Minimax Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

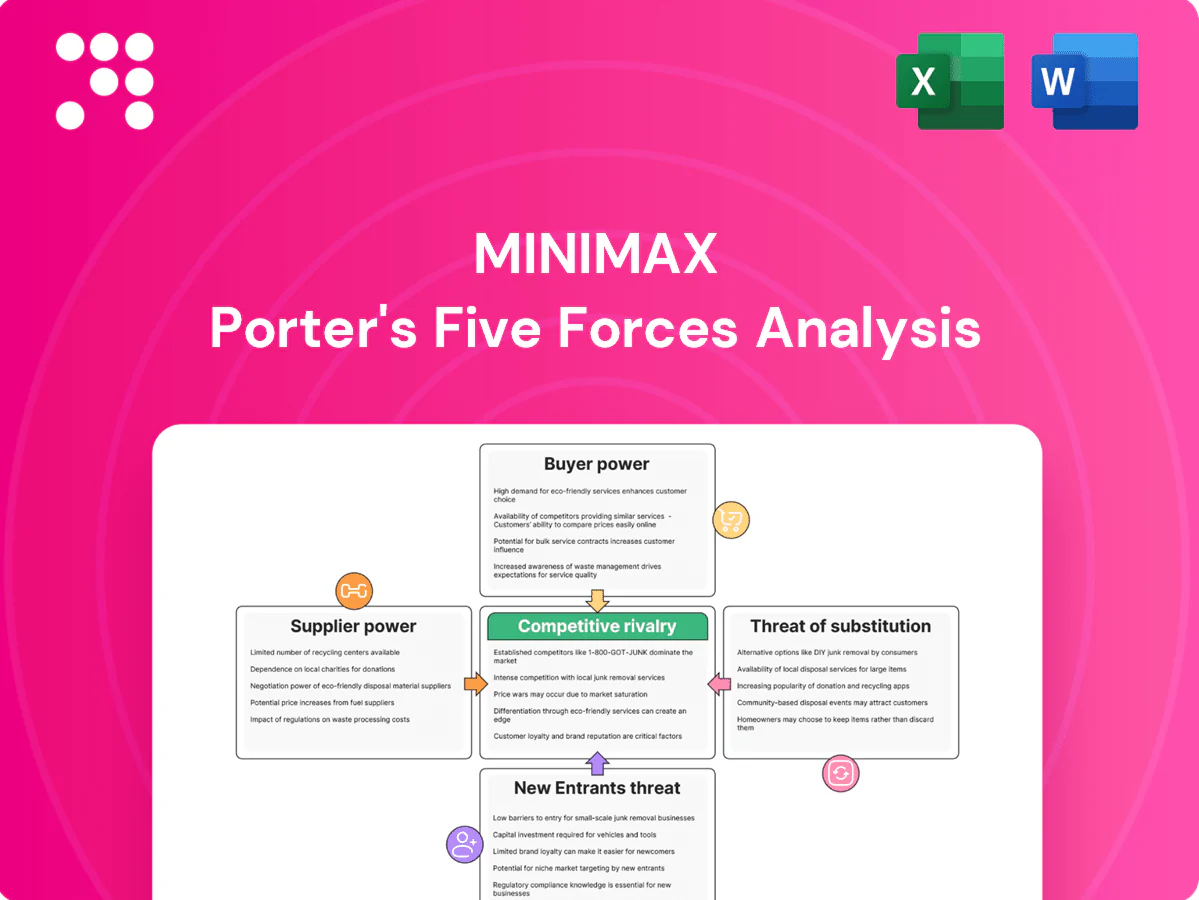

Minimax’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, substitute threats, entry barriers, and competitive rivalry shaping its strategic positioning. Early signals show moderate supplier influence, rising substitute pressure from software alternatives, and intense rivalry compressing margins. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Minimax.

Suppliers Bargaining Power

Specialized components and agents

Minimax depends on certified sensors, valves, controllers and suppression agents from specialized suppliers, where limited qualified sources raise switching costs and lead times typically of 12–24 weeks; supplier concentration thus increases bargaining power. Minimax’s scale helps secure priority allocation—large customers can see ~30% faster fulfillment—and long-term contracts plus dual sourcing are used to mitigate concentration risk.

Standards and certification constraints

UL/FM, EN, NFPA and VdS compliance in 2024 continue to restrict the supplier pool to accredited vendors, concentrating sourcing to a smaller cohort. This certification gate gives approved suppliers leverage on price and delivery windows. Minimax offsets pressure by co-developing specifications and operating in‑house test labs to shorten approval cycles. Joint certification programs lock in cost predictability and consistent quality.

Electronics and semiconductor exposure

Control panels and detectors rely on chips and sensors tied to a semiconductor market of roughly $600B in 2024 and a concentrated foundry base (TSMC ~54% share), so scarcity and cyclicality can push bargaining power upstream. Historical lead times remain elevated (~14 weeks in 2024), amplifying vendor leverage. Active forecasting, buffer inventory and design-for-substitution to broaden approved parts mitigate supplier power and reduce disruption.

Bulk materials vs. differentiated inputs

Steel pipe and fittings are largely commoditized with low supplier power, while proprietary nozzles, actuation devices and specialized agent blends give suppliers clear pricing leverage; Minimax offsets this by combining in-house manufacturing and tooling and by pursuing vertical integration to lower dependency on critical SKUs in 2024.

- Commoditized inputs: low supplier power

- Differentiated inputs: high supplier leverage

- Mitigation: in-house manufacturing

- Mitigation: vertical integration, reduced dependency

Logistics and global footprint

International projects demand synchronized supply across regions, raising supplier bargaining power due to freight, hazmat regulations, and customs that increase coordination complexity.

Minimax’s global procurement hubs use scale-based contracts and long-term freight agreements to lower supplier leverage, while regional stocking points and pre-positioned inventory reduce last-mile dependence.

- Scale negotiation: centralized hubs

- Regulatory friction: freight, hazmat, customs

- Mitigation: regional stocking points

12–24 wk lead times, supplier concentration and chip exposure risk

Minimax relies on certified sensors/agents with 12–24 week lead times and concentrated suppliers, raising supplier power; scale yields ~30% faster fulfillment for large customers. Semiconductor exposure (market ~$600B, TSMC ~54% share in 2024) amplifies upstream leverage. Mitigations: dual sourcing, in‑house testing, vertical integration and regional stocking to cut disruption.

| Input | 2024 metric | Impact |

|---|---|---|

| Certified parts | 12–24 wk lead | High power |

| Semiconductors | $600B market; TSMC ~54% | Elevated risk |

What is included in the product

Comprehensive Porter's Five Forces assessment for Minimax that evaluates competitive rivalry, buyer and supplier power, substitutes, and entry barriers, highlights disruptive threats and strategic levers to defend margins, and is fully editable for investor materials, internal strategy decks, or academic use.

Compact Minimax Porter's Five Forces that quantifies and visualizes competitive pressure for quick strategic decisions, with customizable weights and slide-ready charts to relieve analysis bottlenecks.

Customers Bargaining Power

Large enterprise and EPC buyers

Large enterprise and EPC buyers run competitive tenders, tightening price and terms and in 2024 increasingly centralizing procurement to drive efficiency. Their professional sourcing teams elevate bargaining power, forcing suppliers to justify margins. Minimax counters by quantifying total cost of ownership and risk reduction, and secures framework agreements that trade staged discounts for committed volume and loyalty.

Code-driven but spec-flexible demand

Regulations such as IBC and NFPA 101 mandate fire protection in most commercial buildings, reducing pure price sensitivity while keeping demand code-driven. Multiple code-compliant solutions and typical tender shortlists of 3 vendors enable switching, and performance-based specs plus value engineering can cut system costs by up to 10%. Minimax gains advantage by influencing specs early and offering turnkey scope to capture higher-margin contracts.

Switching costs in lifecycle service

Commissioning, proprietary software and certifications create high switching frictions in maintenance, with 2024 industry reports showing service contracts account for about 40% of OEM lifecycle revenue and average 5-year terms. Multi-year contracts anchor revenue and blunt buyer power, though buyers can unbundle to third parties to cut costs. Minimax defends with uptime SLAs and real-time digital monitoring that field studies show can cut downtime by ~30%.

Project risk and schedule pressure

Missed milestones are costly, so reliable delivery commands a premium; in 2024 buyers shifted focus from lowest price to execution certainty as schedule risk rose, with liquidated damages commonly specified at 0.1–0.5% of contract value per day and often priced into bids. Minimax mitigates by leveraging disciplined project management and global field teams to protect margins and meet tight timelines.

- Execution over price

- LD 0.1–0.5%/day

- Schedule risk priced into bids

- PM + global field teams

Multi-site global accounts

Global customers demand standardized solutions and unified pricing; consolidation of spend increases their negotiating leverage, and in 2024 Minimax provides global master service agreements with consistent compliance across regions. Data-driven fleet reporting delivers measurable operational insights and adds stickiness and value to multi-site accounts.

- Global MSAs: standardized pricing and compliance (2024)

- Consolidated spend: higher buyer leverage

- Fleet reporting: increased retention via data-driven insights

Centralized procurement: shortlists ≈3; services ≈40% rev

Large enterprise buyers centralize procurement in 2024, running competitive tenders that pressure price and terms; professional sourcing teams elevate bargaining power. Regulation-driven demand reduces pure price sensitivity; shortlist switching remains (~3 vendors) and value engineering can cut system costs up to 10%. Service contracts ≈40% of OEM lifecycle revenue (2024), typical 5-year terms; uptime SLAs and monitoring lower downtime ~30%.

| Metric | 2024 Value |

|---|---|

| Service contracts (% revenue) | ≈40% |

| Typical contract term | 5 years |

| Vendor shortlist | ≈3 |

| LD | 0.1–0.5%/day |

| Downtime reduction (monitoring) | ≈30% |

| Cost cut (value engineering) | Up to 10% |

What You See Is What You Get

Minimax Porter's Five Forces Analysis

This preview shows the exact Minimax Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the ready-to-use full analysis, fully formatted and professionally written. Once you buy, you'll get instant access to this same file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Minimax’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, substitute threats, entry barriers, and competitive rivalry shaping its strategic positioning. Early signals show moderate supplier influence, rising substitute pressure from software alternatives, and intense rivalry compressing margins. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Minimax.

Suppliers Bargaining Power

Specialized components and agents

Minimax depends on certified sensors, valves, controllers and suppression agents from specialized suppliers, where limited qualified sources raise switching costs and lead times typically of 12–24 weeks; supplier concentration thus increases bargaining power. Minimax’s scale helps secure priority allocation—large customers can see ~30% faster fulfillment—and long-term contracts plus dual sourcing are used to mitigate concentration risk.

Standards and certification constraints

UL/FM, EN, NFPA and VdS compliance in 2024 continue to restrict the supplier pool to accredited vendors, concentrating sourcing to a smaller cohort. This certification gate gives approved suppliers leverage on price and delivery windows. Minimax offsets pressure by co-developing specifications and operating in‑house test labs to shorten approval cycles. Joint certification programs lock in cost predictability and consistent quality.

Electronics and semiconductor exposure

Control panels and detectors rely on chips and sensors tied to a semiconductor market of roughly $600B in 2024 and a concentrated foundry base (TSMC ~54% share), so scarcity and cyclicality can push bargaining power upstream. Historical lead times remain elevated (~14 weeks in 2024), amplifying vendor leverage. Active forecasting, buffer inventory and design-for-substitution to broaden approved parts mitigate supplier power and reduce disruption.

Bulk materials vs. differentiated inputs

Steel pipe and fittings are largely commoditized with low supplier power, while proprietary nozzles, actuation devices and specialized agent blends give suppliers clear pricing leverage; Minimax offsets this by combining in-house manufacturing and tooling and by pursuing vertical integration to lower dependency on critical SKUs in 2024.

- Commoditized inputs: low supplier power

- Differentiated inputs: high supplier leverage

- Mitigation: in-house manufacturing

- Mitigation: vertical integration, reduced dependency

Logistics and global footprint

International projects demand synchronized supply across regions, raising supplier bargaining power due to freight, hazmat regulations, and customs that increase coordination complexity.

Minimax’s global procurement hubs use scale-based contracts and long-term freight agreements to lower supplier leverage, while regional stocking points and pre-positioned inventory reduce last-mile dependence.

- Scale negotiation: centralized hubs

- Regulatory friction: freight, hazmat, customs

- Mitigation: regional stocking points

12–24 wk lead times, supplier concentration and chip exposure risk

Minimax relies on certified sensors/agents with 12–24 week lead times and concentrated suppliers, raising supplier power; scale yields ~30% faster fulfillment for large customers. Semiconductor exposure (market ~$600B, TSMC ~54% share in 2024) amplifies upstream leverage. Mitigations: dual sourcing, in‑house testing, vertical integration and regional stocking to cut disruption.

| Input | 2024 metric | Impact |

|---|---|---|

| Certified parts | 12–24 wk lead | High power |

| Semiconductors | $600B market; TSMC ~54% | Elevated risk |

What is included in the product

Comprehensive Porter's Five Forces assessment for Minimax that evaluates competitive rivalry, buyer and supplier power, substitutes, and entry barriers, highlights disruptive threats and strategic levers to defend margins, and is fully editable for investor materials, internal strategy decks, or academic use.

Compact Minimax Porter's Five Forces that quantifies and visualizes competitive pressure for quick strategic decisions, with customizable weights and slide-ready charts to relieve analysis bottlenecks.

Customers Bargaining Power

Large enterprise and EPC buyers

Large enterprise and EPC buyers run competitive tenders, tightening price and terms and in 2024 increasingly centralizing procurement to drive efficiency. Their professional sourcing teams elevate bargaining power, forcing suppliers to justify margins. Minimax counters by quantifying total cost of ownership and risk reduction, and secures framework agreements that trade staged discounts for committed volume and loyalty.

Code-driven but spec-flexible demand

Regulations such as IBC and NFPA 101 mandate fire protection in most commercial buildings, reducing pure price sensitivity while keeping demand code-driven. Multiple code-compliant solutions and typical tender shortlists of 3 vendors enable switching, and performance-based specs plus value engineering can cut system costs by up to 10%. Minimax gains advantage by influencing specs early and offering turnkey scope to capture higher-margin contracts.

Switching costs in lifecycle service

Commissioning, proprietary software and certifications create high switching frictions in maintenance, with 2024 industry reports showing service contracts account for about 40% of OEM lifecycle revenue and average 5-year terms. Multi-year contracts anchor revenue and blunt buyer power, though buyers can unbundle to third parties to cut costs. Minimax defends with uptime SLAs and real-time digital monitoring that field studies show can cut downtime by ~30%.

Project risk and schedule pressure

Missed milestones are costly, so reliable delivery commands a premium; in 2024 buyers shifted focus from lowest price to execution certainty as schedule risk rose, with liquidated damages commonly specified at 0.1–0.5% of contract value per day and often priced into bids. Minimax mitigates by leveraging disciplined project management and global field teams to protect margins and meet tight timelines.

- Execution over price

- LD 0.1–0.5%/day

- Schedule risk priced into bids

- PM + global field teams

Multi-site global accounts

Global customers demand standardized solutions and unified pricing; consolidation of spend increases their negotiating leverage, and in 2024 Minimax provides global master service agreements with consistent compliance across regions. Data-driven fleet reporting delivers measurable operational insights and adds stickiness and value to multi-site accounts.

- Global MSAs: standardized pricing and compliance (2024)

- Consolidated spend: higher buyer leverage

- Fleet reporting: increased retention via data-driven insights

Centralized procurement: shortlists ≈3; services ≈40% rev

Large enterprise buyers centralize procurement in 2024, running competitive tenders that pressure price and terms; professional sourcing teams elevate bargaining power. Regulation-driven demand reduces pure price sensitivity; shortlist switching remains (~3 vendors) and value engineering can cut system costs up to 10%. Service contracts ≈40% of OEM lifecycle revenue (2024), typical 5-year terms; uptime SLAs and monitoring lower downtime ~30%.

| Metric | 2024 Value |

|---|---|

| Service contracts (% revenue) | ≈40% |

| Typical contract term | 5 years |

| Vendor shortlist | ≈3 |

| LD | 0.1–0.5%/day |

| Downtime reduction (monitoring) | ≈30% |

| Cost cut (value engineering) | Up to 10% |

What You See Is What You Get

Minimax Porter's Five Forces Analysis

This preview shows the exact Minimax Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the ready-to-use full analysis, fully formatted and professionally written. Once you buy, you'll get instant access to this same file.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Minimax’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, substitute threats, entry barriers, and competitive rivalry shaping its strategic positioning. Early signals show moderate supplier influence, rising substitute pressure from software alternatives, and intense rivalry compressing margins. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Minimax.

Suppliers Bargaining Power

Specialized components and agents

Minimax depends on certified sensors, valves, controllers and suppression agents from specialized suppliers, where limited qualified sources raise switching costs and lead times typically of 12–24 weeks; supplier concentration thus increases bargaining power. Minimax’s scale helps secure priority allocation—large customers can see ~30% faster fulfillment—and long-term contracts plus dual sourcing are used to mitigate concentration risk.

Standards and certification constraints

UL/FM, EN, NFPA and VdS compliance in 2024 continue to restrict the supplier pool to accredited vendors, concentrating sourcing to a smaller cohort. This certification gate gives approved suppliers leverage on price and delivery windows. Minimax offsets pressure by co-developing specifications and operating in‑house test labs to shorten approval cycles. Joint certification programs lock in cost predictability and consistent quality.

Electronics and semiconductor exposure

Control panels and detectors rely on chips and sensors tied to a semiconductor market of roughly $600B in 2024 and a concentrated foundry base (TSMC ~54% share), so scarcity and cyclicality can push bargaining power upstream. Historical lead times remain elevated (~14 weeks in 2024), amplifying vendor leverage. Active forecasting, buffer inventory and design-for-substitution to broaden approved parts mitigate supplier power and reduce disruption.

Bulk materials vs. differentiated inputs

Steel pipe and fittings are largely commoditized with low supplier power, while proprietary nozzles, actuation devices and specialized agent blends give suppliers clear pricing leverage; Minimax offsets this by combining in-house manufacturing and tooling and by pursuing vertical integration to lower dependency on critical SKUs in 2024.

- Commoditized inputs: low supplier power

- Differentiated inputs: high supplier leverage

- Mitigation: in-house manufacturing

- Mitigation: vertical integration, reduced dependency

Logistics and global footprint

International projects demand synchronized supply across regions, raising supplier bargaining power due to freight, hazmat regulations, and customs that increase coordination complexity.

Minimax’s global procurement hubs use scale-based contracts and long-term freight agreements to lower supplier leverage, while regional stocking points and pre-positioned inventory reduce last-mile dependence.

- Scale negotiation: centralized hubs

- Regulatory friction: freight, hazmat, customs

- Mitigation: regional stocking points

12–24 wk lead times, supplier concentration and chip exposure risk

Minimax relies on certified sensors/agents with 12–24 week lead times and concentrated suppliers, raising supplier power; scale yields ~30% faster fulfillment for large customers. Semiconductor exposure (market ~$600B, TSMC ~54% share in 2024) amplifies upstream leverage. Mitigations: dual sourcing, in‑house testing, vertical integration and regional stocking to cut disruption.

| Input | 2024 metric | Impact |

|---|---|---|

| Certified parts | 12–24 wk lead | High power |

| Semiconductors | $600B market; TSMC ~54% | Elevated risk |

What is included in the product

Comprehensive Porter's Five Forces assessment for Minimax that evaluates competitive rivalry, buyer and supplier power, substitutes, and entry barriers, highlights disruptive threats and strategic levers to defend margins, and is fully editable for investor materials, internal strategy decks, or academic use.

Compact Minimax Porter's Five Forces that quantifies and visualizes competitive pressure for quick strategic decisions, with customizable weights and slide-ready charts to relieve analysis bottlenecks.

Customers Bargaining Power

Large enterprise and EPC buyers

Large enterprise and EPC buyers run competitive tenders, tightening price and terms and in 2024 increasingly centralizing procurement to drive efficiency. Their professional sourcing teams elevate bargaining power, forcing suppliers to justify margins. Minimax counters by quantifying total cost of ownership and risk reduction, and secures framework agreements that trade staged discounts for committed volume and loyalty.

Code-driven but spec-flexible demand

Regulations such as IBC and NFPA 101 mandate fire protection in most commercial buildings, reducing pure price sensitivity while keeping demand code-driven. Multiple code-compliant solutions and typical tender shortlists of 3 vendors enable switching, and performance-based specs plus value engineering can cut system costs by up to 10%. Minimax gains advantage by influencing specs early and offering turnkey scope to capture higher-margin contracts.

Switching costs in lifecycle service

Commissioning, proprietary software and certifications create high switching frictions in maintenance, with 2024 industry reports showing service contracts account for about 40% of OEM lifecycle revenue and average 5-year terms. Multi-year contracts anchor revenue and blunt buyer power, though buyers can unbundle to third parties to cut costs. Minimax defends with uptime SLAs and real-time digital monitoring that field studies show can cut downtime by ~30%.

Project risk and schedule pressure

Missed milestones are costly, so reliable delivery commands a premium; in 2024 buyers shifted focus from lowest price to execution certainty as schedule risk rose, with liquidated damages commonly specified at 0.1–0.5% of contract value per day and often priced into bids. Minimax mitigates by leveraging disciplined project management and global field teams to protect margins and meet tight timelines.

- Execution over price

- LD 0.1–0.5%/day

- Schedule risk priced into bids

- PM + global field teams

Multi-site global accounts

Global customers demand standardized solutions and unified pricing; consolidation of spend increases their negotiating leverage, and in 2024 Minimax provides global master service agreements with consistent compliance across regions. Data-driven fleet reporting delivers measurable operational insights and adds stickiness and value to multi-site accounts.

- Global MSAs: standardized pricing and compliance (2024)

- Consolidated spend: higher buyer leverage

- Fleet reporting: increased retention via data-driven insights

Centralized procurement: shortlists ≈3; services ≈40% rev

Large enterprise buyers centralize procurement in 2024, running competitive tenders that pressure price and terms; professional sourcing teams elevate bargaining power. Regulation-driven demand reduces pure price sensitivity; shortlist switching remains (~3 vendors) and value engineering can cut system costs up to 10%. Service contracts ≈40% of OEM lifecycle revenue (2024), typical 5-year terms; uptime SLAs and monitoring lower downtime ~30%.

| Metric | 2024 Value |

|---|---|

| Service contracts (% revenue) | ≈40% |

| Typical contract term | 5 years |

| Vendor shortlist | ≈3 |

| LD | 0.1–0.5%/day |

| Downtime reduction (monitoring) | ≈30% |

| Cost cut (value engineering) | Up to 10% |

What You See Is What You Get

Minimax Porter's Five Forces Analysis

This preview shows the exact Minimax Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the ready-to-use full analysis, fully formatted and professionally written. Once you buy, you'll get instant access to this same file.