MGP PESTLE Analysis

Skip the Research. Get the Strategy.

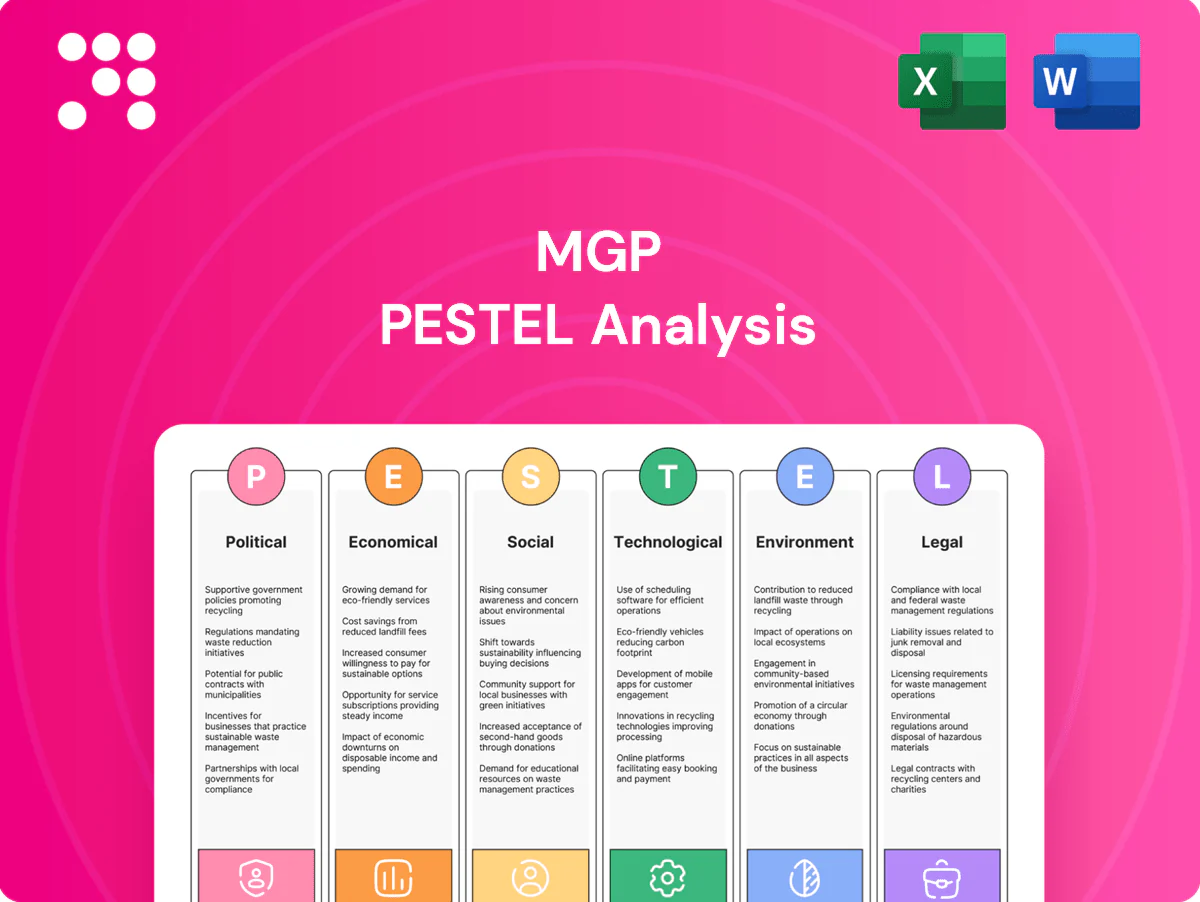

Unlock how political shifts, economic cycles, social trends, and regulatory pressures are shaping MGP’s strategic outlook with our concise PESTLE snapshot—designed for investors and strategists who need clarity fast. Buy the full analysis to access detailed risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Excise tax and alcohol policy shifts

Changes to federal and state excise taxes directly affect spirits pricing and margins; the U.S. federal excise tax remains $13.50 per proof gallon, while state rates and policy shifts create material variability. Temporary tax reliefs or hikes can swiftly alter profitability and brand competitiveness. Public health debates that restrict availability or advertising could slow demand velocity, so MGP must scenario-plan for multi-year tax regimes across key markets.

Trade policy, tariffs, and export access

Tariffs on spirits, glass or agricultural inputs — often as high as 25% on U.S. whiskey in past disputes — raise input costs and compress margins, forcing price adjustments across portfolios.

Retaliatory measures between the U.S. and trading partners have historically reduced premium-whiskey export growth, cutting volumes and pricing power in key markets.

Suspension/removal of EU/UK tariff frictions since 2021 has materially improved access for American whiskey shipments to Europe.

MGP’s ingredient exports hinge on sanitary/phytosanitary standards and customs efficiency, where inspections or delays can stall shipments and revenue recognition.

Agricultural support and farm policy

USDA programs and subsidies (PLC/ARC, crop insurance) materially influence wheat and corn availability and pricing by underpinning grower planting and revenue decisions. The Renewable Fuel Standard statutory cap of 15 billion gallons of corn ethanol drives significant grain allocation to biofuels and can elevate input costs for distilling and ingredients. Federal crop insurance now covers roughly 90% of U.S. corn acres and conservation programs shape long-term supply resilience. MGP benefits from stable farm policy that supports sustainable, high-quality grain supply.

State-level licensing and distribution regimes

The US three-tier system and 17 control jurisdictions shape MGP’s route-to-market and compress margins by adding mandatory distributor/retailer layers; state and local licensing regimes force variable pricing, taxes and promotional limits. Variability across states drives complexity in compliance and go-to-market execution, while recent political shifts (e.g., expanding Sunday sales and the 41 states allowing some DTC wine shipments) can rapidly change retail access. MGP must tailor brand strategies and supply plans jurisdiction-by-jurisdiction to protect margins and reach.

- Three-tier system: mandatory distributor layer

- Control jurisdictions: 17 states

- DTC variability: ~41 states allow wine DTC

- Political shifts affect Sunday sales, licensing and promotions

Geopolitical stability and energy policy

Geopolitical conflicts and sanctions periodically spike energy and logistics costs for distillers, increasing production margins and transport spend for MGP.

Domestic energy policy and infrastructure funding influence plant reliability and freight capacity, while port congestion and maritime risks delay exports and inbound inputs.

MGP mitigates exposure through diversified carriers, energy hedging contracts, and strategic inventory buffers to preserve supply continuity.

- Carrier diversification

- Energy hedging

- Inventory buffers

- Monitoring port/maritime risk

Federal excise, RFS cap and tariffs compress margins; corn insurance steadies supply

MGP faces federal excise at $13.50/proof gallon, state excise variability and alcohol control jurisdictions that compress margins; USDA crop insurance covers ~90% of U.S. corn acres and RFS 15bn gallon cap shifts grain to ethanol. Tariffs have reached ~25% historically, EU/UK tariff relief since 2021 improved EU access; sanctions and energy policy raise logistics costs.

| Metric | 2024/2025 | Impact |

|---|---|---|

| Federal excise | $13.50/proof gal | Direct COGS effect |

| Corn acres insured | ~90% | Supply stability |

| RFS cap | 15bn gal | Grain demand pressure |

| Tariff peak | ~25% | Export margin hit |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect MGP, using data-driven trends and region-specific examples to reveal risks and growth levers. Designed for executives and investors, it offers forward-looking insights and ready-to-use content for plans and decks.

Clean, summarized PESTLE insights for MGP that are visually segmented by category and written in plain language, making it easy to drop into presentations or share across teams; editable notes enable quick localization for region- or business-specific planning.

Economic factors

Consumer spending and premiumization

Trading up to premium bourbon and rye supports mix and pricing power—MGP saw branded and premium sales contribute to roughly 40% of net sales in FY2024, helping average selling prices rise mid-single digits year-over-year.

In downturns consumers may shift to value or private labels, pressuring branded margins; private-label contracts, which made up about 35–45% of capacity in 2024, provide volume stability but lower margins.

On-premise recovery through 2024 lifted higher-margin formats, while off-premise remained the primary volume driver; MGP’s dual exposure to brands and private label balanced these cycles and supported cash flow resilience.

Commodity and input cost volatility

Wheat (~$6.50/bu) and corn (~$4.50/bu) swings, Henry Hub natural gas (~$3.50/MMBtu) and glass container costs (≈+12% YoY in 2024) materially shift MGP COGS; droughts or bumper crops move the grain basis while logistics surcharges (typically +5–8% delivered) raise landed cost. Hedging and multi‑year supplier contracts dampen spot swings but introduce basis risk; flexible ingredient formulations manage customer cost‑in‑use.

Interest rates and capital intensity

Rising rates — US effective fed funds ~5.25% (mid‑2025) — elevate borrowing costs for inventory barreling, warehousing and plant upgrades, adding hundreds of basis points to carry on capital-intensive projects. Whiskey maturation (commonly 4–8 years) ties up working capital for multiple reporting periods, magnifying cost of carry. Tight credit conditions can slow M&A or capacity expansions, while strong cash flow and disciplined capex cadence protect returns and lower leverage risk.

Labor markets and wage inflation

Tight U.S. labor markets (avg unemployment ~3.7% in 2024) have pushed wage growth for skilled distilling, maintenance and QA roles—average hourly earnings rose about 4.0% YoY in 2024—raising overtime and training costs during capacity ramps and new line startups. Automation reduces headcount pressure but demands upfront capex, while proximity to grain belts cuts recruitment friction and inbound grain logistics costs.

- Wage growth: +4.0% YoY (2024)

- Unemployment: ~3.7% (2024)

- Automation: higher capex, lower operating payroll

- Location: near grain belt improves hiring and lowers transport

FX and global demand dynamics

Dollar strength (DXY ~104 mid‑2025) pressures export competitiveness for American whiskey, widening landed-price gaps versus Scotch and Canadian rivals. Global tourism recovery—travel volumes >90% of 2019 in 2024 (UNWTO)—and duty‑free growth boost premium spirits pull‑through. Rising affluence in EMs expands addressable demand for aged whiskey while ingredients sales follow the ~USD1.9tn packaged‑food cycle and reformulation trends.

- FX: DXY ~104 (mid‑2025)

- Tourism: travel >90% of 2019 (2024, UNWTO)

- EM demand: growing aged‑whiskey addressable market

- Ingredients: tied to ~USD1.9tn packaged‑food market and reformulation

Federal excise, RFS cap and tariffs compress margins; corn insurance steadies supply

Premium mix (~40% of net sales FY2024) and on‑premise recovery supported ASPs, while 35–45% private‑label capacity (2024) cushions volume but lowers margins. Commodity swings (wheat $6.50/bu, corn $4.50/bu, gas $3.50/MMBtu, glass +12% YoY 2024) and DXY ~104 (mid‑2025) drive COGS and export competitiveness; Fed funds ~5.25% (mid‑2025) raises carry on long maturation cycles.

| Metric | Value (year) |

|---|---|

| Branded mix | ~40% (FY2024) |

| Private‑label capacity | 35–45% (2024) |

| Wheat / Corn | $6.50 / $4.50 /bu (2024) |

| Nat. Gas | $3.50/MMBtu (2024) |

| Glass | +12% YoY (2024) |

| Fed funds | ~5.25% (mid‑2025) |

| DXY | ~104 (mid‑2025) |

Preview Before You Purchase

MGP PESTLE Analysis

The MGP PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and professional layout visible in this preview are identical to the final file you’ll download immediately after payment. No placeholders or teasers—this is the finished, ready-to-use analysis.

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, social trends, and regulatory pressures are shaping MGP’s strategic outlook with our concise PESTLE snapshot—designed for investors and strategists who need clarity fast. Buy the full analysis to access detailed risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Excise tax and alcohol policy shifts

Changes to federal and state excise taxes directly affect spirits pricing and margins; the U.S. federal excise tax remains $13.50 per proof gallon, while state rates and policy shifts create material variability. Temporary tax reliefs or hikes can swiftly alter profitability and brand competitiveness. Public health debates that restrict availability or advertising could slow demand velocity, so MGP must scenario-plan for multi-year tax regimes across key markets.

Trade policy, tariffs, and export access

Tariffs on spirits, glass or agricultural inputs — often as high as 25% on U.S. whiskey in past disputes — raise input costs and compress margins, forcing price adjustments across portfolios.

Retaliatory measures between the U.S. and trading partners have historically reduced premium-whiskey export growth, cutting volumes and pricing power in key markets.

Suspension/removal of EU/UK tariff frictions since 2021 has materially improved access for American whiskey shipments to Europe.

MGP’s ingredient exports hinge on sanitary/phytosanitary standards and customs efficiency, where inspections or delays can stall shipments and revenue recognition.

Agricultural support and farm policy

USDA programs and subsidies (PLC/ARC, crop insurance) materially influence wheat and corn availability and pricing by underpinning grower planting and revenue decisions. The Renewable Fuel Standard statutory cap of 15 billion gallons of corn ethanol drives significant grain allocation to biofuels and can elevate input costs for distilling and ingredients. Federal crop insurance now covers roughly 90% of U.S. corn acres and conservation programs shape long-term supply resilience. MGP benefits from stable farm policy that supports sustainable, high-quality grain supply.

State-level licensing and distribution regimes

The US three-tier system and 17 control jurisdictions shape MGP’s route-to-market and compress margins by adding mandatory distributor/retailer layers; state and local licensing regimes force variable pricing, taxes and promotional limits. Variability across states drives complexity in compliance and go-to-market execution, while recent political shifts (e.g., expanding Sunday sales and the 41 states allowing some DTC wine shipments) can rapidly change retail access. MGP must tailor brand strategies and supply plans jurisdiction-by-jurisdiction to protect margins and reach.

- Three-tier system: mandatory distributor layer

- Control jurisdictions: 17 states

- DTC variability: ~41 states allow wine DTC

- Political shifts affect Sunday sales, licensing and promotions

Geopolitical stability and energy policy

Geopolitical conflicts and sanctions periodically spike energy and logistics costs for distillers, increasing production margins and transport spend for MGP.

Domestic energy policy and infrastructure funding influence plant reliability and freight capacity, while port congestion and maritime risks delay exports and inbound inputs.

MGP mitigates exposure through diversified carriers, energy hedging contracts, and strategic inventory buffers to preserve supply continuity.

- Carrier diversification

- Energy hedging

- Inventory buffers

- Monitoring port/maritime risk

Federal excise, RFS cap and tariffs compress margins; corn insurance steadies supply

MGP faces federal excise at $13.50/proof gallon, state excise variability and alcohol control jurisdictions that compress margins; USDA crop insurance covers ~90% of U.S. corn acres and RFS 15bn gallon cap shifts grain to ethanol. Tariffs have reached ~25% historically, EU/UK tariff relief since 2021 improved EU access; sanctions and energy policy raise logistics costs.

| Metric | 2024/2025 | Impact |

|---|---|---|

| Federal excise | $13.50/proof gal | Direct COGS effect |

| Corn acres insured | ~90% | Supply stability |

| RFS cap | 15bn gal | Grain demand pressure |

| Tariff peak | ~25% | Export margin hit |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect MGP, using data-driven trends and region-specific examples to reveal risks and growth levers. Designed for executives and investors, it offers forward-looking insights and ready-to-use content for plans and decks.

Clean, summarized PESTLE insights for MGP that are visually segmented by category and written in plain language, making it easy to drop into presentations or share across teams; editable notes enable quick localization for region- or business-specific planning.

Economic factors

Consumer spending and premiumization

Trading up to premium bourbon and rye supports mix and pricing power—MGP saw branded and premium sales contribute to roughly 40% of net sales in FY2024, helping average selling prices rise mid-single digits year-over-year.

In downturns consumers may shift to value or private labels, pressuring branded margins; private-label contracts, which made up about 35–45% of capacity in 2024, provide volume stability but lower margins.

On-premise recovery through 2024 lifted higher-margin formats, while off-premise remained the primary volume driver; MGP’s dual exposure to brands and private label balanced these cycles and supported cash flow resilience.

Commodity and input cost volatility

Wheat (~$6.50/bu) and corn (~$4.50/bu) swings, Henry Hub natural gas (~$3.50/MMBtu) and glass container costs (≈+12% YoY in 2024) materially shift MGP COGS; droughts or bumper crops move the grain basis while logistics surcharges (typically +5–8% delivered) raise landed cost. Hedging and multi‑year supplier contracts dampen spot swings but introduce basis risk; flexible ingredient formulations manage customer cost‑in‑use.

Interest rates and capital intensity

Rising rates — US effective fed funds ~5.25% (mid‑2025) — elevate borrowing costs for inventory barreling, warehousing and plant upgrades, adding hundreds of basis points to carry on capital-intensive projects. Whiskey maturation (commonly 4–8 years) ties up working capital for multiple reporting periods, magnifying cost of carry. Tight credit conditions can slow M&A or capacity expansions, while strong cash flow and disciplined capex cadence protect returns and lower leverage risk.

Labor markets and wage inflation

Tight U.S. labor markets (avg unemployment ~3.7% in 2024) have pushed wage growth for skilled distilling, maintenance and QA roles—average hourly earnings rose about 4.0% YoY in 2024—raising overtime and training costs during capacity ramps and new line startups. Automation reduces headcount pressure but demands upfront capex, while proximity to grain belts cuts recruitment friction and inbound grain logistics costs.

- Wage growth: +4.0% YoY (2024)

- Unemployment: ~3.7% (2024)

- Automation: higher capex, lower operating payroll

- Location: near grain belt improves hiring and lowers transport

FX and global demand dynamics

Dollar strength (DXY ~104 mid‑2025) pressures export competitiveness for American whiskey, widening landed-price gaps versus Scotch and Canadian rivals. Global tourism recovery—travel volumes >90% of 2019 in 2024 (UNWTO)—and duty‑free growth boost premium spirits pull‑through. Rising affluence in EMs expands addressable demand for aged whiskey while ingredients sales follow the ~USD1.9tn packaged‑food cycle and reformulation trends.

- FX: DXY ~104 (mid‑2025)

- Tourism: travel >90% of 2019 (2024, UNWTO)

- EM demand: growing aged‑whiskey addressable market

- Ingredients: tied to ~USD1.9tn packaged‑food market and reformulation

Federal excise, RFS cap and tariffs compress margins; corn insurance steadies supply

Premium mix (~40% of net sales FY2024) and on‑premise recovery supported ASPs, while 35–45% private‑label capacity (2024) cushions volume but lowers margins. Commodity swings (wheat $6.50/bu, corn $4.50/bu, gas $3.50/MMBtu, glass +12% YoY 2024) and DXY ~104 (mid‑2025) drive COGS and export competitiveness; Fed funds ~5.25% (mid‑2025) raises carry on long maturation cycles.

| Metric | Value (year) |

|---|---|

| Branded mix | ~40% (FY2024) |

| Private‑label capacity | 35–45% (2024) |

| Wheat / Corn | $6.50 / $4.50 /bu (2024) |

| Nat. Gas | $3.50/MMBtu (2024) |

| Glass | +12% YoY (2024) |

| Fed funds | ~5.25% (mid‑2025) |

| DXY | ~104 (mid‑2025) |

Preview Before You Purchase

MGP PESTLE Analysis

The MGP PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and professional layout visible in this preview are identical to the final file you’ll download immediately after payment. No placeholders or teasers—this is the finished, ready-to-use analysis.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, social trends, and regulatory pressures are shaping MGP’s strategic outlook with our concise PESTLE snapshot—designed for investors and strategists who need clarity fast. Buy the full analysis to access detailed risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Excise tax and alcohol policy shifts

Changes to federal and state excise taxes directly affect spirits pricing and margins; the U.S. federal excise tax remains $13.50 per proof gallon, while state rates and policy shifts create material variability. Temporary tax reliefs or hikes can swiftly alter profitability and brand competitiveness. Public health debates that restrict availability or advertising could slow demand velocity, so MGP must scenario-plan for multi-year tax regimes across key markets.

Trade policy, tariffs, and export access

Tariffs on spirits, glass or agricultural inputs — often as high as 25% on U.S. whiskey in past disputes — raise input costs and compress margins, forcing price adjustments across portfolios.

Retaliatory measures between the U.S. and trading partners have historically reduced premium-whiskey export growth, cutting volumes and pricing power in key markets.

Suspension/removal of EU/UK tariff frictions since 2021 has materially improved access for American whiskey shipments to Europe.

MGP’s ingredient exports hinge on sanitary/phytosanitary standards and customs efficiency, where inspections or delays can stall shipments and revenue recognition.

Agricultural support and farm policy

USDA programs and subsidies (PLC/ARC, crop insurance) materially influence wheat and corn availability and pricing by underpinning grower planting and revenue decisions. The Renewable Fuel Standard statutory cap of 15 billion gallons of corn ethanol drives significant grain allocation to biofuels and can elevate input costs for distilling and ingredients. Federal crop insurance now covers roughly 90% of U.S. corn acres and conservation programs shape long-term supply resilience. MGP benefits from stable farm policy that supports sustainable, high-quality grain supply.

State-level licensing and distribution regimes

The US three-tier system and 17 control jurisdictions shape MGP’s route-to-market and compress margins by adding mandatory distributor/retailer layers; state and local licensing regimes force variable pricing, taxes and promotional limits. Variability across states drives complexity in compliance and go-to-market execution, while recent political shifts (e.g., expanding Sunday sales and the 41 states allowing some DTC wine shipments) can rapidly change retail access. MGP must tailor brand strategies and supply plans jurisdiction-by-jurisdiction to protect margins and reach.

- Three-tier system: mandatory distributor layer

- Control jurisdictions: 17 states

- DTC variability: ~41 states allow wine DTC

- Political shifts affect Sunday sales, licensing and promotions

Geopolitical stability and energy policy

Geopolitical conflicts and sanctions periodically spike energy and logistics costs for distillers, increasing production margins and transport spend for MGP.

Domestic energy policy and infrastructure funding influence plant reliability and freight capacity, while port congestion and maritime risks delay exports and inbound inputs.

MGP mitigates exposure through diversified carriers, energy hedging contracts, and strategic inventory buffers to preserve supply continuity.

- Carrier diversification

- Energy hedging

- Inventory buffers

- Monitoring port/maritime risk

Federal excise, RFS cap and tariffs compress margins; corn insurance steadies supply

MGP faces federal excise at $13.50/proof gallon, state excise variability and alcohol control jurisdictions that compress margins; USDA crop insurance covers ~90% of U.S. corn acres and RFS 15bn gallon cap shifts grain to ethanol. Tariffs have reached ~25% historically, EU/UK tariff relief since 2021 improved EU access; sanctions and energy policy raise logistics costs.

| Metric | 2024/2025 | Impact |

|---|---|---|

| Federal excise | $13.50/proof gal | Direct COGS effect |

| Corn acres insured | ~90% | Supply stability |

| RFS cap | 15bn gal | Grain demand pressure |

| Tariff peak | ~25% | Export margin hit |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect MGP, using data-driven trends and region-specific examples to reveal risks and growth levers. Designed for executives and investors, it offers forward-looking insights and ready-to-use content for plans and decks.

Clean, summarized PESTLE insights for MGP that are visually segmented by category and written in plain language, making it easy to drop into presentations or share across teams; editable notes enable quick localization for region- or business-specific planning.

Economic factors

Consumer spending and premiumization

Trading up to premium bourbon and rye supports mix and pricing power—MGP saw branded and premium sales contribute to roughly 40% of net sales in FY2024, helping average selling prices rise mid-single digits year-over-year.

In downturns consumers may shift to value or private labels, pressuring branded margins; private-label contracts, which made up about 35–45% of capacity in 2024, provide volume stability but lower margins.

On-premise recovery through 2024 lifted higher-margin formats, while off-premise remained the primary volume driver; MGP’s dual exposure to brands and private label balanced these cycles and supported cash flow resilience.

Commodity and input cost volatility

Wheat (~$6.50/bu) and corn (~$4.50/bu) swings, Henry Hub natural gas (~$3.50/MMBtu) and glass container costs (≈+12% YoY in 2024) materially shift MGP COGS; droughts or bumper crops move the grain basis while logistics surcharges (typically +5–8% delivered) raise landed cost. Hedging and multi‑year supplier contracts dampen spot swings but introduce basis risk; flexible ingredient formulations manage customer cost‑in‑use.

Interest rates and capital intensity

Rising rates — US effective fed funds ~5.25% (mid‑2025) — elevate borrowing costs for inventory barreling, warehousing and plant upgrades, adding hundreds of basis points to carry on capital-intensive projects. Whiskey maturation (commonly 4–8 years) ties up working capital for multiple reporting periods, magnifying cost of carry. Tight credit conditions can slow M&A or capacity expansions, while strong cash flow and disciplined capex cadence protect returns and lower leverage risk.

Labor markets and wage inflation

Tight U.S. labor markets (avg unemployment ~3.7% in 2024) have pushed wage growth for skilled distilling, maintenance and QA roles—average hourly earnings rose about 4.0% YoY in 2024—raising overtime and training costs during capacity ramps and new line startups. Automation reduces headcount pressure but demands upfront capex, while proximity to grain belts cuts recruitment friction and inbound grain logistics costs.

- Wage growth: +4.0% YoY (2024)

- Unemployment: ~3.7% (2024)

- Automation: higher capex, lower operating payroll

- Location: near grain belt improves hiring and lowers transport

FX and global demand dynamics

Dollar strength (DXY ~104 mid‑2025) pressures export competitiveness for American whiskey, widening landed-price gaps versus Scotch and Canadian rivals. Global tourism recovery—travel volumes >90% of 2019 in 2024 (UNWTO)—and duty‑free growth boost premium spirits pull‑through. Rising affluence in EMs expands addressable demand for aged whiskey while ingredients sales follow the ~USD1.9tn packaged‑food cycle and reformulation trends.

- FX: DXY ~104 (mid‑2025)

- Tourism: travel >90% of 2019 (2024, UNWTO)

- EM demand: growing aged‑whiskey addressable market

- Ingredients: tied to ~USD1.9tn packaged‑food market and reformulation

Federal excise, RFS cap and tariffs compress margins; corn insurance steadies supply

Premium mix (~40% of net sales FY2024) and on‑premise recovery supported ASPs, while 35–45% private‑label capacity (2024) cushions volume but lowers margins. Commodity swings (wheat $6.50/bu, corn $4.50/bu, gas $3.50/MMBtu, glass +12% YoY 2024) and DXY ~104 (mid‑2025) drive COGS and export competitiveness; Fed funds ~5.25% (mid‑2025) raises carry on long maturation cycles.

| Metric | Value (year) |

|---|---|

| Branded mix | ~40% (FY2024) |

| Private‑label capacity | 35–45% (2024) |

| Wheat / Corn | $6.50 / $4.50 /bu (2024) |

| Nat. Gas | $3.50/MMBtu (2024) |

| Glass | +12% YoY (2024) |

| Fed funds | ~5.25% (mid‑2025) |

| DXY | ~104 (mid‑2025) |

Preview Before You Purchase

MGP PESTLE Analysis

The MGP PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and professional layout visible in this preview are identical to the final file you’ll download immediately after payment. No placeholders or teasers—this is the finished, ready-to-use analysis.