Mitsubishi Steel Mfg Porter's Five Forces Analysis

Don't Miss the Bigger Picture

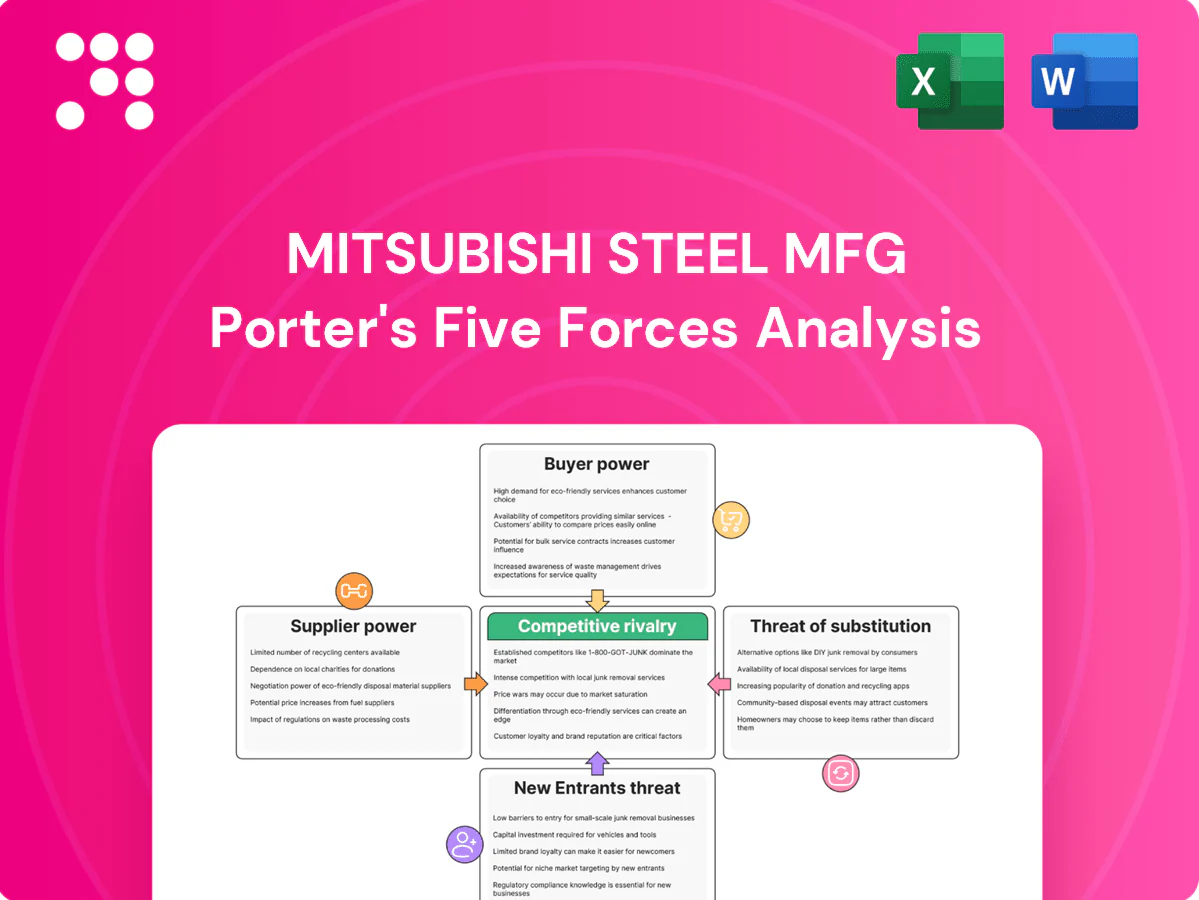

Mitsubishi Steel Mfg faces intense supplier and buyer pressures, moderate threat from substitutes, high rivalry, and barriers that shape its margin outlook. This snapshot highlights strategic choke points and growth levers for suppliers, OEMs, and investors. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for investment or strategy.

Suppliers Bargaining Power

Concentrated raw material sources

High-performance steels depend on iron ore, coking coal and alloyers supplied by a few global miners: Vale, BHP and Rio Tinto account for roughly 70% of seaborne iron ore, while Australia supplies ~60% of metallurgical coal exports; such concentration raises supplier leverage on price and allocation, long-term contracts/hedges reduce but do not remove volatility, and disruptions in mining regions or logistics can quickly tighten inputs and lift costs.

Volatile energy and industrial gases

Steelmaking energy intensity for electric-arc furnaces is about 400–600 kWh/ton, making electricity, natural gas and oxygen/argon critical inputs; energy can account for roughly 10–25% of conversion costs. Volatile energy prices in Japan—after 2022 shocks—continue to pressure margins and conversion-cost stability in 2024. Regionally dominant utilities and gas suppliers (top providers often >70% market share locally) can pass costs through, while efficiency upgrades and off-peak shifting reduce exposure but require significant capital investment.

Specialty alloys and scrap market tightness

Premium alloying elements and high-grade scrap experienced episodic shortages in 2024, pushing alloy premiums roughly 20% higher during aerospace and EV demand spikes and squeezing Mitsubishi Steel Mfg margins. Diversified sourcing and larger inventory buffers mitigate disruption but raised working capital needs and inventory carrying costs. Qualifying alternative suppliers remains slow and costly due to stringent aerospace-grade quality requirements.

FX exposure on imports

Mitsubishi Steel imports a portion of alloying inputs and coking coal, exposing procurement to yen fluctuations. The yen weakened to about 155 JPY per USD in 2024, raising USD-priced input costs and strengthening supplier bargaining power. Currency hedges can reduce volatility but add hedging costs and operational complexity. Pass-through to customers often lags, squeezing near-term margins.

- FX rate: ~155 JPY/USD (2024)

- Hedging reduces volatility but increases cost

- Lagged pass-through can compress margins

Equipment and consumables dependency

Maintenance parts, refractories and tooling for Mitsubishi Steel Mfg are sourced from specialized vendors, giving those suppliers elevated bargaining power, especially during unplanned outages or rebuilds when downtime risk sharply increases and lead times tighten. Multi-sourcing and robust preventive maintenance programs reduce but do not eliminate dependence; OEM service contracts, while often costly, remain critical to restore uptime quickly.

- Specialized vendors drive supply leverage

- Outages amplify supplier bargaining

- Multi-sourcing and PM mitigate risk

- OEM contracts pricey but key for uptime

Supplier dominance and rising costs squeeze margins: ~70% / +20% / ~155

Supplier concentration (Vale/BHP/Rio ~70% seaborne iron ore; Australia ~60% met coal) and specialized inputs give suppliers strong leverage; energy (10–25% of conversion costs) and alloy premiums (~+20% in 2024) further tighten margins. Yen ~155 JPY/USD in 2024 raises dollar-priced input costs; hedges mitigate but add cost. Multi-sourcing and inventories reduce risk but raise working capital.

| Metric | 2024 |

|---|---|

| Seaborne iron ore share (top3) | ~70% |

| Australia met coal export share | ~60% |

| Energy % of conversion cost | 10–25% |

| Alloy premium spike | ~+20% |

| JPY/USD | ~155 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Mitsubishi Steel Mfg, evaluating supplier and buyer power, substitutes, rivalry, and barriers protecting incumbents.

A concise one-sheet Porter's Five Forces for Mitsubishi Steel Mfg that highlights supplier power, buyer leverage, rivalry, and threats of entry/substitutes—ideal for fast strategic decisions. Editable radar chart and clean layout let you model scenarios, swap in current data, and drop it straight into decks.

Customers Bargaining Power

Automotive OEM and Tier‑1 dominance

Automakers and Tier‑1s are Mitsubishi Steel Mfg's primary customers, with the top 10 OEMs representing roughly 60% of global vehicle output and exercising strong procurement leverage. Their scale enforces aggressive price, delivery and warranty terms and routine annual cost‑downs of about 1–3%. Losing a platform can cut volumes and plant utilization by an estimated 10–30%, materially affecting margins and free cash flow.

High qualification and switching costs

Critical components for Mitsubishi Steel require stringent PPAP/APQP certification, with qualification cycles typically taking 6–18 months, creating substantial switching frictions that moderate buyer power after award. Buyers nonetheless commonly dual-source—industry estimates around 50–60% of contracts—to retain leverage. Performance failures can trigger rapid share loss and penalties often reaching single-digit percentages of order value or OEM chargebacks.

Custom specs and JIT delivery

Customers demand tight tolerances, metallurgy design and JIT logistics, increasing Mitsubishi Steel’s embedment but raising service burdens and operational complexity. Penalties for delivery or quality misses commonly range 0.5–3% of order value, strengthening buyer negotiating stance. Customized work reduces buyer switching but heightens cost exposure, with value-added engineering support able to justify premium pricing of roughly 5–15% in 2024 contracts.

Cyclical demand and scheduling flexibility

Cyclical swings in automotive and machinery demand drive volatile order patterns and inventory; global light-vehicle production rebounded to about 82 million units in 2024, amplifying upcycle reservation requests while downcycles push buyers for price concessions and shorter lead times.

- Buyers: push capacity reservations in upcycles

- Downcycles: demand price concessions, cut orders

- Suppliers: need flexible production and backlog control

- Risk: uneven customer forecasts shift variability to suppliers

Global benchmarking and import options

Buyers benchmark Mitsubishi Steel prices across Japan, Korea, China and Europe, with import penetration for commoditized grades exceeding 20% in some East Asian markets in 2024, increasing alternatives and price sensitivity; trade policy shifts and logistics costs intermittently reduce this leverage. Differentiated metallurgical performance and proprietary grades constrain direct comparability and preserve premium pricing.

Top‑10 OEMs ≈60% share; cost‑downs 1–3%

Automakers/Tier‑1s (top‑10 ≈60% global output) exert strong price/delivery leverage, driving annual cost‑downs ~1–3% and platform losses cutting volumes 10–30%. Qualification cycles 6–18 months and dual‑sourcing (~50–60%) moderate but do not eliminate buyer power; penalties 0.5–3% and chargebacks common. Commodity import penetration >20% (2024) raises price sensitivity; differentiated grades support 5–15% premium.

| Metric | Value |

|---|---|

| Top‑10 OEM share | ≈60% |

| Annual cost‑downs | 1–3% |

| Dual‑sourcing | 50–60% |

| Platform loss impact | 10–30% |

| Penalties | 0.5–3% |

| Premium pricing | 5–15% |

| LV production (2024) | ≈82M |

| Import penetration (commodity) | >20% |

What You See Is What You Get

Mitsubishi Steel Mfg Porter's Five Forces Analysis

This preview shows the exact Mitsubishi Steel Mfg Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The full, professionally formatted document is ready for download and use the moment you buy. You're viewing the final deliverable in its entirety.

Don't Miss the Bigger Picture

Mitsubishi Steel Mfg faces intense supplier and buyer pressures, moderate threat from substitutes, high rivalry, and barriers that shape its margin outlook. This snapshot highlights strategic choke points and growth levers for suppliers, OEMs, and investors. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for investment or strategy.

Suppliers Bargaining Power

Concentrated raw material sources

High-performance steels depend on iron ore, coking coal and alloyers supplied by a few global miners: Vale, BHP and Rio Tinto account for roughly 70% of seaborne iron ore, while Australia supplies ~60% of metallurgical coal exports; such concentration raises supplier leverage on price and allocation, long-term contracts/hedges reduce but do not remove volatility, and disruptions in mining regions or logistics can quickly tighten inputs and lift costs.

Volatile energy and industrial gases

Steelmaking energy intensity for electric-arc furnaces is about 400–600 kWh/ton, making electricity, natural gas and oxygen/argon critical inputs; energy can account for roughly 10–25% of conversion costs. Volatile energy prices in Japan—after 2022 shocks—continue to pressure margins and conversion-cost stability in 2024. Regionally dominant utilities and gas suppliers (top providers often >70% market share locally) can pass costs through, while efficiency upgrades and off-peak shifting reduce exposure but require significant capital investment.

Specialty alloys and scrap market tightness

Premium alloying elements and high-grade scrap experienced episodic shortages in 2024, pushing alloy premiums roughly 20% higher during aerospace and EV demand spikes and squeezing Mitsubishi Steel Mfg margins. Diversified sourcing and larger inventory buffers mitigate disruption but raised working capital needs and inventory carrying costs. Qualifying alternative suppliers remains slow and costly due to stringent aerospace-grade quality requirements.

FX exposure on imports

Mitsubishi Steel imports a portion of alloying inputs and coking coal, exposing procurement to yen fluctuations. The yen weakened to about 155 JPY per USD in 2024, raising USD-priced input costs and strengthening supplier bargaining power. Currency hedges can reduce volatility but add hedging costs and operational complexity. Pass-through to customers often lags, squeezing near-term margins.

- FX rate: ~155 JPY/USD (2024)

- Hedging reduces volatility but increases cost

- Lagged pass-through can compress margins

Equipment and consumables dependency

Maintenance parts, refractories and tooling for Mitsubishi Steel Mfg are sourced from specialized vendors, giving those suppliers elevated bargaining power, especially during unplanned outages or rebuilds when downtime risk sharply increases and lead times tighten. Multi-sourcing and robust preventive maintenance programs reduce but do not eliminate dependence; OEM service contracts, while often costly, remain critical to restore uptime quickly.

- Specialized vendors drive supply leverage

- Outages amplify supplier bargaining

- Multi-sourcing and PM mitigate risk

- OEM contracts pricey but key for uptime

Supplier dominance and rising costs squeeze margins: ~70% / +20% / ~155

Supplier concentration (Vale/BHP/Rio ~70% seaborne iron ore; Australia ~60% met coal) and specialized inputs give suppliers strong leverage; energy (10–25% of conversion costs) and alloy premiums (~+20% in 2024) further tighten margins. Yen ~155 JPY/USD in 2024 raises dollar-priced input costs; hedges mitigate but add cost. Multi-sourcing and inventories reduce risk but raise working capital.

| Metric | 2024 |

|---|---|

| Seaborne iron ore share (top3) | ~70% |

| Australia met coal export share | ~60% |

| Energy % of conversion cost | 10–25% |

| Alloy premium spike | ~+20% |

| JPY/USD | ~155 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Mitsubishi Steel Mfg, evaluating supplier and buyer power, substitutes, rivalry, and barriers protecting incumbents.

A concise one-sheet Porter's Five Forces for Mitsubishi Steel Mfg that highlights supplier power, buyer leverage, rivalry, and threats of entry/substitutes—ideal for fast strategic decisions. Editable radar chart and clean layout let you model scenarios, swap in current data, and drop it straight into decks.

Customers Bargaining Power

Automotive OEM and Tier‑1 dominance

Automakers and Tier‑1s are Mitsubishi Steel Mfg's primary customers, with the top 10 OEMs representing roughly 60% of global vehicle output and exercising strong procurement leverage. Their scale enforces aggressive price, delivery and warranty terms and routine annual cost‑downs of about 1–3%. Losing a platform can cut volumes and plant utilization by an estimated 10–30%, materially affecting margins and free cash flow.

High qualification and switching costs

Critical components for Mitsubishi Steel require stringent PPAP/APQP certification, with qualification cycles typically taking 6–18 months, creating substantial switching frictions that moderate buyer power after award. Buyers nonetheless commonly dual-source—industry estimates around 50–60% of contracts—to retain leverage. Performance failures can trigger rapid share loss and penalties often reaching single-digit percentages of order value or OEM chargebacks.

Custom specs and JIT delivery

Customers demand tight tolerances, metallurgy design and JIT logistics, increasing Mitsubishi Steel’s embedment but raising service burdens and operational complexity. Penalties for delivery or quality misses commonly range 0.5–3% of order value, strengthening buyer negotiating stance. Customized work reduces buyer switching but heightens cost exposure, with value-added engineering support able to justify premium pricing of roughly 5–15% in 2024 contracts.

Cyclical demand and scheduling flexibility

Cyclical swings in automotive and machinery demand drive volatile order patterns and inventory; global light-vehicle production rebounded to about 82 million units in 2024, amplifying upcycle reservation requests while downcycles push buyers for price concessions and shorter lead times.

- Buyers: push capacity reservations in upcycles

- Downcycles: demand price concessions, cut orders

- Suppliers: need flexible production and backlog control

- Risk: uneven customer forecasts shift variability to suppliers

Global benchmarking and import options

Buyers benchmark Mitsubishi Steel prices across Japan, Korea, China and Europe, with import penetration for commoditized grades exceeding 20% in some East Asian markets in 2024, increasing alternatives and price sensitivity; trade policy shifts and logistics costs intermittently reduce this leverage. Differentiated metallurgical performance and proprietary grades constrain direct comparability and preserve premium pricing.

Top‑10 OEMs ≈60% share; cost‑downs 1–3%

Automakers/Tier‑1s (top‑10 ≈60% global output) exert strong price/delivery leverage, driving annual cost‑downs ~1–3% and platform losses cutting volumes 10–30%. Qualification cycles 6–18 months and dual‑sourcing (~50–60%) moderate but do not eliminate buyer power; penalties 0.5–3% and chargebacks common. Commodity import penetration >20% (2024) raises price sensitivity; differentiated grades support 5–15% premium.

| Metric | Value |

|---|---|

| Top‑10 OEM share | ≈60% |

| Annual cost‑downs | 1–3% |

| Dual‑sourcing | 50–60% |

| Platform loss impact | 10–30% |

| Penalties | 0.5–3% |

| Premium pricing | 5–15% |

| LV production (2024) | ≈82M |

| Import penetration (commodity) | >20% |

What You See Is What You Get

Mitsubishi Steel Mfg Porter's Five Forces Analysis

This preview shows the exact Mitsubishi Steel Mfg Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The full, professionally formatted document is ready for download and use the moment you buy. You're viewing the final deliverable in its entirety.

Description

Don't Miss the Bigger Picture

Mitsubishi Steel Mfg faces intense supplier and buyer pressures, moderate threat from substitutes, high rivalry, and barriers that shape its margin outlook. This snapshot highlights strategic choke points and growth levers for suppliers, OEMs, and investors. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for investment or strategy.

Suppliers Bargaining Power

Concentrated raw material sources

High-performance steels depend on iron ore, coking coal and alloyers supplied by a few global miners: Vale, BHP and Rio Tinto account for roughly 70% of seaborne iron ore, while Australia supplies ~60% of metallurgical coal exports; such concentration raises supplier leverage on price and allocation, long-term contracts/hedges reduce but do not remove volatility, and disruptions in mining regions or logistics can quickly tighten inputs and lift costs.

Volatile energy and industrial gases

Steelmaking energy intensity for electric-arc furnaces is about 400–600 kWh/ton, making electricity, natural gas and oxygen/argon critical inputs; energy can account for roughly 10–25% of conversion costs. Volatile energy prices in Japan—after 2022 shocks—continue to pressure margins and conversion-cost stability in 2024. Regionally dominant utilities and gas suppliers (top providers often >70% market share locally) can pass costs through, while efficiency upgrades and off-peak shifting reduce exposure but require significant capital investment.

Specialty alloys and scrap market tightness

Premium alloying elements and high-grade scrap experienced episodic shortages in 2024, pushing alloy premiums roughly 20% higher during aerospace and EV demand spikes and squeezing Mitsubishi Steel Mfg margins. Diversified sourcing and larger inventory buffers mitigate disruption but raised working capital needs and inventory carrying costs. Qualifying alternative suppliers remains slow and costly due to stringent aerospace-grade quality requirements.

FX exposure on imports

Mitsubishi Steel imports a portion of alloying inputs and coking coal, exposing procurement to yen fluctuations. The yen weakened to about 155 JPY per USD in 2024, raising USD-priced input costs and strengthening supplier bargaining power. Currency hedges can reduce volatility but add hedging costs and operational complexity. Pass-through to customers often lags, squeezing near-term margins.

- FX rate: ~155 JPY/USD (2024)

- Hedging reduces volatility but increases cost

- Lagged pass-through can compress margins

Equipment and consumables dependency

Maintenance parts, refractories and tooling for Mitsubishi Steel Mfg are sourced from specialized vendors, giving those suppliers elevated bargaining power, especially during unplanned outages or rebuilds when downtime risk sharply increases and lead times tighten. Multi-sourcing and robust preventive maintenance programs reduce but do not eliminate dependence; OEM service contracts, while often costly, remain critical to restore uptime quickly.

- Specialized vendors drive supply leverage

- Outages amplify supplier bargaining

- Multi-sourcing and PM mitigate risk

- OEM contracts pricey but key for uptime

Supplier dominance and rising costs squeeze margins: ~70% / +20% / ~155

Supplier concentration (Vale/BHP/Rio ~70% seaborne iron ore; Australia ~60% met coal) and specialized inputs give suppliers strong leverage; energy (10–25% of conversion costs) and alloy premiums (~+20% in 2024) further tighten margins. Yen ~155 JPY/USD in 2024 raises dollar-priced input costs; hedges mitigate but add cost. Multi-sourcing and inventories reduce risk but raise working capital.

| Metric | 2024 |

|---|---|

| Seaborne iron ore share (top3) | ~70% |

| Australia met coal export share | ~60% |

| Energy % of conversion cost | 10–25% |

| Alloy premium spike | ~+20% |

| JPY/USD | ~155 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Mitsubishi Steel Mfg, evaluating supplier and buyer power, substitutes, rivalry, and barriers protecting incumbents.

A concise one-sheet Porter's Five Forces for Mitsubishi Steel Mfg that highlights supplier power, buyer leverage, rivalry, and threats of entry/substitutes—ideal for fast strategic decisions. Editable radar chart and clean layout let you model scenarios, swap in current data, and drop it straight into decks.

Customers Bargaining Power

Automotive OEM and Tier‑1 dominance

Automakers and Tier‑1s are Mitsubishi Steel Mfg's primary customers, with the top 10 OEMs representing roughly 60% of global vehicle output and exercising strong procurement leverage. Their scale enforces aggressive price, delivery and warranty terms and routine annual cost‑downs of about 1–3%. Losing a platform can cut volumes and plant utilization by an estimated 10–30%, materially affecting margins and free cash flow.

High qualification and switching costs

Critical components for Mitsubishi Steel require stringent PPAP/APQP certification, with qualification cycles typically taking 6–18 months, creating substantial switching frictions that moderate buyer power after award. Buyers nonetheless commonly dual-source—industry estimates around 50–60% of contracts—to retain leverage. Performance failures can trigger rapid share loss and penalties often reaching single-digit percentages of order value or OEM chargebacks.

Custom specs and JIT delivery

Customers demand tight tolerances, metallurgy design and JIT logistics, increasing Mitsubishi Steel’s embedment but raising service burdens and operational complexity. Penalties for delivery or quality misses commonly range 0.5–3% of order value, strengthening buyer negotiating stance. Customized work reduces buyer switching but heightens cost exposure, with value-added engineering support able to justify premium pricing of roughly 5–15% in 2024 contracts.

Cyclical demand and scheduling flexibility

Cyclical swings in automotive and machinery demand drive volatile order patterns and inventory; global light-vehicle production rebounded to about 82 million units in 2024, amplifying upcycle reservation requests while downcycles push buyers for price concessions and shorter lead times.

- Buyers: push capacity reservations in upcycles

- Downcycles: demand price concessions, cut orders

- Suppliers: need flexible production and backlog control

- Risk: uneven customer forecasts shift variability to suppliers

Global benchmarking and import options

Buyers benchmark Mitsubishi Steel prices across Japan, Korea, China and Europe, with import penetration for commoditized grades exceeding 20% in some East Asian markets in 2024, increasing alternatives and price sensitivity; trade policy shifts and logistics costs intermittently reduce this leverage. Differentiated metallurgical performance and proprietary grades constrain direct comparability and preserve premium pricing.

Top‑10 OEMs ≈60% share; cost‑downs 1–3%

Automakers/Tier‑1s (top‑10 ≈60% global output) exert strong price/delivery leverage, driving annual cost‑downs ~1–3% and platform losses cutting volumes 10–30%. Qualification cycles 6–18 months and dual‑sourcing (~50–60%) moderate but do not eliminate buyer power; penalties 0.5–3% and chargebacks common. Commodity import penetration >20% (2024) raises price sensitivity; differentiated grades support 5–15% premium.

| Metric | Value |

|---|---|

| Top‑10 OEM share | ≈60% |

| Annual cost‑downs | 1–3% |

| Dual‑sourcing | 50–60% |

| Platform loss impact | 10–30% |

| Penalties | 0.5–3% |

| Premium pricing | 5–15% |

| LV production (2024) | ≈82M |

| Import penetration (commodity) | >20% |

What You See Is What You Get

Mitsubishi Steel Mfg Porter's Five Forces Analysis

This preview shows the exact Mitsubishi Steel Mfg Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The full, professionally formatted document is ready for download and use the moment you buy. You're viewing the final deliverable in its entirety.