Metcash Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

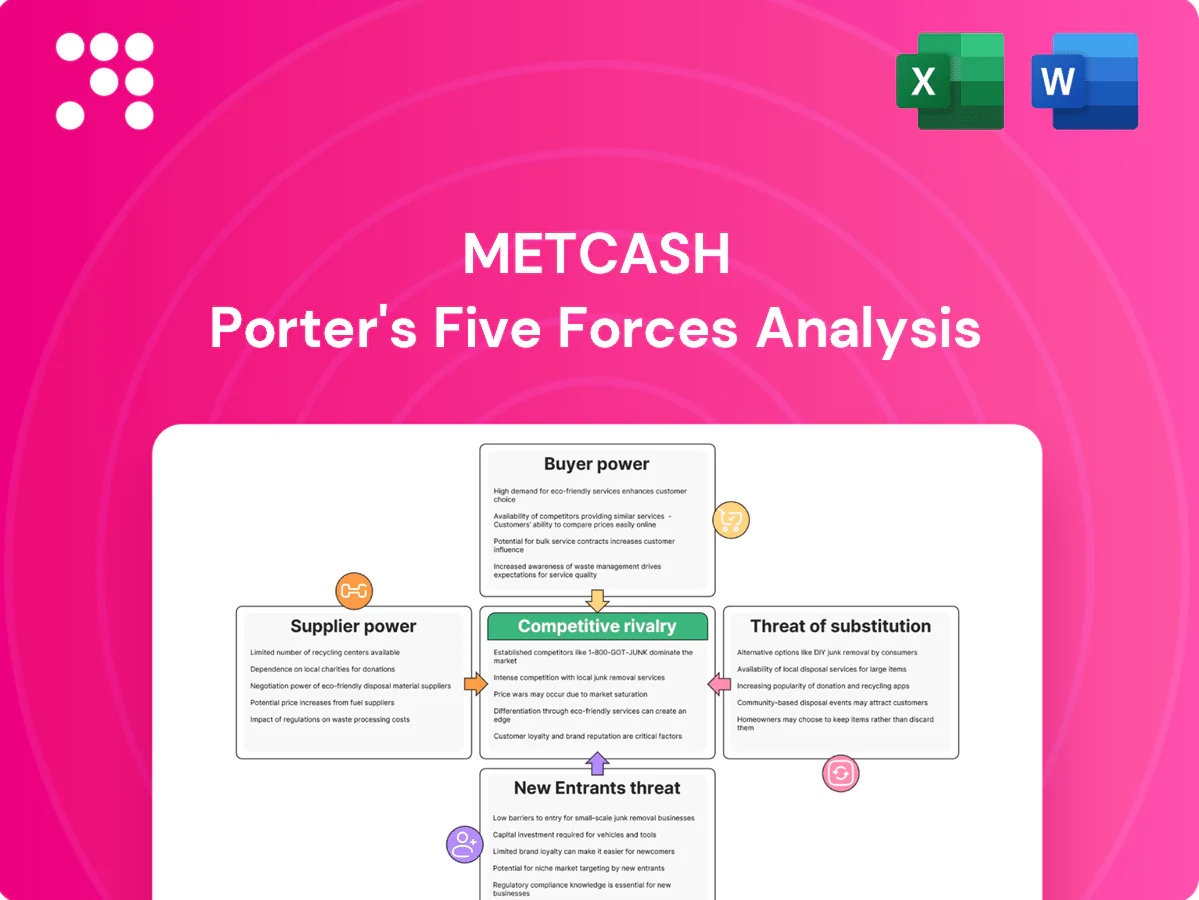

Metcash faces intense buyer power, concentrated retail competition, and steady supplier negotiation pressure, while barriers to entry and substitutes shape margin resilience; strategic positioning hinges on scale and distribution strengths. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Metcash’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier concentration

Branded FMCG, liquor and hardware categories are dominated by a few global and local majors, giving those suppliers greater leverage on price and terms. Icon brands are often must‑stock, constraining Metcash’s ability to delist. As of 2024 Metcash aggregates volume across thousands of independent retailers to counterbalance this concentration. Scale buying and joint business plans partially neutralize supplier power.

Private label leverage

Expanding private label and exclusive brands give Metcash credible alternatives to power brands, reducing dependence on national suppliers and improving margins; Metcash supplies around 8,000 independent retailers in Australia and New Zealand, so own-brand leverage scales across its network. This creates switching options and negotiation leverage, with suppliers facing real risk of shelf-space reallocation if terms are unfavorable.

Multi-sourcing options

For many categories Metcash can tender across multiple regional and international suppliers, with import substitution and parallel sourcing constraining supplier pricing; Metcash supplies over 4,000 independent retailers in Australia (2024). Fresh produce and some hardware lines remain highly fragmented, further diluting supplier power. Strategic sourcing hubs and distribution centres increase flexibility and resilience.

Logistics and data access

Metcash’s broad distribution footprint and cold-chain capability, serving around 5,000 retail outlets in 2024, plus granular POS and loyalty data, make its network strategically valuable to suppliers and incentivise trading on cooperative terms.

Joint promotions and collaborative demand-planning reduce suppliers’ sales volatility and inventory costs, while mutual dependency on shelf space and logistics capacity tempers supplier bargaining power.

- Network: ~5,000 outlets (2024)

- Cold-chain: national DCs with chilled/frozen capability

- Data: POS/loyalty analytics driving joint promos

- Effect: lower supplier price pressure, higher collaboration

Contracting and risk-sharing

Long-term agreements, rebates and service-level KPIs align supplier incentives and reduce spot exposure; penalties for non-performance and volume commitments standardise terms so suppliers get predictable offtake while Metcash gains price certainty. Structured contracts cut ad-hoc power plays and stabilise margins across Metcash’s FY2024 wholesale network.

- Long-term contracts: secure volumes

- Rebates & KPIs: align performance

- Penalties & commitments: standardise terms

- Outcome: predictable offtake for suppliers, price certainty for Metcash

Distributor scale, private label and contracts blunt supplier power across FMCG, liquor and hardware

Branded FMCG, liquor and hardware are concentrated among a few majors, giving suppliers pricing leverage and must‑stock icons. Metcash offsets this via scale aggregation, private‑label expansion and long‑term contracts—supplying ~5,000 outlets in 2024 and leveraging an ~8,000‑store ANZ network. Joint promotions, POS/loyalty data and multi‑sourcing materially temper supplier bargaining power.

What is included in the product

Tailored Porter's Five Forces analysis for Metcash that uncovers competitive drivers, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptors threatening market share, delivered in fully editable Word format for integration into reports and strategy decks.

One-sheet Metcash Porter's Five Forces summary that instantly highlights competitive pressures with an editable spider chart—perfect for quick, deck-ready decisions; customize force levels, swap in your data, and integrate seamlessly into Excel dashboards without macros.

Customers Bargaining Power

Fragmented independents

Metcash supplies roughly 3,500 independent retailers, so no single customer exerts significant leverage; the largest banner groups still represent a minority of group sales. Individual stores have limited scale but face high switching costs from supply, merchandising and IT integration. Banner programs like IGA, Cellarbrations and Mitre 10 aggregate buying influence yet operate largely inside Metcash’s ecosystem. This fragmentation moderates overall buyer power.

Thin margins, high price sensitivity

Independent retailers operate on razor-thin margins—often below 3% in 2024—and aggressively push for sharp buy-ins, rebates and promo support to protect profitability. High price elasticity in commoditised lines amplifies buyer pressure, with price often the deciding factor for customers. Metcash, supplying roughly 1,400 independent supermarkets, must defend value through superior service, tailored range and promotional funding to sustain topline and margin.

Value-added services lock-in

Metcash embeds logistics, IT, planograms and marketing support into operations across c.12,000 independent stores, and FY24 group sales of about A$14.4bn, creating operational dependence that raises switching costs beyond price. The potential loss of rebates, proprietary systems and scale purchasing deals deters multi-homing. Deep service integration reduces buyer bargaining leverage and weakens pure price-based negotiation.

Alternative wholesale channels

Rival wholesalers and direct-sourcing options in liquor and hardware—plus larger independents that can partially self- or dual-source—raise buyer power at the margin; Metcash still supplies over 5,000 independent retailers across its banners. Metcash defends margins through bundle economics, category exclusivities and private-label programs across IGA and Mitre 10.

- Over 5,000 independent retailers supplied

- Dual-sourcing raises marginal buyer leverage

- Bundle economics and exclusivities reduce churn

Local exclusivities and community fit

Banner and territory arrangements give semi-exclusive catchments across Metcash's network of over 3,400 independent outlets, boosting community-focused format loyalty and higher repeat rates in regional markets. Localized ranging and tailored support from Metcash's FY2024 programs are hard to replicate, embedding local advantage and softening buyers' negotiating stance.

- semi-exclusive territories

- 3,400+ independent outlets (2024)

- localized ranging increases loyalty

Indie retailers cut buyer power; banners and A$14.4bn scale raise costs

Metcash supplies c.5,000 independent retailers and c.3,400+ outlet banners (FY24), diluting single-customer leverage while banner aggregation (IGA, Mitre 10) concentrates buying influence. Retailers operate on sub-3% margins (2024) and push for rebates and promos, raising price pressure on commoditised lines. Deep logistics, IT and territory protections (FY24 A$14.4bn group sales) raise switching costs and moderate buyer power.

| Metric | 2024 |

|---|---|

| Group sales | A$14.4bn |

| Independent retailers supplied | c.5,000 |

| Outlet banners | 3,400+ |

| Typical retailer margin | <3% |

Preview Before You Purchase

Metcash Porter's Five Forces Analysis

This preview is the exact Metcash Porter’s Five Forces Analysis you’ll receive after purchase—fully written, formatted and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of entry and substitutes with actionable insights. No samples or placeholders; buy and download this same file instantly.

Go Beyond the Preview—Access the Full Strategic Report

Metcash faces intense buyer power, concentrated retail competition, and steady supplier negotiation pressure, while barriers to entry and substitutes shape margin resilience; strategic positioning hinges on scale and distribution strengths. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Metcash’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier concentration

Branded FMCG, liquor and hardware categories are dominated by a few global and local majors, giving those suppliers greater leverage on price and terms. Icon brands are often must‑stock, constraining Metcash’s ability to delist. As of 2024 Metcash aggregates volume across thousands of independent retailers to counterbalance this concentration. Scale buying and joint business plans partially neutralize supplier power.

Private label leverage

Expanding private label and exclusive brands give Metcash credible alternatives to power brands, reducing dependence on national suppliers and improving margins; Metcash supplies around 8,000 independent retailers in Australia and New Zealand, so own-brand leverage scales across its network. This creates switching options and negotiation leverage, with suppliers facing real risk of shelf-space reallocation if terms are unfavorable.

Multi-sourcing options

For many categories Metcash can tender across multiple regional and international suppliers, with import substitution and parallel sourcing constraining supplier pricing; Metcash supplies over 4,000 independent retailers in Australia (2024). Fresh produce and some hardware lines remain highly fragmented, further diluting supplier power. Strategic sourcing hubs and distribution centres increase flexibility and resilience.

Logistics and data access

Metcash’s broad distribution footprint and cold-chain capability, serving around 5,000 retail outlets in 2024, plus granular POS and loyalty data, make its network strategically valuable to suppliers and incentivise trading on cooperative terms.

Joint promotions and collaborative demand-planning reduce suppliers’ sales volatility and inventory costs, while mutual dependency on shelf space and logistics capacity tempers supplier bargaining power.

- Network: ~5,000 outlets (2024)

- Cold-chain: national DCs with chilled/frozen capability

- Data: POS/loyalty analytics driving joint promos

- Effect: lower supplier price pressure, higher collaboration

Contracting and risk-sharing

Long-term agreements, rebates and service-level KPIs align supplier incentives and reduce spot exposure; penalties for non-performance and volume commitments standardise terms so suppliers get predictable offtake while Metcash gains price certainty. Structured contracts cut ad-hoc power plays and stabilise margins across Metcash’s FY2024 wholesale network.

- Long-term contracts: secure volumes

- Rebates & KPIs: align performance

- Penalties & commitments: standardise terms

- Outcome: predictable offtake for suppliers, price certainty for Metcash

Distributor scale, private label and contracts blunt supplier power across FMCG, liquor and hardware

Branded FMCG, liquor and hardware are concentrated among a few majors, giving suppliers pricing leverage and must‑stock icons. Metcash offsets this via scale aggregation, private‑label expansion and long‑term contracts—supplying ~5,000 outlets in 2024 and leveraging an ~8,000‑store ANZ network. Joint promotions, POS/loyalty data and multi‑sourcing materially temper supplier bargaining power.

What is included in the product

Tailored Porter's Five Forces analysis for Metcash that uncovers competitive drivers, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptors threatening market share, delivered in fully editable Word format for integration into reports and strategy decks.

One-sheet Metcash Porter's Five Forces summary that instantly highlights competitive pressures with an editable spider chart—perfect for quick, deck-ready decisions; customize force levels, swap in your data, and integrate seamlessly into Excel dashboards without macros.

Customers Bargaining Power

Fragmented independents

Metcash supplies roughly 3,500 independent retailers, so no single customer exerts significant leverage; the largest banner groups still represent a minority of group sales. Individual stores have limited scale but face high switching costs from supply, merchandising and IT integration. Banner programs like IGA, Cellarbrations and Mitre 10 aggregate buying influence yet operate largely inside Metcash’s ecosystem. This fragmentation moderates overall buyer power.

Thin margins, high price sensitivity

Independent retailers operate on razor-thin margins—often below 3% in 2024—and aggressively push for sharp buy-ins, rebates and promo support to protect profitability. High price elasticity in commoditised lines amplifies buyer pressure, with price often the deciding factor for customers. Metcash, supplying roughly 1,400 independent supermarkets, must defend value through superior service, tailored range and promotional funding to sustain topline and margin.

Value-added services lock-in

Metcash embeds logistics, IT, planograms and marketing support into operations across c.12,000 independent stores, and FY24 group sales of about A$14.4bn, creating operational dependence that raises switching costs beyond price. The potential loss of rebates, proprietary systems and scale purchasing deals deters multi-homing. Deep service integration reduces buyer bargaining leverage and weakens pure price-based negotiation.

Alternative wholesale channels

Rival wholesalers and direct-sourcing options in liquor and hardware—plus larger independents that can partially self- or dual-source—raise buyer power at the margin; Metcash still supplies over 5,000 independent retailers across its banners. Metcash defends margins through bundle economics, category exclusivities and private-label programs across IGA and Mitre 10.

- Over 5,000 independent retailers supplied

- Dual-sourcing raises marginal buyer leverage

- Bundle economics and exclusivities reduce churn

Local exclusivities and community fit

Banner and territory arrangements give semi-exclusive catchments across Metcash's network of over 3,400 independent outlets, boosting community-focused format loyalty and higher repeat rates in regional markets. Localized ranging and tailored support from Metcash's FY2024 programs are hard to replicate, embedding local advantage and softening buyers' negotiating stance.

- semi-exclusive territories

- 3,400+ independent outlets (2024)

- localized ranging increases loyalty

Indie retailers cut buyer power; banners and A$14.4bn scale raise costs

Metcash supplies c.5,000 independent retailers and c.3,400+ outlet banners (FY24), diluting single-customer leverage while banner aggregation (IGA, Mitre 10) concentrates buying influence. Retailers operate on sub-3% margins (2024) and push for rebates and promos, raising price pressure on commoditised lines. Deep logistics, IT and territory protections (FY24 A$14.4bn group sales) raise switching costs and moderate buyer power.

| Metric | 2024 |

|---|---|

| Group sales | A$14.4bn |

| Independent retailers supplied | c.5,000 |

| Outlet banners | 3,400+ |

| Typical retailer margin | <3% |

Preview Before You Purchase

Metcash Porter's Five Forces Analysis

This preview is the exact Metcash Porter’s Five Forces Analysis you’ll receive after purchase—fully written, formatted and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of entry and substitutes with actionable insights. No samples or placeholders; buy and download this same file instantly.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Metcash faces intense buyer power, concentrated retail competition, and steady supplier negotiation pressure, while barriers to entry and substitutes shape margin resilience; strategic positioning hinges on scale and distribution strengths. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Metcash’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier concentration

Branded FMCG, liquor and hardware categories are dominated by a few global and local majors, giving those suppliers greater leverage on price and terms. Icon brands are often must‑stock, constraining Metcash’s ability to delist. As of 2024 Metcash aggregates volume across thousands of independent retailers to counterbalance this concentration. Scale buying and joint business plans partially neutralize supplier power.

Private label leverage

Expanding private label and exclusive brands give Metcash credible alternatives to power brands, reducing dependence on national suppliers and improving margins; Metcash supplies around 8,000 independent retailers in Australia and New Zealand, so own-brand leverage scales across its network. This creates switching options and negotiation leverage, with suppliers facing real risk of shelf-space reallocation if terms are unfavorable.

Multi-sourcing options

For many categories Metcash can tender across multiple regional and international suppliers, with import substitution and parallel sourcing constraining supplier pricing; Metcash supplies over 4,000 independent retailers in Australia (2024). Fresh produce and some hardware lines remain highly fragmented, further diluting supplier power. Strategic sourcing hubs and distribution centres increase flexibility and resilience.

Logistics and data access

Metcash’s broad distribution footprint and cold-chain capability, serving around 5,000 retail outlets in 2024, plus granular POS and loyalty data, make its network strategically valuable to suppliers and incentivise trading on cooperative terms.

Joint promotions and collaborative demand-planning reduce suppliers’ sales volatility and inventory costs, while mutual dependency on shelf space and logistics capacity tempers supplier bargaining power.

- Network: ~5,000 outlets (2024)

- Cold-chain: national DCs with chilled/frozen capability

- Data: POS/loyalty analytics driving joint promos

- Effect: lower supplier price pressure, higher collaboration

Contracting and risk-sharing

Long-term agreements, rebates and service-level KPIs align supplier incentives and reduce spot exposure; penalties for non-performance and volume commitments standardise terms so suppliers get predictable offtake while Metcash gains price certainty. Structured contracts cut ad-hoc power plays and stabilise margins across Metcash’s FY2024 wholesale network.

- Long-term contracts: secure volumes

- Rebates & KPIs: align performance

- Penalties & commitments: standardise terms

- Outcome: predictable offtake for suppliers, price certainty for Metcash

Distributor scale, private label and contracts blunt supplier power across FMCG, liquor and hardware

Branded FMCG, liquor and hardware are concentrated among a few majors, giving suppliers pricing leverage and must‑stock icons. Metcash offsets this via scale aggregation, private‑label expansion and long‑term contracts—supplying ~5,000 outlets in 2024 and leveraging an ~8,000‑store ANZ network. Joint promotions, POS/loyalty data and multi‑sourcing materially temper supplier bargaining power.

What is included in the product

Tailored Porter's Five Forces analysis for Metcash that uncovers competitive drivers, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and substitutes or disruptors threatening market share, delivered in fully editable Word format for integration into reports and strategy decks.

One-sheet Metcash Porter's Five Forces summary that instantly highlights competitive pressures with an editable spider chart—perfect for quick, deck-ready decisions; customize force levels, swap in your data, and integrate seamlessly into Excel dashboards without macros.

Customers Bargaining Power

Fragmented independents

Metcash supplies roughly 3,500 independent retailers, so no single customer exerts significant leverage; the largest banner groups still represent a minority of group sales. Individual stores have limited scale but face high switching costs from supply, merchandising and IT integration. Banner programs like IGA, Cellarbrations and Mitre 10 aggregate buying influence yet operate largely inside Metcash’s ecosystem. This fragmentation moderates overall buyer power.

Thin margins, high price sensitivity

Independent retailers operate on razor-thin margins—often below 3% in 2024—and aggressively push for sharp buy-ins, rebates and promo support to protect profitability. High price elasticity in commoditised lines amplifies buyer pressure, with price often the deciding factor for customers. Metcash, supplying roughly 1,400 independent supermarkets, must defend value through superior service, tailored range and promotional funding to sustain topline and margin.

Value-added services lock-in

Metcash embeds logistics, IT, planograms and marketing support into operations across c.12,000 independent stores, and FY24 group sales of about A$14.4bn, creating operational dependence that raises switching costs beyond price. The potential loss of rebates, proprietary systems and scale purchasing deals deters multi-homing. Deep service integration reduces buyer bargaining leverage and weakens pure price-based negotiation.

Alternative wholesale channels

Rival wholesalers and direct-sourcing options in liquor and hardware—plus larger independents that can partially self- or dual-source—raise buyer power at the margin; Metcash still supplies over 5,000 independent retailers across its banners. Metcash defends margins through bundle economics, category exclusivities and private-label programs across IGA and Mitre 10.

- Over 5,000 independent retailers supplied

- Dual-sourcing raises marginal buyer leverage

- Bundle economics and exclusivities reduce churn

Local exclusivities and community fit

Banner and territory arrangements give semi-exclusive catchments across Metcash's network of over 3,400 independent outlets, boosting community-focused format loyalty and higher repeat rates in regional markets. Localized ranging and tailored support from Metcash's FY2024 programs are hard to replicate, embedding local advantage and softening buyers' negotiating stance.

- semi-exclusive territories

- 3,400+ independent outlets (2024)

- localized ranging increases loyalty

Indie retailers cut buyer power; banners and A$14.4bn scale raise costs

Metcash supplies c.5,000 independent retailers and c.3,400+ outlet banners (FY24), diluting single-customer leverage while banner aggregation (IGA, Mitre 10) concentrates buying influence. Retailers operate on sub-3% margins (2024) and push for rebates and promos, raising price pressure on commoditised lines. Deep logistics, IT and territory protections (FY24 A$14.4bn group sales) raise switching costs and moderate buyer power.

| Metric | 2024 |

|---|---|

| Group sales | A$14.4bn |

| Independent retailers supplied | c.5,000 |

| Outlet banners | 3,400+ |

| Typical retailer margin | <3% |

Preview Before You Purchase

Metcash Porter's Five Forces Analysis

This preview is the exact Metcash Porter’s Five Forces Analysis you’ll receive after purchase—fully written, formatted and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of entry and substitutes with actionable insights. No samples or placeholders; buy and download this same file instantly.