Metro SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Metro’s SWOT analysis highlights its operational strengths, competitive vulnerabilities, and strategic opportunities across retail and wholesale channels. Our summary surfaces key risks and growth drivers, but the full report delivers detailed, research-backed insights and financial context. Purchase the complete SWOT to get a professionally formatted Word report plus an editable Excel matrix for planning and investor-ready presentations.

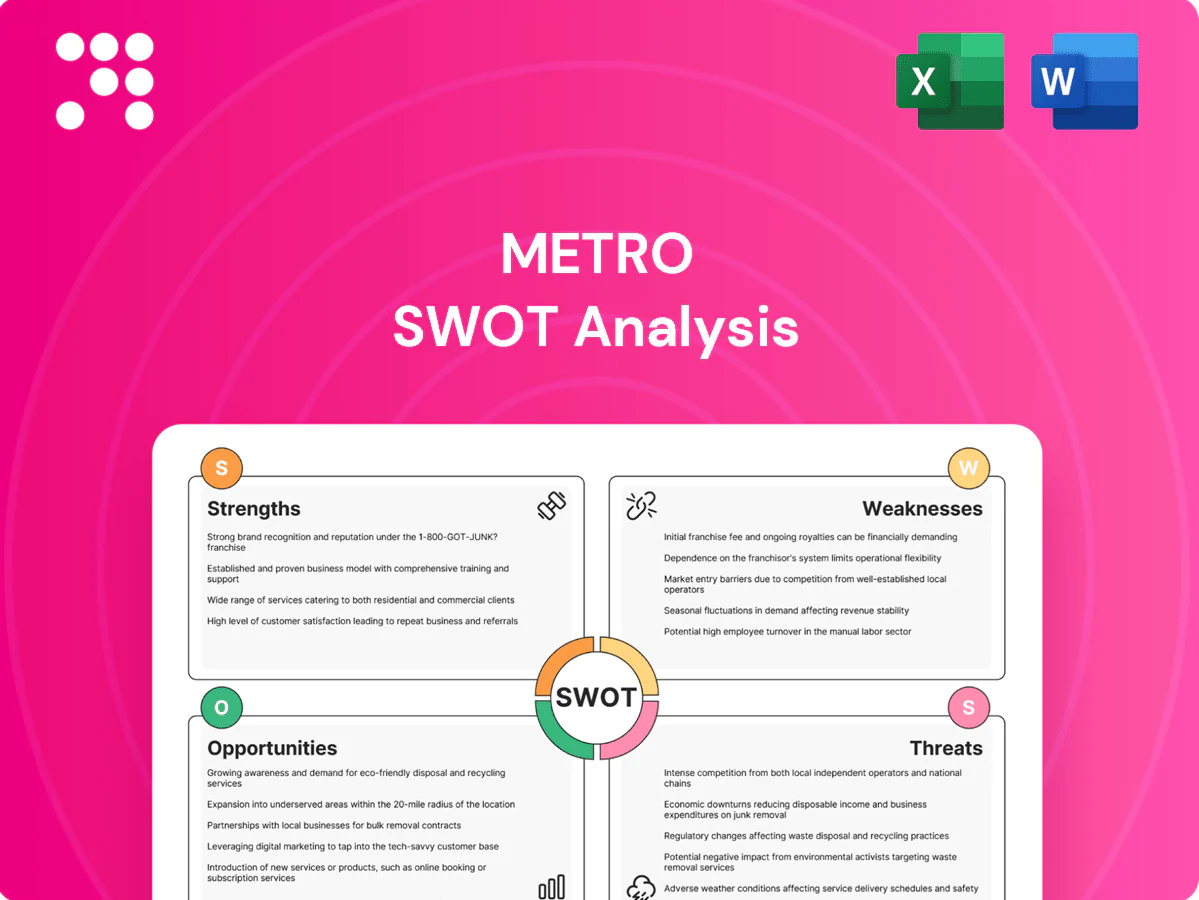

Strengths

Regional market leadership in Quebec and Ontario

Metro holds roughly 40% market share in Quebec and is a top-three grocer in Ontario, backed by strong brand recognition and local loyalty. Its dense network of over 1,000 stores drives foot traffic, scale economies and supplier bargaining power. Grocery demand remains resilient and non-discretionary across cycles. Local merchandising and community presence reinforce customer retention and regional insights.

Diversified banners across supermarkets, discount, and drugstores

Metro’s portfolio spans conventional Metro, discount Food Basics and Jean Coutu pharmacies, covering value to premium price points across over 1,000 stores. Cross-traffic between grocery and pharmacy missions boosts basket depth and frequency, with pharmacy items often raising average ticket by double-digit percentages. Revenue mix—roughly CA$22.5B in 2024—smooths category cyclicality and banners can be tailored to local demographics by format and assortment.

Integrated retail, distribution, and franchising model

Metro’s vertical integration links centralized procurement, national distribution centers and in-store operations across more than 750 wholesale and retail outlets in 34 countries, lowering logistics costs and speeding product flow to improve freshness and availability. Franchising enables capital-light expansion and aligns local entrepreneurs with brand standards, accelerating openings without heavy capex. Scale in procurement and logistics delivers buying power and route optimization, supporting higher inventory turns and stronger retail margins.

Strong private-label and loyalty capabilities

Metro’s strong private-label offering boosts gross margins by allowing higher-margin penetration and clear product differentiation versus national brands, while pricing flexibility supports targeted value positioning.

The loyalty program and targeted promotions drive repeat purchases and larger basket sizes; customer data enables localized assortments and assortment optimization.

Operational efficiency and resilient supply chain

- Distribution centers: automation, category mgmt

- Shrink control: planograms, replenishment accuracy

- Cold-chain: reliable supplier network

- Cost discipline: stable cash flows

Quebec grocery leader: ~40% share, 1,000+ stores, CA$22.5B

Metro holds ~40% share in Quebec and is top-three in Ontario, operating 1,000+ stores and generating CA$22.5B revenue in 2024. Dense network and centralized distribution drive scale, private-label growth and margin expansion. Loyalty program and data enable localized assortments and larger basket sizes. Automated DCs and cold-chain reduce shrink and stabilize cash flow.

| Metric | Value |

|---|---|

| Stores | 1,000+ |

| 2024 Revenue | CA$22.5B |

| QC Market Share | ~40% |

What is included in the product

Delivers a strategic overview of Metro’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, and operational risks.

Delivers a compact Metro SWOT matrix that pinpoints operational and customer pain points for rapid mitigation; ideal for quick stakeholder alignment and tactical action planning.

Weaknesses

Geographic concentration risk

Metro's retail footprint is concentrated exclusively in Quebec and Ontario, meaning nearly 100% of revenue depends on these two provinces; together they account for about 61% of Canada's population. This creates exposure to region-specific economic slowdowns or regulatory changes (eg, minimum wage or grocery pricing measures) that can disproportionately hit Metro. Limited geographic diversification versus national peers constrains expansion and imposes a lower growth ceiling in saturated core markets.

Relative scale disadvantage vs. big-box and global players

Relative scale hurts Metro: rivals spend vastly more on procurement and marketing—Walmart $611B revenue (FY24), Amazon $562B (2024) and Costco $242B (FY24) versus Metro ~€37B—reducing Metro’s bargaining power and national-brand leverage. Thinner margins leave less room to absorb price wars or wage inflation, and Metro cannot match rapid, costly nationwide tech investments that big-box players fund.

Omnichannel and e-commerce depth

Metro lags leaders in online assortment depth, same‑day delivery speed and last‑mile coverage, with EU online grocery penetration at about 12% in 2024 highlighting rising customer expectations. Click‑and‑collect and home delivery remain margin‑challenged—last‑mile can represent over 50% of delivery costs—pressuring profitability. Complex legacy tech stacks and in‑store change management slow rollout of omnichannel features, while pure‑play retailers set faster delivery and UX benchmarks.

Margin exposure to discount mix and promotions

Discount banners and aggressive competitor pricing have compressed Metro’s gross margins, driving a reported margin erosion of c.150 bps in 2023–24 as the group leaned on price-led strategies to protect volumes.

Frequent promotions—needed to defend share—raise promotional spend and limit pass-through of rising input costs (food and energy inflation remained elevated into 2024), while trading-down behavior risks diluting ASP and category mix.

- promo intensity: higher frequency to defend share

- margin impact: ~150 bps compression (2023–24)

- input cost passthrough: incomplete vs. inflation

- mix risk: trading-down dilutes ASP

Labor intensity and union exposure

High store labor requirements and complex scheduling drive costs—frontline labor typically represents 10–15% of grocery sales—while union negotiations can add wage rigidity with common contract escalators of 3–5% annually, limiting flexibility. Unions increase disruption risk and can constrain productivity initiatives; compliance and pharmacy/food training impose recurring per-store administrative and certification costs.

- High labor intensity: 10–15% of sales

- Union escalators: 3–5% annually

- Disruption risk: strikes/negotiations

- Compliance/training: recurring per-store costs

Regional grocer: Quebec/Ontario ≈61%, margins down ≈150bps

Metro is regionally concentrated in Quebec and Ontario (~61% of Canada’s population), limiting national scale and exposing it to provincial shocks. Revenue (~C$19.6bn FY24) and smaller scale reduce procurement leverage versus Walmart/Costco/Amazon, squeezing margins (≈150bps erosion 2023–24). Omnichannel and last‑mile lag peers, raising fulfillment costs and capping growth.

| Metric | Value |

|---|---|

| FY24 Revenue | C$19.6bn |

| Population exposure | Quebec+Ontario ≈61% |

| Margin change | ≈-150bps (2023–24) |

| Frontline labor | 10–15% of sales |

Preview Before You Purchase

Metro SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and purchasing unlocks the complete, editable version. You’re viewing a live preview of the real file; the full, detailed report becomes available after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Metro’s SWOT analysis highlights its operational strengths, competitive vulnerabilities, and strategic opportunities across retail and wholesale channels. Our summary surfaces key risks and growth drivers, but the full report delivers detailed, research-backed insights and financial context. Purchase the complete SWOT to get a professionally formatted Word report plus an editable Excel matrix for planning and investor-ready presentations.

Strengths

Regional market leadership in Quebec and Ontario

Metro holds roughly 40% market share in Quebec and is a top-three grocer in Ontario, backed by strong brand recognition and local loyalty. Its dense network of over 1,000 stores drives foot traffic, scale economies and supplier bargaining power. Grocery demand remains resilient and non-discretionary across cycles. Local merchandising and community presence reinforce customer retention and regional insights.

Diversified banners across supermarkets, discount, and drugstores

Metro’s portfolio spans conventional Metro, discount Food Basics and Jean Coutu pharmacies, covering value to premium price points across over 1,000 stores. Cross-traffic between grocery and pharmacy missions boosts basket depth and frequency, with pharmacy items often raising average ticket by double-digit percentages. Revenue mix—roughly CA$22.5B in 2024—smooths category cyclicality and banners can be tailored to local demographics by format and assortment.

Integrated retail, distribution, and franchising model

Metro’s vertical integration links centralized procurement, national distribution centers and in-store operations across more than 750 wholesale and retail outlets in 34 countries, lowering logistics costs and speeding product flow to improve freshness and availability. Franchising enables capital-light expansion and aligns local entrepreneurs with brand standards, accelerating openings without heavy capex. Scale in procurement and logistics delivers buying power and route optimization, supporting higher inventory turns and stronger retail margins.

Strong private-label and loyalty capabilities

Metro’s strong private-label offering boosts gross margins by allowing higher-margin penetration and clear product differentiation versus national brands, while pricing flexibility supports targeted value positioning.

The loyalty program and targeted promotions drive repeat purchases and larger basket sizes; customer data enables localized assortments and assortment optimization.

Operational efficiency and resilient supply chain

- Distribution centers: automation, category mgmt

- Shrink control: planograms, replenishment accuracy

- Cold-chain: reliable supplier network

- Cost discipline: stable cash flows

Quebec grocery leader: ~40% share, 1,000+ stores, CA$22.5B

Metro holds ~40% share in Quebec and is top-three in Ontario, operating 1,000+ stores and generating CA$22.5B revenue in 2024. Dense network and centralized distribution drive scale, private-label growth and margin expansion. Loyalty program and data enable localized assortments and larger basket sizes. Automated DCs and cold-chain reduce shrink and stabilize cash flow.

| Metric | Value |

|---|---|

| Stores | 1,000+ |

| 2024 Revenue | CA$22.5B |

| QC Market Share | ~40% |

What is included in the product

Delivers a strategic overview of Metro’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, and operational risks.

Delivers a compact Metro SWOT matrix that pinpoints operational and customer pain points for rapid mitigation; ideal for quick stakeholder alignment and tactical action planning.

Weaknesses

Geographic concentration risk

Metro's retail footprint is concentrated exclusively in Quebec and Ontario, meaning nearly 100% of revenue depends on these two provinces; together they account for about 61% of Canada's population. This creates exposure to region-specific economic slowdowns or regulatory changes (eg, minimum wage or grocery pricing measures) that can disproportionately hit Metro. Limited geographic diversification versus national peers constrains expansion and imposes a lower growth ceiling in saturated core markets.

Relative scale disadvantage vs. big-box and global players

Relative scale hurts Metro: rivals spend vastly more on procurement and marketing—Walmart $611B revenue (FY24), Amazon $562B (2024) and Costco $242B (FY24) versus Metro ~€37B—reducing Metro’s bargaining power and national-brand leverage. Thinner margins leave less room to absorb price wars or wage inflation, and Metro cannot match rapid, costly nationwide tech investments that big-box players fund.

Omnichannel and e-commerce depth

Metro lags leaders in online assortment depth, same‑day delivery speed and last‑mile coverage, with EU online grocery penetration at about 12% in 2024 highlighting rising customer expectations. Click‑and‑collect and home delivery remain margin‑challenged—last‑mile can represent over 50% of delivery costs—pressuring profitability. Complex legacy tech stacks and in‑store change management slow rollout of omnichannel features, while pure‑play retailers set faster delivery and UX benchmarks.

Margin exposure to discount mix and promotions

Discount banners and aggressive competitor pricing have compressed Metro’s gross margins, driving a reported margin erosion of c.150 bps in 2023–24 as the group leaned on price-led strategies to protect volumes.

Frequent promotions—needed to defend share—raise promotional spend and limit pass-through of rising input costs (food and energy inflation remained elevated into 2024), while trading-down behavior risks diluting ASP and category mix.

- promo intensity: higher frequency to defend share

- margin impact: ~150 bps compression (2023–24)

- input cost passthrough: incomplete vs. inflation

- mix risk: trading-down dilutes ASP

Labor intensity and union exposure

High store labor requirements and complex scheduling drive costs—frontline labor typically represents 10–15% of grocery sales—while union negotiations can add wage rigidity with common contract escalators of 3–5% annually, limiting flexibility. Unions increase disruption risk and can constrain productivity initiatives; compliance and pharmacy/food training impose recurring per-store administrative and certification costs.

- High labor intensity: 10–15% of sales

- Union escalators: 3–5% annually

- Disruption risk: strikes/negotiations

- Compliance/training: recurring per-store costs

Regional grocer: Quebec/Ontario ≈61%, margins down ≈150bps

Metro is regionally concentrated in Quebec and Ontario (~61% of Canada’s population), limiting national scale and exposing it to provincial shocks. Revenue (~C$19.6bn FY24) and smaller scale reduce procurement leverage versus Walmart/Costco/Amazon, squeezing margins (≈150bps erosion 2023–24). Omnichannel and last‑mile lag peers, raising fulfillment costs and capping growth.

| Metric | Value |

|---|---|

| FY24 Revenue | C$19.6bn |

| Population exposure | Quebec+Ontario ≈61% |

| Margin change | ≈-150bps (2023–24) |

| Frontline labor | 10–15% of sales |

Preview Before You Purchase

Metro SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and purchasing unlocks the complete, editable version. You’re viewing a live preview of the real file; the full, detailed report becomes available after checkout.

Description

Go Beyond the Preview—Access the Full Strategic Report

Metro’s SWOT analysis highlights its operational strengths, competitive vulnerabilities, and strategic opportunities across retail and wholesale channels. Our summary surfaces key risks and growth drivers, but the full report delivers detailed, research-backed insights and financial context. Purchase the complete SWOT to get a professionally formatted Word report plus an editable Excel matrix for planning and investor-ready presentations.

Strengths

Regional market leadership in Quebec and Ontario

Metro holds roughly 40% market share in Quebec and is a top-three grocer in Ontario, backed by strong brand recognition and local loyalty. Its dense network of over 1,000 stores drives foot traffic, scale economies and supplier bargaining power. Grocery demand remains resilient and non-discretionary across cycles. Local merchandising and community presence reinforce customer retention and regional insights.

Diversified banners across supermarkets, discount, and drugstores

Metro’s portfolio spans conventional Metro, discount Food Basics and Jean Coutu pharmacies, covering value to premium price points across over 1,000 stores. Cross-traffic between grocery and pharmacy missions boosts basket depth and frequency, with pharmacy items often raising average ticket by double-digit percentages. Revenue mix—roughly CA$22.5B in 2024—smooths category cyclicality and banners can be tailored to local demographics by format and assortment.

Integrated retail, distribution, and franchising model

Metro’s vertical integration links centralized procurement, national distribution centers and in-store operations across more than 750 wholesale and retail outlets in 34 countries, lowering logistics costs and speeding product flow to improve freshness and availability. Franchising enables capital-light expansion and aligns local entrepreneurs with brand standards, accelerating openings without heavy capex. Scale in procurement and logistics delivers buying power and route optimization, supporting higher inventory turns and stronger retail margins.

Strong private-label and loyalty capabilities

Metro’s strong private-label offering boosts gross margins by allowing higher-margin penetration and clear product differentiation versus national brands, while pricing flexibility supports targeted value positioning.

The loyalty program and targeted promotions drive repeat purchases and larger basket sizes; customer data enables localized assortments and assortment optimization.

Operational efficiency and resilient supply chain

- Distribution centers: automation, category mgmt

- Shrink control: planograms, replenishment accuracy

- Cold-chain: reliable supplier network

- Cost discipline: stable cash flows

Quebec grocery leader: ~40% share, 1,000+ stores, CA$22.5B

Metro holds ~40% share in Quebec and is top-three in Ontario, operating 1,000+ stores and generating CA$22.5B revenue in 2024. Dense network and centralized distribution drive scale, private-label growth and margin expansion. Loyalty program and data enable localized assortments and larger basket sizes. Automated DCs and cold-chain reduce shrink and stabilize cash flow.

| Metric | Value |

|---|---|

| Stores | 1,000+ |

| 2024 Revenue | CA$22.5B |

| QC Market Share | ~40% |

What is included in the product

Delivers a strategic overview of Metro’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, and operational risks.

Delivers a compact Metro SWOT matrix that pinpoints operational and customer pain points for rapid mitigation; ideal for quick stakeholder alignment and tactical action planning.

Weaknesses

Geographic concentration risk

Metro's retail footprint is concentrated exclusively in Quebec and Ontario, meaning nearly 100% of revenue depends on these two provinces; together they account for about 61% of Canada's population. This creates exposure to region-specific economic slowdowns or regulatory changes (eg, minimum wage or grocery pricing measures) that can disproportionately hit Metro. Limited geographic diversification versus national peers constrains expansion and imposes a lower growth ceiling in saturated core markets.

Relative scale disadvantage vs. big-box and global players

Relative scale hurts Metro: rivals spend vastly more on procurement and marketing—Walmart $611B revenue (FY24), Amazon $562B (2024) and Costco $242B (FY24) versus Metro ~€37B—reducing Metro’s bargaining power and national-brand leverage. Thinner margins leave less room to absorb price wars or wage inflation, and Metro cannot match rapid, costly nationwide tech investments that big-box players fund.

Omnichannel and e-commerce depth

Metro lags leaders in online assortment depth, same‑day delivery speed and last‑mile coverage, with EU online grocery penetration at about 12% in 2024 highlighting rising customer expectations. Click‑and‑collect and home delivery remain margin‑challenged—last‑mile can represent over 50% of delivery costs—pressuring profitability. Complex legacy tech stacks and in‑store change management slow rollout of omnichannel features, while pure‑play retailers set faster delivery and UX benchmarks.

Margin exposure to discount mix and promotions

Discount banners and aggressive competitor pricing have compressed Metro’s gross margins, driving a reported margin erosion of c.150 bps in 2023–24 as the group leaned on price-led strategies to protect volumes.

Frequent promotions—needed to defend share—raise promotional spend and limit pass-through of rising input costs (food and energy inflation remained elevated into 2024), while trading-down behavior risks diluting ASP and category mix.

- promo intensity: higher frequency to defend share

- margin impact: ~150 bps compression (2023–24)

- input cost passthrough: incomplete vs. inflation

- mix risk: trading-down dilutes ASP

Labor intensity and union exposure

High store labor requirements and complex scheduling drive costs—frontline labor typically represents 10–15% of grocery sales—while union negotiations can add wage rigidity with common contract escalators of 3–5% annually, limiting flexibility. Unions increase disruption risk and can constrain productivity initiatives; compliance and pharmacy/food training impose recurring per-store administrative and certification costs.

- High labor intensity: 10–15% of sales

- Union escalators: 3–5% annually

- Disruption risk: strikes/negotiations

- Compliance/training: recurring per-store costs

Regional grocer: Quebec/Ontario ≈61%, margins down ≈150bps

Metro is regionally concentrated in Quebec and Ontario (~61% of Canada’s population), limiting national scale and exposing it to provincial shocks. Revenue (~C$19.6bn FY24) and smaller scale reduce procurement leverage versus Walmart/Costco/Amazon, squeezing margins (≈150bps erosion 2023–24). Omnichannel and last‑mile lag peers, raising fulfillment costs and capping growth.

| Metric | Value |

|---|---|

| FY24 Revenue | C$19.6bn |

| Population exposure | Quebec+Ontario ≈61% |

| Margin change | ≈-150bps (2023–24) |

| Frontline labor | 10–15% of sales |

Preview Before You Purchase

Metro SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and purchasing unlocks the complete, editable version. You’re viewing a live preview of the real file; the full, detailed report becomes available after checkout.