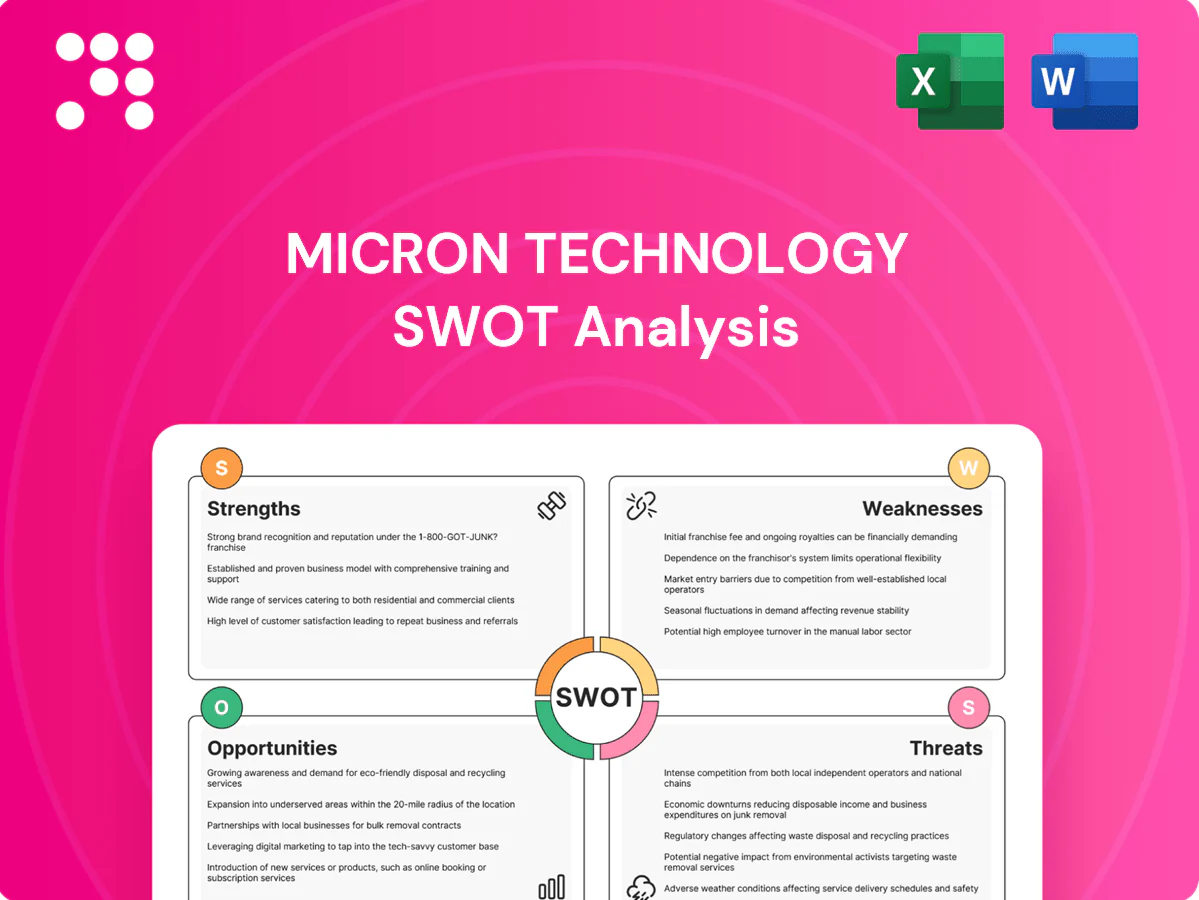

Micron Technology SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Micron Technology blends leading memory technology and scale with cyclical market exposure and intense competition, so strategic clarity is vital. Discover the full SWOT analysis for actionable insights, financial context, and risk mitigation strategies. Purchase the complete, editable Word and Excel package to present, plan, and invest with confidence.

Strengths

Leading memory technology roadmap

Micron advances DRAM with 1-beta/1-gamma nodes and 232–240+ layer NAND, boosting density and performance to sustain bit-cost and power-per-bit declines critical for AI and data-center workloads. Leadership across LPDDR5X, DDR5, GDDR and HBM3E aligns with next-gen platforms, while a strong R&D engine and process know-how underpin a durable technology advantage.

Diversified end-market exposure

Micron's FY2024 revenue was about $27.7 billion and spans data center, client, mobile, industrial and automotive, smoothing cycles vs single‑segment peers. Automotive and industrial demand features multi‑year lifecycles and strict quality specs, producing stickier revenue. Growth in AI servers and edge devices is shifting mix toward higher‑value bits, reducing reliance on any single device cycle.

HBM and AI acceleration tailwinds

HBM is critical for AI training and inference, exemplified by NVIDIA H100 using up to 80GB HBM3 versus V100's 16GB HBM2 (≈5x more memory per GPU), driving much higher bit demand. Rising attach rates per GPU are lifting ASPs. Micron's HBM3E ramp positions it in this fastest-growing memory niche. Close alignment with leading AI platform vendors strengthens design-win momentum and a premium mix versus commodity DRAM.

Scale manufacturing and global footprint

Micron’s scale manufacturing spans the U.S., Singapore, Japan and Taiwan, giving capacity flexibility and regional risk dispersion; this supports end-to-end execution with backend, packaging and controller capabilities and helps absorb fixed costs and gain procurement leverage—contributing to Micron’s FY2024 revenue of about 27.7 billion USD and enabling faster ramping across markets.

- Global sites: US, Singapore, Japan, Taiwan

- FY2024 revenue ~27.7B; scale aids cost absorption and procurement leverage

Robust IP portfolio and ecosystem partnerships

Micron’s extensive patents and controller firmware expertise differentiate its products beyond raw bit density, enabling co-optimization of power, reliability and latency for premium sockets and enterprise workloads. Deep partnerships with CPU/GPU vendors and hyperscalers accelerate qualification and adoption, while IP depth raises barriers to entry and helps protect long-term returns.

- Patents/IP moat

- Firmware differentiation

- Hyperscaler & OEM partnerships

- Performance/power co-optimization

Memory leader scales HBM3E, 1-beta/1-gamma DRAM and 232-240+-layer NAND; FY24 ≈27.7B

Micron advances 1‑beta/1‑gamma DRAM nodes and 232–240+ layer NAND, sustaining bit‑cost and power gains for AI/datacenter workloads. FY2024 revenue ≈27.7B and global fabs (US, Singapore, Japan, Taiwan) provide scale and risk dispersion. HBM3E leadership and OEM/hyperscaler design wins boost ASPs and sticky, higher‑value mix (H100 uses up to 80GB vs V100 16GB).

| Metric | Value |

|---|---|

| FY2024 Revenue | ≈27.7B USD |

| NAND | 232–240+ layers |

| DRAM nodes | 1‑beta/1‑gamma |

| HBM | HBM3E; H100 80GB vs V100 16GB |

| Sites | US, Singapore, Japan, Taiwan |

What is included in the product

Provides a concise SWOT framework outlining Micron Technology’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position and future growth.

Provides a concise SWOT matrix for fast strategic alignment around Micron Technology's memory-market dynamics, helping teams prioritize product, capacity and supply-chain actions. Ideal for executives needing a quick, high-level snapshot to streamline decisions and stakeholder communications.

Weaknesses

High cyclicality and ASP volatility

Memory pricing swings—DRAM ASPs plunged roughly 40–50% during the 2022–23 downturn per industry reports—drive sharp revenue and margin fluctuations for Micron. Downcycles have forced inventory write-downs and periodic negative free cash flow, while Micron's annual capital expenditure (typically in the mid-single-digit billions, ~$5–7bn) becomes harder to time. Rapid supply–demand shifts make forecasting difficult and complicate long-term capital planning.

Capital intensity and long payback

Fabs and equipment require multi-billion-dollar investments—advanced DRAM/NAND fabs typically cost $10–20 billion per site— with long lead times that tie up capital. Returns hinge on sustained yield and utilization, and cyclical downturns can submerge margins and extend payback. Any delay in node ramps amplifies depreciation drag; high ongoing capex raises the break-even threshold and strategic risk.

Scale disadvantage vs top competitors

Samsung (≈43% DRAM market share in 2024) and SK hynix (≈30%) wield larger output and cost leverage than Micron (≈21%), especially in DRAM and HBM; their scale enables aggressive pricing in downturns, and Micron’s slower capacity ramp for hot products risks losing share during peak demand windows and compressing margins.

Product commoditization risk

- Limited product differentiation

- Controller/firmware advantages hard to sustain

- Cost-driven customer purchasing

Customer concentration and qualification hurdles

Micron relies heavily on hyperscalers, leading GPU platforms and top handset OEMs, with fiscal 2024 revenue of 30.8 billion USD concentrated in these segments. Losing a design slot or delayed qualification can materially reduce shipments and revenue. Lengthy validation cycles tie up engineering resources and dependence on few buyers magnifies negotiation pressure.

Memory-chip maker hit by volatile DRAM pricing, high capex and scale disadvantage

Micron faces volatile memory pricing (DRAM ASPs fell ~40–50% in 2022–23) causing sharp revenue/margin swings and inventory write-downs; FY2024 revenue ~30.8B. High capex ($5–7B/yr; DRAM/NAND fabs $10–20B/site) and long ramps raise break-even risk. Scale disadvantage versus Samsung ~43% and SK hynix ~30% (Micron ~21%) pressures pricing and share.

| Metric | Value |

|---|---|

| FY2024 revenue | 30.8B |

| DRAM ASP drop (2022–23) | 40–50% |

| Market share (DRAM, 2024) | Samsung ≈43%, SK hynix ≈30%, Micron ≈21% |

Full Version Awaits

Micron Technology SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download after payment.

Dive Deeper Into the Company’s Strategic Blueprint

Micron Technology blends leading memory technology and scale with cyclical market exposure and intense competition, so strategic clarity is vital. Discover the full SWOT analysis for actionable insights, financial context, and risk mitigation strategies. Purchase the complete, editable Word and Excel package to present, plan, and invest with confidence.

Strengths

Leading memory technology roadmap

Micron advances DRAM with 1-beta/1-gamma nodes and 232–240+ layer NAND, boosting density and performance to sustain bit-cost and power-per-bit declines critical for AI and data-center workloads. Leadership across LPDDR5X, DDR5, GDDR and HBM3E aligns with next-gen platforms, while a strong R&D engine and process know-how underpin a durable technology advantage.

Diversified end-market exposure

Micron's FY2024 revenue was about $27.7 billion and spans data center, client, mobile, industrial and automotive, smoothing cycles vs single‑segment peers. Automotive and industrial demand features multi‑year lifecycles and strict quality specs, producing stickier revenue. Growth in AI servers and edge devices is shifting mix toward higher‑value bits, reducing reliance on any single device cycle.

HBM and AI acceleration tailwinds

HBM is critical for AI training and inference, exemplified by NVIDIA H100 using up to 80GB HBM3 versus V100's 16GB HBM2 (≈5x more memory per GPU), driving much higher bit demand. Rising attach rates per GPU are lifting ASPs. Micron's HBM3E ramp positions it in this fastest-growing memory niche. Close alignment with leading AI platform vendors strengthens design-win momentum and a premium mix versus commodity DRAM.

Scale manufacturing and global footprint

Micron’s scale manufacturing spans the U.S., Singapore, Japan and Taiwan, giving capacity flexibility and regional risk dispersion; this supports end-to-end execution with backend, packaging and controller capabilities and helps absorb fixed costs and gain procurement leverage—contributing to Micron’s FY2024 revenue of about 27.7 billion USD and enabling faster ramping across markets.

- Global sites: US, Singapore, Japan, Taiwan

- FY2024 revenue ~27.7B; scale aids cost absorption and procurement leverage

Robust IP portfolio and ecosystem partnerships

Micron’s extensive patents and controller firmware expertise differentiate its products beyond raw bit density, enabling co-optimization of power, reliability and latency for premium sockets and enterprise workloads. Deep partnerships with CPU/GPU vendors and hyperscalers accelerate qualification and adoption, while IP depth raises barriers to entry and helps protect long-term returns.

- Patents/IP moat

- Firmware differentiation

- Hyperscaler & OEM partnerships

- Performance/power co-optimization

Memory leader scales HBM3E, 1-beta/1-gamma DRAM and 232-240+-layer NAND; FY24 ≈27.7B

Micron advances 1‑beta/1‑gamma DRAM nodes and 232–240+ layer NAND, sustaining bit‑cost and power gains for AI/datacenter workloads. FY2024 revenue ≈27.7B and global fabs (US, Singapore, Japan, Taiwan) provide scale and risk dispersion. HBM3E leadership and OEM/hyperscaler design wins boost ASPs and sticky, higher‑value mix (H100 uses up to 80GB vs V100 16GB).

| Metric | Value |

|---|---|

| FY2024 Revenue | ≈27.7B USD |

| NAND | 232–240+ layers |

| DRAM nodes | 1‑beta/1‑gamma |

| HBM | HBM3E; H100 80GB vs V100 16GB |

| Sites | US, Singapore, Japan, Taiwan |

What is included in the product

Provides a concise SWOT framework outlining Micron Technology’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position and future growth.

Provides a concise SWOT matrix for fast strategic alignment around Micron Technology's memory-market dynamics, helping teams prioritize product, capacity and supply-chain actions. Ideal for executives needing a quick, high-level snapshot to streamline decisions and stakeholder communications.

Weaknesses

High cyclicality and ASP volatility

Memory pricing swings—DRAM ASPs plunged roughly 40–50% during the 2022–23 downturn per industry reports—drive sharp revenue and margin fluctuations for Micron. Downcycles have forced inventory write-downs and periodic negative free cash flow, while Micron's annual capital expenditure (typically in the mid-single-digit billions, ~$5–7bn) becomes harder to time. Rapid supply–demand shifts make forecasting difficult and complicate long-term capital planning.

Capital intensity and long payback

Fabs and equipment require multi-billion-dollar investments—advanced DRAM/NAND fabs typically cost $10–20 billion per site— with long lead times that tie up capital. Returns hinge on sustained yield and utilization, and cyclical downturns can submerge margins and extend payback. Any delay in node ramps amplifies depreciation drag; high ongoing capex raises the break-even threshold and strategic risk.

Scale disadvantage vs top competitors

Samsung (≈43% DRAM market share in 2024) and SK hynix (≈30%) wield larger output and cost leverage than Micron (≈21%), especially in DRAM and HBM; their scale enables aggressive pricing in downturns, and Micron’s slower capacity ramp for hot products risks losing share during peak demand windows and compressing margins.

Product commoditization risk

- Limited product differentiation

- Controller/firmware advantages hard to sustain

- Cost-driven customer purchasing

Customer concentration and qualification hurdles

Micron relies heavily on hyperscalers, leading GPU platforms and top handset OEMs, with fiscal 2024 revenue of 30.8 billion USD concentrated in these segments. Losing a design slot or delayed qualification can materially reduce shipments and revenue. Lengthy validation cycles tie up engineering resources and dependence on few buyers magnifies negotiation pressure.

Memory-chip maker hit by volatile DRAM pricing, high capex and scale disadvantage

Micron faces volatile memory pricing (DRAM ASPs fell ~40–50% in 2022–23) causing sharp revenue/margin swings and inventory write-downs; FY2024 revenue ~30.8B. High capex ($5–7B/yr; DRAM/NAND fabs $10–20B/site) and long ramps raise break-even risk. Scale disadvantage versus Samsung ~43% and SK hynix ~30% (Micron ~21%) pressures pricing and share.

| Metric | Value |

|---|---|

| FY2024 revenue | 30.8B |

| DRAM ASP drop (2022–23) | 40–50% |

| Market share (DRAM, 2024) | Samsung ≈43%, SK hynix ≈30%, Micron ≈21% |

Full Version Awaits

Micron Technology SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download after payment.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Micron Technology blends leading memory technology and scale with cyclical market exposure and intense competition, so strategic clarity is vital. Discover the full SWOT analysis for actionable insights, financial context, and risk mitigation strategies. Purchase the complete, editable Word and Excel package to present, plan, and invest with confidence.

Strengths

Leading memory technology roadmap

Micron advances DRAM with 1-beta/1-gamma nodes and 232–240+ layer NAND, boosting density and performance to sustain bit-cost and power-per-bit declines critical for AI and data-center workloads. Leadership across LPDDR5X, DDR5, GDDR and HBM3E aligns with next-gen platforms, while a strong R&D engine and process know-how underpin a durable technology advantage.

Diversified end-market exposure

Micron's FY2024 revenue was about $27.7 billion and spans data center, client, mobile, industrial and automotive, smoothing cycles vs single‑segment peers. Automotive and industrial demand features multi‑year lifecycles and strict quality specs, producing stickier revenue. Growth in AI servers and edge devices is shifting mix toward higher‑value bits, reducing reliance on any single device cycle.

HBM and AI acceleration tailwinds

HBM is critical for AI training and inference, exemplified by NVIDIA H100 using up to 80GB HBM3 versus V100's 16GB HBM2 (≈5x more memory per GPU), driving much higher bit demand. Rising attach rates per GPU are lifting ASPs. Micron's HBM3E ramp positions it in this fastest-growing memory niche. Close alignment with leading AI platform vendors strengthens design-win momentum and a premium mix versus commodity DRAM.

Scale manufacturing and global footprint

Micron’s scale manufacturing spans the U.S., Singapore, Japan and Taiwan, giving capacity flexibility and regional risk dispersion; this supports end-to-end execution with backend, packaging and controller capabilities and helps absorb fixed costs and gain procurement leverage—contributing to Micron’s FY2024 revenue of about 27.7 billion USD and enabling faster ramping across markets.

- Global sites: US, Singapore, Japan, Taiwan

- FY2024 revenue ~27.7B; scale aids cost absorption and procurement leverage

Robust IP portfolio and ecosystem partnerships

Micron’s extensive patents and controller firmware expertise differentiate its products beyond raw bit density, enabling co-optimization of power, reliability and latency for premium sockets and enterprise workloads. Deep partnerships with CPU/GPU vendors and hyperscalers accelerate qualification and adoption, while IP depth raises barriers to entry and helps protect long-term returns.

- Patents/IP moat

- Firmware differentiation

- Hyperscaler & OEM partnerships

- Performance/power co-optimization

Memory leader scales HBM3E, 1-beta/1-gamma DRAM and 232-240+-layer NAND; FY24 ≈27.7B

Micron advances 1‑beta/1‑gamma DRAM nodes and 232–240+ layer NAND, sustaining bit‑cost and power gains for AI/datacenter workloads. FY2024 revenue ≈27.7B and global fabs (US, Singapore, Japan, Taiwan) provide scale and risk dispersion. HBM3E leadership and OEM/hyperscaler design wins boost ASPs and sticky, higher‑value mix (H100 uses up to 80GB vs V100 16GB).

| Metric | Value |

|---|---|

| FY2024 Revenue | ≈27.7B USD |

| NAND | 232–240+ layers |

| DRAM nodes | 1‑beta/1‑gamma |

| HBM | HBM3E; H100 80GB vs V100 16GB |

| Sites | US, Singapore, Japan, Taiwan |

What is included in the product

Provides a concise SWOT framework outlining Micron Technology’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position and future growth.

Provides a concise SWOT matrix for fast strategic alignment around Micron Technology's memory-market dynamics, helping teams prioritize product, capacity and supply-chain actions. Ideal for executives needing a quick, high-level snapshot to streamline decisions and stakeholder communications.

Weaknesses

High cyclicality and ASP volatility

Memory pricing swings—DRAM ASPs plunged roughly 40–50% during the 2022–23 downturn per industry reports—drive sharp revenue and margin fluctuations for Micron. Downcycles have forced inventory write-downs and periodic negative free cash flow, while Micron's annual capital expenditure (typically in the mid-single-digit billions, ~$5–7bn) becomes harder to time. Rapid supply–demand shifts make forecasting difficult and complicate long-term capital planning.

Capital intensity and long payback

Fabs and equipment require multi-billion-dollar investments—advanced DRAM/NAND fabs typically cost $10–20 billion per site— with long lead times that tie up capital. Returns hinge on sustained yield and utilization, and cyclical downturns can submerge margins and extend payback. Any delay in node ramps amplifies depreciation drag; high ongoing capex raises the break-even threshold and strategic risk.

Scale disadvantage vs top competitors

Samsung (≈43% DRAM market share in 2024) and SK hynix (≈30%) wield larger output and cost leverage than Micron (≈21%), especially in DRAM and HBM; their scale enables aggressive pricing in downturns, and Micron’s slower capacity ramp for hot products risks losing share during peak demand windows and compressing margins.

Product commoditization risk

- Limited product differentiation

- Controller/firmware advantages hard to sustain

- Cost-driven customer purchasing

Customer concentration and qualification hurdles

Micron relies heavily on hyperscalers, leading GPU platforms and top handset OEMs, with fiscal 2024 revenue of 30.8 billion USD concentrated in these segments. Losing a design slot or delayed qualification can materially reduce shipments and revenue. Lengthy validation cycles tie up engineering resources and dependence on few buyers magnifies negotiation pressure.

Memory-chip maker hit by volatile DRAM pricing, high capex and scale disadvantage

Micron faces volatile memory pricing (DRAM ASPs fell ~40–50% in 2022–23) causing sharp revenue/margin swings and inventory write-downs; FY2024 revenue ~30.8B. High capex ($5–7B/yr; DRAM/NAND fabs $10–20B/site) and long ramps raise break-even risk. Scale disadvantage versus Samsung ~43% and SK hynix ~30% (Micron ~21%) pressures pricing and share.

| Metric | Value |

|---|---|

| FY2024 revenue | 30.8B |

| DRAM ASP drop (2022–23) | 40–50% |

| Market share (DRAM, 2024) | Samsung ≈43%, SK hynix ≈30%, Micron ≈21% |

Full Version Awaits

Micron Technology SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real, editable SWOT analysis you'll download after payment.