Mincon Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

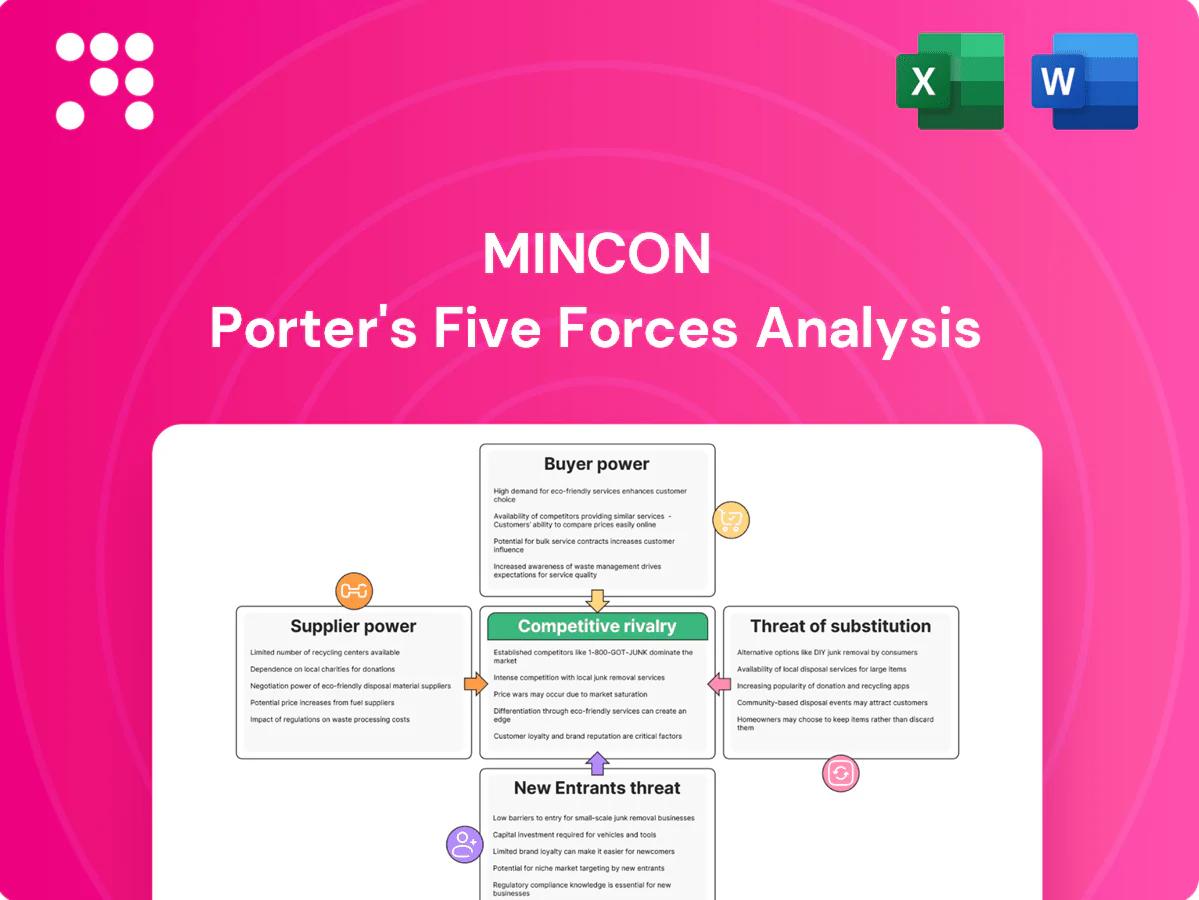

Mincon faces nuanced pressures from suppliers, buyers, new entrants and substitutes that shape margins and growth prospects. Our snapshot highlights key competitive dynamics and strategic risks specific to Mincon. Want force-by-force ratings, visuals and actionable implications? Unlock the full Porter's Five Forces Analysis to explore Mincon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty metals and carbide concentration

Mincon depends on high-grade alloy steels and tungsten carbide sourced from a concentrated supplier base, with China supplying roughly 80% of global tungsten concentrate in 2024, giving suppliers significant leverage. Limited qualified alternatives and typical lead times of 12–20 weeks elevate risk and bargaining power. Metal price volatility has historically squeezed margins, making hedging important. Strategic partnerships and dual-sourcing are used to mitigate supply and price exposure.

Process-intensive components and treatments

Heat treatment, precision machining and hard-facing are critical to tool performance, and a small pool of qualified vendors with tight tolerances and certifications raises switching costs; any deviation causes field failures and warranty expense, so vertical integration or in-house capability is used to reduce exposure.

Logistics complexity across regions

Global distribution to mining and HDD hubs relies on reliable freight and customs brokers; after 2021-22 peak turmoil, container freight rates in 2024 remained roughly 60–70% below peak but still volatile, so disruptions quickly raise input and shipping costs that suppliers can pass through. Regionalization buffers shocks but often reduces scale economies, and vendor-managed inventory programs, which can cut inventory variability by up to 30%, help smooth supply swings.

Proprietary subcomponents and seals

High-performance hammers and bits use specialized seals, brazing materials and inserts, creating reliance on niche suppliers. Proprietary specifications limit the vendor pool and increase supplier bargaining power. Qualification cycles often exceed 12 months, delaying substitutions, while multi-year framework agreements can lock pricing and capacity.

- Supplier concentration: niche components

- Qualification time: >12 months

- Contracting: multi-year frameworks

ESG and compliance obligations

ESG and compliance obligations like conflict-free tungsten, REACH conformity and third-party sustainability audits have narrowed eligible suppliers, raising oversight and switching barriers; by 2024 many OEMs intensified supplier audits and passed compliance tasks downstream in tight markets, shifting cost burdens and elevating failure risk. Collaborative compliance programs between Mincon and OEMs can align incentives and reduce per-supplier cost.

- narrow supplier pool: conflict-free + REACH

- cost shift: OEMs absorb compliance in tight markets

- risk: failure increases oversight & switching barriers

- solution: collaborative compliance lowers unit cost

China ~80% tungsten dominance raises supplier leverage; dual sourcing cuts stock 30%

Mincon relies on concentrated suppliers—China supplied ~80% of global tungsten concentrate in 2024—giving suppliers strong leverage. Long lead times (12–20 weeks) and >12‑month qualification cycles raise switching costs. Freight volatility and metal price swings compress margins. VMI or dual‑sourcing can cut inventory variability by up to 30%.

What is included in the product

Uncovers key competitive drivers, supplier and buyer power, substitutes and entry threats specific to Mincon, with strategic commentary and industry data to assess pricing power, profitability and market resilience.

A one-sheet Mincon Porter’s Five Forces that simplifies competitive pressure into adjustable scores and a radar chart—ideal for quick strategic decisions, slide-ready summaries, and seamless integration into reports or dashboards.

Customers Bargaining Power

Large industrial buyers and tenders

Mining houses, quarry groups and HDD contractors increasingly purchase via RFQs and multi-year tenders, with aggregated volumes giving buyers strong pricing leverage and requirement for service-level commitments. In 2024 large tenders continued to compress margins as competitive benchmarking and supplier scorecards intensified discount pressure. Suppliers defend price by offering value-added services and performance guarantees tied to uptime and lifecycle cost metrics.

Performance-critical, cost-per-meter focus

Buyers optimize total cost-per-meter rather than unit price, with 2024 industry analyses indicating that 10–30% higher penetration rates and 5–15% greater uptime can cut drilling cost-per-meter materially. Superior tool durability and proven lifecycle economics—often reducing total drilling lifecycle cost by around 10–20% in field studies—erode buyer bargaining power. Data logging and on-site trials are pivotal: validated trial data in 2024 became a primary procurement requirement to justify premium pricing.

Interchangeability and switching costs

Many downhole tools fit industry-standard rigs enabling cross-brand substitution, but real-world switching typically costs operators days–weeks of trial downtime and retraining in 2024. Embedded service agreements and on-site spares increase lock-in by shortening mean time to replace equipment. Contractual rebates and consignment stock further reduce churn by smoothing cash flow and inventory availability.

Aftermarket service expectations

- rapid support

- local inventory

- service SLAs

- uptime KPIs

Cyclical demand and budgeting

Cyclical commodity swings and construction seasonality drive buyer urgency; with IMF 2024 global growth at 3.1% softer demand amplifies buyer leverage in downturns. Buyers push for lower prices and extended payment terms in recessions, while upcycles reduce negotiating power as urgency rises. Flexible financing and a ~$140bn global equipment rental market in 2024 help smooth these swings.

- Buyers gain leverage in downturns

- Upcycles reduce buyer negotiating power

- Financing and rentals (~$140bn 2024) smooth volatility

Buyers leverage RFQs, tenders compress margins; rentals & durability cut lifecycle costs

Buyers wield strong leverage via RFQs and multi-year tenders; 2024 tendering compressed margins as benchmarking intensified. Procurement focuses on total cost-per-meter; field studies show 10–20% lifecycle cost savings for higher-durability tools. Real switching costs (days–weeks) and service coverage curb churn. Downturns amplify buyer power (IMF 2024 growth 3.1%); rentals soften volatility (~$140bn 2024).

| Metric | 2024 |

|---|---|

| IMF global growth | 3.1% |

| Rental market | $140bn |

| Lifecycle cost savings | 10–20% |

| Uptime gains | 5–15% |

Same Document Delivered

Mincon Porter's Five Forces Analysis

This preview displays the Mincon Porter's Five Forces Analysis exactly as delivered after purchase, with full methodology, findings, and implications. The document is professionally formatted and ready for immediate download and use. No placeholders or mockups—what you see is what you get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Mincon faces nuanced pressures from suppliers, buyers, new entrants and substitutes that shape margins and growth prospects. Our snapshot highlights key competitive dynamics and strategic risks specific to Mincon. Want force-by-force ratings, visuals and actionable implications? Unlock the full Porter's Five Forces Analysis to explore Mincon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty metals and carbide concentration

Mincon depends on high-grade alloy steels and tungsten carbide sourced from a concentrated supplier base, with China supplying roughly 80% of global tungsten concentrate in 2024, giving suppliers significant leverage. Limited qualified alternatives and typical lead times of 12–20 weeks elevate risk and bargaining power. Metal price volatility has historically squeezed margins, making hedging important. Strategic partnerships and dual-sourcing are used to mitigate supply and price exposure.

Process-intensive components and treatments

Heat treatment, precision machining and hard-facing are critical to tool performance, and a small pool of qualified vendors with tight tolerances and certifications raises switching costs; any deviation causes field failures and warranty expense, so vertical integration or in-house capability is used to reduce exposure.

Logistics complexity across regions

Global distribution to mining and HDD hubs relies on reliable freight and customs brokers; after 2021-22 peak turmoil, container freight rates in 2024 remained roughly 60–70% below peak but still volatile, so disruptions quickly raise input and shipping costs that suppliers can pass through. Regionalization buffers shocks but often reduces scale economies, and vendor-managed inventory programs, which can cut inventory variability by up to 30%, help smooth supply swings.

Proprietary subcomponents and seals

High-performance hammers and bits use specialized seals, brazing materials and inserts, creating reliance on niche suppliers. Proprietary specifications limit the vendor pool and increase supplier bargaining power. Qualification cycles often exceed 12 months, delaying substitutions, while multi-year framework agreements can lock pricing and capacity.

- Supplier concentration: niche components

- Qualification time: >12 months

- Contracting: multi-year frameworks

ESG and compliance obligations

ESG and compliance obligations like conflict-free tungsten, REACH conformity and third-party sustainability audits have narrowed eligible suppliers, raising oversight and switching barriers; by 2024 many OEMs intensified supplier audits and passed compliance tasks downstream in tight markets, shifting cost burdens and elevating failure risk. Collaborative compliance programs between Mincon and OEMs can align incentives and reduce per-supplier cost.

- narrow supplier pool: conflict-free + REACH

- cost shift: OEMs absorb compliance in tight markets

- risk: failure increases oversight & switching barriers

- solution: collaborative compliance lowers unit cost

China ~80% tungsten dominance raises supplier leverage; dual sourcing cuts stock 30%

Mincon relies on concentrated suppliers—China supplied ~80% of global tungsten concentrate in 2024—giving suppliers strong leverage. Long lead times (12–20 weeks) and >12‑month qualification cycles raise switching costs. Freight volatility and metal price swings compress margins. VMI or dual‑sourcing can cut inventory variability by up to 30%.

What is included in the product

Uncovers key competitive drivers, supplier and buyer power, substitutes and entry threats specific to Mincon, with strategic commentary and industry data to assess pricing power, profitability and market resilience.

A one-sheet Mincon Porter’s Five Forces that simplifies competitive pressure into adjustable scores and a radar chart—ideal for quick strategic decisions, slide-ready summaries, and seamless integration into reports or dashboards.

Customers Bargaining Power

Large industrial buyers and tenders

Mining houses, quarry groups and HDD contractors increasingly purchase via RFQs and multi-year tenders, with aggregated volumes giving buyers strong pricing leverage and requirement for service-level commitments. In 2024 large tenders continued to compress margins as competitive benchmarking and supplier scorecards intensified discount pressure. Suppliers defend price by offering value-added services and performance guarantees tied to uptime and lifecycle cost metrics.

Performance-critical, cost-per-meter focus

Buyers optimize total cost-per-meter rather than unit price, with 2024 industry analyses indicating that 10–30% higher penetration rates and 5–15% greater uptime can cut drilling cost-per-meter materially. Superior tool durability and proven lifecycle economics—often reducing total drilling lifecycle cost by around 10–20% in field studies—erode buyer bargaining power. Data logging and on-site trials are pivotal: validated trial data in 2024 became a primary procurement requirement to justify premium pricing.

Interchangeability and switching costs

Many downhole tools fit industry-standard rigs enabling cross-brand substitution, but real-world switching typically costs operators days–weeks of trial downtime and retraining in 2024. Embedded service agreements and on-site spares increase lock-in by shortening mean time to replace equipment. Contractual rebates and consignment stock further reduce churn by smoothing cash flow and inventory availability.

Aftermarket service expectations

- rapid support

- local inventory

- service SLAs

- uptime KPIs

Cyclical demand and budgeting

Cyclical commodity swings and construction seasonality drive buyer urgency; with IMF 2024 global growth at 3.1% softer demand amplifies buyer leverage in downturns. Buyers push for lower prices and extended payment terms in recessions, while upcycles reduce negotiating power as urgency rises. Flexible financing and a ~$140bn global equipment rental market in 2024 help smooth these swings.

- Buyers gain leverage in downturns

- Upcycles reduce buyer negotiating power

- Financing and rentals (~$140bn 2024) smooth volatility

Buyers leverage RFQs, tenders compress margins; rentals & durability cut lifecycle costs

Buyers wield strong leverage via RFQs and multi-year tenders; 2024 tendering compressed margins as benchmarking intensified. Procurement focuses on total cost-per-meter; field studies show 10–20% lifecycle cost savings for higher-durability tools. Real switching costs (days–weeks) and service coverage curb churn. Downturns amplify buyer power (IMF 2024 growth 3.1%); rentals soften volatility (~$140bn 2024).

| Metric | 2024 |

|---|---|

| IMF global growth | 3.1% |

| Rental market | $140bn |

| Lifecycle cost savings | 10–20% |

| Uptime gains | 5–15% |

Same Document Delivered

Mincon Porter's Five Forces Analysis

This preview displays the Mincon Porter's Five Forces Analysis exactly as delivered after purchase, with full methodology, findings, and implications. The document is professionally formatted and ready for immediate download and use. No placeholders or mockups—what you see is what you get.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Mincon faces nuanced pressures from suppliers, buyers, new entrants and substitutes that shape margins and growth prospects. Our snapshot highlights key competitive dynamics and strategic risks specific to Mincon. Want force-by-force ratings, visuals and actionable implications? Unlock the full Porter's Five Forces Analysis to explore Mincon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty metals and carbide concentration

Mincon depends on high-grade alloy steels and tungsten carbide sourced from a concentrated supplier base, with China supplying roughly 80% of global tungsten concentrate in 2024, giving suppliers significant leverage. Limited qualified alternatives and typical lead times of 12–20 weeks elevate risk and bargaining power. Metal price volatility has historically squeezed margins, making hedging important. Strategic partnerships and dual-sourcing are used to mitigate supply and price exposure.

Process-intensive components and treatments

Heat treatment, precision machining and hard-facing are critical to tool performance, and a small pool of qualified vendors with tight tolerances and certifications raises switching costs; any deviation causes field failures and warranty expense, so vertical integration or in-house capability is used to reduce exposure.

Logistics complexity across regions

Global distribution to mining and HDD hubs relies on reliable freight and customs brokers; after 2021-22 peak turmoil, container freight rates in 2024 remained roughly 60–70% below peak but still volatile, so disruptions quickly raise input and shipping costs that suppliers can pass through. Regionalization buffers shocks but often reduces scale economies, and vendor-managed inventory programs, which can cut inventory variability by up to 30%, help smooth supply swings.

Proprietary subcomponents and seals

High-performance hammers and bits use specialized seals, brazing materials and inserts, creating reliance on niche suppliers. Proprietary specifications limit the vendor pool and increase supplier bargaining power. Qualification cycles often exceed 12 months, delaying substitutions, while multi-year framework agreements can lock pricing and capacity.

- Supplier concentration: niche components

- Qualification time: >12 months

- Contracting: multi-year frameworks

ESG and compliance obligations

ESG and compliance obligations like conflict-free tungsten, REACH conformity and third-party sustainability audits have narrowed eligible suppliers, raising oversight and switching barriers; by 2024 many OEMs intensified supplier audits and passed compliance tasks downstream in tight markets, shifting cost burdens and elevating failure risk. Collaborative compliance programs between Mincon and OEMs can align incentives and reduce per-supplier cost.

- narrow supplier pool: conflict-free + REACH

- cost shift: OEMs absorb compliance in tight markets

- risk: failure increases oversight & switching barriers

- solution: collaborative compliance lowers unit cost

China ~80% tungsten dominance raises supplier leverage; dual sourcing cuts stock 30%

Mincon relies on concentrated suppliers—China supplied ~80% of global tungsten concentrate in 2024—giving suppliers strong leverage. Long lead times (12–20 weeks) and >12‑month qualification cycles raise switching costs. Freight volatility and metal price swings compress margins. VMI or dual‑sourcing can cut inventory variability by up to 30%.

What is included in the product

Uncovers key competitive drivers, supplier and buyer power, substitutes and entry threats specific to Mincon, with strategic commentary and industry data to assess pricing power, profitability and market resilience.

A one-sheet Mincon Porter’s Five Forces that simplifies competitive pressure into adjustable scores and a radar chart—ideal for quick strategic decisions, slide-ready summaries, and seamless integration into reports or dashboards.

Customers Bargaining Power

Large industrial buyers and tenders

Mining houses, quarry groups and HDD contractors increasingly purchase via RFQs and multi-year tenders, with aggregated volumes giving buyers strong pricing leverage and requirement for service-level commitments. In 2024 large tenders continued to compress margins as competitive benchmarking and supplier scorecards intensified discount pressure. Suppliers defend price by offering value-added services and performance guarantees tied to uptime and lifecycle cost metrics.

Performance-critical, cost-per-meter focus

Buyers optimize total cost-per-meter rather than unit price, with 2024 industry analyses indicating that 10–30% higher penetration rates and 5–15% greater uptime can cut drilling cost-per-meter materially. Superior tool durability and proven lifecycle economics—often reducing total drilling lifecycle cost by around 10–20% in field studies—erode buyer bargaining power. Data logging and on-site trials are pivotal: validated trial data in 2024 became a primary procurement requirement to justify premium pricing.

Interchangeability and switching costs

Many downhole tools fit industry-standard rigs enabling cross-brand substitution, but real-world switching typically costs operators days–weeks of trial downtime and retraining in 2024. Embedded service agreements and on-site spares increase lock-in by shortening mean time to replace equipment. Contractual rebates and consignment stock further reduce churn by smoothing cash flow and inventory availability.

Aftermarket service expectations

- rapid support

- local inventory

- service SLAs

- uptime KPIs

Cyclical demand and budgeting

Cyclical commodity swings and construction seasonality drive buyer urgency; with IMF 2024 global growth at 3.1% softer demand amplifies buyer leverage in downturns. Buyers push for lower prices and extended payment terms in recessions, while upcycles reduce negotiating power as urgency rises. Flexible financing and a ~$140bn global equipment rental market in 2024 help smooth these swings.

- Buyers gain leverage in downturns

- Upcycles reduce buyer negotiating power

- Financing and rentals (~$140bn 2024) smooth volatility

Buyers leverage RFQs, tenders compress margins; rentals & durability cut lifecycle costs

Buyers wield strong leverage via RFQs and multi-year tenders; 2024 tendering compressed margins as benchmarking intensified. Procurement focuses on total cost-per-meter; field studies show 10–20% lifecycle cost savings for higher-durability tools. Real switching costs (days–weeks) and service coverage curb churn. Downturns amplify buyer power (IMF 2024 growth 3.1%); rentals soften volatility (~$140bn 2024).

| Metric | 2024 |

|---|---|

| IMF global growth | 3.1% |

| Rental market | $140bn |

| Lifecycle cost savings | 10–20% |

| Uptime gains | 5–15% |

Same Document Delivered

Mincon Porter's Five Forces Analysis

This preview displays the Mincon Porter's Five Forces Analysis exactly as delivered after purchase, with full methodology, findings, and implications. The document is professionally formatted and ready for immediate download and use. No placeholders or mockups—what you see is what you get.