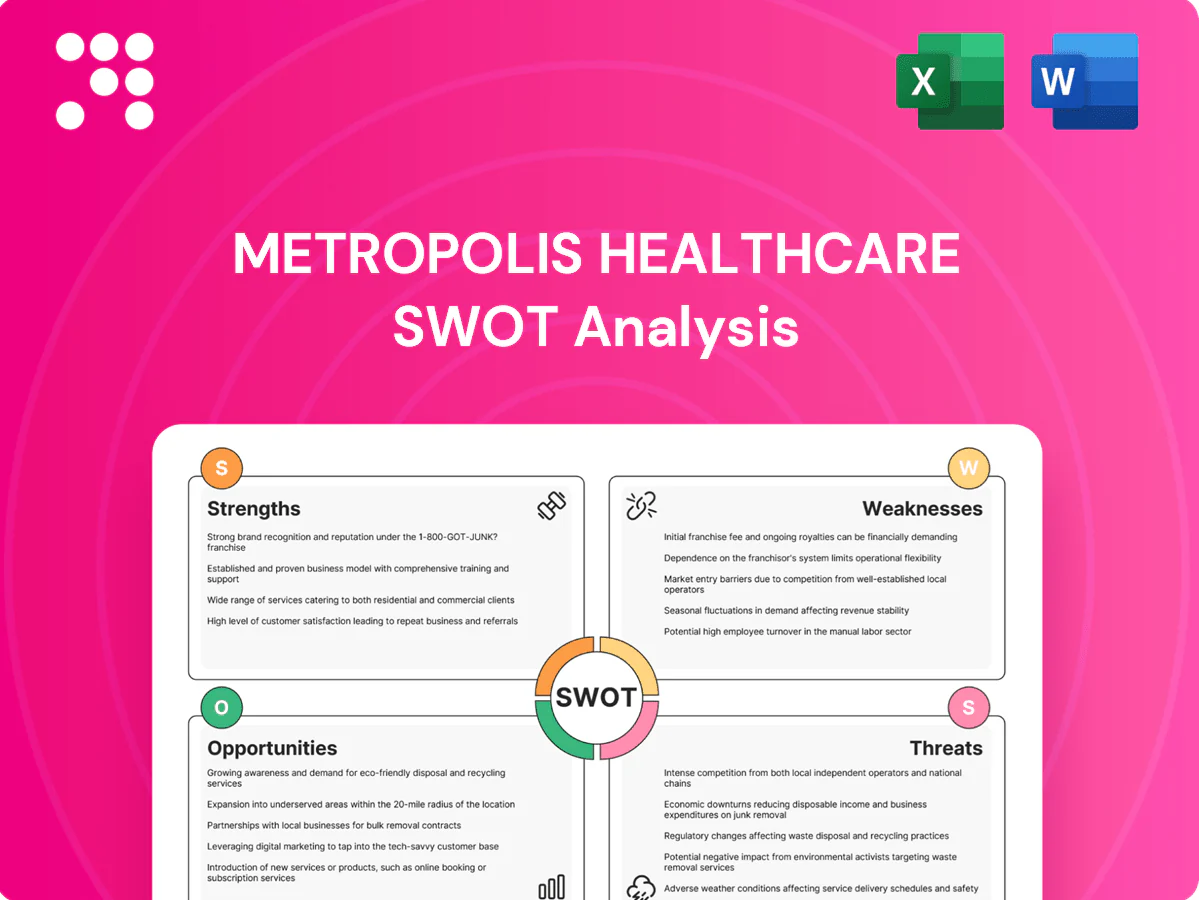

Metropolis Healthcare SWOT Analysis

Your Strategic Toolkit Starts Here

Metropolis Healthcare SWOT exposes core strengths like a national lab network and brand trust, alongside risks from competition and regulatory shifts, plus growth drivers in diagnostics and digital health. This report provides financial context and tactical recommendations. Purchase the full SWOT for a research-backed, editable Word and Excel package to strategize, pitch, or invest with confidence.

Strengths

Strong brand and quality accreditations

Metropolis is widely recognized for reliable, accurate diagnostics, holding NABL and CAP accreditations and being a publicly listed diagnostics leader. Robust quality systems and regular proficiency testing heighten clinician trust and drive repeat referrals. This premium positioning, combined with strong QA, lowers retest rates and boosts operating efficiency—supporting reported FY2024 revenue of ₹2,051 crore.

Comprehensive test menu and specialty focus

Metropolis Healthcare offers a wide spectrum from routine pathology to esoteric and genetic tests, enabling capture of both high-volume and high-margin workflows. Depth in specialty areas attracts complex cases with superior margins and supports cross-selling of advanced panels to existing clients. A broad test menu reduces dependency on any single category, enhancing revenue resilience.

Omnichannel access: B2B, B2C, home collection

Omnichannel access across B2B, B2C and home collection diversifies Metropolis Healthcare revenue by serving hospitals, clinics, doctors and individual consumers, reducing dependency on any single segment. Home sample collection and digital reporting boost convenience and patient stickiness, with reported home-visit volumes rising in recent years. Multiple channels smooth demand volatility across inpatient, outpatient and retail segments. Integrated logistics and lab network enable faster turnaround times and higher capacity utilization.

Pan-regional network and hub-and-spoke model

Metropolis leverages 125+ central and satellite labs with ~3,500 collection centres (company disclosures 2023-24), optimizing scale through centralized testing and local pickup. Standardized SOPs across the pan-regional network create cost leverage and consistent quality. Efficient routing and batch processing compress turnaround times, while geographic spread cushions localized demand shocks.

- Scale: 125+ labs, ~3,500 centres (2023-24)

- Efficiency: standardized SOPs, centralized batching

- Speed: reduced TAT via routing

- Resilience: diversified geography

Strong clinician relationships and medical leadership

Strong clinician relationships at Metropolis drive steady referrals, backed by medical leadership that accelerates adoption of tests and clinical protocols. Education and CME programs bolster credibility among physicians. The company’s ecosystem—including over 400 labs and ~1,300 collection centres—creates a moat hard for new entrants to replicate.

- Clinician referrals

- Medical leadership

- CME programs

- Network scale: 400+ labs, ~1,300 centres

NABL/CAP-accredited lab network — FY2024 revenue ₹2,051 cr, 125+ labs

Metropolis combines NABL/CAP accreditations, low retest rates and strong QA with FY2024 revenue of ₹2,051 crore, building clinician trust and repeat referrals. A broad test menu from routine to esoteric and omnichannel reach (B2B, B2C, home collection) captures diverse, higher-margin demand. Scale of 125+ labs and ~3,500 collection centres (2023-24) lowers costs and improves TAT.

| Metric | Value |

|---|---|

| FY2024 Revenue | ₹2,051 crore |

| Central/satellite labs | 125+ |

| Collection centres | ~3,500 (2023-24) |

What is included in the product

Provides a concise SWOT analysis of Metropolis Healthcare, outlining its core strengths and operational weaknesses while mapping market opportunities and external threats that will shape its strategic trajectory.

Provides a concise SWOT matrix tailored to Metropolis Healthcare for rapid identification of operational and market pain points, enabling swift strategy adjustments and clear communication to stakeholders.

Weaknesses

High fixed costs and operating leverage

Labs, high-end analyzers, reagents and regulatory compliance create a heavy fixed-cost base for Metropolis, making margins highly sensitive to volume swings. Even modest patient-volume dips can sharply compress profitability due to operating leverage. Underutilized capacity in newer regions has dragged margins as demand ramps more slowly than planned. Scaling requires tight alignment of capex and phased demand growth to protect margins.

Urban concentration risk

Network density skews to metros and Tier-1 cities, with Metropolis operating over 200 clinical laboratories and more than 3,000 collection centres concentrated in urban hubs; this limits reach into fast-growing Tier-2/3 markets where diagnostic demand is rising. Overexposure to urban price competition pressures yields and margins. Expansion into smaller cities requires substantial investment in localized logistics and skilled talent.

Price sensitivity in commoditized tests

Routine pathology faces aggressive pricing from organized and unorganized players, with organized chains capturing about 40% of the Indian diagnostics market by 2024, intensifying price competition.

Promotional discounts and bundling have eroded average realizations, pressuring margins where routine tests drive high volumes.

Consumers often switch for small price differences, forcing Metropolis to invest in costly quality differentiation and accreditations to retain share.

Dependence on referral networks

Doctor and hospital referrals are the primary source of patient samples, so shifts in clinician or hospital preferences can materially reduce test volumes and revenue. Growing hospital in-sourcing of pathology services and diagnostics labs poses a direct displacement risk to outsourced volumes. Sustaining referral relationships demands ongoing commercial and CRM investment to retain throughput and margins.

- Referral-driven sample flow

- Vulnerability to referral shifts

- Hospital in-sourcing threat

- Continuous relationship management costs

Regulatory and compliance complexity

Diagnostics face evolving standards, licensing, and external quality assurance mandates that increase complexity for Metropolis Healthcare and require continuous updates to protocols and staff training.

Compliance lapses can damage reputation and disrupt operations; multi-state rules add administrative burden and slow expansion.

Costs rise with stricter data protection and biosafety norms, increasing CAPEX and OPEX for labs and IT systems.

High fixed costs and metro focus compress margins; 200+ labs, 3,000+ centres organized ~40%

High fixed costs (labs, analyzers, reagents) make margins highly volume-sensitive; underutilized capacity in new regions compresses profitability. Network concentrated in metros—200+ labs and 3,000+ collection centres—limits Tier-2/3 reach and raises urban price competition. Organized chains hold ~40% of the market (2024), intensifying pricing pressure and referral vulnerability.

| Metric | Value |

|---|---|

| Labs | 200+ |

| Collection centres | 3,000+ |

| Organized market share (2024) | ~40% |

Preview the Actual Deliverable

Metropolis Healthcare SWOT Analysis

This is the actual Metropolis Healthcare SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats.

Your Strategic Toolkit Starts Here

Metropolis Healthcare SWOT exposes core strengths like a national lab network and brand trust, alongside risks from competition and regulatory shifts, plus growth drivers in diagnostics and digital health. This report provides financial context and tactical recommendations. Purchase the full SWOT for a research-backed, editable Word and Excel package to strategize, pitch, or invest with confidence.

Strengths

Strong brand and quality accreditations

Metropolis is widely recognized for reliable, accurate diagnostics, holding NABL and CAP accreditations and being a publicly listed diagnostics leader. Robust quality systems and regular proficiency testing heighten clinician trust and drive repeat referrals. This premium positioning, combined with strong QA, lowers retest rates and boosts operating efficiency—supporting reported FY2024 revenue of ₹2,051 crore.

Comprehensive test menu and specialty focus

Metropolis Healthcare offers a wide spectrum from routine pathology to esoteric and genetic tests, enabling capture of both high-volume and high-margin workflows. Depth in specialty areas attracts complex cases with superior margins and supports cross-selling of advanced panels to existing clients. A broad test menu reduces dependency on any single category, enhancing revenue resilience.

Omnichannel access: B2B, B2C, home collection

Omnichannel access across B2B, B2C and home collection diversifies Metropolis Healthcare revenue by serving hospitals, clinics, doctors and individual consumers, reducing dependency on any single segment. Home sample collection and digital reporting boost convenience and patient stickiness, with reported home-visit volumes rising in recent years. Multiple channels smooth demand volatility across inpatient, outpatient and retail segments. Integrated logistics and lab network enable faster turnaround times and higher capacity utilization.

Pan-regional network and hub-and-spoke model

Metropolis leverages 125+ central and satellite labs with ~3,500 collection centres (company disclosures 2023-24), optimizing scale through centralized testing and local pickup. Standardized SOPs across the pan-regional network create cost leverage and consistent quality. Efficient routing and batch processing compress turnaround times, while geographic spread cushions localized demand shocks.

- Scale: 125+ labs, ~3,500 centres (2023-24)

- Efficiency: standardized SOPs, centralized batching

- Speed: reduced TAT via routing

- Resilience: diversified geography

Strong clinician relationships and medical leadership

Strong clinician relationships at Metropolis drive steady referrals, backed by medical leadership that accelerates adoption of tests and clinical protocols. Education and CME programs bolster credibility among physicians. The company’s ecosystem—including over 400 labs and ~1,300 collection centres—creates a moat hard for new entrants to replicate.

- Clinician referrals

- Medical leadership

- CME programs

- Network scale: 400+ labs, ~1,300 centres

NABL/CAP-accredited lab network — FY2024 revenue ₹2,051 cr, 125+ labs

Metropolis combines NABL/CAP accreditations, low retest rates and strong QA with FY2024 revenue of ₹2,051 crore, building clinician trust and repeat referrals. A broad test menu from routine to esoteric and omnichannel reach (B2B, B2C, home collection) captures diverse, higher-margin demand. Scale of 125+ labs and ~3,500 collection centres (2023-24) lowers costs and improves TAT.

| Metric | Value |

|---|---|

| FY2024 Revenue | ₹2,051 crore |

| Central/satellite labs | 125+ |

| Collection centres | ~3,500 (2023-24) |

What is included in the product

Provides a concise SWOT analysis of Metropolis Healthcare, outlining its core strengths and operational weaknesses while mapping market opportunities and external threats that will shape its strategic trajectory.

Provides a concise SWOT matrix tailored to Metropolis Healthcare for rapid identification of operational and market pain points, enabling swift strategy adjustments and clear communication to stakeholders.

Weaknesses

High fixed costs and operating leverage

Labs, high-end analyzers, reagents and regulatory compliance create a heavy fixed-cost base for Metropolis, making margins highly sensitive to volume swings. Even modest patient-volume dips can sharply compress profitability due to operating leverage. Underutilized capacity in newer regions has dragged margins as demand ramps more slowly than planned. Scaling requires tight alignment of capex and phased demand growth to protect margins.

Urban concentration risk

Network density skews to metros and Tier-1 cities, with Metropolis operating over 200 clinical laboratories and more than 3,000 collection centres concentrated in urban hubs; this limits reach into fast-growing Tier-2/3 markets where diagnostic demand is rising. Overexposure to urban price competition pressures yields and margins. Expansion into smaller cities requires substantial investment in localized logistics and skilled talent.

Price sensitivity in commoditized tests

Routine pathology faces aggressive pricing from organized and unorganized players, with organized chains capturing about 40% of the Indian diagnostics market by 2024, intensifying price competition.

Promotional discounts and bundling have eroded average realizations, pressuring margins where routine tests drive high volumes.

Consumers often switch for small price differences, forcing Metropolis to invest in costly quality differentiation and accreditations to retain share.

Dependence on referral networks

Doctor and hospital referrals are the primary source of patient samples, so shifts in clinician or hospital preferences can materially reduce test volumes and revenue. Growing hospital in-sourcing of pathology services and diagnostics labs poses a direct displacement risk to outsourced volumes. Sustaining referral relationships demands ongoing commercial and CRM investment to retain throughput and margins.

- Referral-driven sample flow

- Vulnerability to referral shifts

- Hospital in-sourcing threat

- Continuous relationship management costs

Regulatory and compliance complexity

Diagnostics face evolving standards, licensing, and external quality assurance mandates that increase complexity for Metropolis Healthcare and require continuous updates to protocols and staff training.

Compliance lapses can damage reputation and disrupt operations; multi-state rules add administrative burden and slow expansion.

Costs rise with stricter data protection and biosafety norms, increasing CAPEX and OPEX for labs and IT systems.

High fixed costs and metro focus compress margins; 200+ labs, 3,000+ centres organized ~40%

High fixed costs (labs, analyzers, reagents) make margins highly volume-sensitive; underutilized capacity in new regions compresses profitability. Network concentrated in metros—200+ labs and 3,000+ collection centres—limits Tier-2/3 reach and raises urban price competition. Organized chains hold ~40% of the market (2024), intensifying pricing pressure and referral vulnerability.

| Metric | Value |

|---|---|

| Labs | 200+ |

| Collection centres | 3,000+ |

| Organized market share (2024) | ~40% |

Preview the Actual Deliverable

Metropolis Healthcare SWOT Analysis

This is the actual Metropolis Healthcare SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Metropolis Healthcare SWOT exposes core strengths like a national lab network and brand trust, alongside risks from competition and regulatory shifts, plus growth drivers in diagnostics and digital health. This report provides financial context and tactical recommendations. Purchase the full SWOT for a research-backed, editable Word and Excel package to strategize, pitch, or invest with confidence.

Strengths

Strong brand and quality accreditations

Metropolis is widely recognized for reliable, accurate diagnostics, holding NABL and CAP accreditations and being a publicly listed diagnostics leader. Robust quality systems and regular proficiency testing heighten clinician trust and drive repeat referrals. This premium positioning, combined with strong QA, lowers retest rates and boosts operating efficiency—supporting reported FY2024 revenue of ₹2,051 crore.

Comprehensive test menu and specialty focus

Metropolis Healthcare offers a wide spectrum from routine pathology to esoteric and genetic tests, enabling capture of both high-volume and high-margin workflows. Depth in specialty areas attracts complex cases with superior margins and supports cross-selling of advanced panels to existing clients. A broad test menu reduces dependency on any single category, enhancing revenue resilience.

Omnichannel access: B2B, B2C, home collection

Omnichannel access across B2B, B2C and home collection diversifies Metropolis Healthcare revenue by serving hospitals, clinics, doctors and individual consumers, reducing dependency on any single segment. Home sample collection and digital reporting boost convenience and patient stickiness, with reported home-visit volumes rising in recent years. Multiple channels smooth demand volatility across inpatient, outpatient and retail segments. Integrated logistics and lab network enable faster turnaround times and higher capacity utilization.

Pan-regional network and hub-and-spoke model

Metropolis leverages 125+ central and satellite labs with ~3,500 collection centres (company disclosures 2023-24), optimizing scale through centralized testing and local pickup. Standardized SOPs across the pan-regional network create cost leverage and consistent quality. Efficient routing and batch processing compress turnaround times, while geographic spread cushions localized demand shocks.

- Scale: 125+ labs, ~3,500 centres (2023-24)

- Efficiency: standardized SOPs, centralized batching

- Speed: reduced TAT via routing

- Resilience: diversified geography

Strong clinician relationships and medical leadership

Strong clinician relationships at Metropolis drive steady referrals, backed by medical leadership that accelerates adoption of tests and clinical protocols. Education and CME programs bolster credibility among physicians. The company’s ecosystem—including over 400 labs and ~1,300 collection centres—creates a moat hard for new entrants to replicate.

- Clinician referrals

- Medical leadership

- CME programs

- Network scale: 400+ labs, ~1,300 centres

NABL/CAP-accredited lab network — FY2024 revenue ₹2,051 cr, 125+ labs

Metropolis combines NABL/CAP accreditations, low retest rates and strong QA with FY2024 revenue of ₹2,051 crore, building clinician trust and repeat referrals. A broad test menu from routine to esoteric and omnichannel reach (B2B, B2C, home collection) captures diverse, higher-margin demand. Scale of 125+ labs and ~3,500 collection centres (2023-24) lowers costs and improves TAT.

| Metric | Value |

|---|---|

| FY2024 Revenue | ₹2,051 crore |

| Central/satellite labs | 125+ |

| Collection centres | ~3,500 (2023-24) |

What is included in the product

Provides a concise SWOT analysis of Metropolis Healthcare, outlining its core strengths and operational weaknesses while mapping market opportunities and external threats that will shape its strategic trajectory.

Provides a concise SWOT matrix tailored to Metropolis Healthcare for rapid identification of operational and market pain points, enabling swift strategy adjustments and clear communication to stakeholders.

Weaknesses

High fixed costs and operating leverage

Labs, high-end analyzers, reagents and regulatory compliance create a heavy fixed-cost base for Metropolis, making margins highly sensitive to volume swings. Even modest patient-volume dips can sharply compress profitability due to operating leverage. Underutilized capacity in newer regions has dragged margins as demand ramps more slowly than planned. Scaling requires tight alignment of capex and phased demand growth to protect margins.

Urban concentration risk

Network density skews to metros and Tier-1 cities, with Metropolis operating over 200 clinical laboratories and more than 3,000 collection centres concentrated in urban hubs; this limits reach into fast-growing Tier-2/3 markets where diagnostic demand is rising. Overexposure to urban price competition pressures yields and margins. Expansion into smaller cities requires substantial investment in localized logistics and skilled talent.

Price sensitivity in commoditized tests

Routine pathology faces aggressive pricing from organized and unorganized players, with organized chains capturing about 40% of the Indian diagnostics market by 2024, intensifying price competition.

Promotional discounts and bundling have eroded average realizations, pressuring margins where routine tests drive high volumes.

Consumers often switch for small price differences, forcing Metropolis to invest in costly quality differentiation and accreditations to retain share.

Dependence on referral networks

Doctor and hospital referrals are the primary source of patient samples, so shifts in clinician or hospital preferences can materially reduce test volumes and revenue. Growing hospital in-sourcing of pathology services and diagnostics labs poses a direct displacement risk to outsourced volumes. Sustaining referral relationships demands ongoing commercial and CRM investment to retain throughput and margins.

- Referral-driven sample flow

- Vulnerability to referral shifts

- Hospital in-sourcing threat

- Continuous relationship management costs

Regulatory and compliance complexity

Diagnostics face evolving standards, licensing, and external quality assurance mandates that increase complexity for Metropolis Healthcare and require continuous updates to protocols and staff training.

Compliance lapses can damage reputation and disrupt operations; multi-state rules add administrative burden and slow expansion.

Costs rise with stricter data protection and biosafety norms, increasing CAPEX and OPEX for labs and IT systems.

High fixed costs and metro focus compress margins; 200+ labs, 3,000+ centres organized ~40%

High fixed costs (labs, analyzers, reagents) make margins highly volume-sensitive; underutilized capacity in new regions compresses profitability. Network concentrated in metros—200+ labs and 3,000+ collection centres—limits Tier-2/3 reach and raises urban price competition. Organized chains hold ~40% of the market (2024), intensifying pricing pressure and referral vulnerability.

| Metric | Value |

|---|---|

| Labs | 200+ |

| Collection centres | 3,000+ |

| Organized market share (2024) | ~40% |

Preview the Actual Deliverable

Metropolis Healthcare SWOT Analysis

This is the actual Metropolis Healthcare SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version with detailed strengths, weaknesses, opportunities and threats.