Shenzhen Mindray Bio-Medical Electronics Boston Consulting Group Matrix

Download Your Competitive Advantage

Quick look: Shenzhen Mindray Bio‑Medical Electronics’ portfolio shows clear winners and a few products sputtering for attention — terrific growth in patient monitoring, steady cash generation from core analyzers, and some question marks in new therapeutics. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a roadmap to where to invest or divest next. Get it in Word + Excel and skip the guesswork — actionable strategy, ready to present.

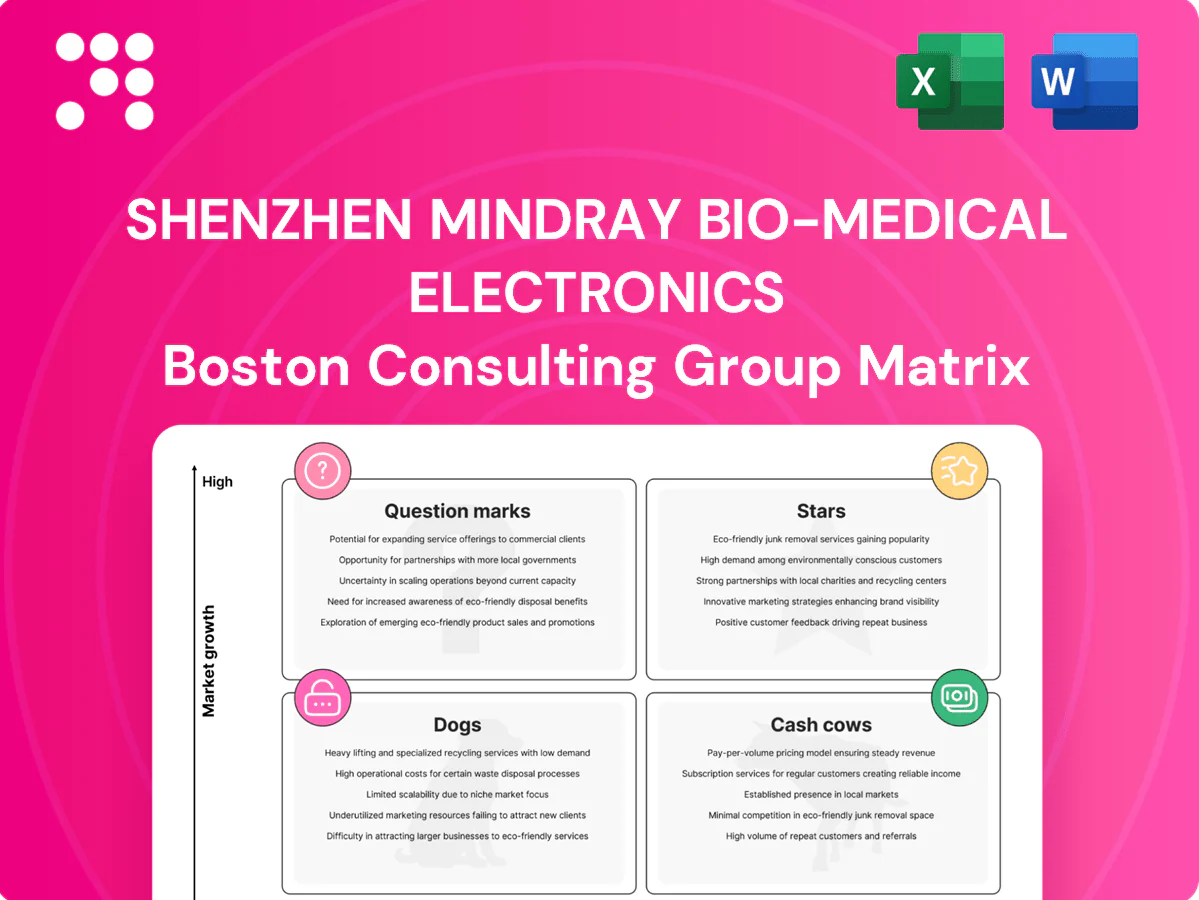

Stars

Flagship patient monitoring platforms

Mindray’s flagship patient monitoring platforms are top-3 global players with roughly 20% market share in critical care and ORs, and demand in emerging markets growing at an estimated 7–10% CAGR; they anchor hospital standardization deals and drive accessories and service sales. Growth requires upfront cash for placements, integrations and training (often 15–25% of project cost), but return on installed systems typically recoups investment within 18–24 months, so continued investment is warranted to defend leadership and lock long-term contracts.

Life-support: anesthesia & ventilators

OR build-outs and ICU upgrades keep Mindray’s anesthesia and ventilator line on a fast track, with global OR/ICU equipment spend rising ~6–8% annually and ventilator market estimated near $6bn in 2024. Mindray’s value-performance pitch wins tenders while premium-feature mix climbed, lifting ASPs and gross margins. The line consumes working capital for demos, trials and service readiness; double down in regions where procedure volumes are rising and competitors price 20–40% higher.

Chemiluminescence immunoassay (CLIA)

Chemiluminescence immunoassay (CLIA) sits in a high-growth IVD segment—global IVD market ~100 billion USD in 2024 with CLIA growing near 7% CAGR—driving sticky reagent pull-through and expanding test menus. Installed-base momentum as labs standardize boosts recurring revenue, but scaling requires footprint expansion, field apps, and reagent logistics, a cash-intensive strategic investment. Prioritize hub labs and fast-track regulatory clearances to widen test coverage and accelerate market capture.

Mid-to-high-end ultrasound (e.g., Resona/DC series)

Mid-to-high-end ultrasound (Resona/DC) is a Stars segment as clinicians in 2024 increasingly trade up for superior image quality, streamlined workflow, and AI-assisted tools, driving strong unit demand across cardiology, OB/GYN, and general imaging.

Mindray is visibly gaining share in these specialties, using Resona/DC as a showcase that requires continuous R&D investment and KOL marketing to defend the top end while offering bundled departmental deals to expand footprint.

- 2024 focus: defend top-tier pricing and feature set

- Strategy: aggressive R&D + KOL programs

- Sales: push cross-department bundles to increase share

Emergency & transport monitoring

Emergency & transport monitoring is rapidly adopted across pre-hospital networks and intra-hospital transport with the portable monitor segment forecast at 7.8% CAGR (2024–2028); rugged, simple, interoperable devices drive wins. Placements are capital-light but scale with disposables and service revenue. Maintain channel investment in EMS and trauma centers to cement leadership.

- Pre-hospital & intra-hospital growth

- Ruggedness + interoperability = market wins

- Capital-light placements; recurring disposables/service

- Prioritize EMS and trauma center partnerships

20% critical-care monitor share; ROI 18-24 months; EM growth 7-10% (2024)

Mindray’s patient monitors: ~20% global share in critical care/OR; installed-system ROI 18–24 months; emerging markets demand +7–10% CAGR (2024). Ventilators/anesthesia: ventilator market ~$6bn (2024); ASPs rising, margins improving. CLIA/IVD: global IVD ~$100bn (2024), CLIA ~7% CAGR; prioritize hub labs and regulatory clearances.

| Segment | 2024 metric | CAGR/notes |

|---|---|---|

| Patient Monitoring | ~20% share; ROI 18–24m | 7–10% EM growth |

| Ventilators | $6bn market | 6–8% OR/ICU spend |

| CLIA/IVD | $100bn market | ~7% CLIA CAGR |

What is included in the product

In-depth BCG review of Mindray's product lines, identifying Stars, Cash Cows, Question Marks, Dogs with strategic invest/divest guidance.

One-page BCG Matrix for Shenzhen Mindray — clarifies portfolio pain points, highlights where to invest or divest for fast C-level decisions.

Cash Cows

Entry-level patient monitors

Entry-level patient monitors are a mature, high-share Shenzhen Mindray segment with predictable public tender cadence and typical 3–7 year refresh cycles in hospitals.

Low promotional spend and parts commonality sustain margins, often in the mid-teens operating range for monitor platforms as scale drives cost efficiency.

The line generates steady cash to fund higher-growth ICU and remote-monitoring bets while management enforces cost discipline and defends price points versus local imitators.

3-part diff hematology analyzers

3-part diff hematology analyzers deliver stable demand from community hospitals and clinics, supporting Mindray’s recurring-consumables model; Mindray reported ~RMB 33.0 billion revenue in 2023, with diagnostics consumables forming a majority of recurring sales. Reagents (≈60% of hematology consumable spend) ensure dependable cash flow; limited R&D beyond reliability upgrades keeps capex low. Tight supply chain and service bundles reduce churn and sustain utilization-driven cash generation.

Infusion & syringe pumps

Infusion and syringe pumps sit as cash cows for Mindray with a large installed base and standardized fleets across wards, underpinning steady replacement cycles; the global infusion pump market was about $5.1 billion in 2024 with ~6.2% CAGR (2024–2030). Replacement parts and consumables yield recurring margins, making the line quietly profitable despite modest market growth. Competition is intense but Mindray’s share in China and emerging markets remains defensible; optimizing service contracts and connectivity add-ons can lift margins further.

Black-and-white cart ultrasound

Black-and-white cart ultrasound sits in a mature, price-sensitive market where Mindray scales efficiently; in 2024 the company reported ultrasound segment growth of ~4% YoY, driven by volume rather than feature expansion, with uptime and durability cited as primary purchase drivers.

Product is cash-positive with high installed-base churn rates low; minimal marketing spend required—maintain light refreshes and channel-led sales to sustain steady volumes and margin stability.

- Market maturity: low growth, price-driven

- Mindray 2024 ultrasound growth ~4% YoY

- Buyers prioritize durability and uptime

- Cash-positive; minimal marketing needed

- Strategy: lite refreshes + channel sales

Hospital defibrillators (in-hospital)

Hospital defibrillators (in-hospital) are steady, compliance-driven purchases with predictable 8–10 year replacement cycles and budgeted capex in 2024, delivering reliable cash rather than hyper-growth. Service and training upsells plus accessories sustain high-margin annuity revenue, so fleet standardization is the primary commercial lever to retain share and expand per-unit revenue.

- Replacement cycle: 8–10 years

- Revenue profile: stable cash cow, low growth

- Upsell drivers: service, training, accessories

- Strategy: fleet standardization to secure annuity

Cash-cow devices drive mid-teens margins, funding ICU and remote-care growth

Mindray cash cows (entry monitors, 3-part hematology, infusion/syringe pumps, B/W ultrasound, in-hospital defibrillators) deliver steady, mid-teens operating margins, funding ICU/remote growth; company revenue ~RMB 33.0 billion (2023), ultrasound +4% YoY (2024), global infusion market $5.1bn (2024).

| Product | Role | Key metrics | Margin drivers |

|---|---|---|---|

| Entry monitors | Cash cow | 3–7y refresh | Scale, low promo |

| Hematology | Recurring consumables | Reagents ≈60% | Consumables annuity |

| Infusion | Installed base | $5.1bn market | Parts & service |

| Ultrasound | Volume-driven | +4% 2024 | Durability |

| Defibrillators | Compliance buys | 8–10y cycle | Service upsells |

Full Transparency, Always

Shenzhen Mindray Bio-Medical Electronics BCG Matrix

The file you're previewing is the final Shenzhen Mindray Bio‑Medical Electronics BCG Matrix you'll receive after purchase — no watermarks, no demo content, just a polished strategic report. It mirrors the exact downloadable document, crafted with market‑backed analysis and clear formatting. After buying, the full file is instantly available for editing, printing, or presenting to stakeholders. No surprises — ready to plug into your planning right away.

Download Your Competitive Advantage

Quick look: Shenzhen Mindray Bio‑Medical Electronics’ portfolio shows clear winners and a few products sputtering for attention — terrific growth in patient monitoring, steady cash generation from core analyzers, and some question marks in new therapeutics. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a roadmap to where to invest or divest next. Get it in Word + Excel and skip the guesswork — actionable strategy, ready to present.

Stars

Flagship patient monitoring platforms

Mindray’s flagship patient monitoring platforms are top-3 global players with roughly 20% market share in critical care and ORs, and demand in emerging markets growing at an estimated 7–10% CAGR; they anchor hospital standardization deals and drive accessories and service sales. Growth requires upfront cash for placements, integrations and training (often 15–25% of project cost), but return on installed systems typically recoups investment within 18–24 months, so continued investment is warranted to defend leadership and lock long-term contracts.

Life-support: anesthesia & ventilators

OR build-outs and ICU upgrades keep Mindray’s anesthesia and ventilator line on a fast track, with global OR/ICU equipment spend rising ~6–8% annually and ventilator market estimated near $6bn in 2024. Mindray’s value-performance pitch wins tenders while premium-feature mix climbed, lifting ASPs and gross margins. The line consumes working capital for demos, trials and service readiness; double down in regions where procedure volumes are rising and competitors price 20–40% higher.

Chemiluminescence immunoassay (CLIA)

Chemiluminescence immunoassay (CLIA) sits in a high-growth IVD segment—global IVD market ~100 billion USD in 2024 with CLIA growing near 7% CAGR—driving sticky reagent pull-through and expanding test menus. Installed-base momentum as labs standardize boosts recurring revenue, but scaling requires footprint expansion, field apps, and reagent logistics, a cash-intensive strategic investment. Prioritize hub labs and fast-track regulatory clearances to widen test coverage and accelerate market capture.

Mid-to-high-end ultrasound (e.g., Resona/DC series)

Mid-to-high-end ultrasound (Resona/DC) is a Stars segment as clinicians in 2024 increasingly trade up for superior image quality, streamlined workflow, and AI-assisted tools, driving strong unit demand across cardiology, OB/GYN, and general imaging.

Mindray is visibly gaining share in these specialties, using Resona/DC as a showcase that requires continuous R&D investment and KOL marketing to defend the top end while offering bundled departmental deals to expand footprint.

- 2024 focus: defend top-tier pricing and feature set

- Strategy: aggressive R&D + KOL programs

- Sales: push cross-department bundles to increase share

Emergency & transport monitoring

Emergency & transport monitoring is rapidly adopted across pre-hospital networks and intra-hospital transport with the portable monitor segment forecast at 7.8% CAGR (2024–2028); rugged, simple, interoperable devices drive wins. Placements are capital-light but scale with disposables and service revenue. Maintain channel investment in EMS and trauma centers to cement leadership.

- Pre-hospital & intra-hospital growth

- Ruggedness + interoperability = market wins

- Capital-light placements; recurring disposables/service

- Prioritize EMS and trauma center partnerships

20% critical-care monitor share; ROI 18-24 months; EM growth 7-10% (2024)

Mindray’s patient monitors: ~20% global share in critical care/OR; installed-system ROI 18–24 months; emerging markets demand +7–10% CAGR (2024). Ventilators/anesthesia: ventilator market ~$6bn (2024); ASPs rising, margins improving. CLIA/IVD: global IVD ~$100bn (2024), CLIA ~7% CAGR; prioritize hub labs and regulatory clearances.

| Segment | 2024 metric | CAGR/notes |

|---|---|---|

| Patient Monitoring | ~20% share; ROI 18–24m | 7–10% EM growth |

| Ventilators | $6bn market | 6–8% OR/ICU spend |

| CLIA/IVD | $100bn market | ~7% CLIA CAGR |

What is included in the product

In-depth BCG review of Mindray's product lines, identifying Stars, Cash Cows, Question Marks, Dogs with strategic invest/divest guidance.

One-page BCG Matrix for Shenzhen Mindray — clarifies portfolio pain points, highlights where to invest or divest for fast C-level decisions.

Cash Cows

Entry-level patient monitors

Entry-level patient monitors are a mature, high-share Shenzhen Mindray segment with predictable public tender cadence and typical 3–7 year refresh cycles in hospitals.

Low promotional spend and parts commonality sustain margins, often in the mid-teens operating range for monitor platforms as scale drives cost efficiency.

The line generates steady cash to fund higher-growth ICU and remote-monitoring bets while management enforces cost discipline and defends price points versus local imitators.

3-part diff hematology analyzers

3-part diff hematology analyzers deliver stable demand from community hospitals and clinics, supporting Mindray’s recurring-consumables model; Mindray reported ~RMB 33.0 billion revenue in 2023, with diagnostics consumables forming a majority of recurring sales. Reagents (≈60% of hematology consumable spend) ensure dependable cash flow; limited R&D beyond reliability upgrades keeps capex low. Tight supply chain and service bundles reduce churn and sustain utilization-driven cash generation.

Infusion & syringe pumps

Infusion and syringe pumps sit as cash cows for Mindray with a large installed base and standardized fleets across wards, underpinning steady replacement cycles; the global infusion pump market was about $5.1 billion in 2024 with ~6.2% CAGR (2024–2030). Replacement parts and consumables yield recurring margins, making the line quietly profitable despite modest market growth. Competition is intense but Mindray’s share in China and emerging markets remains defensible; optimizing service contracts and connectivity add-ons can lift margins further.

Black-and-white cart ultrasound

Black-and-white cart ultrasound sits in a mature, price-sensitive market where Mindray scales efficiently; in 2024 the company reported ultrasound segment growth of ~4% YoY, driven by volume rather than feature expansion, with uptime and durability cited as primary purchase drivers.

Product is cash-positive with high installed-base churn rates low; minimal marketing spend required—maintain light refreshes and channel-led sales to sustain steady volumes and margin stability.

- Market maturity: low growth, price-driven

- Mindray 2024 ultrasound growth ~4% YoY

- Buyers prioritize durability and uptime

- Cash-positive; minimal marketing needed

- Strategy: lite refreshes + channel sales

Hospital defibrillators (in-hospital)

Hospital defibrillators (in-hospital) are steady, compliance-driven purchases with predictable 8–10 year replacement cycles and budgeted capex in 2024, delivering reliable cash rather than hyper-growth. Service and training upsells plus accessories sustain high-margin annuity revenue, so fleet standardization is the primary commercial lever to retain share and expand per-unit revenue.

- Replacement cycle: 8–10 years

- Revenue profile: stable cash cow, low growth

- Upsell drivers: service, training, accessories

- Strategy: fleet standardization to secure annuity

Cash-cow devices drive mid-teens margins, funding ICU and remote-care growth

Mindray cash cows (entry monitors, 3-part hematology, infusion/syringe pumps, B/W ultrasound, in-hospital defibrillators) deliver steady, mid-teens operating margins, funding ICU/remote growth; company revenue ~RMB 33.0 billion (2023), ultrasound +4% YoY (2024), global infusion market $5.1bn (2024).

| Product | Role | Key metrics | Margin drivers |

|---|---|---|---|

| Entry monitors | Cash cow | 3–7y refresh | Scale, low promo |

| Hematology | Recurring consumables | Reagents ≈60% | Consumables annuity |

| Infusion | Installed base | $5.1bn market | Parts & service |

| Ultrasound | Volume-driven | +4% 2024 | Durability |

| Defibrillators | Compliance buys | 8–10y cycle | Service upsells |

Full Transparency, Always

Shenzhen Mindray Bio-Medical Electronics BCG Matrix

The file you're previewing is the final Shenzhen Mindray Bio‑Medical Electronics BCG Matrix you'll receive after purchase — no watermarks, no demo content, just a polished strategic report. It mirrors the exact downloadable document, crafted with market‑backed analysis and clear formatting. After buying, the full file is instantly available for editing, printing, or presenting to stakeholders. No surprises — ready to plug into your planning right away.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

Quick look: Shenzhen Mindray Bio‑Medical Electronics’ portfolio shows clear winners and a few products sputtering for attention — terrific growth in patient monitoring, steady cash generation from core analyzers, and some question marks in new therapeutics. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a roadmap to where to invest or divest next. Get it in Word + Excel and skip the guesswork — actionable strategy, ready to present.

Stars

Flagship patient monitoring platforms

Mindray’s flagship patient monitoring platforms are top-3 global players with roughly 20% market share in critical care and ORs, and demand in emerging markets growing at an estimated 7–10% CAGR; they anchor hospital standardization deals and drive accessories and service sales. Growth requires upfront cash for placements, integrations and training (often 15–25% of project cost), but return on installed systems typically recoups investment within 18–24 months, so continued investment is warranted to defend leadership and lock long-term contracts.

Life-support: anesthesia & ventilators

OR build-outs and ICU upgrades keep Mindray’s anesthesia and ventilator line on a fast track, with global OR/ICU equipment spend rising ~6–8% annually and ventilator market estimated near $6bn in 2024. Mindray’s value-performance pitch wins tenders while premium-feature mix climbed, lifting ASPs and gross margins. The line consumes working capital for demos, trials and service readiness; double down in regions where procedure volumes are rising and competitors price 20–40% higher.

Chemiluminescence immunoassay (CLIA)

Chemiluminescence immunoassay (CLIA) sits in a high-growth IVD segment—global IVD market ~100 billion USD in 2024 with CLIA growing near 7% CAGR—driving sticky reagent pull-through and expanding test menus. Installed-base momentum as labs standardize boosts recurring revenue, but scaling requires footprint expansion, field apps, and reagent logistics, a cash-intensive strategic investment. Prioritize hub labs and fast-track regulatory clearances to widen test coverage and accelerate market capture.

Mid-to-high-end ultrasound (e.g., Resona/DC series)

Mid-to-high-end ultrasound (Resona/DC) is a Stars segment as clinicians in 2024 increasingly trade up for superior image quality, streamlined workflow, and AI-assisted tools, driving strong unit demand across cardiology, OB/GYN, and general imaging.

Mindray is visibly gaining share in these specialties, using Resona/DC as a showcase that requires continuous R&D investment and KOL marketing to defend the top end while offering bundled departmental deals to expand footprint.

- 2024 focus: defend top-tier pricing and feature set

- Strategy: aggressive R&D + KOL programs

- Sales: push cross-department bundles to increase share

Emergency & transport monitoring

Emergency & transport monitoring is rapidly adopted across pre-hospital networks and intra-hospital transport with the portable monitor segment forecast at 7.8% CAGR (2024–2028); rugged, simple, interoperable devices drive wins. Placements are capital-light but scale with disposables and service revenue. Maintain channel investment in EMS and trauma centers to cement leadership.

- Pre-hospital & intra-hospital growth

- Ruggedness + interoperability = market wins

- Capital-light placements; recurring disposables/service

- Prioritize EMS and trauma center partnerships

20% critical-care monitor share; ROI 18-24 months; EM growth 7-10% (2024)

Mindray’s patient monitors: ~20% global share in critical care/OR; installed-system ROI 18–24 months; emerging markets demand +7–10% CAGR (2024). Ventilators/anesthesia: ventilator market ~$6bn (2024); ASPs rising, margins improving. CLIA/IVD: global IVD ~$100bn (2024), CLIA ~7% CAGR; prioritize hub labs and regulatory clearances.

| Segment | 2024 metric | CAGR/notes |

|---|---|---|

| Patient Monitoring | ~20% share; ROI 18–24m | 7–10% EM growth |

| Ventilators | $6bn market | 6–8% OR/ICU spend |

| CLIA/IVD | $100bn market | ~7% CLIA CAGR |

What is included in the product

In-depth BCG review of Mindray's product lines, identifying Stars, Cash Cows, Question Marks, Dogs with strategic invest/divest guidance.

One-page BCG Matrix for Shenzhen Mindray — clarifies portfolio pain points, highlights where to invest or divest for fast C-level decisions.

Cash Cows

Entry-level patient monitors

Entry-level patient monitors are a mature, high-share Shenzhen Mindray segment with predictable public tender cadence and typical 3–7 year refresh cycles in hospitals.

Low promotional spend and parts commonality sustain margins, often in the mid-teens operating range for monitor platforms as scale drives cost efficiency.

The line generates steady cash to fund higher-growth ICU and remote-monitoring bets while management enforces cost discipline and defends price points versus local imitators.

3-part diff hematology analyzers

3-part diff hematology analyzers deliver stable demand from community hospitals and clinics, supporting Mindray’s recurring-consumables model; Mindray reported ~RMB 33.0 billion revenue in 2023, with diagnostics consumables forming a majority of recurring sales. Reagents (≈60% of hematology consumable spend) ensure dependable cash flow; limited R&D beyond reliability upgrades keeps capex low. Tight supply chain and service bundles reduce churn and sustain utilization-driven cash generation.

Infusion & syringe pumps

Infusion and syringe pumps sit as cash cows for Mindray with a large installed base and standardized fleets across wards, underpinning steady replacement cycles; the global infusion pump market was about $5.1 billion in 2024 with ~6.2% CAGR (2024–2030). Replacement parts and consumables yield recurring margins, making the line quietly profitable despite modest market growth. Competition is intense but Mindray’s share in China and emerging markets remains defensible; optimizing service contracts and connectivity add-ons can lift margins further.

Black-and-white cart ultrasound

Black-and-white cart ultrasound sits in a mature, price-sensitive market where Mindray scales efficiently; in 2024 the company reported ultrasound segment growth of ~4% YoY, driven by volume rather than feature expansion, with uptime and durability cited as primary purchase drivers.

Product is cash-positive with high installed-base churn rates low; minimal marketing spend required—maintain light refreshes and channel-led sales to sustain steady volumes and margin stability.

- Market maturity: low growth, price-driven

- Mindray 2024 ultrasound growth ~4% YoY

- Buyers prioritize durability and uptime

- Cash-positive; minimal marketing needed

- Strategy: lite refreshes + channel sales

Hospital defibrillators (in-hospital)

Hospital defibrillators (in-hospital) are steady, compliance-driven purchases with predictable 8–10 year replacement cycles and budgeted capex in 2024, delivering reliable cash rather than hyper-growth. Service and training upsells plus accessories sustain high-margin annuity revenue, so fleet standardization is the primary commercial lever to retain share and expand per-unit revenue.

- Replacement cycle: 8–10 years

- Revenue profile: stable cash cow, low growth

- Upsell drivers: service, training, accessories

- Strategy: fleet standardization to secure annuity

Cash-cow devices drive mid-teens margins, funding ICU and remote-care growth

Mindray cash cows (entry monitors, 3-part hematology, infusion/syringe pumps, B/W ultrasound, in-hospital defibrillators) deliver steady, mid-teens operating margins, funding ICU/remote growth; company revenue ~RMB 33.0 billion (2023), ultrasound +4% YoY (2024), global infusion market $5.1bn (2024).

| Product | Role | Key metrics | Margin drivers |

|---|---|---|---|

| Entry monitors | Cash cow | 3–7y refresh | Scale, low promo |

| Hematology | Recurring consumables | Reagents ≈60% | Consumables annuity |

| Infusion | Installed base | $5.1bn market | Parts & service |

| Ultrasound | Volume-driven | +4% 2024 | Durability |

| Defibrillators | Compliance buys | 8–10y cycle | Service upsells |

Full Transparency, Always

Shenzhen Mindray Bio-Medical Electronics BCG Matrix

The file you're previewing is the final Shenzhen Mindray Bio‑Medical Electronics BCG Matrix you'll receive after purchase — no watermarks, no demo content, just a polished strategic report. It mirrors the exact downloadable document, crafted with market‑backed analysis and clear formatting. After buying, the full file is instantly available for editing, printing, or presenting to stakeholders. No surprises — ready to plug into your planning right away.