Mitsubishi HC Capital PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE Analysis of Mitsubishi HC Capital—three to five focused insights revealing how political regulation, economic cycles, and technological change shape its prospects. Perfect for investors and strategists, this briefing highlights risks and opportunities you can act on immediately. Purchase the full analysis for a complete, downloadable toolkit to inform your next decision.

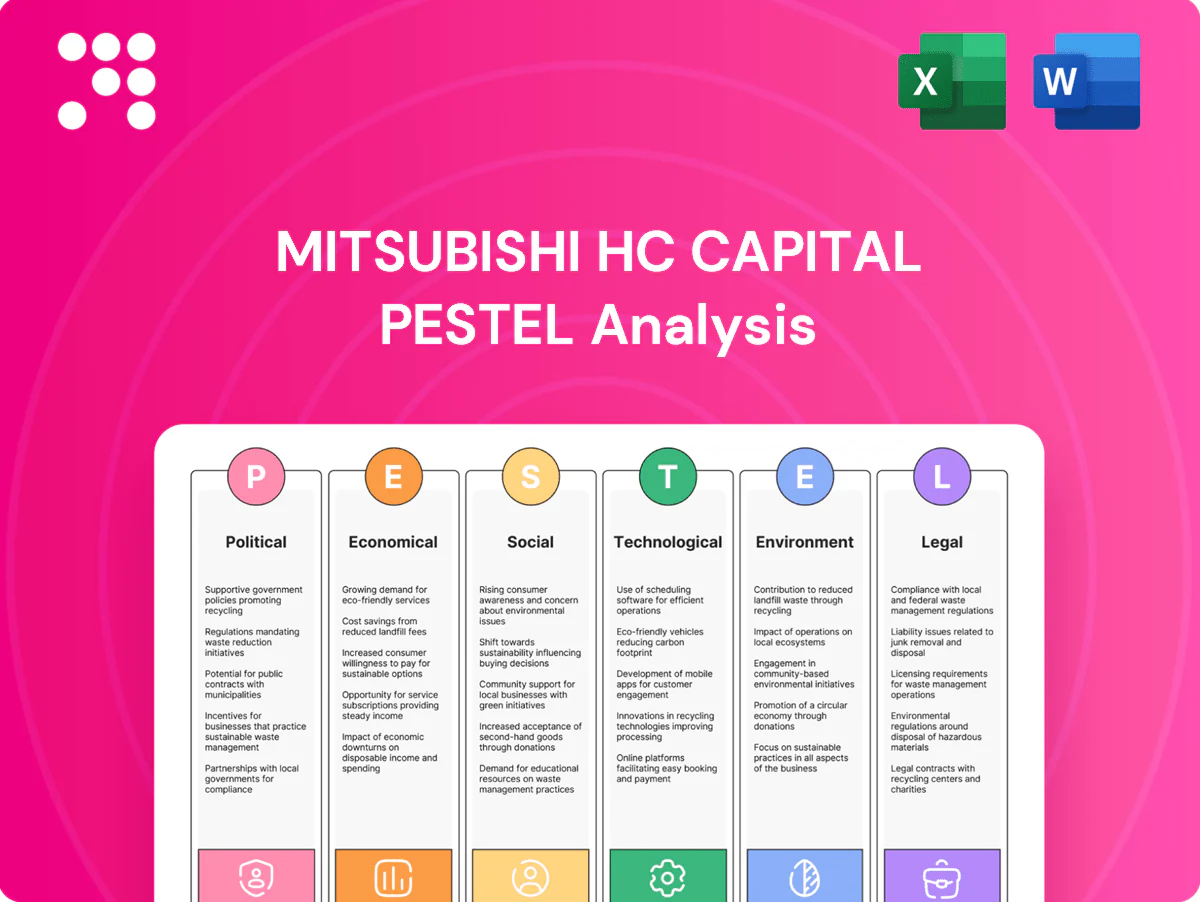

Political factors

Energy transition policies and subsidies

Japan's 2030 target of 36–38% renewables and global EVs at about 14% of new car sales in 2023 show policy-driven demand; expanding incentives for renewables, EVs and storage are creating leasing and project‑finance opportunities for Mitsubishi HC Capital across energy and environment. Continuity of budgets and subsidy rules determines pipeline visibility, and abrupt subsidy resets can compress asset values and utilization rates.

Healthcare and mobility public spending

Government budgets for healthcare infrastructure and public transport directly shape demand for equipment leasing and mobility solutions; Japan spent 11.2% of GDP on health (OECD, 2022), sustaining capex needs. Aging societies—29.1% aged 65+ in 2023 (Statistics Bureau of Japan)—drive sustained medical investments, stabilizing cash flows. Urban mobility programs accelerate fleet electrification while procurement rules and tender cycles constrain pricing power.

Geopolitical risk and supply chain realignment

US‑China tensions and reshoring policies—highlighted by the US CHIPS and Science Act (about USD 52 billion for domestic semiconductor incentives)—are shifting capex toward Japan and ASEAN, driving demand for equipment and facility financing. Expanded export controls on advanced chips since 2022–24 increase compliance and counterparty risk for lessors. Supplier diversification reduces used-equipment prices and complicates repossession logistics, raising residual-value uncertainty for financiers.

Monetary and fiscal policy coordination

Monetary and fiscal policy divergence—US Fed funds at 5.25–5.50% (2024–25), ECB deposit near 4.0%, and Japan policy rates around 0–0.1%—shapes credit spreads and asset valuations; prolonged Japanese accommodation supports leasing volumes, while tightening in US/EU raises default pressure on weaker lessees. Japan’s FY2024 budget near ¥114 trillion and infrastructure stimulus expands PPP financing, but policy reversals can force repricing of long-duration contracts.

- Policy divergence: Fed 5.25–5.50%

- ECB ≈4.0%

- BOJ ≈0–0.1%

- Japan FY2024 budget ≈¥114T (infrastructure → PPP)

- Tightening → stress on weaker borrowers; reversals → contract repricing

Local regulatory fragmentation

Local regulatory fragmentation across Japans 47 prefectures and roughly 1,718 municipalities shapes real estate, renewable siting and mobility operations for Mitsubishi HC Capital; prefectural and municipal permit processes frequently add complexity that can delay project deployment and revenue recognition. Local incentives, when stacked with national subsidies, can materially improve project IRR, and proactive stakeholder engagement reduces political and community opposition risk.

- 47 prefectures

- ~1,718 municipalities

- Permitting-driven deployment risk

- Stackable local+national incentives boost IRR

- Stakeholder engagement mitigates opposition

Japan's renewables push, aging society and policy split heighten financing and deployment risks

Policy-driven renewable/EV targets (Japan 36–38% renewables 2030; global EVs ~14% new car sales 2023) and aging population (29.1% 65+ in 2023) sustain leasing demand; fiscal/monetary divergence (Fed 5.25–5.50% 2024–25; BOJ ~0–0.1%) and Japan FY2024 budget ≈¥114T shape financing costs and PPP pipelines; US CHIPS ~USD52bn and local permit fragmentation (47 prefectures, ~1,718 municipalities) raise compliance and deployment risk.

| Indicator | Value | Implication |

|---|---|---|

| Japan renewables target | 36–38% (2030) | Project finance demand |

| 65+ population | 29.1% (2023) | Healthcare capex |

| Fed rate | 5.25–5.50% (2024–25) | Credit spreads |

What is included in the product

Explores how macro-environmental factors uniquely affect Mitsubishi HC Capital across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry-specific examples. Designed to support executives and investors with forward-looking insights ready for business plans and scenario planning.

A clean, summarized version of Mitsubishi HC Capital's full PESTLE analysis, visually segmented by PESTEL categories for quick interpretation at a glance; easily dropped into presentations or shared across teams for swift alignment during planning sessions.

Economic factors

Interest rate and yield curve dynamics

Rate levels directly drive lease pricing, NIM and residual-value assumptions; with U.S. fed funds at 5.25–5.50% (mid‑2025) and Japan 10y near 1.0% by H1 2025, lease yields and discount rates have risen. Curve steepening can boost carry but reduces borrower affordability and leasing demand. Japan policy normalization would reprice yen assets materially. Hedging effectiveness—1y JPY/USD basis ~1.5% (annualized) in 2024–25—is pivotal for cross‑currency portfolios.

Credit cycle and default risk

Macro slowdowns raise delinquencies in SME and consumer segments, pressuring Mitsubishi HC Capital’s leasing and loan portfolios. Diversification across industries and geographies helps buffer sector-specific shocks. Stricter underwriting standards and tighter collateral controls have been implemented to preserve asset quality. Recovery rates depend heavily on the secondary market depth for repossessed leased assets.

FX volatility and cross-border exposure

Yen traded near 150 per USD in 2024, so yen weakness inflates yen-denominated translation of overseas income while raising unhedged dollar funding costs. Currency swings erode customer affordability for imported equipment, pressuring volume. Robust hedging and local-currency financing reduce P&L noise, since translation effects can otherwise distort reported growth.

Capex trends in target industries

Healthcare, logistics, data centers and renewables show resilient capex with high-single-digit growth in many markets; renewables attracted about 1.7 trillion USD in clean-energy investment in 2023 (IEA). Real estate cycles and rising construction costs compress timelines and increase financing needs. EV and battery value chains continue to draw incremental financing while cyclical sectors demand dynamic pricing and utilization strategies.

- Healthcare: stable, defensive capex

- Logistics: e-commerce-driven expansion

- Data centers: concentrated hyperscaler spending

- Renewables: $1.7T clean-energy investment (2023)

- EV/Battery: rising financing demand

Inflation and asset replacement costs

Input inflation raises equipment prices and lease rates; Japan CPI rose about 3.2% in 2024, lifting replacement costs and pushing Mitsubishi HC Capital to reprice new leases. Higher asset values can improve residuals but heighten customer credit strain and default risk. Index-linked contracts and CPI clauses help preserve margins. Supply constraints have extended lease terms and increased fleet utilization.

- Input inflation: Japan CPI ~3.2% (2024)

- Higher replacement costs → higher lease rates

- Residuals up but credit stress rises

- Index-linked contracts protect margins

- Supply constraints lengthen terms, boost utilization

Japan's renewables push, aging society and policy split heighten financing and deployment risks

Rising global rates (Fed 5.25–5.50% mid‑2025; Japan 10y ~1.0% H1‑2025) lift lease yields but cut demand; JPY ~150 (2024) and hedging costs (1y JPY/USD basis ~1.5% in 2024–25) drive P&L volatility. Macro slowdown elevates SME/consumer delinquencies; diversification and tighter underwriting protect asset quality. Input inflation (Japan CPI ~3.2% 2024) raises replacement costs and lease repricing.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Japan 10y (H1‑2025) | ~1.0% |

| JPY vs USD (2024) | ~150 |

| Japan CPI (2024) | ~3.2% |

| Clean‑energy investment (2023) | $1.7T |

Full Version Awaits

Mitsubishi HC Capital PESTLE Analysis

The Mitsubishi HC Capital PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file contains the complete PESTLE assessment, insights, and supporting details as displayed. No placeholders or teasers—what you see is what you’ll download immediately after payment.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE Analysis of Mitsubishi HC Capital—three to five focused insights revealing how political regulation, economic cycles, and technological change shape its prospects. Perfect for investors and strategists, this briefing highlights risks and opportunities you can act on immediately. Purchase the full analysis for a complete, downloadable toolkit to inform your next decision.

Political factors

Energy transition policies and subsidies

Japan's 2030 target of 36–38% renewables and global EVs at about 14% of new car sales in 2023 show policy-driven demand; expanding incentives for renewables, EVs and storage are creating leasing and project‑finance opportunities for Mitsubishi HC Capital across energy and environment. Continuity of budgets and subsidy rules determines pipeline visibility, and abrupt subsidy resets can compress asset values and utilization rates.

Healthcare and mobility public spending

Government budgets for healthcare infrastructure and public transport directly shape demand for equipment leasing and mobility solutions; Japan spent 11.2% of GDP on health (OECD, 2022), sustaining capex needs. Aging societies—29.1% aged 65+ in 2023 (Statistics Bureau of Japan)—drive sustained medical investments, stabilizing cash flows. Urban mobility programs accelerate fleet electrification while procurement rules and tender cycles constrain pricing power.

Geopolitical risk and supply chain realignment

US‑China tensions and reshoring policies—highlighted by the US CHIPS and Science Act (about USD 52 billion for domestic semiconductor incentives)—are shifting capex toward Japan and ASEAN, driving demand for equipment and facility financing. Expanded export controls on advanced chips since 2022–24 increase compliance and counterparty risk for lessors. Supplier diversification reduces used-equipment prices and complicates repossession logistics, raising residual-value uncertainty for financiers.

Monetary and fiscal policy coordination

Monetary and fiscal policy divergence—US Fed funds at 5.25–5.50% (2024–25), ECB deposit near 4.0%, and Japan policy rates around 0–0.1%—shapes credit spreads and asset valuations; prolonged Japanese accommodation supports leasing volumes, while tightening in US/EU raises default pressure on weaker lessees. Japan’s FY2024 budget near ¥114 trillion and infrastructure stimulus expands PPP financing, but policy reversals can force repricing of long-duration contracts.

- Policy divergence: Fed 5.25–5.50%

- ECB ≈4.0%

- BOJ ≈0–0.1%

- Japan FY2024 budget ≈¥114T (infrastructure → PPP)

- Tightening → stress on weaker borrowers; reversals → contract repricing

Local regulatory fragmentation

Local regulatory fragmentation across Japans 47 prefectures and roughly 1,718 municipalities shapes real estate, renewable siting and mobility operations for Mitsubishi HC Capital; prefectural and municipal permit processes frequently add complexity that can delay project deployment and revenue recognition. Local incentives, when stacked with national subsidies, can materially improve project IRR, and proactive stakeholder engagement reduces political and community opposition risk.

- 47 prefectures

- ~1,718 municipalities

- Permitting-driven deployment risk

- Stackable local+national incentives boost IRR

- Stakeholder engagement mitigates opposition

Japan's renewables push, aging society and policy split heighten financing and deployment risks

Policy-driven renewable/EV targets (Japan 36–38% renewables 2030; global EVs ~14% new car sales 2023) and aging population (29.1% 65+ in 2023) sustain leasing demand; fiscal/monetary divergence (Fed 5.25–5.50% 2024–25; BOJ ~0–0.1%) and Japan FY2024 budget ≈¥114T shape financing costs and PPP pipelines; US CHIPS ~USD52bn and local permit fragmentation (47 prefectures, ~1,718 municipalities) raise compliance and deployment risk.

| Indicator | Value | Implication |

|---|---|---|

| Japan renewables target | 36–38% (2030) | Project finance demand |

| 65+ population | 29.1% (2023) | Healthcare capex |

| Fed rate | 5.25–5.50% (2024–25) | Credit spreads |

What is included in the product

Explores how macro-environmental factors uniquely affect Mitsubishi HC Capital across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry-specific examples. Designed to support executives and investors with forward-looking insights ready for business plans and scenario planning.

A clean, summarized version of Mitsubishi HC Capital's full PESTLE analysis, visually segmented by PESTEL categories for quick interpretation at a glance; easily dropped into presentations or shared across teams for swift alignment during planning sessions.

Economic factors

Interest rate and yield curve dynamics

Rate levels directly drive lease pricing, NIM and residual-value assumptions; with U.S. fed funds at 5.25–5.50% (mid‑2025) and Japan 10y near 1.0% by H1 2025, lease yields and discount rates have risen. Curve steepening can boost carry but reduces borrower affordability and leasing demand. Japan policy normalization would reprice yen assets materially. Hedging effectiveness—1y JPY/USD basis ~1.5% (annualized) in 2024–25—is pivotal for cross‑currency portfolios.

Credit cycle and default risk

Macro slowdowns raise delinquencies in SME and consumer segments, pressuring Mitsubishi HC Capital’s leasing and loan portfolios. Diversification across industries and geographies helps buffer sector-specific shocks. Stricter underwriting standards and tighter collateral controls have been implemented to preserve asset quality. Recovery rates depend heavily on the secondary market depth for repossessed leased assets.

FX volatility and cross-border exposure

Yen traded near 150 per USD in 2024, so yen weakness inflates yen-denominated translation of overseas income while raising unhedged dollar funding costs. Currency swings erode customer affordability for imported equipment, pressuring volume. Robust hedging and local-currency financing reduce P&L noise, since translation effects can otherwise distort reported growth.

Capex trends in target industries

Healthcare, logistics, data centers and renewables show resilient capex with high-single-digit growth in many markets; renewables attracted about 1.7 trillion USD in clean-energy investment in 2023 (IEA). Real estate cycles and rising construction costs compress timelines and increase financing needs. EV and battery value chains continue to draw incremental financing while cyclical sectors demand dynamic pricing and utilization strategies.

- Healthcare: stable, defensive capex

- Logistics: e-commerce-driven expansion

- Data centers: concentrated hyperscaler spending

- Renewables: $1.7T clean-energy investment (2023)

- EV/Battery: rising financing demand

Inflation and asset replacement costs

Input inflation raises equipment prices and lease rates; Japan CPI rose about 3.2% in 2024, lifting replacement costs and pushing Mitsubishi HC Capital to reprice new leases. Higher asset values can improve residuals but heighten customer credit strain and default risk. Index-linked contracts and CPI clauses help preserve margins. Supply constraints have extended lease terms and increased fleet utilization.

- Input inflation: Japan CPI ~3.2% (2024)

- Higher replacement costs → higher lease rates

- Residuals up but credit stress rises

- Index-linked contracts protect margins

- Supply constraints lengthen terms, boost utilization

Japan's renewables push, aging society and policy split heighten financing and deployment risks

Rising global rates (Fed 5.25–5.50% mid‑2025; Japan 10y ~1.0% H1‑2025) lift lease yields but cut demand; JPY ~150 (2024) and hedging costs (1y JPY/USD basis ~1.5% in 2024–25) drive P&L volatility. Macro slowdown elevates SME/consumer delinquencies; diversification and tighter underwriting protect asset quality. Input inflation (Japan CPI ~3.2% 2024) raises replacement costs and lease repricing.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Japan 10y (H1‑2025) | ~1.0% |

| JPY vs USD (2024) | ~150 |

| Japan CPI (2024) | ~3.2% |

| Clean‑energy investment (2023) | $1.7T |

Full Version Awaits

Mitsubishi HC Capital PESTLE Analysis

The Mitsubishi HC Capital PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file contains the complete PESTLE assessment, insights, and supporting details as displayed. No placeholders or teasers—what you see is what you’ll download immediately after payment.

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE Analysis of Mitsubishi HC Capital—three to five focused insights revealing how political regulation, economic cycles, and technological change shape its prospects. Perfect for investors and strategists, this briefing highlights risks and opportunities you can act on immediately. Purchase the full analysis for a complete, downloadable toolkit to inform your next decision.

Political factors

Energy transition policies and subsidies

Japan's 2030 target of 36–38% renewables and global EVs at about 14% of new car sales in 2023 show policy-driven demand; expanding incentives for renewables, EVs and storage are creating leasing and project‑finance opportunities for Mitsubishi HC Capital across energy and environment. Continuity of budgets and subsidy rules determines pipeline visibility, and abrupt subsidy resets can compress asset values and utilization rates.

Healthcare and mobility public spending

Government budgets for healthcare infrastructure and public transport directly shape demand for equipment leasing and mobility solutions; Japan spent 11.2% of GDP on health (OECD, 2022), sustaining capex needs. Aging societies—29.1% aged 65+ in 2023 (Statistics Bureau of Japan)—drive sustained medical investments, stabilizing cash flows. Urban mobility programs accelerate fleet electrification while procurement rules and tender cycles constrain pricing power.

Geopolitical risk and supply chain realignment

US‑China tensions and reshoring policies—highlighted by the US CHIPS and Science Act (about USD 52 billion for domestic semiconductor incentives)—are shifting capex toward Japan and ASEAN, driving demand for equipment and facility financing. Expanded export controls on advanced chips since 2022–24 increase compliance and counterparty risk for lessors. Supplier diversification reduces used-equipment prices and complicates repossession logistics, raising residual-value uncertainty for financiers.

Monetary and fiscal policy coordination

Monetary and fiscal policy divergence—US Fed funds at 5.25–5.50% (2024–25), ECB deposit near 4.0%, and Japan policy rates around 0–0.1%—shapes credit spreads and asset valuations; prolonged Japanese accommodation supports leasing volumes, while tightening in US/EU raises default pressure on weaker lessees. Japan’s FY2024 budget near ¥114 trillion and infrastructure stimulus expands PPP financing, but policy reversals can force repricing of long-duration contracts.

- Policy divergence: Fed 5.25–5.50%

- ECB ≈4.0%

- BOJ ≈0–0.1%

- Japan FY2024 budget ≈¥114T (infrastructure → PPP)

- Tightening → stress on weaker borrowers; reversals → contract repricing

Local regulatory fragmentation

Local regulatory fragmentation across Japans 47 prefectures and roughly 1,718 municipalities shapes real estate, renewable siting and mobility operations for Mitsubishi HC Capital; prefectural and municipal permit processes frequently add complexity that can delay project deployment and revenue recognition. Local incentives, when stacked with national subsidies, can materially improve project IRR, and proactive stakeholder engagement reduces political and community opposition risk.

- 47 prefectures

- ~1,718 municipalities

- Permitting-driven deployment risk

- Stackable local+national incentives boost IRR

- Stakeholder engagement mitigates opposition

Japan's renewables push, aging society and policy split heighten financing and deployment risks

Policy-driven renewable/EV targets (Japan 36–38% renewables 2030; global EVs ~14% new car sales 2023) and aging population (29.1% 65+ in 2023) sustain leasing demand; fiscal/monetary divergence (Fed 5.25–5.50% 2024–25; BOJ ~0–0.1%) and Japan FY2024 budget ≈¥114T shape financing costs and PPP pipelines; US CHIPS ~USD52bn and local permit fragmentation (47 prefectures, ~1,718 municipalities) raise compliance and deployment risk.

| Indicator | Value | Implication |

|---|---|---|

| Japan renewables target | 36–38% (2030) | Project finance demand |

| 65+ population | 29.1% (2023) | Healthcare capex |

| Fed rate | 5.25–5.50% (2024–25) | Credit spreads |

What is included in the product

Explores how macro-environmental factors uniquely affect Mitsubishi HC Capital across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and industry-specific examples. Designed to support executives and investors with forward-looking insights ready for business plans and scenario planning.

A clean, summarized version of Mitsubishi HC Capital's full PESTLE analysis, visually segmented by PESTEL categories for quick interpretation at a glance; easily dropped into presentations or shared across teams for swift alignment during planning sessions.

Economic factors

Interest rate and yield curve dynamics

Rate levels directly drive lease pricing, NIM and residual-value assumptions; with U.S. fed funds at 5.25–5.50% (mid‑2025) and Japan 10y near 1.0% by H1 2025, lease yields and discount rates have risen. Curve steepening can boost carry but reduces borrower affordability and leasing demand. Japan policy normalization would reprice yen assets materially. Hedging effectiveness—1y JPY/USD basis ~1.5% (annualized) in 2024–25—is pivotal for cross‑currency portfolios.

Credit cycle and default risk

Macro slowdowns raise delinquencies in SME and consumer segments, pressuring Mitsubishi HC Capital’s leasing and loan portfolios. Diversification across industries and geographies helps buffer sector-specific shocks. Stricter underwriting standards and tighter collateral controls have been implemented to preserve asset quality. Recovery rates depend heavily on the secondary market depth for repossessed leased assets.

FX volatility and cross-border exposure

Yen traded near 150 per USD in 2024, so yen weakness inflates yen-denominated translation of overseas income while raising unhedged dollar funding costs. Currency swings erode customer affordability for imported equipment, pressuring volume. Robust hedging and local-currency financing reduce P&L noise, since translation effects can otherwise distort reported growth.

Capex trends in target industries

Healthcare, logistics, data centers and renewables show resilient capex with high-single-digit growth in many markets; renewables attracted about 1.7 trillion USD in clean-energy investment in 2023 (IEA). Real estate cycles and rising construction costs compress timelines and increase financing needs. EV and battery value chains continue to draw incremental financing while cyclical sectors demand dynamic pricing and utilization strategies.

- Healthcare: stable, defensive capex

- Logistics: e-commerce-driven expansion

- Data centers: concentrated hyperscaler spending

- Renewables: $1.7T clean-energy investment (2023)

- EV/Battery: rising financing demand

Inflation and asset replacement costs

Input inflation raises equipment prices and lease rates; Japan CPI rose about 3.2% in 2024, lifting replacement costs and pushing Mitsubishi HC Capital to reprice new leases. Higher asset values can improve residuals but heighten customer credit strain and default risk. Index-linked contracts and CPI clauses help preserve margins. Supply constraints have extended lease terms and increased fleet utilization.

- Input inflation: Japan CPI ~3.2% (2024)

- Higher replacement costs → higher lease rates

- Residuals up but credit stress rises

- Index-linked contracts protect margins

- Supply constraints lengthen terms, boost utilization

Japan's renewables push, aging society and policy split heighten financing and deployment risks

Rising global rates (Fed 5.25–5.50% mid‑2025; Japan 10y ~1.0% H1‑2025) lift lease yields but cut demand; JPY ~150 (2024) and hedging costs (1y JPY/USD basis ~1.5% in 2024–25) drive P&L volatility. Macro slowdown elevates SME/consumer delinquencies; diversification and tighter underwriting protect asset quality. Input inflation (Japan CPI ~3.2% 2024) raises replacement costs and lease repricing.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Japan 10y (H1‑2025) | ~1.0% |

| JPY vs USD (2024) | ~150 |

| Japan CPI (2024) | ~3.2% |

| Clean‑energy investment (2023) | $1.7T |

Full Version Awaits

Mitsubishi HC Capital PESTLE Analysis

The Mitsubishi HC Capital PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This file contains the complete PESTLE assessment, insights, and supporting details as displayed. No placeholders or teasers—what you see is what you’ll download immediately after payment.