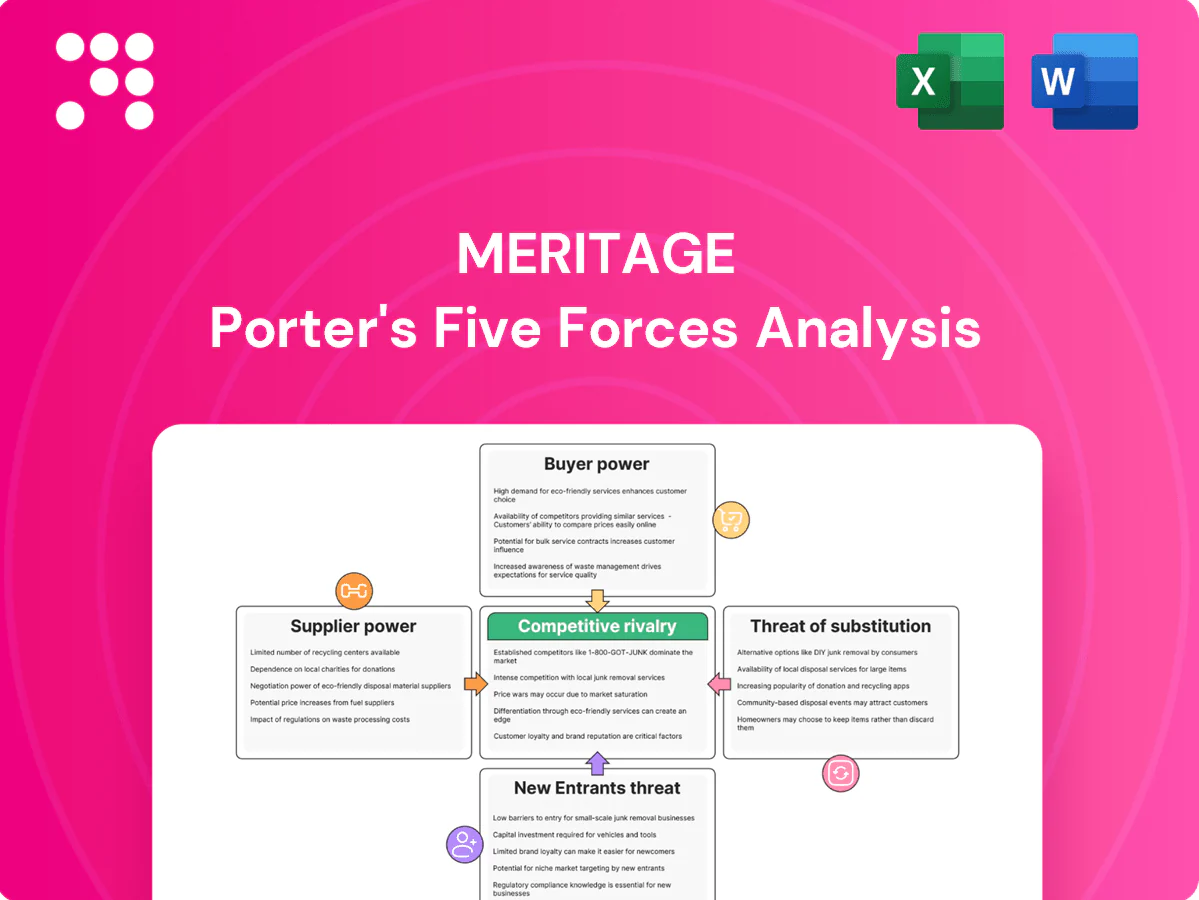

Meritage faces moderate buyer power, fragmented suppliers, and growing competitive pressure from national builders and niche local firms, while substitutes and regulatory shifts shape pricing and margins. This snapshot highlights key stress points and strategic levers for management. The full Porter's Five Forces Analysis quantifies each force, provides visuals and tactical recommendations tailored to Meritage. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Franchisor control & approved suppliers

As Wendy's largest franchisee, Meritage must source from franchisor-approved vendors, concentrating supplier options and limiting substitution; Wendy's reported roughly 6,900 systemwide restaurants in 2024, underscoring the scale of its approved-supplier network. Wendy's strict specifications, QA and branding standards increase supplier leverage by narrowing eligible producers and enforcing compliance. Meritage's scale, however, can still secure volume discounts and preferred terms within the approved network, though compliance requirements reduce flexibility during supply shocks.

Commodity volatility (beef, buns, produce)

Core inputs like beef, buns and produce faced volatile 2024 swings—beef input costs rose roughly 10% YoY, wheat/bakery costs about 8% and produce inflation near 6%—giving upstream suppliers episodic pricing power tied to weather and disease. Menu price adjustments typically lag these spikes, squeezing margins during cost surges. Hedging and menu engineering reduce exposure but do not eliminate volatility, while approved-supplier contracts can delay repricing or rapid re-sourcing.

Packaging, beverages, and CPG brand power

Beverage contracts and branded condiments/packaging typically use standardized list pricing with limited negotiation; in the US carbonated soft drink market Coca-Cola and PepsiCo together account for roughly 65–70% share, constraining buyer leverage. Global CPG suppliers wield strong brand equity and scale—global packaging industry surpassed about $1 trillion in 2024—reinforcing supplier bargaining power. Multi-year agreements stabilize costs but lock buyers into pricing and reduce flexibility, while volume rebates (commonly 1–3% on high-volume deals) partly offset list prices.

Labor and staffing intermediaries

Tight 2024 labor markets (U.S. unemployment near 4.0%) plus rising wages and higher compliance costs have increased the bargaining power of labor suppliers for Meritage; dependence on staffing pipelines and training vendors creates cost stickiness and limits flexibility. Scale aids investment in recruitment tech and retention programs but does not fully offset wage pressure, while elevated turnover raises replacement costs and hiring premium.

- Higher bargaining power: low unemployment (~4.0% in 2024)

- Cost stickiness: reliance on staffing/training vendors

- Scale benefits: recruitment tech, retention spend

- Replacement cost driver: higher turnover raises hiring premiums

Real estate landlords and utilities

Prime drive-thru sites remain scarce, with vacancy near 2% in top U.S. metros in 2024, letting landlords push rent and renewals; NNN leases and CAM charges on high-traffic corners are often non-negotiable. Utilities act as local monopolies with routine pass-through increases, and Meritage’s portfolio breadth enables site swaps but cannot eliminate absolute rent inflation.

- Scarcity: vacancy ~2% (2024)

- Lease pressure: NNN/CAM non-negotiable on corners

- Utilities: local monopolies, pass-through hikes

- Mitigation: portfolio swaps help but not stop rent inflation

Network of 6,900 units concentrates supplier power; beef +10%

Meritage is limited to Wendy's ~6,900 approved-supplier network (2024), concentrating supplier power despite Meritage volume leverage. Key inputs saw 2024 cost swings—beef +10% YoY, wheat +8%, produce +6%—raising episodic supplier pricing power. Beverage/packaging dominated by Coca-Cola/PepsiCo (65–70% CSD share) and $1T+ packaging market, locking pricing.

| Item | 2024 Metric |

|---|---|

| Wendy's system | ~6,900 restaurants |

| Beef costs | +10% YoY |

| Wheat/bakery | +8% |

| Produce | +6% |

| CSD share | 65–70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Meritage that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic commentary to inform pricing, market positioning, and defensive growth initiatives.

Meritage Porter's Five Forces provides a one-sheet, customizable analysis with radar-chart visualization and clean, no-code layout—so teams can quickly assess competitive pressure, simulate scenarios, and drop insights straight into decks or dashboards.

Customers Bargaining Power

Price-sensitive, low-switching diners

QSR guests can switch instantly across brands, making demand highly price-elastic; in the US QSR channel (≈$300B 2024), small price deltas or promotions trigger measurable traffic shifts. Value menus and bundled offers remain essential tools to defend share and recover margin. Individual diners lack formal bargaining power, but collectively they force constant pricing and promotion cycles.

Brand loyalty to Wendy’s

Wendy’s brand equity and menu innovation—notably expanded breakfast and premium offerings—create stickiness that tempers buyer power, supported by a loyalty program exceeding 20 million members and a global footprint of over 7,000 restaurants. Consistent execution across locations sustains repeat visits, while perceived differentiation from premium items raises switching costs. Loyalty strains when broad price hikes occur, prompting churn during inflationary periods.

Digital transparency and reviews

Mobile apps, ratings, and social media amplify buyer voice and comparison shopping—with about 4.9 billion global social media users in 2024, consumers can instantly compare prices, wait times, and deals. Visibility of real-time wait times and dynamic pricing raises buyer bargaining power and drives churn. Negative reviews can shift local demand within hours, while strong operational execution (speed, consistency, service) directly moderates this force.

Third-party delivery platforms

Third-party aggregators steer discovery, promotion placement and pricing, shifting bargaining power toward buyers and platforms; commissions commonly range 15-30%, compressing restaurant margins and constraining pass-through pricing, while delivery still expands addressable demand.

- Commission range 15-30%

- DoorDash ~60% US market share (2024)

- Optimize first-party channels to reduce dependency

Local income and traffic patterns

Trade-area dynamics—commuter flows, schools, and events—shape buyer density and choice sets; U.S. median household income was $74,580 (2023 Census) and average commute ~27.6 minutes (2023 ACS), driving where and when customers buy. When alternatives cluster, buyers gain leverage through convenience; high-quality sites and fast drive-thru throughput (now over half of many QSR transactions) reduce time cost and blunt that leverage, making real estate strategy a critical counterweight.

- Trade-area pull: commuter density, schools, events

- Income/commute: $74,580 median; 27.6 min avg commute (2023)

- Counterweights: premium site + drive-thru throughput >50%

QSR market $300B: price-elastic demand - promos shift traffic, aggregators boost buyer leverage

QSR demand is highly price-elastic; US QSR ≈$300B (2024) so small price/promotions shift traffic. Wendy’s loyalty >20M and 7,000+ restaurants create some stickiness but broad price hikes drive churn. Aggregators (commissions 15-30%; DoorDash ~60% US share 2024) raise buyer leverage; real estate and drive-thru throughput blunt it.

| Metric | Value |

|---|---|

| US QSR | $300B (2024) |

| Wendy’s loyalty | >20M |

| Restaurants | 7,000+ |

| Aggregator commission | 15-30% |

| DoorDash US share | ~60% (2024) |

What You See Is What You Get

Meritage Porter's Five Forces Analysis

This preview shows the exact Meritage Porter's Five Forces Analysis you'll receive after purchase—fully formatted, professionally written, and ready to use. It contains the complete competitive assessment, covering supplier and buyer power, threat of substitutes and new entrants, and industry rivalry insights. No samples or placeholders—buying grants immediate access to this identical file.

A Must-Have Tool for Decision-Makers

Meritage faces moderate buyer power, fragmented suppliers, and growing competitive pressure from national builders and niche local firms, while substitutes and regulatory shifts shape pricing and margins. This snapshot highlights key stress points and strategic levers for management. The full Porter's Five Forces Analysis quantifies each force, provides visuals and tactical recommendations tailored to Meritage. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Franchisor control & approved suppliers

As Wendy's largest franchisee, Meritage must source from franchisor-approved vendors, concentrating supplier options and limiting substitution; Wendy's reported roughly 6,900 systemwide restaurants in 2024, underscoring the scale of its approved-supplier network. Wendy's strict specifications, QA and branding standards increase supplier leverage by narrowing eligible producers and enforcing compliance. Meritage's scale, however, can still secure volume discounts and preferred terms within the approved network, though compliance requirements reduce flexibility during supply shocks.

Commodity volatility (beef, buns, produce)

Core inputs like beef, buns and produce faced volatile 2024 swings—beef input costs rose roughly 10% YoY, wheat/bakery costs about 8% and produce inflation near 6%—giving upstream suppliers episodic pricing power tied to weather and disease. Menu price adjustments typically lag these spikes, squeezing margins during cost surges. Hedging and menu engineering reduce exposure but do not eliminate volatility, while approved-supplier contracts can delay repricing or rapid re-sourcing.

Packaging, beverages, and CPG brand power

Beverage contracts and branded condiments/packaging typically use standardized list pricing with limited negotiation; in the US carbonated soft drink market Coca-Cola and PepsiCo together account for roughly 65–70% share, constraining buyer leverage. Global CPG suppliers wield strong brand equity and scale—global packaging industry surpassed about $1 trillion in 2024—reinforcing supplier bargaining power. Multi-year agreements stabilize costs but lock buyers into pricing and reduce flexibility, while volume rebates (commonly 1–3% on high-volume deals) partly offset list prices.

Labor and staffing intermediaries

Tight 2024 labor markets (U.S. unemployment near 4.0%) plus rising wages and higher compliance costs have increased the bargaining power of labor suppliers for Meritage; dependence on staffing pipelines and training vendors creates cost stickiness and limits flexibility. Scale aids investment in recruitment tech and retention programs but does not fully offset wage pressure, while elevated turnover raises replacement costs and hiring premium.

- Higher bargaining power: low unemployment (~4.0% in 2024)

- Cost stickiness: reliance on staffing/training vendors

- Scale benefits: recruitment tech, retention spend

- Replacement cost driver: higher turnover raises hiring premiums

Real estate landlords and utilities

Prime drive-thru sites remain scarce, with vacancy near 2% in top U.S. metros in 2024, letting landlords push rent and renewals; NNN leases and CAM charges on high-traffic corners are often non-negotiable. Utilities act as local monopolies with routine pass-through increases, and Meritage’s portfolio breadth enables site swaps but cannot eliminate absolute rent inflation.

- Scarcity: vacancy ~2% (2024)

- Lease pressure: NNN/CAM non-negotiable on corners

- Utilities: local monopolies, pass-through hikes

- Mitigation: portfolio swaps help but not stop rent inflation

Network of 6,900 units concentrates supplier power; beef +10%

Meritage is limited to Wendy's ~6,900 approved-supplier network (2024), concentrating supplier power despite Meritage volume leverage. Key inputs saw 2024 cost swings—beef +10% YoY, wheat +8%, produce +6%—raising episodic supplier pricing power. Beverage/packaging dominated by Coca-Cola/PepsiCo (65–70% CSD share) and $1T+ packaging market, locking pricing.

| Item | 2024 Metric |

|---|---|

| Wendy's system | ~6,900 restaurants |

| Beef costs | +10% YoY |

| Wheat/bakery | +8% |

| Produce | +6% |

| CSD share | 65–70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Meritage that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic commentary to inform pricing, market positioning, and defensive growth initiatives.

Meritage Porter's Five Forces provides a one-sheet, customizable analysis with radar-chart visualization and clean, no-code layout—so teams can quickly assess competitive pressure, simulate scenarios, and drop insights straight into decks or dashboards.

Customers Bargaining Power

Price-sensitive, low-switching diners

QSR guests can switch instantly across brands, making demand highly price-elastic; in the US QSR channel (≈$300B 2024), small price deltas or promotions trigger measurable traffic shifts. Value menus and bundled offers remain essential tools to defend share and recover margin. Individual diners lack formal bargaining power, but collectively they force constant pricing and promotion cycles.

Brand loyalty to Wendy’s

Wendy’s brand equity and menu innovation—notably expanded breakfast and premium offerings—create stickiness that tempers buyer power, supported by a loyalty program exceeding 20 million members and a global footprint of over 7,000 restaurants. Consistent execution across locations sustains repeat visits, while perceived differentiation from premium items raises switching costs. Loyalty strains when broad price hikes occur, prompting churn during inflationary periods.

Digital transparency and reviews

Mobile apps, ratings, and social media amplify buyer voice and comparison shopping—with about 4.9 billion global social media users in 2024, consumers can instantly compare prices, wait times, and deals. Visibility of real-time wait times and dynamic pricing raises buyer bargaining power and drives churn. Negative reviews can shift local demand within hours, while strong operational execution (speed, consistency, service) directly moderates this force.

Third-party delivery platforms

Third-party aggregators steer discovery, promotion placement and pricing, shifting bargaining power toward buyers and platforms; commissions commonly range 15-30%, compressing restaurant margins and constraining pass-through pricing, while delivery still expands addressable demand.

- Commission range 15-30%

- DoorDash ~60% US market share (2024)

- Optimize first-party channels to reduce dependency

Local income and traffic patterns

Trade-area dynamics—commuter flows, schools, and events—shape buyer density and choice sets; U.S. median household income was $74,580 (2023 Census) and average commute ~27.6 minutes (2023 ACS), driving where and when customers buy. When alternatives cluster, buyers gain leverage through convenience; high-quality sites and fast drive-thru throughput (now over half of many QSR transactions) reduce time cost and blunt that leverage, making real estate strategy a critical counterweight.

- Trade-area pull: commuter density, schools, events

- Income/commute: $74,580 median; 27.6 min avg commute (2023)

- Counterweights: premium site + drive-thru throughput >50%

QSR market $300B: price-elastic demand - promos shift traffic, aggregators boost buyer leverage

QSR demand is highly price-elastic; US QSR ≈$300B (2024) so small price/promotions shift traffic. Wendy’s loyalty >20M and 7,000+ restaurants create some stickiness but broad price hikes drive churn. Aggregators (commissions 15-30%; DoorDash ~60% US share 2024) raise buyer leverage; real estate and drive-thru throughput blunt it.

| Metric | Value |

|---|---|

| US QSR | $300B (2024) |

| Wendy’s loyalty | >20M |

| Restaurants | 7,000+ |

| Aggregator commission | 15-30% |

| DoorDash US share | ~60% (2024) |

What You See Is What You Get

Meritage Porter's Five Forces Analysis

This preview shows the exact Meritage Porter's Five Forces Analysis you'll receive after purchase—fully formatted, professionally written, and ready to use. It contains the complete competitive assessment, covering supplier and buyer power, threat of substitutes and new entrants, and industry rivalry insights. No samples or placeholders—buying grants immediate access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Meritage faces moderate buyer power, fragmented suppliers, and growing competitive pressure from national builders and niche local firms, while substitutes and regulatory shifts shape pricing and margins. This snapshot highlights key stress points and strategic levers for management. The full Porter's Five Forces Analysis quantifies each force, provides visuals and tactical recommendations tailored to Meritage. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Franchisor control & approved suppliers

As Wendy's largest franchisee, Meritage must source from franchisor-approved vendors, concentrating supplier options and limiting substitution; Wendy's reported roughly 6,900 systemwide restaurants in 2024, underscoring the scale of its approved-supplier network. Wendy's strict specifications, QA and branding standards increase supplier leverage by narrowing eligible producers and enforcing compliance. Meritage's scale, however, can still secure volume discounts and preferred terms within the approved network, though compliance requirements reduce flexibility during supply shocks.

Commodity volatility (beef, buns, produce)

Core inputs like beef, buns and produce faced volatile 2024 swings—beef input costs rose roughly 10% YoY, wheat/bakery costs about 8% and produce inflation near 6%—giving upstream suppliers episodic pricing power tied to weather and disease. Menu price adjustments typically lag these spikes, squeezing margins during cost surges. Hedging and menu engineering reduce exposure but do not eliminate volatility, while approved-supplier contracts can delay repricing or rapid re-sourcing.

Packaging, beverages, and CPG brand power

Beverage contracts and branded condiments/packaging typically use standardized list pricing with limited negotiation; in the US carbonated soft drink market Coca-Cola and PepsiCo together account for roughly 65–70% share, constraining buyer leverage. Global CPG suppliers wield strong brand equity and scale—global packaging industry surpassed about $1 trillion in 2024—reinforcing supplier bargaining power. Multi-year agreements stabilize costs but lock buyers into pricing and reduce flexibility, while volume rebates (commonly 1–3% on high-volume deals) partly offset list prices.

Labor and staffing intermediaries

Tight 2024 labor markets (U.S. unemployment near 4.0%) plus rising wages and higher compliance costs have increased the bargaining power of labor suppliers for Meritage; dependence on staffing pipelines and training vendors creates cost stickiness and limits flexibility. Scale aids investment in recruitment tech and retention programs but does not fully offset wage pressure, while elevated turnover raises replacement costs and hiring premium.

- Higher bargaining power: low unemployment (~4.0% in 2024)

- Cost stickiness: reliance on staffing/training vendors

- Scale benefits: recruitment tech, retention spend

- Replacement cost driver: higher turnover raises hiring premiums

Real estate landlords and utilities

Prime drive-thru sites remain scarce, with vacancy near 2% in top U.S. metros in 2024, letting landlords push rent and renewals; NNN leases and CAM charges on high-traffic corners are often non-negotiable. Utilities act as local monopolies with routine pass-through increases, and Meritage’s portfolio breadth enables site swaps but cannot eliminate absolute rent inflation.

- Scarcity: vacancy ~2% (2024)

- Lease pressure: NNN/CAM non-negotiable on corners

- Utilities: local monopolies, pass-through hikes

- Mitigation: portfolio swaps help but not stop rent inflation

Network of 6,900 units concentrates supplier power; beef +10%

Meritage is limited to Wendy's ~6,900 approved-supplier network (2024), concentrating supplier power despite Meritage volume leverage. Key inputs saw 2024 cost swings—beef +10% YoY, wheat +8%, produce +6%—raising episodic supplier pricing power. Beverage/packaging dominated by Coca-Cola/PepsiCo (65–70% CSD share) and $1T+ packaging market, locking pricing.

| Item | 2024 Metric |

|---|---|

| Wendy's system | ~6,900 restaurants |

| Beef costs | +10% YoY |

| Wheat/bakery | +8% |

| Produce | +6% |

| CSD share | 65–70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Meritage that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic commentary to inform pricing, market positioning, and defensive growth initiatives.

Meritage Porter's Five Forces provides a one-sheet, customizable analysis with radar-chart visualization and clean, no-code layout—so teams can quickly assess competitive pressure, simulate scenarios, and drop insights straight into decks or dashboards.

Customers Bargaining Power

Price-sensitive, low-switching diners

QSR guests can switch instantly across brands, making demand highly price-elastic; in the US QSR channel (≈$300B 2024), small price deltas or promotions trigger measurable traffic shifts. Value menus and bundled offers remain essential tools to defend share and recover margin. Individual diners lack formal bargaining power, but collectively they force constant pricing and promotion cycles.

Brand loyalty to Wendy’s

Wendy’s brand equity and menu innovation—notably expanded breakfast and premium offerings—create stickiness that tempers buyer power, supported by a loyalty program exceeding 20 million members and a global footprint of over 7,000 restaurants. Consistent execution across locations sustains repeat visits, while perceived differentiation from premium items raises switching costs. Loyalty strains when broad price hikes occur, prompting churn during inflationary periods.

Digital transparency and reviews

Mobile apps, ratings, and social media amplify buyer voice and comparison shopping—with about 4.9 billion global social media users in 2024, consumers can instantly compare prices, wait times, and deals. Visibility of real-time wait times and dynamic pricing raises buyer bargaining power and drives churn. Negative reviews can shift local demand within hours, while strong operational execution (speed, consistency, service) directly moderates this force.

Third-party delivery platforms

Third-party aggregators steer discovery, promotion placement and pricing, shifting bargaining power toward buyers and platforms; commissions commonly range 15-30%, compressing restaurant margins and constraining pass-through pricing, while delivery still expands addressable demand.

- Commission range 15-30%

- DoorDash ~60% US market share (2024)

- Optimize first-party channels to reduce dependency

Local income and traffic patterns

Trade-area dynamics—commuter flows, schools, and events—shape buyer density and choice sets; U.S. median household income was $74,580 (2023 Census) and average commute ~27.6 minutes (2023 ACS), driving where and when customers buy. When alternatives cluster, buyers gain leverage through convenience; high-quality sites and fast drive-thru throughput (now over half of many QSR transactions) reduce time cost and blunt that leverage, making real estate strategy a critical counterweight.

- Trade-area pull: commuter density, schools, events

- Income/commute: $74,580 median; 27.6 min avg commute (2023)

- Counterweights: premium site + drive-thru throughput >50%

QSR market $300B: price-elastic demand - promos shift traffic, aggregators boost buyer leverage

QSR demand is highly price-elastic; US QSR ≈$300B (2024) so small price/promotions shift traffic. Wendy’s loyalty >20M and 7,000+ restaurants create some stickiness but broad price hikes drive churn. Aggregators (commissions 15-30%; DoorDash ~60% US share 2024) raise buyer leverage; real estate and drive-thru throughput blunt it.

| Metric | Value |

|---|---|

| US QSR | $300B (2024) |

| Wendy’s loyalty | >20M |

| Restaurants | 7,000+ |

| Aggregator commission | 15-30% |

| DoorDash US share | ~60% (2024) |

What You See Is What You Get

Meritage Porter's Five Forces Analysis

This preview shows the exact Meritage Porter's Five Forces Analysis you'll receive after purchase—fully formatted, professionally written, and ready to use. It contains the complete competitive assessment, covering supplier and buyer power, threat of substitutes and new entrants, and industry rivalry insights. No samples or placeholders—buying grants immediate access to this identical file.