MicroStrategy Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

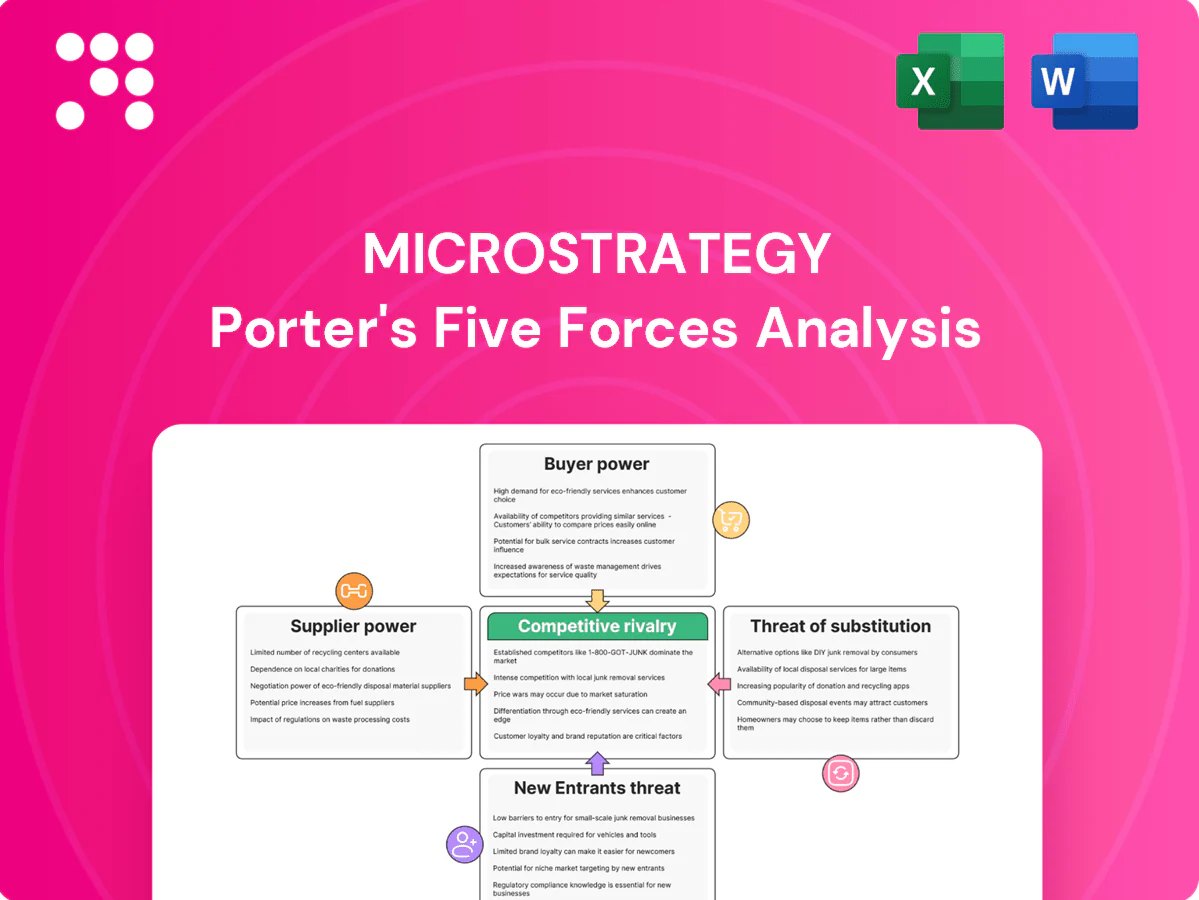

MicroStrategy faces high buyer sensitivity due to enterprise analytics alternatives, moderate threat from new entrants given platform complexity, strong supplier leverage in data providers, and significant substitute pressure from open-source BI; competitive rivalry is intense among established analytics firms. Unlock the full Porter's Five Forces Analysis to explore MicroStrategy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud infrastructure leverage

MicroStrategy relies on hyperscalers for hosting, compute and storage, concentrating supplier power given AWS, Microsoft and Google held roughly 33%, 22% and 11% of the cloud market in 2024. Reserved instances and multi-cloud strategies reduce but do not remove pricing exposure and capacity lock-in. Egress charges and proprietary APIs raise switching costs across clouds. Service outages or policy shifts can cascade into SLAs and compress margins.

Data platform dependencies

Connectivity to Snowflake, Databricks, BigQuery and SQL Server is mission-critical for MicroStrategy’s deployment and retention. Snowflake reported $2.07B revenue in FY2024 and Databricks carried a ~43B valuation, so API or pricing shifts can quickly tilt leverage to platform providers. Native BI bundling (eg. Power BI, Looker) compresses attach rates and value capture; certifications and joint GTM lower but do not remove supplier power.

Talent and specialized engineers

Highly skilled analytics, mobile, and security engineers act as scarce suppliers to MicroStrategy, with the U.S. Bureau of Labor Statistics reporting a May 2023 median wage for software developers of $120,730 and a projected 22% employment growth 2022–32, fueling wage pressure. Tight labor markets raise retention risk and replacement costs as knowledge concentrates in small teams. Remote hiring widens the pool but intensifies global competition and ramp time.

Open-source and component stacks

MicroStrategy integrates and competes with open-source tools; 96% of enterprises used OSS in 2024 (Synopsys). While direct license costs are low, roadmap shifts and community dynamics create supply risk and potential feature divergence. Forking or replacing components requires notable engineering capacity, and 85% of apps had OSS vulnerabilities in 2024, forcing unplanned remediation and support costs.

- OSS adoption: 96% (Synopsys 2024)

- Vulnerabilities: 85% of apps affected (Synopsys 2024)

- Risks: roadmap shifts, forking cost, emergency security work

Crypto custody and liquidity rails

MicroStrategy’s large bitcoin position—over 190,000 BTC per 2024 SEC disclosures—creates dependence on custodians, trading venues and auditors, making fees and custody terms material to treasury flexibility. Regulatory shifts and margin rules for custodians can constrain liquidity access, and stressed markets have widened BTC spreads and slippage, raising indirect costs. Operational custody and settlement dependencies represent a supplier risk uncommon to pure-play software peers.

- Custody concentration: reliance on regulated custodians

- Liquidity risk: wider spreads/slippage in stress

- Fee exposure: custody and trading costs affect returns

- Operational vendor risk vs software peers

Firm exposed to supplier concentration: AWS 33%/Azure 22%/GCP 11%, OSS 96%, 190,000+ BTC

MicroStrategy faces concentrated supplier power from hyperscalers (AWS 33%, Azure 22%, GCP 11% cloud share 2024), key data platforms (Snowflake $2.07B rev FY2024; Databricks ~$43B valuation) and scarce engineering talent (median dev wage $120,730 May 2023). OSS reliance (96% adop. 2024) and 190,000+ BTC custody exposure amplify vendor and operational risks.

| Supplier | Metric | 2024 |

|---|---|---|

| Hyperscalers | Market share | AWS 33%/Azure 22%/GCP 11% |

| Data platforms | Scale | Snowflake $2.07B/Databricks $43B |

| OSS | Adoption | 96% (Synopsys) |

| Bitcoin | Holding | 190,000+ BTC |

What is included in the product

Tailored Porter's Five Forces analysis for MicroStrategy that uncovers key drivers of competition, customer influence, and market entry risks specific to its enterprise-software and bitcoin-centric strategy. Identifies disruptive substitutes, supplier/buyer power, and barriers protecting incumbents, with strategic commentary for investor and management use.

A clear one-sheet Porter's Five Forces for MicroStrategy—quickly visualize competitive pressure with an interactive radar and customize force levels for regulatory shifts, Bitcoin volatility, or new entrants to relieve strategic pain points.

Customers Bargaining Power

Enterprise CIOs demand value

Large enterprise CIOs push MicroStrategy hard on price, support SLAs, and product roadmap influence, often leveraging consolidation of analytics standards in 2024 to secure stronger terms. Multi-year contracts and platform breadth temper discounting but do not eliminate it, as demonstrable ROI and lower total cost of ownership drive renewal decisions. Buyers increasingly demand quantifiable outcomes tied to spend, making value proof central to negotiations.

Abundant alternatives

Buyers can pivot to Power BI, Tableau, Looker and Qlik, with Gartner's 2024 Magic Quadrant again ranking Microsoft, Salesforce (Tableau) and Qlik among leaders, increasing buyer leverage. Hyperscaler bundled pricing from AWS/Azure/GCP compresses standalone BI margins and pressures MicroStrategy's pricing. Feature parity in dashboards and self-service analytics narrows differentiation. Switching is feasible when data models and pipelines are decoupled, lowering migration cost.

Switching costs vary

Embedded analytics, semantic layers, and governance in MicroStrategy drive high stickiness—supporting roughly 3,600 enterprise customers as of 2024—by centralizing metadata and access controls. Lightweight dashboarding with minimal customization lowers exit barriers for smaller users. Extensive professional services and training deepen entrenchment among large clients. Rivals’ migration tooling and cloud-native alternatives in 2024 increasingly target these moats.

Price sensitivity and seat mix

Viewer-heavy deployments erode average revenue per user as passive users dilute seat-based pricing, so per-user and capacity pricing must match utilization patterns to protect margins. Economic downturns prompt customers to optimize seats and consolidate licenses, increasing bargaining power. Competitors offering usage-based models recalibrate customer expectations, pressuring MicroStrategy to adapt pricing flexibility.

- Viewer-heavy deployments reduce ARPU

- Pricing must align with utilization

- Economic cycles drive seat consolidation

- Usage-based competitors reset expectations

Security and compliance requirements

Regulated industries demand certifications and data residency controls, and failure to meet standards like GDPR or HIPAA can immediately disqualify MicroStrategy from consideration. Strong governance and audit features let MicroStrategy command premium positioning among buyers seeking certified platforms. Buyers routinely use compliance gaps as leverage to drive price concessions or stricter SLAs.

- Compliance as gatekeeper

- Data residency requirement

- Premium for strong governance

- Negotiation leverage

Buyers gain leverage as 2024 consolidation raises pricing, compliance and ROI demands

Buyers hold moderate-to-high power: 2024 consolidation to Microsoft, Salesforce (Tableau) and Qlik in Gartner leaders increases leverage, while MicroStrategy's 3,600 enterprise customers create stickiness via governance and semantic layers. Cost, ROI proof, compliance (GDPR/HIPAA) and usage-based rivals drive tougher pricing and SLA demands.

| Metric | Impact | 2024 Evidence |

|---|---|---|

| Enterprise customers | Stickiness | 3,600 |

| Market leaders | Buyer leverage | Microsoft, Tableau, Qlik (Gartner 2024) |

Preview the Actual Deliverable

MicroStrategy Porter's Five Forces Analysis

This preview shows the exact MicroStrategy Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the full, professionally formatted assessment of competitive pressures, ready for instant download and use. Purchase grants immediate access to this identical file.

A Must-Have Tool for Decision-Makers

MicroStrategy faces high buyer sensitivity due to enterprise analytics alternatives, moderate threat from new entrants given platform complexity, strong supplier leverage in data providers, and significant substitute pressure from open-source BI; competitive rivalry is intense among established analytics firms. Unlock the full Porter's Five Forces Analysis to explore MicroStrategy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud infrastructure leverage

MicroStrategy relies on hyperscalers for hosting, compute and storage, concentrating supplier power given AWS, Microsoft and Google held roughly 33%, 22% and 11% of the cloud market in 2024. Reserved instances and multi-cloud strategies reduce but do not remove pricing exposure and capacity lock-in. Egress charges and proprietary APIs raise switching costs across clouds. Service outages or policy shifts can cascade into SLAs and compress margins.

Data platform dependencies

Connectivity to Snowflake, Databricks, BigQuery and SQL Server is mission-critical for MicroStrategy’s deployment and retention. Snowflake reported $2.07B revenue in FY2024 and Databricks carried a ~43B valuation, so API or pricing shifts can quickly tilt leverage to platform providers. Native BI bundling (eg. Power BI, Looker) compresses attach rates and value capture; certifications and joint GTM lower but do not remove supplier power.

Talent and specialized engineers

Highly skilled analytics, mobile, and security engineers act as scarce suppliers to MicroStrategy, with the U.S. Bureau of Labor Statistics reporting a May 2023 median wage for software developers of $120,730 and a projected 22% employment growth 2022–32, fueling wage pressure. Tight labor markets raise retention risk and replacement costs as knowledge concentrates in small teams. Remote hiring widens the pool but intensifies global competition and ramp time.

Open-source and component stacks

MicroStrategy integrates and competes with open-source tools; 96% of enterprises used OSS in 2024 (Synopsys). While direct license costs are low, roadmap shifts and community dynamics create supply risk and potential feature divergence. Forking or replacing components requires notable engineering capacity, and 85% of apps had OSS vulnerabilities in 2024, forcing unplanned remediation and support costs.

- OSS adoption: 96% (Synopsys 2024)

- Vulnerabilities: 85% of apps affected (Synopsys 2024)

- Risks: roadmap shifts, forking cost, emergency security work

Crypto custody and liquidity rails

MicroStrategy’s large bitcoin position—over 190,000 BTC per 2024 SEC disclosures—creates dependence on custodians, trading venues and auditors, making fees and custody terms material to treasury flexibility. Regulatory shifts and margin rules for custodians can constrain liquidity access, and stressed markets have widened BTC spreads and slippage, raising indirect costs. Operational custody and settlement dependencies represent a supplier risk uncommon to pure-play software peers.

- Custody concentration: reliance on regulated custodians

- Liquidity risk: wider spreads/slippage in stress

- Fee exposure: custody and trading costs affect returns

- Operational vendor risk vs software peers

Firm exposed to supplier concentration: AWS 33%/Azure 22%/GCP 11%, OSS 96%, 190,000+ BTC

MicroStrategy faces concentrated supplier power from hyperscalers (AWS 33%, Azure 22%, GCP 11% cloud share 2024), key data platforms (Snowflake $2.07B rev FY2024; Databricks ~$43B valuation) and scarce engineering talent (median dev wage $120,730 May 2023). OSS reliance (96% adop. 2024) and 190,000+ BTC custody exposure amplify vendor and operational risks.

| Supplier | Metric | 2024 |

|---|---|---|

| Hyperscalers | Market share | AWS 33%/Azure 22%/GCP 11% |

| Data platforms | Scale | Snowflake $2.07B/Databricks $43B |

| OSS | Adoption | 96% (Synopsys) |

| Bitcoin | Holding | 190,000+ BTC |

What is included in the product

Tailored Porter's Five Forces analysis for MicroStrategy that uncovers key drivers of competition, customer influence, and market entry risks specific to its enterprise-software and bitcoin-centric strategy. Identifies disruptive substitutes, supplier/buyer power, and barriers protecting incumbents, with strategic commentary for investor and management use.

A clear one-sheet Porter's Five Forces for MicroStrategy—quickly visualize competitive pressure with an interactive radar and customize force levels for regulatory shifts, Bitcoin volatility, or new entrants to relieve strategic pain points.

Customers Bargaining Power

Enterprise CIOs demand value

Large enterprise CIOs push MicroStrategy hard on price, support SLAs, and product roadmap influence, often leveraging consolidation of analytics standards in 2024 to secure stronger terms. Multi-year contracts and platform breadth temper discounting but do not eliminate it, as demonstrable ROI and lower total cost of ownership drive renewal decisions. Buyers increasingly demand quantifiable outcomes tied to spend, making value proof central to negotiations.

Abundant alternatives

Buyers can pivot to Power BI, Tableau, Looker and Qlik, with Gartner's 2024 Magic Quadrant again ranking Microsoft, Salesforce (Tableau) and Qlik among leaders, increasing buyer leverage. Hyperscaler bundled pricing from AWS/Azure/GCP compresses standalone BI margins and pressures MicroStrategy's pricing. Feature parity in dashboards and self-service analytics narrows differentiation. Switching is feasible when data models and pipelines are decoupled, lowering migration cost.

Switching costs vary

Embedded analytics, semantic layers, and governance in MicroStrategy drive high stickiness—supporting roughly 3,600 enterprise customers as of 2024—by centralizing metadata and access controls. Lightweight dashboarding with minimal customization lowers exit barriers for smaller users. Extensive professional services and training deepen entrenchment among large clients. Rivals’ migration tooling and cloud-native alternatives in 2024 increasingly target these moats.

Price sensitivity and seat mix

Viewer-heavy deployments erode average revenue per user as passive users dilute seat-based pricing, so per-user and capacity pricing must match utilization patterns to protect margins. Economic downturns prompt customers to optimize seats and consolidate licenses, increasing bargaining power. Competitors offering usage-based models recalibrate customer expectations, pressuring MicroStrategy to adapt pricing flexibility.

- Viewer-heavy deployments reduce ARPU

- Pricing must align with utilization

- Economic cycles drive seat consolidation

- Usage-based competitors reset expectations

Security and compliance requirements

Regulated industries demand certifications and data residency controls, and failure to meet standards like GDPR or HIPAA can immediately disqualify MicroStrategy from consideration. Strong governance and audit features let MicroStrategy command premium positioning among buyers seeking certified platforms. Buyers routinely use compliance gaps as leverage to drive price concessions or stricter SLAs.

- Compliance as gatekeeper

- Data residency requirement

- Premium for strong governance

- Negotiation leverage

Buyers gain leverage as 2024 consolidation raises pricing, compliance and ROI demands

Buyers hold moderate-to-high power: 2024 consolidation to Microsoft, Salesforce (Tableau) and Qlik in Gartner leaders increases leverage, while MicroStrategy's 3,600 enterprise customers create stickiness via governance and semantic layers. Cost, ROI proof, compliance (GDPR/HIPAA) and usage-based rivals drive tougher pricing and SLA demands.

| Metric | Impact | 2024 Evidence |

|---|---|---|

| Enterprise customers | Stickiness | 3,600 |

| Market leaders | Buyer leverage | Microsoft, Tableau, Qlik (Gartner 2024) |

Preview the Actual Deliverable

MicroStrategy Porter's Five Forces Analysis

This preview shows the exact MicroStrategy Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the full, professionally formatted assessment of competitive pressures, ready for instant download and use. Purchase grants immediate access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

MicroStrategy faces high buyer sensitivity due to enterprise analytics alternatives, moderate threat from new entrants given platform complexity, strong supplier leverage in data providers, and significant substitute pressure from open-source BI; competitive rivalry is intense among established analytics firms. Unlock the full Porter's Five Forces Analysis to explore MicroStrategy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud infrastructure leverage

MicroStrategy relies on hyperscalers for hosting, compute and storage, concentrating supplier power given AWS, Microsoft and Google held roughly 33%, 22% and 11% of the cloud market in 2024. Reserved instances and multi-cloud strategies reduce but do not remove pricing exposure and capacity lock-in. Egress charges and proprietary APIs raise switching costs across clouds. Service outages or policy shifts can cascade into SLAs and compress margins.

Data platform dependencies

Connectivity to Snowflake, Databricks, BigQuery and SQL Server is mission-critical for MicroStrategy’s deployment and retention. Snowflake reported $2.07B revenue in FY2024 and Databricks carried a ~43B valuation, so API or pricing shifts can quickly tilt leverage to platform providers. Native BI bundling (eg. Power BI, Looker) compresses attach rates and value capture; certifications and joint GTM lower but do not remove supplier power.

Talent and specialized engineers

Highly skilled analytics, mobile, and security engineers act as scarce suppliers to MicroStrategy, with the U.S. Bureau of Labor Statistics reporting a May 2023 median wage for software developers of $120,730 and a projected 22% employment growth 2022–32, fueling wage pressure. Tight labor markets raise retention risk and replacement costs as knowledge concentrates in small teams. Remote hiring widens the pool but intensifies global competition and ramp time.

Open-source and component stacks

MicroStrategy integrates and competes with open-source tools; 96% of enterprises used OSS in 2024 (Synopsys). While direct license costs are low, roadmap shifts and community dynamics create supply risk and potential feature divergence. Forking or replacing components requires notable engineering capacity, and 85% of apps had OSS vulnerabilities in 2024, forcing unplanned remediation and support costs.

- OSS adoption: 96% (Synopsys 2024)

- Vulnerabilities: 85% of apps affected (Synopsys 2024)

- Risks: roadmap shifts, forking cost, emergency security work

Crypto custody and liquidity rails

MicroStrategy’s large bitcoin position—over 190,000 BTC per 2024 SEC disclosures—creates dependence on custodians, trading venues and auditors, making fees and custody terms material to treasury flexibility. Regulatory shifts and margin rules for custodians can constrain liquidity access, and stressed markets have widened BTC spreads and slippage, raising indirect costs. Operational custody and settlement dependencies represent a supplier risk uncommon to pure-play software peers.

- Custody concentration: reliance on regulated custodians

- Liquidity risk: wider spreads/slippage in stress

- Fee exposure: custody and trading costs affect returns

- Operational vendor risk vs software peers

Firm exposed to supplier concentration: AWS 33%/Azure 22%/GCP 11%, OSS 96%, 190,000+ BTC

MicroStrategy faces concentrated supplier power from hyperscalers (AWS 33%, Azure 22%, GCP 11% cloud share 2024), key data platforms (Snowflake $2.07B rev FY2024; Databricks ~$43B valuation) and scarce engineering talent (median dev wage $120,730 May 2023). OSS reliance (96% adop. 2024) and 190,000+ BTC custody exposure amplify vendor and operational risks.

| Supplier | Metric | 2024 |

|---|---|---|

| Hyperscalers | Market share | AWS 33%/Azure 22%/GCP 11% |

| Data platforms | Scale | Snowflake $2.07B/Databricks $43B |

| OSS | Adoption | 96% (Synopsys) |

| Bitcoin | Holding | 190,000+ BTC |

What is included in the product

Tailored Porter's Five Forces analysis for MicroStrategy that uncovers key drivers of competition, customer influence, and market entry risks specific to its enterprise-software and bitcoin-centric strategy. Identifies disruptive substitutes, supplier/buyer power, and barriers protecting incumbents, with strategic commentary for investor and management use.

A clear one-sheet Porter's Five Forces for MicroStrategy—quickly visualize competitive pressure with an interactive radar and customize force levels for regulatory shifts, Bitcoin volatility, or new entrants to relieve strategic pain points.

Customers Bargaining Power

Enterprise CIOs demand value

Large enterprise CIOs push MicroStrategy hard on price, support SLAs, and product roadmap influence, often leveraging consolidation of analytics standards in 2024 to secure stronger terms. Multi-year contracts and platform breadth temper discounting but do not eliminate it, as demonstrable ROI and lower total cost of ownership drive renewal decisions. Buyers increasingly demand quantifiable outcomes tied to spend, making value proof central to negotiations.

Abundant alternatives

Buyers can pivot to Power BI, Tableau, Looker and Qlik, with Gartner's 2024 Magic Quadrant again ranking Microsoft, Salesforce (Tableau) and Qlik among leaders, increasing buyer leverage. Hyperscaler bundled pricing from AWS/Azure/GCP compresses standalone BI margins and pressures MicroStrategy's pricing. Feature parity in dashboards and self-service analytics narrows differentiation. Switching is feasible when data models and pipelines are decoupled, lowering migration cost.

Switching costs vary

Embedded analytics, semantic layers, and governance in MicroStrategy drive high stickiness—supporting roughly 3,600 enterprise customers as of 2024—by centralizing metadata and access controls. Lightweight dashboarding with minimal customization lowers exit barriers for smaller users. Extensive professional services and training deepen entrenchment among large clients. Rivals’ migration tooling and cloud-native alternatives in 2024 increasingly target these moats.

Price sensitivity and seat mix

Viewer-heavy deployments erode average revenue per user as passive users dilute seat-based pricing, so per-user and capacity pricing must match utilization patterns to protect margins. Economic downturns prompt customers to optimize seats and consolidate licenses, increasing bargaining power. Competitors offering usage-based models recalibrate customer expectations, pressuring MicroStrategy to adapt pricing flexibility.

- Viewer-heavy deployments reduce ARPU

- Pricing must align with utilization

- Economic cycles drive seat consolidation

- Usage-based competitors reset expectations

Security and compliance requirements

Regulated industries demand certifications and data residency controls, and failure to meet standards like GDPR or HIPAA can immediately disqualify MicroStrategy from consideration. Strong governance and audit features let MicroStrategy command premium positioning among buyers seeking certified platforms. Buyers routinely use compliance gaps as leverage to drive price concessions or stricter SLAs.

- Compliance as gatekeeper

- Data residency requirement

- Premium for strong governance

- Negotiation leverage

Buyers gain leverage as 2024 consolidation raises pricing, compliance and ROI demands

Buyers hold moderate-to-high power: 2024 consolidation to Microsoft, Salesforce (Tableau) and Qlik in Gartner leaders increases leverage, while MicroStrategy's 3,600 enterprise customers create stickiness via governance and semantic layers. Cost, ROI proof, compliance (GDPR/HIPAA) and usage-based rivals drive tougher pricing and SLA demands.

| Metric | Impact | 2024 Evidence |

|---|---|---|

| Enterprise customers | Stickiness | 3,600 |

| Market leaders | Buyer leverage | Microsoft, Tableau, Qlik (Gartner 2024) |

Preview the Actual Deliverable

MicroStrategy Porter's Five Forces Analysis

This preview shows the exact MicroStrategy Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the full, professionally formatted assessment of competitive pressures, ready for instant download and use. Purchase grants immediate access to this identical file.