Mirum PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

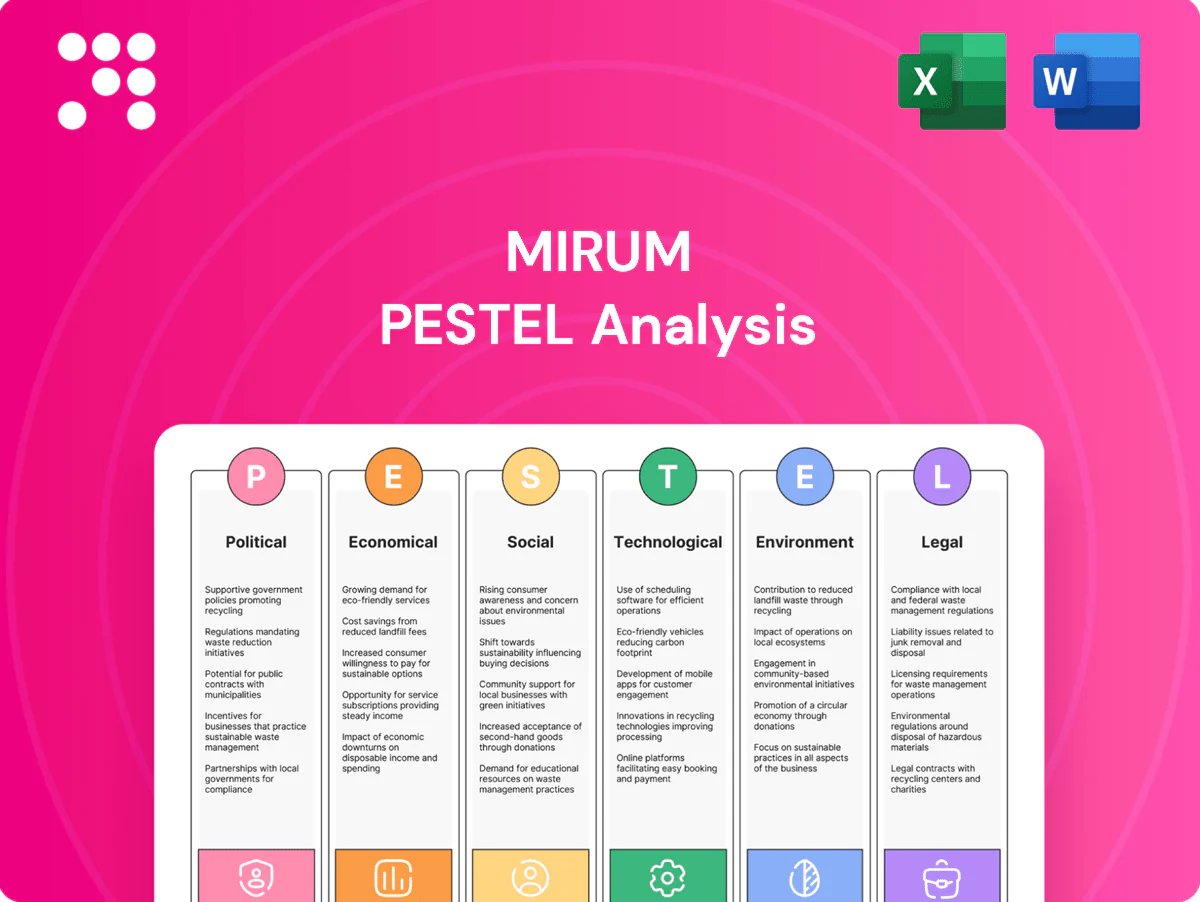

Gain a strategic advantage with our Mirum PESTLE Analysis—three to five sentence summary revealing how political, economic, social, technological, legal, and environmental forces shape Mirum’s trajectory. Perfect for investors and strategists, it surfaces risks, growth levers, and market signals. Purchase the full report for detailed, actionable insights and ready-to-use charts for immediate decision-making.

Political factors

Regulatory policy stability

Biopharma outcomes for Mirum hinge on FDA, EMA and other regulators’ guidance for rare liver diseases; shifts in endpoints or accelerated pathways materially affect launch timing. Consistent orphan frameworks (Orphan Drug Act 1983) offer 7 years US and 10 years EU exclusivity, de‑risking timelines. Policy volatility increases trial costs and uncertainty; FDA review goals are 6 months (priority) and 10 months (standard).

Orphan and pediatric incentives

US orphan exclusivity (7 years) and EU orphan protection (10 years), plus pediatric priority review vouchers (PRVs) and fee waivers, materially boost ROI for Mirum in cholestatic diseases. PRV sales have historically ranged up to about 350 million USD, helping offset small patient pools. Any rollback of these incentives would compress margins; stronger incentives would significantly improve pipeline economics.

Drug pricing scrutiny

National pricing reforms, notably the US Inflation Reduction Act (enacted 2022) enabling Medicare negotiation from 2026, target specialty drugs that now account for roughly 55% of US drug spend (IQVIA 2023). Reference pricing and health-technology assessments in markets like Europe cap revenue per patient through value-based ceilings. Market access increasingly requires robust randomized and real-world outcomes evidence. Political pressure is raising rebate demands and constraining list-price growth.

Public health funding priorities

Grants from NIH programs such as the Rare Diseases Clinical Research Network (RDCRN, NCATS-supported since 2003) and EU Horizon Europe (95.5 billion EUR programme 2021–27) underpin rare-disease networks; prioritizing pediatric liver conditions like biliary atresia (incidence ~1 in 10,000–15,000 births) can accelerate trial enrollment, while budget constraints risk diverting funds away from specialty trials; stable funding strengthens registries and data infrastructure.

- NIH/NCATS RDCRN

- Horizon Europe 95.5 billion EUR

- Biliary atresia ~1/10,000–15,000

- Stable funding → stronger registries

Geopolitics and supply chains

Geopolitical tensions and export controls increasingly affect APIs and key intermediates, with China and India supplying over 60% of global APIs (2023), raising exposure for Mirum; sanctions and logistics bottlenecks have delayed manufacturing by months in past shock events; localization policies in the US, EU and India are driving incentives for regional production; diversification across suppliers and sites mitigates political shocks.

- trade_tensions: export controls on APIs

- sanctions_logistics: manufacturing delays

- localization: regional production mandates

- mitigation: supply diversification

Orphan exclusivity shortens timelines; Medicare pricing and >60% API China/India

Regulatory shifts (FDA/EMA) dictate Mirum launch timing; orphan pathways (US 7y, EU 10y) de‑risk timelines. Medicare negotiation from 2026 and HTA/reference pricing compress US/EU pricing; PRVs have fetched up to 350M USD. API exposure (>60% from China/India in 2023) raises supply-chain geopolitical risk.

| Policy/Data | Figure/Impact |

|---|---|

| Orphan exclusivity | US 7y / EU 10y |

| Medicare negotiation | Effective 2026 (IRA 2022) |

| PRV value | Up to 350M USD |

| API sourcing | >60% from China/India (2023) |

What is included in the product

Explores how macro-environmental forces uniquely affect Mirum across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region- and industry-specific insights; designed for executives and investors, it’s ready for reports and includes forward-looking scenarios to inform strategy and risk mitigation.

A concise, visually segmented Mirum PESTLE summary that highlights external risks and strategic opportunities for quick inclusion in presentations or planning sessions; editable notes let teams tailor insights to region or business line.

Economic factors

Capital market conditions

Biotech financing cycles dictate R&D pace and runway, with global life‑sciences VC recovering to roughly $31B in 2024 versus 2021 peaks, lengthening some programs but keeping burn discipline. Tight IPO/SPAC windows push Mirum toward partnerships or debt financing. Higher rates — Fed target ~5.25–5.50% in 2024–mid‑2025 — raise discount rates and compress valuations. Bull market windows enable label expansions and lifecycle investments.

Reimbursement dynamics

Payer mix and HTA outcomes plus formularies dictate realized price, with the three largest PBMs controlling roughly 70% of US lives, concentrating negotiating power. Premium therapies increasingly face outcomes-based contracts as payers demand real-world value; relatively few contracts have broad use. Coverage decision delays commonly extend time-to-revenue by about 12 months, while robust health-economic dossiers materially improve uptake.

Rare disease pricing elasticity

Ultra-rare therapies command premium pricing—examples include Zolgensma at about $2.1m and Luxturna near $850k—yet face intense payer and HTA scrutiny. Small patient volumes mean a handful of accounts can drive large revenue swings, amplifying volatility. Adherence and hub programs materially affect net revenue through persistence and wastage reduction. EU external reference pricing causes regional price cuts to ripple across linked markets.

M&A and partnerships

Strategic alliances let Mirum share development risk and broaden geographic reach, a trend reinforced by big pharma consolidation such as Pfizer’s $43B acquisition of Seagen in 2023; BD deals supply non-dilutive capital and pipeline breadth, while acquisitive moves can rapidly reset competitive landscapes. Valuation multiples hinge on proof-of-concept and de-risked assets.

- Risk-sharing

- Non-dilutive BD capital

- Competitive reset (e.g., Pfizer-Seagen $43B)

- Multiples tied to PoC/de-risking

FX and inflation

Mirum's global sales expose earnings to currency swings as FX volatility (DXY moved about 6% in 2024) can compress reported revenue; inflation—US CPI ~3.4% and eurozone ~2.4% in 2024—raises COGS, trial site costs and SG&A. Hedging and long-term supplier/contract deals can stabilize margins, but Mirum's pricing power may not fully offset sharp cost surges.

- FX exposure: material for cross-border revenue

- Inflation: increases COGS, trial/site, SG&A

- Mitigants: hedging, long-term contracts

Orphan exclusivity shortens timelines; Medicare pricing and >60% API China/India

Higher rates (Fed ~5.25–5.50% in 2024–mid‑2025) and tighter biotech VC ($31B global 2024) compress valuations and push Mirum to partner/debt options; FX swings (DXY ~6% in 2024) and inflation (US CPI ~3.4%, eurozone ~2.4% in 2024) raise COGS and trial costs. PBM concentration (~70% US lives) and HTA delays extend time‑to‑revenue ~12 months; strategic BD (Pfizer‑Seagen $43B) reshapes competitiveness.

| Metric | Value |

|---|---|

| Fed rate | 5.25–5.50% |

| Life‑sciences VC 2024 | $31B |

| DXY 2024 move | ~6% |

| US CPI 2024 | 3.4% |

Full Version Awaits

Mirum PESTLE Analysis

The Mirum PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and professional structure are identical to the downloadable file, with no placeholders or teasers. After checkout you’ll instantly get this same finished report, ready for implementation.

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our Mirum PESTLE Analysis—three to five sentence summary revealing how political, economic, social, technological, legal, and environmental forces shape Mirum’s trajectory. Perfect for investors and strategists, it surfaces risks, growth levers, and market signals. Purchase the full report for detailed, actionable insights and ready-to-use charts for immediate decision-making.

Political factors

Regulatory policy stability

Biopharma outcomes for Mirum hinge on FDA, EMA and other regulators’ guidance for rare liver diseases; shifts in endpoints or accelerated pathways materially affect launch timing. Consistent orphan frameworks (Orphan Drug Act 1983) offer 7 years US and 10 years EU exclusivity, de‑risking timelines. Policy volatility increases trial costs and uncertainty; FDA review goals are 6 months (priority) and 10 months (standard).

Orphan and pediatric incentives

US orphan exclusivity (7 years) and EU orphan protection (10 years), plus pediatric priority review vouchers (PRVs) and fee waivers, materially boost ROI for Mirum in cholestatic diseases. PRV sales have historically ranged up to about 350 million USD, helping offset small patient pools. Any rollback of these incentives would compress margins; stronger incentives would significantly improve pipeline economics.

Drug pricing scrutiny

National pricing reforms, notably the US Inflation Reduction Act (enacted 2022) enabling Medicare negotiation from 2026, target specialty drugs that now account for roughly 55% of US drug spend (IQVIA 2023). Reference pricing and health-technology assessments in markets like Europe cap revenue per patient through value-based ceilings. Market access increasingly requires robust randomized and real-world outcomes evidence. Political pressure is raising rebate demands and constraining list-price growth.

Public health funding priorities

Grants from NIH programs such as the Rare Diseases Clinical Research Network (RDCRN, NCATS-supported since 2003) and EU Horizon Europe (95.5 billion EUR programme 2021–27) underpin rare-disease networks; prioritizing pediatric liver conditions like biliary atresia (incidence ~1 in 10,000–15,000 births) can accelerate trial enrollment, while budget constraints risk diverting funds away from specialty trials; stable funding strengthens registries and data infrastructure.

- NIH/NCATS RDCRN

- Horizon Europe 95.5 billion EUR

- Biliary atresia ~1/10,000–15,000

- Stable funding → stronger registries

Geopolitics and supply chains

Geopolitical tensions and export controls increasingly affect APIs and key intermediates, with China and India supplying over 60% of global APIs (2023), raising exposure for Mirum; sanctions and logistics bottlenecks have delayed manufacturing by months in past shock events; localization policies in the US, EU and India are driving incentives for regional production; diversification across suppliers and sites mitigates political shocks.

- trade_tensions: export controls on APIs

- sanctions_logistics: manufacturing delays

- localization: regional production mandates

- mitigation: supply diversification

Orphan exclusivity shortens timelines; Medicare pricing and >60% API China/India

Regulatory shifts (FDA/EMA) dictate Mirum launch timing; orphan pathways (US 7y, EU 10y) de‑risk timelines. Medicare negotiation from 2026 and HTA/reference pricing compress US/EU pricing; PRVs have fetched up to 350M USD. API exposure (>60% from China/India in 2023) raises supply-chain geopolitical risk.

| Policy/Data | Figure/Impact |

|---|---|

| Orphan exclusivity | US 7y / EU 10y |

| Medicare negotiation | Effective 2026 (IRA 2022) |

| PRV value | Up to 350M USD |

| API sourcing | >60% from China/India (2023) |

What is included in the product

Explores how macro-environmental forces uniquely affect Mirum across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region- and industry-specific insights; designed for executives and investors, it’s ready for reports and includes forward-looking scenarios to inform strategy and risk mitigation.

A concise, visually segmented Mirum PESTLE summary that highlights external risks and strategic opportunities for quick inclusion in presentations or planning sessions; editable notes let teams tailor insights to region or business line.

Economic factors

Capital market conditions

Biotech financing cycles dictate R&D pace and runway, with global life‑sciences VC recovering to roughly $31B in 2024 versus 2021 peaks, lengthening some programs but keeping burn discipline. Tight IPO/SPAC windows push Mirum toward partnerships or debt financing. Higher rates — Fed target ~5.25–5.50% in 2024–mid‑2025 — raise discount rates and compress valuations. Bull market windows enable label expansions and lifecycle investments.

Reimbursement dynamics

Payer mix and HTA outcomes plus formularies dictate realized price, with the three largest PBMs controlling roughly 70% of US lives, concentrating negotiating power. Premium therapies increasingly face outcomes-based contracts as payers demand real-world value; relatively few contracts have broad use. Coverage decision delays commonly extend time-to-revenue by about 12 months, while robust health-economic dossiers materially improve uptake.

Rare disease pricing elasticity

Ultra-rare therapies command premium pricing—examples include Zolgensma at about $2.1m and Luxturna near $850k—yet face intense payer and HTA scrutiny. Small patient volumes mean a handful of accounts can drive large revenue swings, amplifying volatility. Adherence and hub programs materially affect net revenue through persistence and wastage reduction. EU external reference pricing causes regional price cuts to ripple across linked markets.

M&A and partnerships

Strategic alliances let Mirum share development risk and broaden geographic reach, a trend reinforced by big pharma consolidation such as Pfizer’s $43B acquisition of Seagen in 2023; BD deals supply non-dilutive capital and pipeline breadth, while acquisitive moves can rapidly reset competitive landscapes. Valuation multiples hinge on proof-of-concept and de-risked assets.

- Risk-sharing

- Non-dilutive BD capital

- Competitive reset (e.g., Pfizer-Seagen $43B)

- Multiples tied to PoC/de-risking

FX and inflation

Mirum's global sales expose earnings to currency swings as FX volatility (DXY moved about 6% in 2024) can compress reported revenue; inflation—US CPI ~3.4% and eurozone ~2.4% in 2024—raises COGS, trial site costs and SG&A. Hedging and long-term supplier/contract deals can stabilize margins, but Mirum's pricing power may not fully offset sharp cost surges.

- FX exposure: material for cross-border revenue

- Inflation: increases COGS, trial/site, SG&A

- Mitigants: hedging, long-term contracts

Orphan exclusivity shortens timelines; Medicare pricing and >60% API China/India

Higher rates (Fed ~5.25–5.50% in 2024–mid‑2025) and tighter biotech VC ($31B global 2024) compress valuations and push Mirum to partner/debt options; FX swings (DXY ~6% in 2024) and inflation (US CPI ~3.4%, eurozone ~2.4% in 2024) raise COGS and trial costs. PBM concentration (~70% US lives) and HTA delays extend time‑to‑revenue ~12 months; strategic BD (Pfizer‑Seagen $43B) reshapes competitiveness.

| Metric | Value |

|---|---|

| Fed rate | 5.25–5.50% |

| Life‑sciences VC 2024 | $31B |

| DXY 2024 move | ~6% |

| US CPI 2024 | 3.4% |

Full Version Awaits

Mirum PESTLE Analysis

The Mirum PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and professional structure are identical to the downloadable file, with no placeholders or teasers. After checkout you’ll instantly get this same finished report, ready for implementation.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our Mirum PESTLE Analysis—three to five sentence summary revealing how political, economic, social, technological, legal, and environmental forces shape Mirum’s trajectory. Perfect for investors and strategists, it surfaces risks, growth levers, and market signals. Purchase the full report for detailed, actionable insights and ready-to-use charts for immediate decision-making.

Political factors

Regulatory policy stability

Biopharma outcomes for Mirum hinge on FDA, EMA and other regulators’ guidance for rare liver diseases; shifts in endpoints or accelerated pathways materially affect launch timing. Consistent orphan frameworks (Orphan Drug Act 1983) offer 7 years US and 10 years EU exclusivity, de‑risking timelines. Policy volatility increases trial costs and uncertainty; FDA review goals are 6 months (priority) and 10 months (standard).

Orphan and pediatric incentives

US orphan exclusivity (7 years) and EU orphan protection (10 years), plus pediatric priority review vouchers (PRVs) and fee waivers, materially boost ROI for Mirum in cholestatic diseases. PRV sales have historically ranged up to about 350 million USD, helping offset small patient pools. Any rollback of these incentives would compress margins; stronger incentives would significantly improve pipeline economics.

Drug pricing scrutiny

National pricing reforms, notably the US Inflation Reduction Act (enacted 2022) enabling Medicare negotiation from 2026, target specialty drugs that now account for roughly 55% of US drug spend (IQVIA 2023). Reference pricing and health-technology assessments in markets like Europe cap revenue per patient through value-based ceilings. Market access increasingly requires robust randomized and real-world outcomes evidence. Political pressure is raising rebate demands and constraining list-price growth.

Public health funding priorities

Grants from NIH programs such as the Rare Diseases Clinical Research Network (RDCRN, NCATS-supported since 2003) and EU Horizon Europe (95.5 billion EUR programme 2021–27) underpin rare-disease networks; prioritizing pediatric liver conditions like biliary atresia (incidence ~1 in 10,000–15,000 births) can accelerate trial enrollment, while budget constraints risk diverting funds away from specialty trials; stable funding strengthens registries and data infrastructure.

- NIH/NCATS RDCRN

- Horizon Europe 95.5 billion EUR

- Biliary atresia ~1/10,000–15,000

- Stable funding → stronger registries

Geopolitics and supply chains

Geopolitical tensions and export controls increasingly affect APIs and key intermediates, with China and India supplying over 60% of global APIs (2023), raising exposure for Mirum; sanctions and logistics bottlenecks have delayed manufacturing by months in past shock events; localization policies in the US, EU and India are driving incentives for regional production; diversification across suppliers and sites mitigates political shocks.

- trade_tensions: export controls on APIs

- sanctions_logistics: manufacturing delays

- localization: regional production mandates

- mitigation: supply diversification

Orphan exclusivity shortens timelines; Medicare pricing and >60% API China/India

Regulatory shifts (FDA/EMA) dictate Mirum launch timing; orphan pathways (US 7y, EU 10y) de‑risk timelines. Medicare negotiation from 2026 and HTA/reference pricing compress US/EU pricing; PRVs have fetched up to 350M USD. API exposure (>60% from China/India in 2023) raises supply-chain geopolitical risk.

| Policy/Data | Figure/Impact |

|---|---|

| Orphan exclusivity | US 7y / EU 10y |

| Medicare negotiation | Effective 2026 (IRA 2022) |

| PRV value | Up to 350M USD |

| API sourcing | >60% from China/India (2023) |

What is included in the product

Explores how macro-environmental forces uniquely affect Mirum across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region- and industry-specific insights; designed for executives and investors, it’s ready for reports and includes forward-looking scenarios to inform strategy and risk mitigation.

A concise, visually segmented Mirum PESTLE summary that highlights external risks and strategic opportunities for quick inclusion in presentations or planning sessions; editable notes let teams tailor insights to region or business line.

Economic factors

Capital market conditions

Biotech financing cycles dictate R&D pace and runway, with global life‑sciences VC recovering to roughly $31B in 2024 versus 2021 peaks, lengthening some programs but keeping burn discipline. Tight IPO/SPAC windows push Mirum toward partnerships or debt financing. Higher rates — Fed target ~5.25–5.50% in 2024–mid‑2025 — raise discount rates and compress valuations. Bull market windows enable label expansions and lifecycle investments.

Reimbursement dynamics

Payer mix and HTA outcomes plus formularies dictate realized price, with the three largest PBMs controlling roughly 70% of US lives, concentrating negotiating power. Premium therapies increasingly face outcomes-based contracts as payers demand real-world value; relatively few contracts have broad use. Coverage decision delays commonly extend time-to-revenue by about 12 months, while robust health-economic dossiers materially improve uptake.

Rare disease pricing elasticity

Ultra-rare therapies command premium pricing—examples include Zolgensma at about $2.1m and Luxturna near $850k—yet face intense payer and HTA scrutiny. Small patient volumes mean a handful of accounts can drive large revenue swings, amplifying volatility. Adherence and hub programs materially affect net revenue through persistence and wastage reduction. EU external reference pricing causes regional price cuts to ripple across linked markets.

M&A and partnerships

Strategic alliances let Mirum share development risk and broaden geographic reach, a trend reinforced by big pharma consolidation such as Pfizer’s $43B acquisition of Seagen in 2023; BD deals supply non-dilutive capital and pipeline breadth, while acquisitive moves can rapidly reset competitive landscapes. Valuation multiples hinge on proof-of-concept and de-risked assets.

- Risk-sharing

- Non-dilutive BD capital

- Competitive reset (e.g., Pfizer-Seagen $43B)

- Multiples tied to PoC/de-risking

FX and inflation

Mirum's global sales expose earnings to currency swings as FX volatility (DXY moved about 6% in 2024) can compress reported revenue; inflation—US CPI ~3.4% and eurozone ~2.4% in 2024—raises COGS, trial site costs and SG&A. Hedging and long-term supplier/contract deals can stabilize margins, but Mirum's pricing power may not fully offset sharp cost surges.

- FX exposure: material for cross-border revenue

- Inflation: increases COGS, trial/site, SG&A

- Mitigants: hedging, long-term contracts

Orphan exclusivity shortens timelines; Medicare pricing and >60% API China/India

Higher rates (Fed ~5.25–5.50% in 2024–mid‑2025) and tighter biotech VC ($31B global 2024) compress valuations and push Mirum to partner/debt options; FX swings (DXY ~6% in 2024) and inflation (US CPI ~3.4%, eurozone ~2.4% in 2024) raise COGS and trial costs. PBM concentration (~70% US lives) and HTA delays extend time‑to‑revenue ~12 months; strategic BD (Pfizer‑Seagen $43B) reshapes competitiveness.

| Metric | Value |

|---|---|

| Fed rate | 5.25–5.50% |

| Life‑sciences VC 2024 | $31B |

| DXY 2024 move | ~6% |

| US CPI 2024 | 3.4% |

Full Version Awaits

Mirum PESTLE Analysis

The Mirum PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and professional structure are identical to the downloadable file, with no placeholders or teasers. After checkout you’ll instantly get this same finished report, ready for implementation.