Microchip Technology Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

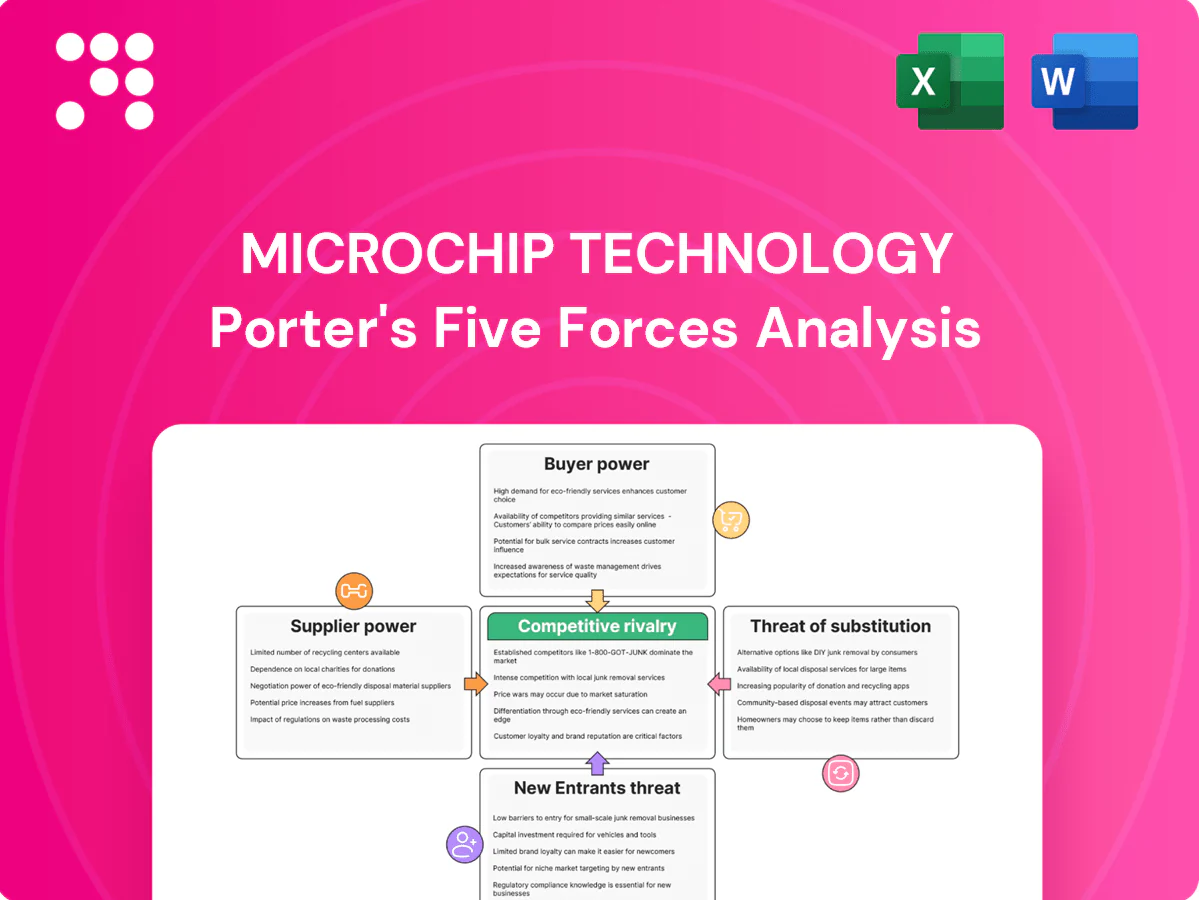

Microchip Technology faces intense rivalry, concentrated supplier channels, and rising buyer sophistication that shape its semiconductor margins and strategic choices. Our snapshot highlights key pressures but omits force-by-force scoring, trend visuals, and scenario implications. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable insights and ready-to-use deliverables.

Suppliers Bargaining Power

Concentrated foundry and OSAT base

Microchip uses internal fabs plus external foundries and OSAT partners; leading foundries (eg TSMC) represented roughly half of global foundry revenue in 2024 and the top three OSATs >50% of OSAT revenue, concentrating allocation power in tight cycles. Mature-node capacity is constrained and often repriced upward; multi-sourcing reduces but cannot fully neutralize supplier scarcity leverage.

Specialty materials and equipment dependencies

Microchip depends on specialized photoresists, specialty gases, substrates and lithography/etch tools sourced from a handful of qualified vendors (top 5 suppliers control roughly 80% of global semiconductor equipment supply), giving those suppliers outsized leverage. Qualification cycles for materials and tools typically run 6–18 months and lead times of 3–12 months, increasing switching friction. Any supplier disruption can quickly degrade yields and extend cycle times, transferring cost and schedule risk to Microchip. Suppliers’ technical uniqueness and long lead times therefore raise their bargaining power.

IP, EDA, and licensing lock-ins

Microchip's FY2024 revenue was $11.729 billion, making supplier-driven IP and EDA costs material to product economics. Dependence on EDA toolchains, reference IP, Flash/analog libraries and training creates embedded switching costs; Synopsys and Cadence together hold roughly 60% of the EDA market. Licensing terms can compress gross margins on new tape-outs, and vendors retain pricing power for advanced verification and security IP.

Automotive-grade quality requirements

Automotive PPAP, AEC-Q100 qualification and zero-defect targets sharply limit usable IC sources, concentrating supply (top 10 suppliers >70% of automotive semiconductor revenue in 2024) and increasing supplier leverage.

Requalification is costly and slow (commonly 6–18 months and multi-million-dollar validation programs), allowing qualified suppliers to secure firmer pricing and multi-year commitments.

- PPAP/AEC-Q100 restricts pool

- Top suppliers control >70% (2024)

- Requal: 6–18 months, multi-$ cost

- Qualified vendors win pricing/terms

Cyclicality and allocation dynamics

In upcycles capacity allocations skew to higher-margin customers, boosting supplier power and pressuring Microchip’s fill rates; in FY2024 Microchip reported roughly $8.4B revenue, leaving some leverage but not immunity. In downcycles the balance shifts as suppliers chase utilization, softening pricing power. Long-term agreements and prepayments on key nodes have helped stabilize terms, while Microchip’s diversified analog, MCU and FPGA mix moderates exposure.

- Upcycle: allocations favor high-margin buyers — increases supplier leverage

- Downcycle: suppliers chase utilization — leverage reverts

- Mitigants: long-term contracts + prepayments

- Microchip: diversified product mix limits but doesn’t remove risk

Foundry and OSAT concentration squeezes mature-node supply; EDA/equipment bottlenecks persist

Suppliers hold high leverage: top foundries ~50% share (2024) and top OSATs >50%, constraining mature-node capacity and allocations. Critical materials and equipment are concentrated (top 5 equipment suppliers ~80%), with EDA/IP reliance (Synopsys+Cadence ~60%) and requalification (6–18 months) raising switching costs. Automotive qualifications (top 10 suppliers >70% of automotive semiconductor revenue) further concentrate supplier power.

| Metric | 2024 Value |

|---|---|

| Microchip FY2024 revenue | $11.729B |

| Top foundry share | ~50% |

| Top OSATs share | >50% |

| Top 5 equip. suppliers | ~80% |

| Synopsys+Cadence (EDA) | ~60% |

| Automotive top10 | >70% |

| Requalification lead time | 6–18 months |

What is included in the product

Tailored Porter’s Five Forces analysis for Microchip Technology, uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive risks and strategic levers affecting profitability.

A concise Porter's Five Forces snapshot for Microchip Technology — instantly highlights supplier, buyer, rivalry, substitution and entry pressures so teams can prioritize risks and opportunities for strategy, M&A or investor decks.

Customers Bargaining Power

Large OEMs and Tier-1s negotiate hard

Large OEMs and Tier-1s in automotive, industrial and communications buy at scale and routinely pressure pricing, with Microchip reporting annual revenue exceeding $7 billion in 2024 that sharpens buyers’ leverage. Approved vendor lists and multi-sourcing keep switching options open for many sockets. Customers demand volume rebates and consignment terms, and strategic accounts—often representing >10% of sales—can shape product roadmaps and support levels.

High switching costs from design-in

MCUs, analog ICs and FPGAs are deeply embedded in firmware, certifications and PCB layouts, so redesigns incur firmware rewrites, recertification costs and schedule delays; recertification alone can add months. Microchip’s 2024 longevity programs commonly exceed 10 years, keeping parts in production and lowering mid‑lifecycle churn. That entrenches suppliers after design‑win and weakens buyer price leverage.

Cyclical demand and inventory digestion

Cyclical demand lets customers amplify pricing pressure in downturns through order pauses and pushouts; Microchip reported roughly $7.3 billion revenue in FY2024, amplifying sensitivity to such volume swings. Distributor channel inventory and order cadence introduce additional negotiating dynamics as channel fill rates and stock turns fluctuate. Hub and buffer agreements with distributors and key OEMs can curb volatility but do not eliminate it, and buyers routinely exploit cycles to reset pricing baselines.

Ecosystem and toolchain lock-in

Development tools, libraries and reference designs tether engineers to Microchip, and training plus code reuse create inertia; migration often requires months and six-figure engineering costs, so buyers face material switching frictions. Microchip's scale (over $8 billion revenue in 2024) amplifies ecosystem lock-in, tempering buyer power despite nominal alternatives.

- Toolchain and libraries lock engineers in

- Training/code reuse incentivize incumbency

- Migration: months of work, often six-figure costs

Certification and reliability requirements

Safety-critical markets require lengthy qualification per part and supplier, often 6–24 months. Buyers prioritize supply assurance and proven field reliability over lowest price, increasing switching costs for Microchip. Vendor change can trigger supplier audits and plant-level validations, creating frictions that constrain customer switching.

- Qualification timelines: 6–24 months

- Switching triggers: audits & plant validations

- Buyer priority: supply assurance > price

Design‑win lock‑in sustains supplier leverage; FY2024 revenue $7.3B

Large OEMs buy at scale and push pricing, but Microchip’s FY2024 revenue ≈ $7.3B and design‑win entrenchment limit buyer leverage. Embedded MCUs, toolchain lock‑in and migration costs (often six‑figure, months) raise switching barriers. Qualification times (6–24 months) and strategic accounts (>10% of sales) further tilt power toward the supplier.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈ $7.3B |

| Major account share | >10% per strategic customer |

| Qualification time | 6–24 months |

| Migration cost | Typically six‑figure, months |

Same Document Delivered

Microchip Technology Porter's Five Forces Analysis

This preview shows the exact Microchip Technology Porter's Five Forces Analysis document you'll receive immediately after purchase—no placeholders, no edits. It is the full, professionally formatted analysis covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes, ready for instant download and use upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Microchip Technology faces intense rivalry, concentrated supplier channels, and rising buyer sophistication that shape its semiconductor margins and strategic choices. Our snapshot highlights key pressures but omits force-by-force scoring, trend visuals, and scenario implications. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable insights and ready-to-use deliverables.

Suppliers Bargaining Power

Concentrated foundry and OSAT base

Microchip uses internal fabs plus external foundries and OSAT partners; leading foundries (eg TSMC) represented roughly half of global foundry revenue in 2024 and the top three OSATs >50% of OSAT revenue, concentrating allocation power in tight cycles. Mature-node capacity is constrained and often repriced upward; multi-sourcing reduces but cannot fully neutralize supplier scarcity leverage.

Specialty materials and equipment dependencies

Microchip depends on specialized photoresists, specialty gases, substrates and lithography/etch tools sourced from a handful of qualified vendors (top 5 suppliers control roughly 80% of global semiconductor equipment supply), giving those suppliers outsized leverage. Qualification cycles for materials and tools typically run 6–18 months and lead times of 3–12 months, increasing switching friction. Any supplier disruption can quickly degrade yields and extend cycle times, transferring cost and schedule risk to Microchip. Suppliers’ technical uniqueness and long lead times therefore raise their bargaining power.

IP, EDA, and licensing lock-ins

Microchip's FY2024 revenue was $11.729 billion, making supplier-driven IP and EDA costs material to product economics. Dependence on EDA toolchains, reference IP, Flash/analog libraries and training creates embedded switching costs; Synopsys and Cadence together hold roughly 60% of the EDA market. Licensing terms can compress gross margins on new tape-outs, and vendors retain pricing power for advanced verification and security IP.

Automotive-grade quality requirements

Automotive PPAP, AEC-Q100 qualification and zero-defect targets sharply limit usable IC sources, concentrating supply (top 10 suppliers >70% of automotive semiconductor revenue in 2024) and increasing supplier leverage.

Requalification is costly and slow (commonly 6–18 months and multi-million-dollar validation programs), allowing qualified suppliers to secure firmer pricing and multi-year commitments.

- PPAP/AEC-Q100 restricts pool

- Top suppliers control >70% (2024)

- Requal: 6–18 months, multi-$ cost

- Qualified vendors win pricing/terms

Cyclicality and allocation dynamics

In upcycles capacity allocations skew to higher-margin customers, boosting supplier power and pressuring Microchip’s fill rates; in FY2024 Microchip reported roughly $8.4B revenue, leaving some leverage but not immunity. In downcycles the balance shifts as suppliers chase utilization, softening pricing power. Long-term agreements and prepayments on key nodes have helped stabilize terms, while Microchip’s diversified analog, MCU and FPGA mix moderates exposure.

- Upcycle: allocations favor high-margin buyers — increases supplier leverage

- Downcycle: suppliers chase utilization — leverage reverts

- Mitigants: long-term contracts + prepayments

- Microchip: diversified product mix limits but doesn’t remove risk

Foundry and OSAT concentration squeezes mature-node supply; EDA/equipment bottlenecks persist

Suppliers hold high leverage: top foundries ~50% share (2024) and top OSATs >50%, constraining mature-node capacity and allocations. Critical materials and equipment are concentrated (top 5 equipment suppliers ~80%), with EDA/IP reliance (Synopsys+Cadence ~60%) and requalification (6–18 months) raising switching costs. Automotive qualifications (top 10 suppliers >70% of automotive semiconductor revenue) further concentrate supplier power.

| Metric | 2024 Value |

|---|---|

| Microchip FY2024 revenue | $11.729B |

| Top foundry share | ~50% |

| Top OSATs share | >50% |

| Top 5 equip. suppliers | ~80% |

| Synopsys+Cadence (EDA) | ~60% |

| Automotive top10 | >70% |

| Requalification lead time | 6–18 months |

What is included in the product

Tailored Porter’s Five Forces analysis for Microchip Technology, uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive risks and strategic levers affecting profitability.

A concise Porter's Five Forces snapshot for Microchip Technology — instantly highlights supplier, buyer, rivalry, substitution and entry pressures so teams can prioritize risks and opportunities for strategy, M&A or investor decks.

Customers Bargaining Power

Large OEMs and Tier-1s negotiate hard

Large OEMs and Tier-1s in automotive, industrial and communications buy at scale and routinely pressure pricing, with Microchip reporting annual revenue exceeding $7 billion in 2024 that sharpens buyers’ leverage. Approved vendor lists and multi-sourcing keep switching options open for many sockets. Customers demand volume rebates and consignment terms, and strategic accounts—often representing >10% of sales—can shape product roadmaps and support levels.

High switching costs from design-in

MCUs, analog ICs and FPGAs are deeply embedded in firmware, certifications and PCB layouts, so redesigns incur firmware rewrites, recertification costs and schedule delays; recertification alone can add months. Microchip’s 2024 longevity programs commonly exceed 10 years, keeping parts in production and lowering mid‑lifecycle churn. That entrenches suppliers after design‑win and weakens buyer price leverage.

Cyclical demand and inventory digestion

Cyclical demand lets customers amplify pricing pressure in downturns through order pauses and pushouts; Microchip reported roughly $7.3 billion revenue in FY2024, amplifying sensitivity to such volume swings. Distributor channel inventory and order cadence introduce additional negotiating dynamics as channel fill rates and stock turns fluctuate. Hub and buffer agreements with distributors and key OEMs can curb volatility but do not eliminate it, and buyers routinely exploit cycles to reset pricing baselines.

Ecosystem and toolchain lock-in

Development tools, libraries and reference designs tether engineers to Microchip, and training plus code reuse create inertia; migration often requires months and six-figure engineering costs, so buyers face material switching frictions. Microchip's scale (over $8 billion revenue in 2024) amplifies ecosystem lock-in, tempering buyer power despite nominal alternatives.

- Toolchain and libraries lock engineers in

- Training/code reuse incentivize incumbency

- Migration: months of work, often six-figure costs

Certification and reliability requirements

Safety-critical markets require lengthy qualification per part and supplier, often 6–24 months. Buyers prioritize supply assurance and proven field reliability over lowest price, increasing switching costs for Microchip. Vendor change can trigger supplier audits and plant-level validations, creating frictions that constrain customer switching.

- Qualification timelines: 6–24 months

- Switching triggers: audits & plant validations

- Buyer priority: supply assurance > price

Design‑win lock‑in sustains supplier leverage; FY2024 revenue $7.3B

Large OEMs buy at scale and push pricing, but Microchip’s FY2024 revenue ≈ $7.3B and design‑win entrenchment limit buyer leverage. Embedded MCUs, toolchain lock‑in and migration costs (often six‑figure, months) raise switching barriers. Qualification times (6–24 months) and strategic accounts (>10% of sales) further tilt power toward the supplier.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈ $7.3B |

| Major account share | >10% per strategic customer |

| Qualification time | 6–24 months |

| Migration cost | Typically six‑figure, months |

Same Document Delivered

Microchip Technology Porter's Five Forces Analysis

This preview shows the exact Microchip Technology Porter's Five Forces Analysis document you'll receive immediately after purchase—no placeholders, no edits. It is the full, professionally formatted analysis covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes, ready for instant download and use upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Microchip Technology faces intense rivalry, concentrated supplier channels, and rising buyer sophistication that shape its semiconductor margins and strategic choices. Our snapshot highlights key pressures but omits force-by-force scoring, trend visuals, and scenario implications. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable insights and ready-to-use deliverables.

Suppliers Bargaining Power

Concentrated foundry and OSAT base

Microchip uses internal fabs plus external foundries and OSAT partners; leading foundries (eg TSMC) represented roughly half of global foundry revenue in 2024 and the top three OSATs >50% of OSAT revenue, concentrating allocation power in tight cycles. Mature-node capacity is constrained and often repriced upward; multi-sourcing reduces but cannot fully neutralize supplier scarcity leverage.

Specialty materials and equipment dependencies

Microchip depends on specialized photoresists, specialty gases, substrates and lithography/etch tools sourced from a handful of qualified vendors (top 5 suppliers control roughly 80% of global semiconductor equipment supply), giving those suppliers outsized leverage. Qualification cycles for materials and tools typically run 6–18 months and lead times of 3–12 months, increasing switching friction. Any supplier disruption can quickly degrade yields and extend cycle times, transferring cost and schedule risk to Microchip. Suppliers’ technical uniqueness and long lead times therefore raise their bargaining power.

IP, EDA, and licensing lock-ins

Microchip's FY2024 revenue was $11.729 billion, making supplier-driven IP and EDA costs material to product economics. Dependence on EDA toolchains, reference IP, Flash/analog libraries and training creates embedded switching costs; Synopsys and Cadence together hold roughly 60% of the EDA market. Licensing terms can compress gross margins on new tape-outs, and vendors retain pricing power for advanced verification and security IP.

Automotive-grade quality requirements

Automotive PPAP, AEC-Q100 qualification and zero-defect targets sharply limit usable IC sources, concentrating supply (top 10 suppliers >70% of automotive semiconductor revenue in 2024) and increasing supplier leverage.

Requalification is costly and slow (commonly 6–18 months and multi-million-dollar validation programs), allowing qualified suppliers to secure firmer pricing and multi-year commitments.

- PPAP/AEC-Q100 restricts pool

- Top suppliers control >70% (2024)

- Requal: 6–18 months, multi-$ cost

- Qualified vendors win pricing/terms

Cyclicality and allocation dynamics

In upcycles capacity allocations skew to higher-margin customers, boosting supplier power and pressuring Microchip’s fill rates; in FY2024 Microchip reported roughly $8.4B revenue, leaving some leverage but not immunity. In downcycles the balance shifts as suppliers chase utilization, softening pricing power. Long-term agreements and prepayments on key nodes have helped stabilize terms, while Microchip’s diversified analog, MCU and FPGA mix moderates exposure.

- Upcycle: allocations favor high-margin buyers — increases supplier leverage

- Downcycle: suppliers chase utilization — leverage reverts

- Mitigants: long-term contracts + prepayments

- Microchip: diversified product mix limits but doesn’t remove risk

Foundry and OSAT concentration squeezes mature-node supply; EDA/equipment bottlenecks persist

Suppliers hold high leverage: top foundries ~50% share (2024) and top OSATs >50%, constraining mature-node capacity and allocations. Critical materials and equipment are concentrated (top 5 equipment suppliers ~80%), with EDA/IP reliance (Synopsys+Cadence ~60%) and requalification (6–18 months) raising switching costs. Automotive qualifications (top 10 suppliers >70% of automotive semiconductor revenue) further concentrate supplier power.

| Metric | 2024 Value |

|---|---|

| Microchip FY2024 revenue | $11.729B |

| Top foundry share | ~50% |

| Top OSATs share | >50% |

| Top 5 equip. suppliers | ~80% |

| Synopsys+Cadence (EDA) | ~60% |

| Automotive top10 | >70% |

| Requalification lead time | 6–18 months |

What is included in the product

Tailored Porter’s Five Forces analysis for Microchip Technology, uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlighting disruptive risks and strategic levers affecting profitability.

A concise Porter's Five Forces snapshot for Microchip Technology — instantly highlights supplier, buyer, rivalry, substitution and entry pressures so teams can prioritize risks and opportunities for strategy, M&A or investor decks.

Customers Bargaining Power

Large OEMs and Tier-1s negotiate hard

Large OEMs and Tier-1s in automotive, industrial and communications buy at scale and routinely pressure pricing, with Microchip reporting annual revenue exceeding $7 billion in 2024 that sharpens buyers’ leverage. Approved vendor lists and multi-sourcing keep switching options open for many sockets. Customers demand volume rebates and consignment terms, and strategic accounts—often representing >10% of sales—can shape product roadmaps and support levels.

High switching costs from design-in

MCUs, analog ICs and FPGAs are deeply embedded in firmware, certifications and PCB layouts, so redesigns incur firmware rewrites, recertification costs and schedule delays; recertification alone can add months. Microchip’s 2024 longevity programs commonly exceed 10 years, keeping parts in production and lowering mid‑lifecycle churn. That entrenches suppliers after design‑win and weakens buyer price leverage.

Cyclical demand and inventory digestion

Cyclical demand lets customers amplify pricing pressure in downturns through order pauses and pushouts; Microchip reported roughly $7.3 billion revenue in FY2024, amplifying sensitivity to such volume swings. Distributor channel inventory and order cadence introduce additional negotiating dynamics as channel fill rates and stock turns fluctuate. Hub and buffer agreements with distributors and key OEMs can curb volatility but do not eliminate it, and buyers routinely exploit cycles to reset pricing baselines.

Ecosystem and toolchain lock-in

Development tools, libraries and reference designs tether engineers to Microchip, and training plus code reuse create inertia; migration often requires months and six-figure engineering costs, so buyers face material switching frictions. Microchip's scale (over $8 billion revenue in 2024) amplifies ecosystem lock-in, tempering buyer power despite nominal alternatives.

- Toolchain and libraries lock engineers in

- Training/code reuse incentivize incumbency

- Migration: months of work, often six-figure costs

Certification and reliability requirements

Safety-critical markets require lengthy qualification per part and supplier, often 6–24 months. Buyers prioritize supply assurance and proven field reliability over lowest price, increasing switching costs for Microchip. Vendor change can trigger supplier audits and plant-level validations, creating frictions that constrain customer switching.

- Qualification timelines: 6–24 months

- Switching triggers: audits & plant validations

- Buyer priority: supply assurance > price

Design‑win lock‑in sustains supplier leverage; FY2024 revenue $7.3B

Large OEMs buy at scale and push pricing, but Microchip’s FY2024 revenue ≈ $7.3B and design‑win entrenchment limit buyer leverage. Embedded MCUs, toolchain lock‑in and migration costs (often six‑figure, months) raise switching barriers. Qualification times (6–24 months) and strategic accounts (>10% of sales) further tilt power toward the supplier.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈ $7.3B |

| Major account share | >10% per strategic customer |

| Qualification time | 6–24 months |

| Migration cost | Typically six‑figure, months |

Same Document Delivered

Microchip Technology Porter's Five Forces Analysis

This preview shows the exact Microchip Technology Porter's Five Forces Analysis document you'll receive immediately after purchase—no placeholders, no edits. It is the full, professionally formatted analysis covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes, ready for instant download and use upon payment.