Minor International Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

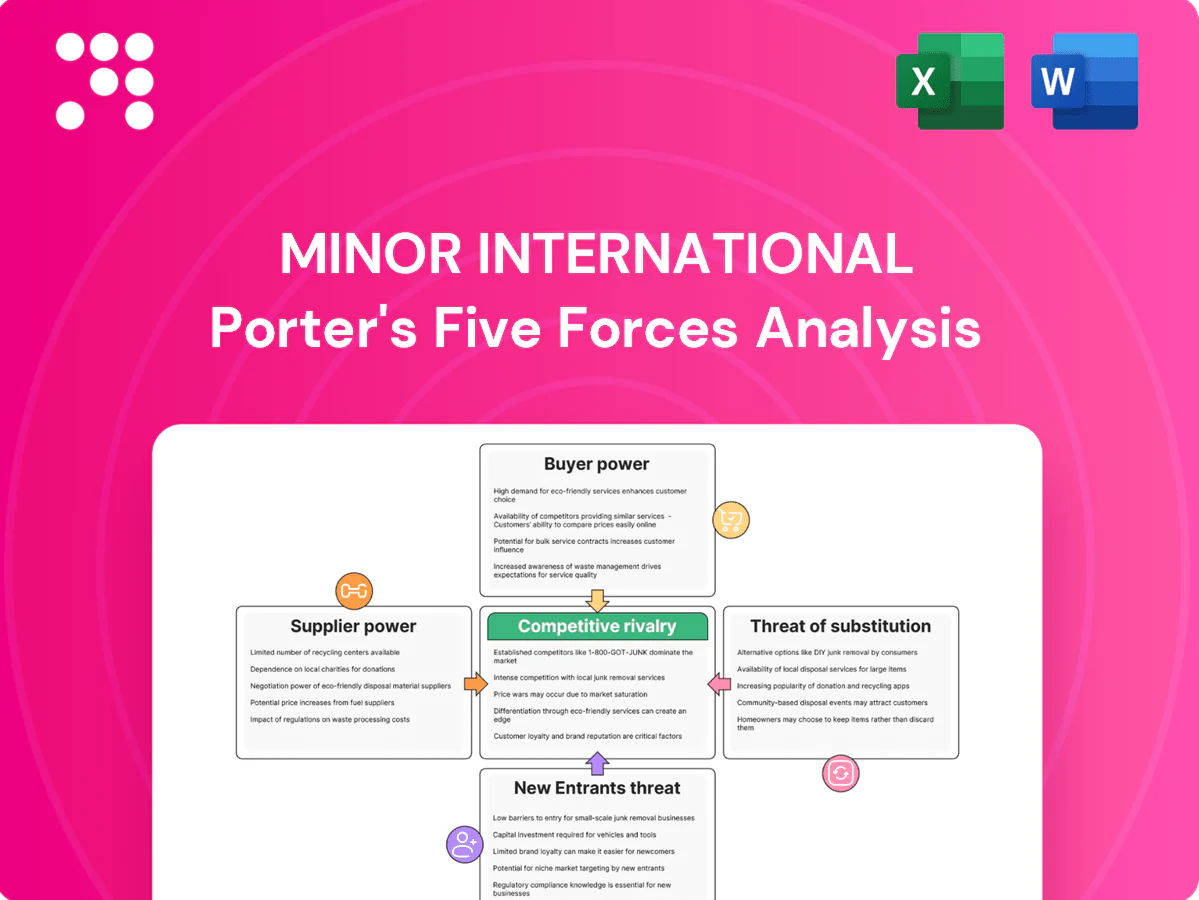

Minor International faces varied pressure from global hotel competitors, bargaining suppliers, and shifting consumer preferences, while scale, brand portfolio and regional growth moderate threat levels. This snapshot highlights key tensions but omits force-by-force ratings, visuals and tactical implications. Unlock the full Porter's Five Forces Analysis to access consultant-grade depth for investment or strategic decisions.

Suppliers Bargaining Power

Global scale in sourcing dampens supplier leverage

Minor International’s multi-brand footprint spans 55 countries with over 500 hotels and more than 2,500 F&B outlets (2024), aggregating demand to secure volume discounts and multi-year contracts. Centralized procurement for F&B, linens, FF&E and amenities lowers unit costs and switching barriers. Preferred-vendor programmes and global tenders standardize pricing. This scale reduces individual supplier bargaining power.

Specialty, location-tied inputs raise dependence

Iconic resorts and luxury positioning demand premium materials, local artisans and bespoke experiences that are difficult to substitute, raising supplier leverage. Remote island and heritage sites—there are over 1,100 UNESCO World Heritage sites worldwide—often constrain vendor choice and extend lead times. Local content and permitting rules in host jurisdictions further limit alternatives, elevating supplier power at select properties.

Labor and talent act as critical suppliers

Skilled hospitality staff, chefs and spa therapists are scarce in key MINT markets, with wage inflation up about 5% in 2024 in Southeast Asia tightening labor supply. High training costs and brand service standards create switching frictions and raise onboarding ROI, increasing effective supplier power. Unionization and stricter labor rules in parts of Europe and Australia add rigidity. Talent dependence thus elevates labor’s supplier-like leverage.

Partial vertical integration and brand ownership offset risk

Partial vertical integration and ownership of brands such as Anantara, AVANI and Oaks, with over 500 hotels across 50+ countries, reduces reliance on third parties; in-house design, project management and standardized SOPs internalize value and speed rollouts, enabling faster supplier substitution and dual-sourcing, which moderates aggregate supplier influence.

- Brand ownership lowers supplier dependency

- In-house design/project mgmt internalizes margins

- Faster supplier substitution/dual-sourcing

- Net effect: reduced aggregate supplier power

Energy and commodity volatility pressures input terms

- Utilities exposure: energy price pass-through constrained

- Food staples: input inflation pressures margins

- Logistics: 2024 freight normalization still volatile

- Mitigants: hedging, menu engineering, short-term contracts

Scale cuts supplier power; ~5% wages and energy swings raise leverage

Minor International’s scale (500+ hotels, 2,500+ F&B outlets in 55 countries, 2024) reduces supplier leverage via centralized procurement, preferred vendors and vertical integration. Luxury resorts, remote sites and scarce skilled staff (wage inflation ~5% SE Asia, 2024) raise supplier power selectively. Energy/food volatility (Brent ~$86/bbl, 2024) can transiently increase leverage.

| Metric | 2024 |

|---|---|

| Hotels | 500+ |

| F&B outlets | 2,500+ |

| SE Asia wage inflation | ~5% |

| Brent | $86/bbl |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Minor International, uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and disruptive forces impacting market share and profitability, with strategic commentary for investor and management use.

A concise, one-sheet Porter's Five Forces for Minor International—instantly visualize competitive pressure with a spider chart and customize force levels as market data shifts. Clean, no-macro layout ready to drop into decks or integrate with broader reports for fast, board-ready insights.

Customers Bargaining Power

OTAs and corporate accounts wield channel power

Online travel agencies aggregate demand and drive visibility, often charging commissions of 15–25% and capturing roughly 30–40% of bookings in many markets, pressuring parity and margins. Corporate and MICE accounts negotiate volume discounts and amenity packages, commonly securing 10–30% rate concessions. Channel-mix management and direct-booking incentives are therefore critical; without strict yield control these buyers exert high bargaining power.

End guests have low switching costs

Price transparency, abundant alternatives and pervasive online reviews make defection easy; in 2024 surveys roughly 70% of consumers consult reviews before dining. Restaurants face especially fluid demand with walk-in and delivery choices and high platform visibility. Loyalty programs and differentiated experiences—loyalty members often spend 10–20% more—can temper churn. Overall consumer buyer power is moderate to high.

Luxury positioning enables price premiums

Luxury positioning lets Minor charge premiums as unique destinations, wellness offerings and curated experiences reduce price sensitivity in upper segments; Minor operated about 537 hotels in 55 countries in 2024, concentrating flagship resorts in limited-room beach and heritage sites. Emotional value and brand equity in Anantara/Avani lower direct comparability, supporting ADR premiums versus midscale peers. Limited capacity in flagship resorts sustains yield, so buyer power diminishes relative to midscale rivals.

Group dispersion diversifies demand

Minor International’s exposure across 58 countries and roughly 2,800 outlets as of 2024 spreads demand across geographies, brands and cuisines, so weakness in one market or segment can be offset by strength elsewhere, reducing dependence on any single buyer cohort and softening aggregate buyer leverage.

- Geographic reach: 58 countries (2024)

- Outlet scale: ~2,800 locations (2024)

- Multi-brand mix: hotels, restaurants, retail

Economic cycles and shocks amplify price sensitivity

Economic downturns prompt travelers and diners to trade down or delay spending, while corporates tighten travel policies and renegotiate contracts, increasing price sensitivity; UNWTO reported international arrivals reached about 88% of 2019 levels in 2023, keeping demand uneven into 2024. Promotions and value bundles have risen, strengthening buyer negotiating stance and making cyclicality an episodic boost to buyer power for Minor International.

- Travelers trade down / delay

- Corporate policy tightening

- Promotions/value bundles ↑

- Cyclicality = episodic buyer power

OTAs grab 30–40% bookings, charge 15–25% fees; reviews give consumers leverage

OTAs capture ~30–40% of bookings and charge 15–25% commissions, pressuring margins; corporate/MICE often secure 10–30% discounts. Price transparency and reviews raise churn (≈70% consult reviews for dining in 2024), giving consumers moderate–high leverage. Luxury brands and limited flagship capacity (537 hotels in 55 countries; ~2,800 outlets across 58 countries in 2024) reduce buyer power in upper segments.

| Metric | 2024 |

|---|---|

| OTAs share | 30–40% |

| OTA commissions | 15–25% |

| Corporate concessions | 10–30% |

| Hotels | 537 (55 countries) |

| Outlets | ~2,800 (58 countries) |

| Dining review consult | ~70% |

Full Version Awaits

Minor International Porter's Five Forces Analysis

This preview shows the complete Minor International Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready to download immediately after purchase. It is the exact document provided to buyers, not a sample or excerpt. No placeholders or mockups: what you see here is the final deliverable, usable for decision-making, presentations, or further research.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Minor International faces varied pressure from global hotel competitors, bargaining suppliers, and shifting consumer preferences, while scale, brand portfolio and regional growth moderate threat levels. This snapshot highlights key tensions but omits force-by-force ratings, visuals and tactical implications. Unlock the full Porter's Five Forces Analysis to access consultant-grade depth for investment or strategic decisions.

Suppliers Bargaining Power

Global scale in sourcing dampens supplier leverage

Minor International’s multi-brand footprint spans 55 countries with over 500 hotels and more than 2,500 F&B outlets (2024), aggregating demand to secure volume discounts and multi-year contracts. Centralized procurement for F&B, linens, FF&E and amenities lowers unit costs and switching barriers. Preferred-vendor programmes and global tenders standardize pricing. This scale reduces individual supplier bargaining power.

Specialty, location-tied inputs raise dependence

Iconic resorts and luxury positioning demand premium materials, local artisans and bespoke experiences that are difficult to substitute, raising supplier leverage. Remote island and heritage sites—there are over 1,100 UNESCO World Heritage sites worldwide—often constrain vendor choice and extend lead times. Local content and permitting rules in host jurisdictions further limit alternatives, elevating supplier power at select properties.

Labor and talent act as critical suppliers

Skilled hospitality staff, chefs and spa therapists are scarce in key MINT markets, with wage inflation up about 5% in 2024 in Southeast Asia tightening labor supply. High training costs and brand service standards create switching frictions and raise onboarding ROI, increasing effective supplier power. Unionization and stricter labor rules in parts of Europe and Australia add rigidity. Talent dependence thus elevates labor’s supplier-like leverage.

Partial vertical integration and brand ownership offset risk

Partial vertical integration and ownership of brands such as Anantara, AVANI and Oaks, with over 500 hotels across 50+ countries, reduces reliance on third parties; in-house design, project management and standardized SOPs internalize value and speed rollouts, enabling faster supplier substitution and dual-sourcing, which moderates aggregate supplier influence.

- Brand ownership lowers supplier dependency

- In-house design/project mgmt internalizes margins

- Faster supplier substitution/dual-sourcing

- Net effect: reduced aggregate supplier power

Energy and commodity volatility pressures input terms

- Utilities exposure: energy price pass-through constrained

- Food staples: input inflation pressures margins

- Logistics: 2024 freight normalization still volatile

- Mitigants: hedging, menu engineering, short-term contracts

Scale cuts supplier power; ~5% wages and energy swings raise leverage

Minor International’s scale (500+ hotels, 2,500+ F&B outlets in 55 countries, 2024) reduces supplier leverage via centralized procurement, preferred vendors and vertical integration. Luxury resorts, remote sites and scarce skilled staff (wage inflation ~5% SE Asia, 2024) raise supplier power selectively. Energy/food volatility (Brent ~$86/bbl, 2024) can transiently increase leverage.

| Metric | 2024 |

|---|---|

| Hotels | 500+ |

| F&B outlets | 2,500+ |

| SE Asia wage inflation | ~5% |

| Brent | $86/bbl |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Minor International, uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and disruptive forces impacting market share and profitability, with strategic commentary for investor and management use.

A concise, one-sheet Porter's Five Forces for Minor International—instantly visualize competitive pressure with a spider chart and customize force levels as market data shifts. Clean, no-macro layout ready to drop into decks or integrate with broader reports for fast, board-ready insights.

Customers Bargaining Power

OTAs and corporate accounts wield channel power

Online travel agencies aggregate demand and drive visibility, often charging commissions of 15–25% and capturing roughly 30–40% of bookings in many markets, pressuring parity and margins. Corporate and MICE accounts negotiate volume discounts and amenity packages, commonly securing 10–30% rate concessions. Channel-mix management and direct-booking incentives are therefore critical; without strict yield control these buyers exert high bargaining power.

End guests have low switching costs

Price transparency, abundant alternatives and pervasive online reviews make defection easy; in 2024 surveys roughly 70% of consumers consult reviews before dining. Restaurants face especially fluid demand with walk-in and delivery choices and high platform visibility. Loyalty programs and differentiated experiences—loyalty members often spend 10–20% more—can temper churn. Overall consumer buyer power is moderate to high.

Luxury positioning enables price premiums

Luxury positioning lets Minor charge premiums as unique destinations, wellness offerings and curated experiences reduce price sensitivity in upper segments; Minor operated about 537 hotels in 55 countries in 2024, concentrating flagship resorts in limited-room beach and heritage sites. Emotional value and brand equity in Anantara/Avani lower direct comparability, supporting ADR premiums versus midscale peers. Limited capacity in flagship resorts sustains yield, so buyer power diminishes relative to midscale rivals.

Group dispersion diversifies demand

Minor International’s exposure across 58 countries and roughly 2,800 outlets as of 2024 spreads demand across geographies, brands and cuisines, so weakness in one market or segment can be offset by strength elsewhere, reducing dependence on any single buyer cohort and softening aggregate buyer leverage.

- Geographic reach: 58 countries (2024)

- Outlet scale: ~2,800 locations (2024)

- Multi-brand mix: hotels, restaurants, retail

Economic cycles and shocks amplify price sensitivity

Economic downturns prompt travelers and diners to trade down or delay spending, while corporates tighten travel policies and renegotiate contracts, increasing price sensitivity; UNWTO reported international arrivals reached about 88% of 2019 levels in 2023, keeping demand uneven into 2024. Promotions and value bundles have risen, strengthening buyer negotiating stance and making cyclicality an episodic boost to buyer power for Minor International.

- Travelers trade down / delay

- Corporate policy tightening

- Promotions/value bundles ↑

- Cyclicality = episodic buyer power

OTAs grab 30–40% bookings, charge 15–25% fees; reviews give consumers leverage

OTAs capture ~30–40% of bookings and charge 15–25% commissions, pressuring margins; corporate/MICE often secure 10–30% discounts. Price transparency and reviews raise churn (≈70% consult reviews for dining in 2024), giving consumers moderate–high leverage. Luxury brands and limited flagship capacity (537 hotels in 55 countries; ~2,800 outlets across 58 countries in 2024) reduce buyer power in upper segments.

| Metric | 2024 |

|---|---|

| OTAs share | 30–40% |

| OTA commissions | 15–25% |

| Corporate concessions | 10–30% |

| Hotels | 537 (55 countries) |

| Outlets | ~2,800 (58 countries) |

| Dining review consult | ~70% |

Full Version Awaits

Minor International Porter's Five Forces Analysis

This preview shows the complete Minor International Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready to download immediately after purchase. It is the exact document provided to buyers, not a sample or excerpt. No placeholders or mockups: what you see here is the final deliverable, usable for decision-making, presentations, or further research.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Minor International faces varied pressure from global hotel competitors, bargaining suppliers, and shifting consumer preferences, while scale, brand portfolio and regional growth moderate threat levels. This snapshot highlights key tensions but omits force-by-force ratings, visuals and tactical implications. Unlock the full Porter's Five Forces Analysis to access consultant-grade depth for investment or strategic decisions.

Suppliers Bargaining Power

Global scale in sourcing dampens supplier leverage

Minor International’s multi-brand footprint spans 55 countries with over 500 hotels and more than 2,500 F&B outlets (2024), aggregating demand to secure volume discounts and multi-year contracts. Centralized procurement for F&B, linens, FF&E and amenities lowers unit costs and switching barriers. Preferred-vendor programmes and global tenders standardize pricing. This scale reduces individual supplier bargaining power.

Specialty, location-tied inputs raise dependence

Iconic resorts and luxury positioning demand premium materials, local artisans and bespoke experiences that are difficult to substitute, raising supplier leverage. Remote island and heritage sites—there are over 1,100 UNESCO World Heritage sites worldwide—often constrain vendor choice and extend lead times. Local content and permitting rules in host jurisdictions further limit alternatives, elevating supplier power at select properties.

Labor and talent act as critical suppliers

Skilled hospitality staff, chefs and spa therapists are scarce in key MINT markets, with wage inflation up about 5% in 2024 in Southeast Asia tightening labor supply. High training costs and brand service standards create switching frictions and raise onboarding ROI, increasing effective supplier power. Unionization and stricter labor rules in parts of Europe and Australia add rigidity. Talent dependence thus elevates labor’s supplier-like leverage.

Partial vertical integration and brand ownership offset risk

Partial vertical integration and ownership of brands such as Anantara, AVANI and Oaks, with over 500 hotels across 50+ countries, reduces reliance on third parties; in-house design, project management and standardized SOPs internalize value and speed rollouts, enabling faster supplier substitution and dual-sourcing, which moderates aggregate supplier influence.

- Brand ownership lowers supplier dependency

- In-house design/project mgmt internalizes margins

- Faster supplier substitution/dual-sourcing

- Net effect: reduced aggregate supplier power

Energy and commodity volatility pressures input terms

- Utilities exposure: energy price pass-through constrained

- Food staples: input inflation pressures margins

- Logistics: 2024 freight normalization still volatile

- Mitigants: hedging, menu engineering, short-term contracts

Scale cuts supplier power; ~5% wages and energy swings raise leverage

Minor International’s scale (500+ hotels, 2,500+ F&B outlets in 55 countries, 2024) reduces supplier leverage via centralized procurement, preferred vendors and vertical integration. Luxury resorts, remote sites and scarce skilled staff (wage inflation ~5% SE Asia, 2024) raise supplier power selectively. Energy/food volatility (Brent ~$86/bbl, 2024) can transiently increase leverage.

| Metric | 2024 |

|---|---|

| Hotels | 500+ |

| F&B outlets | 2,500+ |

| SE Asia wage inflation | ~5% |

| Brent | $86/bbl |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Minor International, uncovering competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and disruptive forces impacting market share and profitability, with strategic commentary for investor and management use.

A concise, one-sheet Porter's Five Forces for Minor International—instantly visualize competitive pressure with a spider chart and customize force levels as market data shifts. Clean, no-macro layout ready to drop into decks or integrate with broader reports for fast, board-ready insights.

Customers Bargaining Power

OTAs and corporate accounts wield channel power

Online travel agencies aggregate demand and drive visibility, often charging commissions of 15–25% and capturing roughly 30–40% of bookings in many markets, pressuring parity and margins. Corporate and MICE accounts negotiate volume discounts and amenity packages, commonly securing 10–30% rate concessions. Channel-mix management and direct-booking incentives are therefore critical; without strict yield control these buyers exert high bargaining power.

End guests have low switching costs

Price transparency, abundant alternatives and pervasive online reviews make defection easy; in 2024 surveys roughly 70% of consumers consult reviews before dining. Restaurants face especially fluid demand with walk-in and delivery choices and high platform visibility. Loyalty programs and differentiated experiences—loyalty members often spend 10–20% more—can temper churn. Overall consumer buyer power is moderate to high.

Luxury positioning enables price premiums

Luxury positioning lets Minor charge premiums as unique destinations, wellness offerings and curated experiences reduce price sensitivity in upper segments; Minor operated about 537 hotels in 55 countries in 2024, concentrating flagship resorts in limited-room beach and heritage sites. Emotional value and brand equity in Anantara/Avani lower direct comparability, supporting ADR premiums versus midscale peers. Limited capacity in flagship resorts sustains yield, so buyer power diminishes relative to midscale rivals.

Group dispersion diversifies demand

Minor International’s exposure across 58 countries and roughly 2,800 outlets as of 2024 spreads demand across geographies, brands and cuisines, so weakness in one market or segment can be offset by strength elsewhere, reducing dependence on any single buyer cohort and softening aggregate buyer leverage.

- Geographic reach: 58 countries (2024)

- Outlet scale: ~2,800 locations (2024)

- Multi-brand mix: hotels, restaurants, retail

Economic cycles and shocks amplify price sensitivity

Economic downturns prompt travelers and diners to trade down or delay spending, while corporates tighten travel policies and renegotiate contracts, increasing price sensitivity; UNWTO reported international arrivals reached about 88% of 2019 levels in 2023, keeping demand uneven into 2024. Promotions and value bundles have risen, strengthening buyer negotiating stance and making cyclicality an episodic boost to buyer power for Minor International.

- Travelers trade down / delay

- Corporate policy tightening

- Promotions/value bundles ↑

- Cyclicality = episodic buyer power

OTAs grab 30–40% bookings, charge 15–25% fees; reviews give consumers leverage

OTAs capture ~30–40% of bookings and charge 15–25% commissions, pressuring margins; corporate/MICE often secure 10–30% discounts. Price transparency and reviews raise churn (≈70% consult reviews for dining in 2024), giving consumers moderate–high leverage. Luxury brands and limited flagship capacity (537 hotels in 55 countries; ~2,800 outlets across 58 countries in 2024) reduce buyer power in upper segments.

| Metric | 2024 |

|---|---|

| OTAs share | 30–40% |

| OTA commissions | 15–25% |

| Corporate concessions | 10–30% |

| Hotels | 537 (55 countries) |

| Outlets | ~2,800 (58 countries) |

| Dining review consult | ~70% |

Full Version Awaits

Minor International Porter's Five Forces Analysis

This preview shows the complete Minor International Porter’s Five Forces analysis you’ll receive—fully written, formatted, and ready to download immediately after purchase. It is the exact document provided to buyers, not a sample or excerpt. No placeholders or mockups: what you see here is the final deliverable, usable for decision-making, presentations, or further research.