Meritz Financial Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our targeted PESTLE Analysis of Meritz Financial Group—three concise sections reveal how political, economic, social, technological, legal, and environmental forces will shape its trajectory. Ideal for investors and strategists seeking fast, actionable intelligence. Purchase the full report to access in-depth scenarios, data-driven risks, and growth opportunities ready for immediate use.

Political factors

Regulatory stance in Korea

Korea’s Financial Services Commission and Financial Supervisory Service set capital, product and conduct rules that directly shape Meritz Financial Group’s insurance, brokerage and asset-management operations. Recent policy emphasis on solvency and consumer protection has increased compliance scope and costs. Variations in supervisory intensity constrain pricing flexibility and growth prospects. Ongoing close engagement is essential for approvals and innovation pilots.

Government healthcare & pensions

Public pension and health systems shape demand for Meritz Financial Group’s private life and health products, with Korea’s elderly relative poverty at about 43.4% (OECD, 2022) underscoring gaps private insurers can fill. Reforms to coverage, premiums or retirement age can redirect savings into or away from private solutions; National Pension Service assets exceeded roughly 1,100 trillion KRW by end-2023, affecting market flows. Sudden policy shifts risk disrupting product portfolios and persistency, creating both threat and opportunity.

Geopolitical risks & peninsula security

Inter-Korean tensions and regional great-power competition amplify market volatility and depress risk appetite, with South Korea a $1.8 trillion economy (World Bank, 2023). Insurance claims, asset values and funding costs can move rapidly under stress, as seen in episodic Korean credit spread widenings. Political-risk hedging and scenario planning are crucial to protect Meritz capital, while investor sentiment toward Korean financials can swing sharply with headline risk.

Industrial policy & digital finance

National pushes for digitalization and the data economy—Korea rolled out open banking in 2019 and expanded regulatory sandboxes under the Financial Services Commission—favor fintech partnerships and regtech adoption, enabling faster product digitization for groups like Meritz; fragmented standards or policy reversals, however, can stall cross-selling and platform rollouts.

- tag:sandbox expansion

- tag:open banking 2019

- tag:fintech partnerships

- tag:policy risk

Tax policy & incentives

Tax shifts directly change customer behavior: Korea’s top corporate tax remains 25% and changes to insurance tax deductibility, capital gains or dividend tax rates can prompt customers to favor holding structures or tax-advantaged products; incentives for retirement/protection products (eg IRP/IRAs) historically lift demand, while adverse reforms can compress Meritz’s margins and reduce retained earnings and payout capacity.

- Top corporate tax: 25%

- Retirement incentives raise product sales (IRP/IRA frameworks)

- Capital gains/dividend tax changes shift customer holdings, affecting margins

Regulatory tightening and elderly poverty squeeze insurers; NPS ≈1,100T

Regulators (FSC/FSS) tighten solvency and consumer rules, raising compliance costs and limiting pricing flexibility for Meritz. Public pensions and Korea’s elderly relative poverty ~43.4% (OECD 2022) with NPS assets ≈1,100 trillion KRW (end‑2023) shape private product demand. Geopolitical risk and $1.8T GDP (World Bank 2023) amplify market volatility and funding cost swings.

| Indicator | Value |

|---|---|

| Elderly relative poverty (OECD) | 43.4% (2022) |

| National Pension Service assets | ≈1,100 trillion KRW (end‑2023) |

| GDP | $1.8 trillion (2023) |

| Top corporate tax | 25% |

What is included in the product

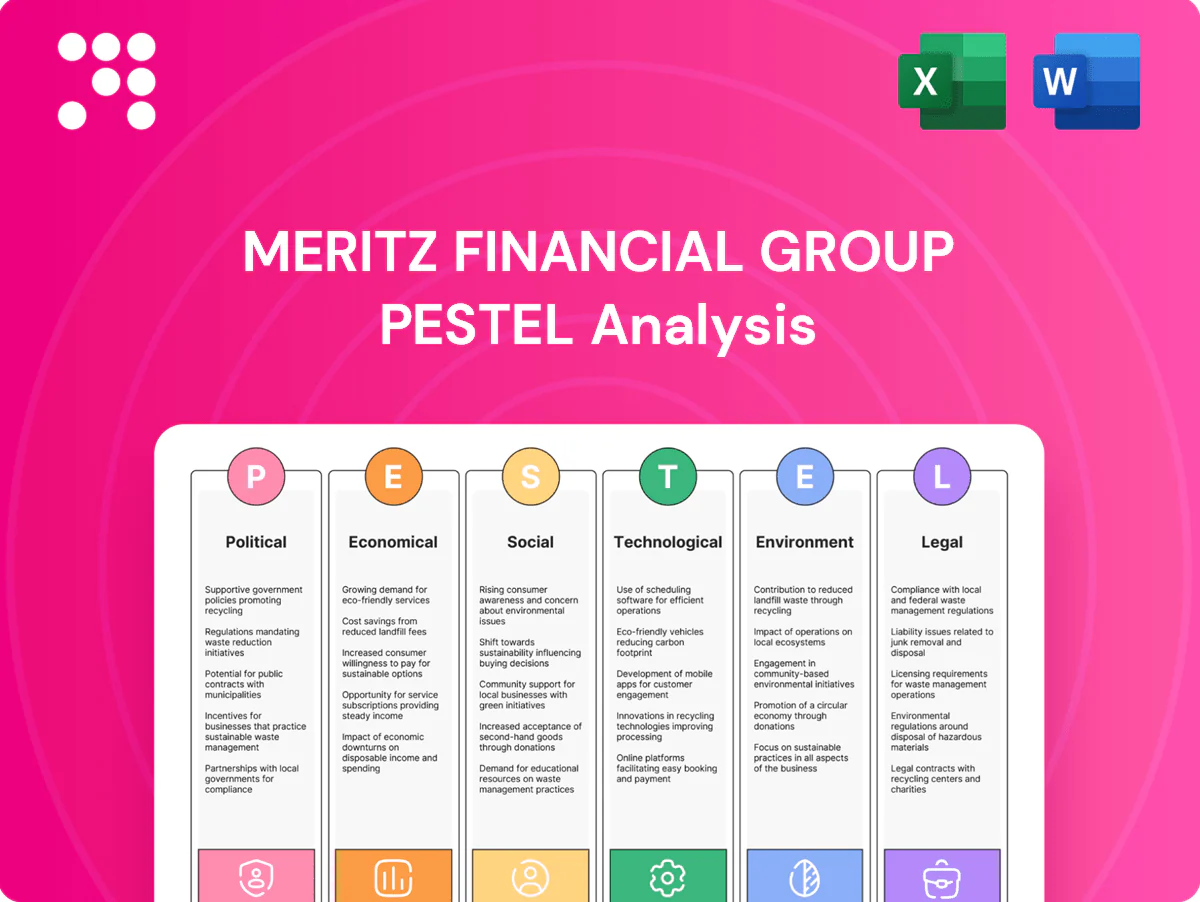

Explores how external macro-environmental factors uniquely affect Meritz Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to its region and industry. Designed to support executives and investors with forward-looking implications for strategy and risk management.

A clean, summarized Meritz Financial Group PESTLE analysis that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and planning sessions.

Economic factors

Interest rate cycle

BOK policy rates drive Meritz Financial Group’s investment yields, reserve discounting and product guarantees; rising rates improve reinvestment yields but increase lapse and spread risks on in-force guarantees, while falling rates compress margins and strain capital for long-duration liabilities. Robust asset-liability management is pivotal to stabilize earnings through rate cycles.

Macroeconomic growth

Slowing macro growth—GDP about 2.5% in 2024 with IMF 2025 forecasts near 1.8%—pressures household income and employment (unemployment ~3.0% in 2024), reducing premium affordability and brokerage activity. Weaker corporate capex and a thinned IPO pipeline cut securities revenues and trading volumes. Slower growth elevates credit risk across investment portfolios, while Meritzs diversification across insurance, securities and asset management helps cushion cyclicality.

Inflation dynamics

Inflation (South Korea CPI 2024 ~2.6%) pushes up claims costs and operating expenses, notably in non-life lines where medical and repair costs have risen. Pricing adequacy for Meritz depends on timely rate adjustments and strict underwriting to protect margins. Inflation alters discount rates and technical reserve valuations as the Bank of Korea policy rate stood near 3.5% (mid‑2025). Active hedging and cost productivity programs help mitigate erosion.

Capital markets volatility

Capital markets volatility directly affects Meritz through fee, trading and AUM-based revenues; 2024 saw elevated market nervousness (VIX averaged about 17), increasing mark-to-market swings under IFRS and quarterly earnings variability. Insurer-sector ROE volatility moved several percentage points in 2024, while liquidity squeezes raised short-term funding spreads by roughly 80–120 bps, heightening funding costs and lapse risk; disciplined investment policies and explicit risk budgets boost resilience.

- Equity/bond swings: revenue sensitivity

- IFRS mark-to-market: earnings variability

- Liquidity: +80–120 bps funding spread

- Mitigation: balanced investments, risk budgets

Household leverage & housing

Korean household debt exceeded 1,900 trillion KRW (Bank of Korea, 2024), and property cycles materially affect Meritz Financial Group’s credit quality and customer spending on protection and savings products. Mortgage tightening and rising DSRs have reduced ancillary financial activity and refinancing, while wealth effects from property/equity moves sway asset management inflows. Stress tests must include lapse and claims sensitivity to housing-led credit shocks.

- household-debt: >1,900 trillion KRW (BOK 2024)

- mortgage-tightening: lowers ancillary revenue

- wealth-effect: drives AM inflows/outflows

- stress-scenarios: lapse & claims sensitivity

Regulatory tightening and elderly poverty squeeze insurers; NPS ≈1,100T

BOK policy (~3.5% mid‑2025) drives reinvestment yields and reserve discounting; rate swings raise lapse/spread risks while lower rates compress margins. GDP ~2.5% (2024) with IMF 2025 ~1.8% and CPI ~2.6% (2024) weaken premium affordability; household debt >1,900 trn KRW amplifies credit/lapse exposure. Capital-market volatility (funding spreads +80–120bps) increases earnings volatility.

| Metric | Value |

|---|---|

| BOK policy rate | ~3.5% (mid‑2025) |

| GDP | 2.5% (2024) / 1.8% (IMF 2025) |

| CPI | ~2.6% (2024) |

| Household debt | >1,900 trn KRW (2024) |

| Funding spread | +80–120 bps |

What You See Is What You Get

Meritz Financial Group PESTLE Analysis

This Meritz Financial Group PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase—ready to use with no placeholders. The content, structure, and layout shown are identical to the downloadable file. You’ll get the same professional, final report immediately after checkout.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our targeted PESTLE Analysis of Meritz Financial Group—three concise sections reveal how political, economic, social, technological, legal, and environmental forces will shape its trajectory. Ideal for investors and strategists seeking fast, actionable intelligence. Purchase the full report to access in-depth scenarios, data-driven risks, and growth opportunities ready for immediate use.

Political factors

Regulatory stance in Korea

Korea’s Financial Services Commission and Financial Supervisory Service set capital, product and conduct rules that directly shape Meritz Financial Group’s insurance, brokerage and asset-management operations. Recent policy emphasis on solvency and consumer protection has increased compliance scope and costs. Variations in supervisory intensity constrain pricing flexibility and growth prospects. Ongoing close engagement is essential for approvals and innovation pilots.

Government healthcare & pensions

Public pension and health systems shape demand for Meritz Financial Group’s private life and health products, with Korea’s elderly relative poverty at about 43.4% (OECD, 2022) underscoring gaps private insurers can fill. Reforms to coverage, premiums or retirement age can redirect savings into or away from private solutions; National Pension Service assets exceeded roughly 1,100 trillion KRW by end-2023, affecting market flows. Sudden policy shifts risk disrupting product portfolios and persistency, creating both threat and opportunity.

Geopolitical risks & peninsula security

Inter-Korean tensions and regional great-power competition amplify market volatility and depress risk appetite, with South Korea a $1.8 trillion economy (World Bank, 2023). Insurance claims, asset values and funding costs can move rapidly under stress, as seen in episodic Korean credit spread widenings. Political-risk hedging and scenario planning are crucial to protect Meritz capital, while investor sentiment toward Korean financials can swing sharply with headline risk.

Industrial policy & digital finance

National pushes for digitalization and the data economy—Korea rolled out open banking in 2019 and expanded regulatory sandboxes under the Financial Services Commission—favor fintech partnerships and regtech adoption, enabling faster product digitization for groups like Meritz; fragmented standards or policy reversals, however, can stall cross-selling and platform rollouts.

- tag:sandbox expansion

- tag:open banking 2019

- tag:fintech partnerships

- tag:policy risk

Tax policy & incentives

Tax shifts directly change customer behavior: Korea’s top corporate tax remains 25% and changes to insurance tax deductibility, capital gains or dividend tax rates can prompt customers to favor holding structures or tax-advantaged products; incentives for retirement/protection products (eg IRP/IRAs) historically lift demand, while adverse reforms can compress Meritz’s margins and reduce retained earnings and payout capacity.

- Top corporate tax: 25%

- Retirement incentives raise product sales (IRP/IRA frameworks)

- Capital gains/dividend tax changes shift customer holdings, affecting margins

Regulatory tightening and elderly poverty squeeze insurers; NPS ≈1,100T

Regulators (FSC/FSS) tighten solvency and consumer rules, raising compliance costs and limiting pricing flexibility for Meritz. Public pensions and Korea’s elderly relative poverty ~43.4% (OECD 2022) with NPS assets ≈1,100 trillion KRW (end‑2023) shape private product demand. Geopolitical risk and $1.8T GDP (World Bank 2023) amplify market volatility and funding cost swings.

| Indicator | Value |

|---|---|

| Elderly relative poverty (OECD) | 43.4% (2022) |

| National Pension Service assets | ≈1,100 trillion KRW (end‑2023) |

| GDP | $1.8 trillion (2023) |

| Top corporate tax | 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Meritz Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to its region and industry. Designed to support executives and investors with forward-looking implications for strategy and risk management.

A clean, summarized Meritz Financial Group PESTLE analysis that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and planning sessions.

Economic factors

Interest rate cycle

BOK policy rates drive Meritz Financial Group’s investment yields, reserve discounting and product guarantees; rising rates improve reinvestment yields but increase lapse and spread risks on in-force guarantees, while falling rates compress margins and strain capital for long-duration liabilities. Robust asset-liability management is pivotal to stabilize earnings through rate cycles.

Macroeconomic growth

Slowing macro growth—GDP about 2.5% in 2024 with IMF 2025 forecasts near 1.8%—pressures household income and employment (unemployment ~3.0% in 2024), reducing premium affordability and brokerage activity. Weaker corporate capex and a thinned IPO pipeline cut securities revenues and trading volumes. Slower growth elevates credit risk across investment portfolios, while Meritzs diversification across insurance, securities and asset management helps cushion cyclicality.

Inflation dynamics

Inflation (South Korea CPI 2024 ~2.6%) pushes up claims costs and operating expenses, notably in non-life lines where medical and repair costs have risen. Pricing adequacy for Meritz depends on timely rate adjustments and strict underwriting to protect margins. Inflation alters discount rates and technical reserve valuations as the Bank of Korea policy rate stood near 3.5% (mid‑2025). Active hedging and cost productivity programs help mitigate erosion.

Capital markets volatility

Capital markets volatility directly affects Meritz through fee, trading and AUM-based revenues; 2024 saw elevated market nervousness (VIX averaged about 17), increasing mark-to-market swings under IFRS and quarterly earnings variability. Insurer-sector ROE volatility moved several percentage points in 2024, while liquidity squeezes raised short-term funding spreads by roughly 80–120 bps, heightening funding costs and lapse risk; disciplined investment policies and explicit risk budgets boost resilience.

- Equity/bond swings: revenue sensitivity

- IFRS mark-to-market: earnings variability

- Liquidity: +80–120 bps funding spread

- Mitigation: balanced investments, risk budgets

Household leverage & housing

Korean household debt exceeded 1,900 trillion KRW (Bank of Korea, 2024), and property cycles materially affect Meritz Financial Group’s credit quality and customer spending on protection and savings products. Mortgage tightening and rising DSRs have reduced ancillary financial activity and refinancing, while wealth effects from property/equity moves sway asset management inflows. Stress tests must include lapse and claims sensitivity to housing-led credit shocks.

- household-debt: >1,900 trillion KRW (BOK 2024)

- mortgage-tightening: lowers ancillary revenue

- wealth-effect: drives AM inflows/outflows

- stress-scenarios: lapse & claims sensitivity

Regulatory tightening and elderly poverty squeeze insurers; NPS ≈1,100T

BOK policy (~3.5% mid‑2025) drives reinvestment yields and reserve discounting; rate swings raise lapse/spread risks while lower rates compress margins. GDP ~2.5% (2024) with IMF 2025 ~1.8% and CPI ~2.6% (2024) weaken premium affordability; household debt >1,900 trn KRW amplifies credit/lapse exposure. Capital-market volatility (funding spreads +80–120bps) increases earnings volatility.

| Metric | Value |

|---|---|

| BOK policy rate | ~3.5% (mid‑2025) |

| GDP | 2.5% (2024) / 1.8% (IMF 2025) |

| CPI | ~2.6% (2024) |

| Household debt | >1,900 trn KRW (2024) |

| Funding spread | +80–120 bps |

What You See Is What You Get

Meritz Financial Group PESTLE Analysis

This Meritz Financial Group PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase—ready to use with no placeholders. The content, structure, and layout shown are identical to the downloadable file. You’ll get the same professional, final report immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our targeted PESTLE Analysis of Meritz Financial Group—three concise sections reveal how political, economic, social, technological, legal, and environmental forces will shape its trajectory. Ideal for investors and strategists seeking fast, actionable intelligence. Purchase the full report to access in-depth scenarios, data-driven risks, and growth opportunities ready for immediate use.

Political factors

Regulatory stance in Korea

Korea’s Financial Services Commission and Financial Supervisory Service set capital, product and conduct rules that directly shape Meritz Financial Group’s insurance, brokerage and asset-management operations. Recent policy emphasis on solvency and consumer protection has increased compliance scope and costs. Variations in supervisory intensity constrain pricing flexibility and growth prospects. Ongoing close engagement is essential for approvals and innovation pilots.

Government healthcare & pensions

Public pension and health systems shape demand for Meritz Financial Group’s private life and health products, with Korea’s elderly relative poverty at about 43.4% (OECD, 2022) underscoring gaps private insurers can fill. Reforms to coverage, premiums or retirement age can redirect savings into or away from private solutions; National Pension Service assets exceeded roughly 1,100 trillion KRW by end-2023, affecting market flows. Sudden policy shifts risk disrupting product portfolios and persistency, creating both threat and opportunity.

Geopolitical risks & peninsula security

Inter-Korean tensions and regional great-power competition amplify market volatility and depress risk appetite, with South Korea a $1.8 trillion economy (World Bank, 2023). Insurance claims, asset values and funding costs can move rapidly under stress, as seen in episodic Korean credit spread widenings. Political-risk hedging and scenario planning are crucial to protect Meritz capital, while investor sentiment toward Korean financials can swing sharply with headline risk.

Industrial policy & digital finance

National pushes for digitalization and the data economy—Korea rolled out open banking in 2019 and expanded regulatory sandboxes under the Financial Services Commission—favor fintech partnerships and regtech adoption, enabling faster product digitization for groups like Meritz; fragmented standards or policy reversals, however, can stall cross-selling and platform rollouts.

- tag:sandbox expansion

- tag:open banking 2019

- tag:fintech partnerships

- tag:policy risk

Tax policy & incentives

Tax shifts directly change customer behavior: Korea’s top corporate tax remains 25% and changes to insurance tax deductibility, capital gains or dividend tax rates can prompt customers to favor holding structures or tax-advantaged products; incentives for retirement/protection products (eg IRP/IRAs) historically lift demand, while adverse reforms can compress Meritz’s margins and reduce retained earnings and payout capacity.

- Top corporate tax: 25%

- Retirement incentives raise product sales (IRP/IRA frameworks)

- Capital gains/dividend tax changes shift customer holdings, affecting margins

Regulatory tightening and elderly poverty squeeze insurers; NPS ≈1,100T

Regulators (FSC/FSS) tighten solvency and consumer rules, raising compliance costs and limiting pricing flexibility for Meritz. Public pensions and Korea’s elderly relative poverty ~43.4% (OECD 2022) with NPS assets ≈1,100 trillion KRW (end‑2023) shape private product demand. Geopolitical risk and $1.8T GDP (World Bank 2023) amplify market volatility and funding cost swings.

| Indicator | Value |

|---|---|

| Elderly relative poverty (OECD) | 43.4% (2022) |

| National Pension Service assets | ≈1,100 trillion KRW (end‑2023) |

| GDP | $1.8 trillion (2023) |

| Top corporate tax | 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Meritz Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to its region and industry. Designed to support executives and investors with forward-looking implications for strategy and risk management.

A clean, summarized Meritz Financial Group PESTLE analysis that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and planning sessions.

Economic factors

Interest rate cycle

BOK policy rates drive Meritz Financial Group’s investment yields, reserve discounting and product guarantees; rising rates improve reinvestment yields but increase lapse and spread risks on in-force guarantees, while falling rates compress margins and strain capital for long-duration liabilities. Robust asset-liability management is pivotal to stabilize earnings through rate cycles.

Macroeconomic growth

Slowing macro growth—GDP about 2.5% in 2024 with IMF 2025 forecasts near 1.8%—pressures household income and employment (unemployment ~3.0% in 2024), reducing premium affordability and brokerage activity. Weaker corporate capex and a thinned IPO pipeline cut securities revenues and trading volumes. Slower growth elevates credit risk across investment portfolios, while Meritzs diversification across insurance, securities and asset management helps cushion cyclicality.

Inflation dynamics

Inflation (South Korea CPI 2024 ~2.6%) pushes up claims costs and operating expenses, notably in non-life lines where medical and repair costs have risen. Pricing adequacy for Meritz depends on timely rate adjustments and strict underwriting to protect margins. Inflation alters discount rates and technical reserve valuations as the Bank of Korea policy rate stood near 3.5% (mid‑2025). Active hedging and cost productivity programs help mitigate erosion.

Capital markets volatility

Capital markets volatility directly affects Meritz through fee, trading and AUM-based revenues; 2024 saw elevated market nervousness (VIX averaged about 17), increasing mark-to-market swings under IFRS and quarterly earnings variability. Insurer-sector ROE volatility moved several percentage points in 2024, while liquidity squeezes raised short-term funding spreads by roughly 80–120 bps, heightening funding costs and lapse risk; disciplined investment policies and explicit risk budgets boost resilience.

- Equity/bond swings: revenue sensitivity

- IFRS mark-to-market: earnings variability

- Liquidity: +80–120 bps funding spread

- Mitigation: balanced investments, risk budgets

Household leverage & housing

Korean household debt exceeded 1,900 trillion KRW (Bank of Korea, 2024), and property cycles materially affect Meritz Financial Group’s credit quality and customer spending on protection and savings products. Mortgage tightening and rising DSRs have reduced ancillary financial activity and refinancing, while wealth effects from property/equity moves sway asset management inflows. Stress tests must include lapse and claims sensitivity to housing-led credit shocks.

- household-debt: >1,900 trillion KRW (BOK 2024)

- mortgage-tightening: lowers ancillary revenue

- wealth-effect: drives AM inflows/outflows

- stress-scenarios: lapse & claims sensitivity

Regulatory tightening and elderly poverty squeeze insurers; NPS ≈1,100T

BOK policy (~3.5% mid‑2025) drives reinvestment yields and reserve discounting; rate swings raise lapse/spread risks while lower rates compress margins. GDP ~2.5% (2024) with IMF 2025 ~1.8% and CPI ~2.6% (2024) weaken premium affordability; household debt >1,900 trn KRW amplifies credit/lapse exposure. Capital-market volatility (funding spreads +80–120bps) increases earnings volatility.

| Metric | Value |

|---|---|

| BOK policy rate | ~3.5% (mid‑2025) |

| GDP | 2.5% (2024) / 1.8% (IMF 2025) |

| CPI | ~2.6% (2024) |

| Household debt | >1,900 trn KRW (2024) |

| Funding spread | +80–120 bps |

What You See Is What You Get

Meritz Financial Group PESTLE Analysis

This Meritz Financial Group PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase—ready to use with no placeholders. The content, structure, and layout shown are identical to the downloadable file. You’ll get the same professional, final report immediately after checkout.