Miquel y Costas & Miquel Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

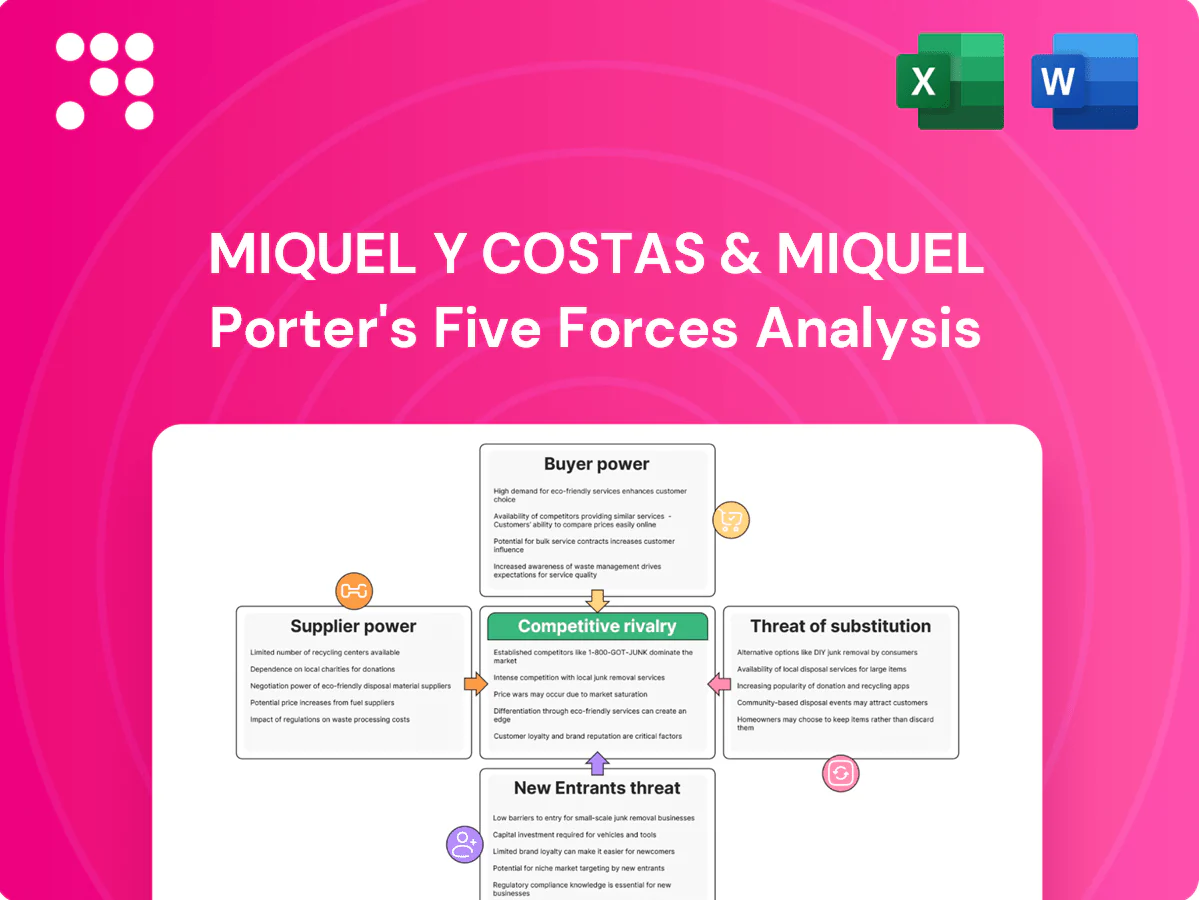

Miquel y Costas & Miquel faces moderate supplier power, niche customer segments, and steady barriers to entry driven by specialized production and brand heritage. Competitive rivalry is shaped by legacy players and evolving packaging trends, while substitutes and buyer pressure vary by end market. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty fiber concentration

Ultra-thin papers depend on high-grade cellulose, flax, hemp and tailored pulp blends sourced from a limited pool of qualified suppliers, a market still concentrated among roughly 10 major pulp producers as of 2024, which raises supplier bargaining power on price and allocation. Miquel y Costas’ scale, multi-sourcing strategy and long-term contracts reduce single-supplier exposure, while in-house formulation expertise further tempers supplier leverage.

Chemicals and additives

Functional papers require specialty chemicals, resins and coatings with tight specs, which elevates supplier importance for Miquel y Costas; approved vendor lists in tobacco-related applications further shrink the supplier universe and raise bargaining power. Standardized formulations across sites and deep process know-how enable switching among vetted suppliers, limiting dependence. Backward integration in recipe development has reduced reliance on any single chemical provider.

Energy and utilities

Paper machines are highly energy-intensive, with energy often accounting for roughly 10–15% of production costs; EU industrial electricity averaged about €0.14/kWh in 2024 and TTF gas averaged near €30/MWh, exposing Miquel y Costas to input-price swings. Utility supplier concentration and market volatility can compress margins during spikes. Hedging, onsite cogeneration and efficiency capex (boilers, insulation) materially reduce this supplier power, while geographic plant diversification evens regional energy risk.

Capital equipment OEMs

Valmet, Voith and ANDRITZ are the leading OEMs for high-speed paper machines in 2024, and their bespoke high-speed lines require custom specifications, raising supplier bargaining power. Long lead times for spare parts and specialized maintenance create switching frictions that favor OEMs, though Miquel y Costas’ technical depth and preventive maintenance programs reduce unplanned dependence. Maintaining multi-OEM supplier relationships improves negotiating leverage over lifecycle costs.

Logistics and fiber sourcing

Global sourcing of pulp and specialty fibers exposes Miquel y Costas to volatile freight and port constraints; container freight rates fell roughly 60% from 2021 peaks by 2024, yet spot capacity tightness in late 2024 pushed some charter rates up ~25%, increasing supplier logistics leverage.

Diversified routes, higher in-transit inventories and nearby mills to major ports moderate that leverage, reducing disruption impact and transit costs for key European operations.

- Freight volatility: -60% vs 2021 peaks (2024)

- Late-2024 charter tightness: +25% pressure

- Mitigants: diversified routes, buffer inventories, port-adjacent mills

High supplier & OEM power; energy €0.14/kWh, freight volatile; mitigated via multi-sourcing

Supplier power is elevated by ~10 major pulp producers (2024) and OEM dominance (Valmet/Voith/ANDRITZ), plus tight specialty-chemical approval pools; energy at ~€0.14/kWh and gas ~€30/MWh (2024) and freight volatility (-60% vs 2021, late-2024 charter +25%) add input risk. Miquel y Costas mitigates via multi-sourcing, long-term contracts, in-house formulation, hedging and cogeneration.

| Factor | 2024 metric | Impact |

|---|---|---|

| Pulp concentration | ~10 suppliers | High |

| Energy | €0.14/kWh; €30/MWh | Medium-High |

| OEMs | Valmet/Voith/ANDRITZ | High |

| Freight | -60% vs 2021; +25% charter | Medium |

What is included in the product

Concise Five Forces analysis for Miquel y Costas & Miquel uncovering competitive intensity, supplier and buyer power, substitute threats, and entry barriers, with strategic commentary on disruptive trends and market dynamics; fully editable for inclusion in investor materials, strategy decks, or academic projects.

A clear, one-sheet Five Forces snapshot for Miquel y Costas & Miquel—instantly highlights supplier/customer bargaining, substitutes, new entrants and rivalry so executives can quickly pinpoint strategic pressures and act with confidence.

Customers Bargaining Power

Large tobacco customers

Large cigarette-paper buyers are few, dominated by majors such as Philip Morris, BAT and JTI, which together accounted for over 50% of global cigarette volume in 2024, giving them strong price leverage. They demand strict specs, audits and dual sourcing, drive long qualification cycles that create supplier stickiness but trigger tough periodic tenders. Miquel y Costas must protect pricing through demonstrable performance, reliability and value-added services to offset buyer power.

Specialty converters

Specialty converters face fragmented industrial and consumer buyer bases in 2024, which dilutes individual bargaining power. Custom grades and tailored coatings raise switching costs and favor Miquel y Costas in renewals. Still, a broad set of alternate specialty suppliers caps pricing upside. Strong service levels and co-development agreements increasingly secure multi-year contracts.

Publishers/ultra-thin print

Bible and ultra-thin print buyers are niche and highly quality-sensitive, and rising digital reading trends constrain volume growth, intensifying buyer focus on price. Product differentiation in opacity, smoothness and runnability reduces direct comparability and helps command premium pricing. Long-standing supply relationships with publishers and converters further support steady margins despite volume pressure.

Global sourcing options

Buyers can benchmark suppliers across European, Asian and American producers, increasing price and terms pressure; transparency from digital procurement platforms amplifies this negotiating leverage. Certifications such as FSC and PEFC and food-contact approvals restrict viable suppliers to certified mills, limiting buyer switching. Miquel y Costas’ global sales footprint in over 100 countries and its compliance portfolio of FSC/PEFC and food-contact certifications mitigate customer bargaining power.

- Global benchmarking: Europe/Asia/US comparisons

- Certifications: FSC/PEFC + food-contact restrict suppliers

- Miquel y Costas: >100-country reach, certified offerings

Switching and qualification costs

Tobacco and critical-paper applications require lengthy trials and regulatory checks often lasting 12–36 months, raising switching and qualification costs and reducing immediate buyer leverage. Price concessions are commonly exchanged for multi-year volume contracts (typically 3–5 years). Performance guarantees and dedicated technical service teams further lock in supplier choice despite large-scale procurement.

- Trial/approval time: 12–36 months

- Common contract length: 3–5 years

- Outcome: lower short-term buyer power

Major buyers >50% drive price leverage; global reach and long trials limit switching

Major cigarette buyers (Philip Morris, BAT, JTI) represented >50% of global cigarette volume in 2024, giving strong price leverage; specialty and niche buyers are more fragmented. Certifications (FSC/PEFC, food-contact) and Miquel y Costas’ presence in >100 countries mitigate switching. Lengthy trials (12–36 months) and typical 3–5 year contracts lower short-term buyer power.

| Metric | 2024 / Typical |

|---|---|

| Major buyer market share | >50% |

| Geographic reach | >100 countries |

| Trial/approval time | 12–36 months |

| Common contract length | 3–5 years |

Full Version Awaits

Miquel y Costas & Miquel Porter's Five Forces Analysis

This Porter's Five Forces analysis for Miquel y Costas & Miquel examines industry rivalry, supplier and buyer power, threat of substitutes and entry, and strategic implications for competitive positioning. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download and use the moment you buy, providing actionable insights for decision-making.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Miquel y Costas & Miquel faces moderate supplier power, niche customer segments, and steady barriers to entry driven by specialized production and brand heritage. Competitive rivalry is shaped by legacy players and evolving packaging trends, while substitutes and buyer pressure vary by end market. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty fiber concentration

Ultra-thin papers depend on high-grade cellulose, flax, hemp and tailored pulp blends sourced from a limited pool of qualified suppliers, a market still concentrated among roughly 10 major pulp producers as of 2024, which raises supplier bargaining power on price and allocation. Miquel y Costas’ scale, multi-sourcing strategy and long-term contracts reduce single-supplier exposure, while in-house formulation expertise further tempers supplier leverage.

Chemicals and additives

Functional papers require specialty chemicals, resins and coatings with tight specs, which elevates supplier importance for Miquel y Costas; approved vendor lists in tobacco-related applications further shrink the supplier universe and raise bargaining power. Standardized formulations across sites and deep process know-how enable switching among vetted suppliers, limiting dependence. Backward integration in recipe development has reduced reliance on any single chemical provider.

Energy and utilities

Paper machines are highly energy-intensive, with energy often accounting for roughly 10–15% of production costs; EU industrial electricity averaged about €0.14/kWh in 2024 and TTF gas averaged near €30/MWh, exposing Miquel y Costas to input-price swings. Utility supplier concentration and market volatility can compress margins during spikes. Hedging, onsite cogeneration and efficiency capex (boilers, insulation) materially reduce this supplier power, while geographic plant diversification evens regional energy risk.

Capital equipment OEMs

Valmet, Voith and ANDRITZ are the leading OEMs for high-speed paper machines in 2024, and their bespoke high-speed lines require custom specifications, raising supplier bargaining power. Long lead times for spare parts and specialized maintenance create switching frictions that favor OEMs, though Miquel y Costas’ technical depth and preventive maintenance programs reduce unplanned dependence. Maintaining multi-OEM supplier relationships improves negotiating leverage over lifecycle costs.

Logistics and fiber sourcing

Global sourcing of pulp and specialty fibers exposes Miquel y Costas to volatile freight and port constraints; container freight rates fell roughly 60% from 2021 peaks by 2024, yet spot capacity tightness in late 2024 pushed some charter rates up ~25%, increasing supplier logistics leverage.

Diversified routes, higher in-transit inventories and nearby mills to major ports moderate that leverage, reducing disruption impact and transit costs for key European operations.

- Freight volatility: -60% vs 2021 peaks (2024)

- Late-2024 charter tightness: +25% pressure

- Mitigants: diversified routes, buffer inventories, port-adjacent mills

High supplier & OEM power; energy €0.14/kWh, freight volatile; mitigated via multi-sourcing

Supplier power is elevated by ~10 major pulp producers (2024) and OEM dominance (Valmet/Voith/ANDRITZ), plus tight specialty-chemical approval pools; energy at ~€0.14/kWh and gas ~€30/MWh (2024) and freight volatility (-60% vs 2021, late-2024 charter +25%) add input risk. Miquel y Costas mitigates via multi-sourcing, long-term contracts, in-house formulation, hedging and cogeneration.

| Factor | 2024 metric | Impact |

|---|---|---|

| Pulp concentration | ~10 suppliers | High |

| Energy | €0.14/kWh; €30/MWh | Medium-High |

| OEMs | Valmet/Voith/ANDRITZ | High |

| Freight | -60% vs 2021; +25% charter | Medium |

What is included in the product

Concise Five Forces analysis for Miquel y Costas & Miquel uncovering competitive intensity, supplier and buyer power, substitute threats, and entry barriers, with strategic commentary on disruptive trends and market dynamics; fully editable for inclusion in investor materials, strategy decks, or academic projects.

A clear, one-sheet Five Forces snapshot for Miquel y Costas & Miquel—instantly highlights supplier/customer bargaining, substitutes, new entrants and rivalry so executives can quickly pinpoint strategic pressures and act with confidence.

Customers Bargaining Power

Large tobacco customers

Large cigarette-paper buyers are few, dominated by majors such as Philip Morris, BAT and JTI, which together accounted for over 50% of global cigarette volume in 2024, giving them strong price leverage. They demand strict specs, audits and dual sourcing, drive long qualification cycles that create supplier stickiness but trigger tough periodic tenders. Miquel y Costas must protect pricing through demonstrable performance, reliability and value-added services to offset buyer power.

Specialty converters

Specialty converters face fragmented industrial and consumer buyer bases in 2024, which dilutes individual bargaining power. Custom grades and tailored coatings raise switching costs and favor Miquel y Costas in renewals. Still, a broad set of alternate specialty suppliers caps pricing upside. Strong service levels and co-development agreements increasingly secure multi-year contracts.

Publishers/ultra-thin print

Bible and ultra-thin print buyers are niche and highly quality-sensitive, and rising digital reading trends constrain volume growth, intensifying buyer focus on price. Product differentiation in opacity, smoothness and runnability reduces direct comparability and helps command premium pricing. Long-standing supply relationships with publishers and converters further support steady margins despite volume pressure.

Global sourcing options

Buyers can benchmark suppliers across European, Asian and American producers, increasing price and terms pressure; transparency from digital procurement platforms amplifies this negotiating leverage. Certifications such as FSC and PEFC and food-contact approvals restrict viable suppliers to certified mills, limiting buyer switching. Miquel y Costas’ global sales footprint in over 100 countries and its compliance portfolio of FSC/PEFC and food-contact certifications mitigate customer bargaining power.

- Global benchmarking: Europe/Asia/US comparisons

- Certifications: FSC/PEFC + food-contact restrict suppliers

- Miquel y Costas: >100-country reach, certified offerings

Switching and qualification costs

Tobacco and critical-paper applications require lengthy trials and regulatory checks often lasting 12–36 months, raising switching and qualification costs and reducing immediate buyer leverage. Price concessions are commonly exchanged for multi-year volume contracts (typically 3–5 years). Performance guarantees and dedicated technical service teams further lock in supplier choice despite large-scale procurement.

- Trial/approval time: 12–36 months

- Common contract length: 3–5 years

- Outcome: lower short-term buyer power

Major buyers >50% drive price leverage; global reach and long trials limit switching

Major cigarette buyers (Philip Morris, BAT, JTI) represented >50% of global cigarette volume in 2024, giving strong price leverage; specialty and niche buyers are more fragmented. Certifications (FSC/PEFC, food-contact) and Miquel y Costas’ presence in >100 countries mitigate switching. Lengthy trials (12–36 months) and typical 3–5 year contracts lower short-term buyer power.

| Metric | 2024 / Typical |

|---|---|

| Major buyer market share | >50% |

| Geographic reach | >100 countries |

| Trial/approval time | 12–36 months |

| Common contract length | 3–5 years |

Full Version Awaits

Miquel y Costas & Miquel Porter's Five Forces Analysis

This Porter's Five Forces analysis for Miquel y Costas & Miquel examines industry rivalry, supplier and buyer power, threat of substitutes and entry, and strategic implications for competitive positioning. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download and use the moment you buy, providing actionable insights for decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Miquel y Costas & Miquel faces moderate supplier power, niche customer segments, and steady barriers to entry driven by specialized production and brand heritage. Competitive rivalry is shaped by legacy players and evolving packaging trends, while substitutes and buyer pressure vary by end market. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty fiber concentration

Ultra-thin papers depend on high-grade cellulose, flax, hemp and tailored pulp blends sourced from a limited pool of qualified suppliers, a market still concentrated among roughly 10 major pulp producers as of 2024, which raises supplier bargaining power on price and allocation. Miquel y Costas’ scale, multi-sourcing strategy and long-term contracts reduce single-supplier exposure, while in-house formulation expertise further tempers supplier leverage.

Chemicals and additives

Functional papers require specialty chemicals, resins and coatings with tight specs, which elevates supplier importance for Miquel y Costas; approved vendor lists in tobacco-related applications further shrink the supplier universe and raise bargaining power. Standardized formulations across sites and deep process know-how enable switching among vetted suppliers, limiting dependence. Backward integration in recipe development has reduced reliance on any single chemical provider.

Energy and utilities

Paper machines are highly energy-intensive, with energy often accounting for roughly 10–15% of production costs; EU industrial electricity averaged about €0.14/kWh in 2024 and TTF gas averaged near €30/MWh, exposing Miquel y Costas to input-price swings. Utility supplier concentration and market volatility can compress margins during spikes. Hedging, onsite cogeneration and efficiency capex (boilers, insulation) materially reduce this supplier power, while geographic plant diversification evens regional energy risk.

Capital equipment OEMs

Valmet, Voith and ANDRITZ are the leading OEMs for high-speed paper machines in 2024, and their bespoke high-speed lines require custom specifications, raising supplier bargaining power. Long lead times for spare parts and specialized maintenance create switching frictions that favor OEMs, though Miquel y Costas’ technical depth and preventive maintenance programs reduce unplanned dependence. Maintaining multi-OEM supplier relationships improves negotiating leverage over lifecycle costs.

Logistics and fiber sourcing

Global sourcing of pulp and specialty fibers exposes Miquel y Costas to volatile freight and port constraints; container freight rates fell roughly 60% from 2021 peaks by 2024, yet spot capacity tightness in late 2024 pushed some charter rates up ~25%, increasing supplier logistics leverage.

Diversified routes, higher in-transit inventories and nearby mills to major ports moderate that leverage, reducing disruption impact and transit costs for key European operations.

- Freight volatility: -60% vs 2021 peaks (2024)

- Late-2024 charter tightness: +25% pressure

- Mitigants: diversified routes, buffer inventories, port-adjacent mills

High supplier & OEM power; energy €0.14/kWh, freight volatile; mitigated via multi-sourcing

Supplier power is elevated by ~10 major pulp producers (2024) and OEM dominance (Valmet/Voith/ANDRITZ), plus tight specialty-chemical approval pools; energy at ~€0.14/kWh and gas ~€30/MWh (2024) and freight volatility (-60% vs 2021, late-2024 charter +25%) add input risk. Miquel y Costas mitigates via multi-sourcing, long-term contracts, in-house formulation, hedging and cogeneration.

| Factor | 2024 metric | Impact |

|---|---|---|

| Pulp concentration | ~10 suppliers | High |

| Energy | €0.14/kWh; €30/MWh | Medium-High |

| OEMs | Valmet/Voith/ANDRITZ | High |

| Freight | -60% vs 2021; +25% charter | Medium |

What is included in the product

Concise Five Forces analysis for Miquel y Costas & Miquel uncovering competitive intensity, supplier and buyer power, substitute threats, and entry barriers, with strategic commentary on disruptive trends and market dynamics; fully editable for inclusion in investor materials, strategy decks, or academic projects.

A clear, one-sheet Five Forces snapshot for Miquel y Costas & Miquel—instantly highlights supplier/customer bargaining, substitutes, new entrants and rivalry so executives can quickly pinpoint strategic pressures and act with confidence.

Customers Bargaining Power

Large tobacco customers

Large cigarette-paper buyers are few, dominated by majors such as Philip Morris, BAT and JTI, which together accounted for over 50% of global cigarette volume in 2024, giving them strong price leverage. They demand strict specs, audits and dual sourcing, drive long qualification cycles that create supplier stickiness but trigger tough periodic tenders. Miquel y Costas must protect pricing through demonstrable performance, reliability and value-added services to offset buyer power.

Specialty converters

Specialty converters face fragmented industrial and consumer buyer bases in 2024, which dilutes individual bargaining power. Custom grades and tailored coatings raise switching costs and favor Miquel y Costas in renewals. Still, a broad set of alternate specialty suppliers caps pricing upside. Strong service levels and co-development agreements increasingly secure multi-year contracts.

Publishers/ultra-thin print

Bible and ultra-thin print buyers are niche and highly quality-sensitive, and rising digital reading trends constrain volume growth, intensifying buyer focus on price. Product differentiation in opacity, smoothness and runnability reduces direct comparability and helps command premium pricing. Long-standing supply relationships with publishers and converters further support steady margins despite volume pressure.

Global sourcing options

Buyers can benchmark suppliers across European, Asian and American producers, increasing price and terms pressure; transparency from digital procurement platforms amplifies this negotiating leverage. Certifications such as FSC and PEFC and food-contact approvals restrict viable suppliers to certified mills, limiting buyer switching. Miquel y Costas’ global sales footprint in over 100 countries and its compliance portfolio of FSC/PEFC and food-contact certifications mitigate customer bargaining power.

- Global benchmarking: Europe/Asia/US comparisons

- Certifications: FSC/PEFC + food-contact restrict suppliers

- Miquel y Costas: >100-country reach, certified offerings

Switching and qualification costs

Tobacco and critical-paper applications require lengthy trials and regulatory checks often lasting 12–36 months, raising switching and qualification costs and reducing immediate buyer leverage. Price concessions are commonly exchanged for multi-year volume contracts (typically 3–5 years). Performance guarantees and dedicated technical service teams further lock in supplier choice despite large-scale procurement.

- Trial/approval time: 12–36 months

- Common contract length: 3–5 years

- Outcome: lower short-term buyer power

Major buyers >50% drive price leverage; global reach and long trials limit switching

Major cigarette buyers (Philip Morris, BAT, JTI) represented >50% of global cigarette volume in 2024, giving strong price leverage; specialty and niche buyers are more fragmented. Certifications (FSC/PEFC, food-contact) and Miquel y Costas’ presence in >100 countries mitigate switching. Lengthy trials (12–36 months) and typical 3–5 year contracts lower short-term buyer power.

| Metric | 2024 / Typical |

|---|---|

| Major buyer market share | >50% |

| Geographic reach | >100 countries |

| Trial/approval time | 12–36 months |

| Common contract length | 3–5 years |

Full Version Awaits

Miquel y Costas & Miquel Porter's Five Forces Analysis

This Porter's Five Forces analysis for Miquel y Costas & Miquel examines industry rivalry, supplier and buyer power, threat of substitutes and entry, and strategic implications for competitive positioning. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download and use the moment you buy, providing actionable insights for decision-making.