Mizrahi Tefahot Bank Business Model Canvas

Strategic Business Model Canvas: Investor-ready roadmap of value, segments, and revenue levers

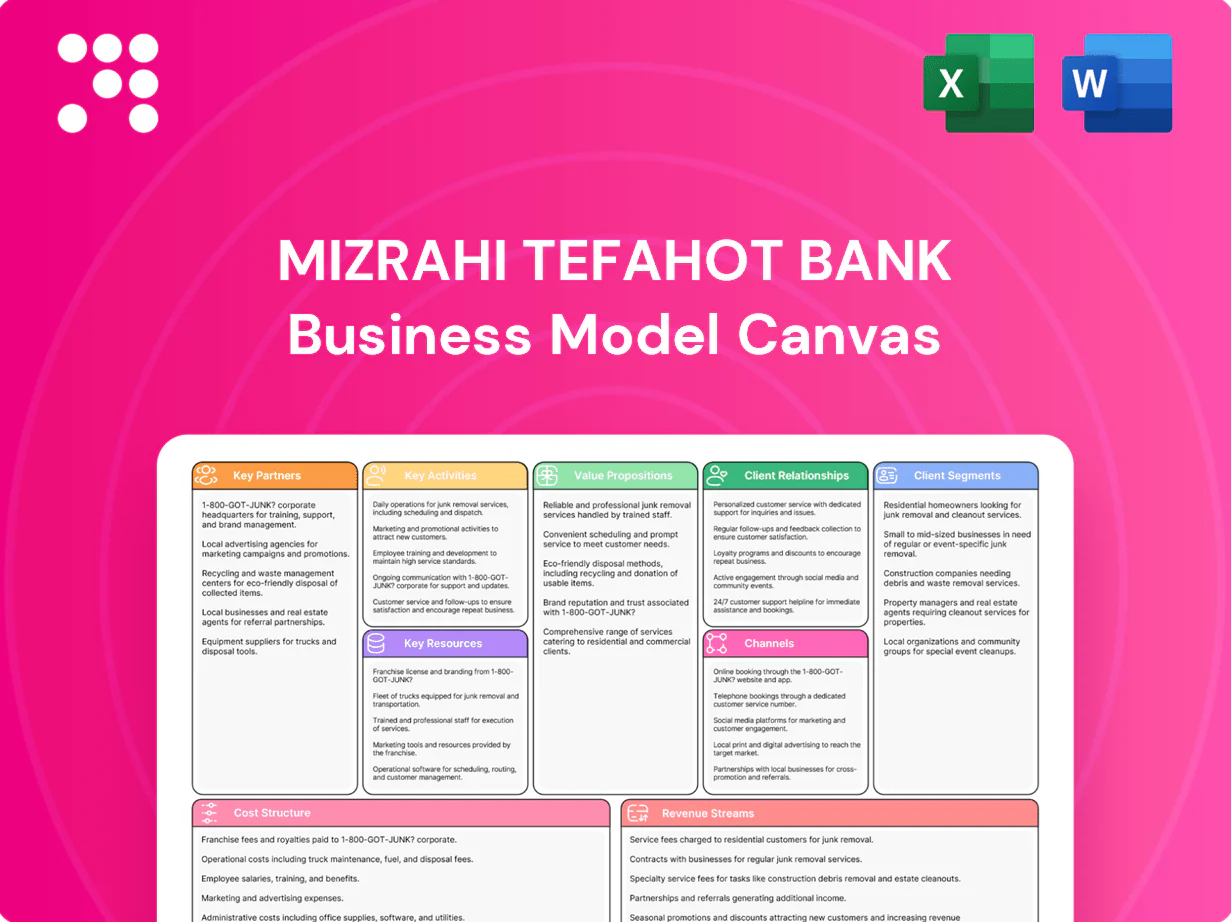

Unlock the strategic blueprint behind Mizrahi Tefahot Bank with our concise Business Model Canvas that maps value propositions, customer segments, and revenue levers. This executive-ready canvas reveals growth levers and operational efficiencies for investors and strategists. Purchase the full Word/Excel version to access company-specific insights and actionable recommendations.

Partnerships

Mortgage brokers and real estate developers

Partnering with mortgage brokers and real estate developers expands Mizrahi Tefahot’s mortgage pipeline and improves lead quality, reinforcing its position as Israel’s largest mortgage bank with roughly 30% market share in 2024.

Co-marketing and preferred-lender arrangements accelerate approvals and raise conversion rates, shortening time-to-close by industry-estimated 15–25% and lifting funded-mortgage rates.

Data-sharing on projects and buyer profiles enhances underwriting precision, reducing credit surprises and supporting the bank’s strong foothold in Israeli home financing.

Payment networks and fintech providers

Alliances with card schemes and fintechs enable Mizrahi Tefahot to deliver seamless transactions and digital wallets, supporting Israel’s shift to cashless payments in 2024. APIs and embedded banking tie the bank into merchants and apps, expanding distribution and transaction volume. Co-developing user journeys improves UX and retention, with partners reporting up to 30% faster adoption. These partnerships cut time-to-market for new services, accelerating product launches.

Institutional investors and capital markets

Tapping institutional partners supports securitizations, covered bonds and wholesale funding, enabling Mizrahi Tefahot to convert mortgage exposures into liquid instruments. Syndication relationships with banks and investors allow the bank to underwrite larger corporate and real estate transactions. Market makers and brokers improve secondary-market liquidity and pricing, collectively lowering funding costs and diversifying balance-sheet risk.

Technology vendors and cloud providers

Technology vendors for core banking, cybersecurity, analytics and cloud underpin Mizrahi Tefahot Bank’s digital transformation, enabling AI-driven underwriting, KYC/AML and CRM deployments with vendor ecosystems accelerating time-to-market.

- Cloud market share 2024: AWS ~32%, Azure ~22%, GCP ~11%

- Typical SLAs: 99.99% uptime and regulatory-grade controls

- Outcome: scalable, resilient infrastructure for growth

Regulators and industry associations

In 2024, constructive engagement with the Bank of Israel and compliance bodies sustains Mizrahi Tefahot Bank’s license integrity, reducing regulatory breach risk and operational surprises. Active participation in industry forums shapes standards for payments, open banking, and risk controls, aligning implementations ahead of enforcement. Early alignment strengthens trust with customers and investors by signaling robust governance.

- Regulator: Bank of Israel engagement

- Standards: payments and open banking

- Risk: proactive compliance reduces surprises

- Trust: improved investor and customer confidence

Partners expand mortgage reach, ~30% share; fintech cuts close 15–25%

Partners—mortgage brokers, developers, fintechs, card schemes, institutional investors and tech vendors—expand distribution and product delivery, supporting Mizrahi Tefahot’s ~30% mortgage market share in 2024.

Co-marketing and preferred-lender deals cut time-to-close ~15–25% and lift conversion; fintech integrations speed adoption ~30% faster.

Institutional ties enable securitizations/covered bonds to lower funding costs; cloud/tech vendors (AWS 32%, Azure 22%, GCP 11% in 2024) underpin digital scale.

| Partner | Role | KPI (2024) |

|---|---|---|

| Mortgage brokers/devs | Origination | ~30% market share |

| Fintechs/cards | Distribution/UX | +30% adoption, 15–25% faster close |

| Institutional investors | Wholesale funding | Enables securitizations |

| Tech vendors | Infrastructure | AWS 32%/Azure 22%/GCP 11% |

What is included in the product

A concise, pre-written Business Model Canvas for Mizrahi Tefahot Bank detailing customer segments, value propositions, channels, revenue streams and key resources across the 9 BMC blocks, reflecting real-world banking operations, competitive advantages, SWOT linkages and strategic insights for investors and analysts.

High-level view of Mizrahi Tefahot Bank’s business model with editable cells, relieving the pain of fragmented strategic planning by condensing lending, retail, and digital initiatives into a single, actionable page for fast decision-making and team alignment.

Activities

Retail and mortgage lending

Originating, underwriting and servicing home loans is Mizrahi Tefahot’s core franchise; as of 2024 the bank’s mortgage portfolio exceeded NIS 160 billion with roughly 22% market share. Pipeline management actively balances credit appetite against demand and regulatory limits to control concentration and LTVs. Pricing and product design adapt to rate cycles and housing trends, using tiered spreads and fixed/variable mixes. Ongoing servicing focuses on arrears management to protect portfolio quality and customer lifetime value.

Commercial and corporate banking

Providing working capital, term loans and treasury services supports SMEs and large corporates, leveraging Mizrahi Tefahot’s position as Israel’s third-largest bank by assets as of 2024. Relationship banking drives cross-sell across cash management and FX, while active credit monitoring and covenants control concentration and sector risk. Syndication expands capacity for large transactions.

Wealth and private banking advisory

In 2024 Mizrahi Tefahot advisors deliver portfolio management, structured products and estate planning tailored to affluent and HNW clients. Suitability checks and fiduciary processes formally guide each recommendation. Offering both discretionary and advisory mandates diversifies fee and commission revenue. Personalized service and relationship managers deepen client retention and share of wallet.

Risk management and compliance

Risk management at Mizrahi Tefahot, one of Israel's largest mortgage banks, uses credit, market, liquidity and operational risk frameworks to protect capital under Bank of Israel supervision; AML/KYC, sanctions screening and transaction monitoring preserve integrity. Regular stress testing and ICAAP/ILAAP reporting meet regulatory expectations, and continuous model validation supports sound underwriting.

- credit risk frameworks

- market & liquidity controls

- AML/KYC + sanctions screening

- stress testing, ICAAP/ILAAP

- continuous model validation

Digital product development

Building mobile, web and API experiences enables self-service and scale, with Mizrahi Tefahot focusing digital channels to reduce branch load and speed transactions.

Agile delivery combined with data analytics drives continuous improvement in customer journeys and personalization.

Robust cybersecurity and fraud controls protect channels while iterative releases keep the bank competitive in a fast-moving market.

- Digital self-service

- Agile + analytics

- Cybersecurity & fraud

- Iterative releases

NIS 160+ bn, ~22% share — Israel's 3rd-largest bank

Originating, underwriting and servicing home loans is Mizrahi Tefahot’s core activity; as of 2024 the mortgage portfolio exceeded NIS 160 billion with ~22% market share. Pipeline management balances credit appetite, concentration and LTVs while pricing adapts to rate cycles. Corporate lending, cash management and syndication support SMEs and large clients as Israel’s third-largest bank by assets in 2024. Digital channels, risk frameworks and wealth advisory diversify revenue and protect capital.

| Metric | 2024 |

|---|---|

| Mortgage portfolio | NIS 160+ bn |

| Mortgage market share | ~22% |

| Bank rank by assets | 3rd in Israel |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the actual Mizrahi Tefahot Bank Business Model Canvas—not a mockup. When you purchase, you’ll receive this exact complete file, ready to edit and present in Word and Excel. No surprises: same content, pages, and formatting as shown.

Strategic Business Model Canvas: Investor-ready roadmap of value, segments, and revenue levers

Unlock the strategic blueprint behind Mizrahi Tefahot Bank with our concise Business Model Canvas that maps value propositions, customer segments, and revenue levers. This executive-ready canvas reveals growth levers and operational efficiencies for investors and strategists. Purchase the full Word/Excel version to access company-specific insights and actionable recommendations.

Partnerships

Mortgage brokers and real estate developers

Partnering with mortgage brokers and real estate developers expands Mizrahi Tefahot’s mortgage pipeline and improves lead quality, reinforcing its position as Israel’s largest mortgage bank with roughly 30% market share in 2024.

Co-marketing and preferred-lender arrangements accelerate approvals and raise conversion rates, shortening time-to-close by industry-estimated 15–25% and lifting funded-mortgage rates.

Data-sharing on projects and buyer profiles enhances underwriting precision, reducing credit surprises and supporting the bank’s strong foothold in Israeli home financing.

Payment networks and fintech providers

Alliances with card schemes and fintechs enable Mizrahi Tefahot to deliver seamless transactions and digital wallets, supporting Israel’s shift to cashless payments in 2024. APIs and embedded banking tie the bank into merchants and apps, expanding distribution and transaction volume. Co-developing user journeys improves UX and retention, with partners reporting up to 30% faster adoption. These partnerships cut time-to-market for new services, accelerating product launches.

Institutional investors and capital markets

Tapping institutional partners supports securitizations, covered bonds and wholesale funding, enabling Mizrahi Tefahot to convert mortgage exposures into liquid instruments. Syndication relationships with banks and investors allow the bank to underwrite larger corporate and real estate transactions. Market makers and brokers improve secondary-market liquidity and pricing, collectively lowering funding costs and diversifying balance-sheet risk.

Technology vendors and cloud providers

Technology vendors for core banking, cybersecurity, analytics and cloud underpin Mizrahi Tefahot Bank’s digital transformation, enabling AI-driven underwriting, KYC/AML and CRM deployments with vendor ecosystems accelerating time-to-market.

- Cloud market share 2024: AWS ~32%, Azure ~22%, GCP ~11%

- Typical SLAs: 99.99% uptime and regulatory-grade controls

- Outcome: scalable, resilient infrastructure for growth

Regulators and industry associations

In 2024, constructive engagement with the Bank of Israel and compliance bodies sustains Mizrahi Tefahot Bank’s license integrity, reducing regulatory breach risk and operational surprises. Active participation in industry forums shapes standards for payments, open banking, and risk controls, aligning implementations ahead of enforcement. Early alignment strengthens trust with customers and investors by signaling robust governance.

- Regulator: Bank of Israel engagement

- Standards: payments and open banking

- Risk: proactive compliance reduces surprises

- Trust: improved investor and customer confidence

Partners expand mortgage reach, ~30% share; fintech cuts close 15–25%

Partners—mortgage brokers, developers, fintechs, card schemes, institutional investors and tech vendors—expand distribution and product delivery, supporting Mizrahi Tefahot’s ~30% mortgage market share in 2024.

Co-marketing and preferred-lender deals cut time-to-close ~15–25% and lift conversion; fintech integrations speed adoption ~30% faster.

Institutional ties enable securitizations/covered bonds to lower funding costs; cloud/tech vendors (AWS 32%, Azure 22%, GCP 11% in 2024) underpin digital scale.

| Partner | Role | KPI (2024) |

|---|---|---|

| Mortgage brokers/devs | Origination | ~30% market share |

| Fintechs/cards | Distribution/UX | +30% adoption, 15–25% faster close |

| Institutional investors | Wholesale funding | Enables securitizations |

| Tech vendors | Infrastructure | AWS 32%/Azure 22%/GCP 11% |

What is included in the product

A concise, pre-written Business Model Canvas for Mizrahi Tefahot Bank detailing customer segments, value propositions, channels, revenue streams and key resources across the 9 BMC blocks, reflecting real-world banking operations, competitive advantages, SWOT linkages and strategic insights for investors and analysts.

High-level view of Mizrahi Tefahot Bank’s business model with editable cells, relieving the pain of fragmented strategic planning by condensing lending, retail, and digital initiatives into a single, actionable page for fast decision-making and team alignment.

Activities

Retail and mortgage lending

Originating, underwriting and servicing home loans is Mizrahi Tefahot’s core franchise; as of 2024 the bank’s mortgage portfolio exceeded NIS 160 billion with roughly 22% market share. Pipeline management actively balances credit appetite against demand and regulatory limits to control concentration and LTVs. Pricing and product design adapt to rate cycles and housing trends, using tiered spreads and fixed/variable mixes. Ongoing servicing focuses on arrears management to protect portfolio quality and customer lifetime value.

Commercial and corporate banking

Providing working capital, term loans and treasury services supports SMEs and large corporates, leveraging Mizrahi Tefahot’s position as Israel’s third-largest bank by assets as of 2024. Relationship banking drives cross-sell across cash management and FX, while active credit monitoring and covenants control concentration and sector risk. Syndication expands capacity for large transactions.

Wealth and private banking advisory

In 2024 Mizrahi Tefahot advisors deliver portfolio management, structured products and estate planning tailored to affluent and HNW clients. Suitability checks and fiduciary processes formally guide each recommendation. Offering both discretionary and advisory mandates diversifies fee and commission revenue. Personalized service and relationship managers deepen client retention and share of wallet.

Risk management and compliance

Risk management at Mizrahi Tefahot, one of Israel's largest mortgage banks, uses credit, market, liquidity and operational risk frameworks to protect capital under Bank of Israel supervision; AML/KYC, sanctions screening and transaction monitoring preserve integrity. Regular stress testing and ICAAP/ILAAP reporting meet regulatory expectations, and continuous model validation supports sound underwriting.

- credit risk frameworks

- market & liquidity controls

- AML/KYC + sanctions screening

- stress testing, ICAAP/ILAAP

- continuous model validation

Digital product development

Building mobile, web and API experiences enables self-service and scale, with Mizrahi Tefahot focusing digital channels to reduce branch load and speed transactions.

Agile delivery combined with data analytics drives continuous improvement in customer journeys and personalization.

Robust cybersecurity and fraud controls protect channels while iterative releases keep the bank competitive in a fast-moving market.

- Digital self-service

- Agile + analytics

- Cybersecurity & fraud

- Iterative releases

NIS 160+ bn, ~22% share — Israel's 3rd-largest bank

Originating, underwriting and servicing home loans is Mizrahi Tefahot’s core activity; as of 2024 the mortgage portfolio exceeded NIS 160 billion with ~22% market share. Pipeline management balances credit appetite, concentration and LTVs while pricing adapts to rate cycles. Corporate lending, cash management and syndication support SMEs and large clients as Israel’s third-largest bank by assets in 2024. Digital channels, risk frameworks and wealth advisory diversify revenue and protect capital.

| Metric | 2024 |

|---|---|

| Mortgage portfolio | NIS 160+ bn |

| Mortgage market share | ~22% |

| Bank rank by assets | 3rd in Israel |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the actual Mizrahi Tefahot Bank Business Model Canvas—not a mockup. When you purchase, you’ll receive this exact complete file, ready to edit and present in Word and Excel. No surprises: same content, pages, and formatting as shown.

Original: $10.00

-65%$10.00

$3.50Description

Strategic Business Model Canvas: Investor-ready roadmap of value, segments, and revenue levers

Unlock the strategic blueprint behind Mizrahi Tefahot Bank with our concise Business Model Canvas that maps value propositions, customer segments, and revenue levers. This executive-ready canvas reveals growth levers and operational efficiencies for investors and strategists. Purchase the full Word/Excel version to access company-specific insights and actionable recommendations.

Partnerships

Mortgage brokers and real estate developers

Partnering with mortgage brokers and real estate developers expands Mizrahi Tefahot’s mortgage pipeline and improves lead quality, reinforcing its position as Israel’s largest mortgage bank with roughly 30% market share in 2024.

Co-marketing and preferred-lender arrangements accelerate approvals and raise conversion rates, shortening time-to-close by industry-estimated 15–25% and lifting funded-mortgage rates.

Data-sharing on projects and buyer profiles enhances underwriting precision, reducing credit surprises and supporting the bank’s strong foothold in Israeli home financing.

Payment networks and fintech providers

Alliances with card schemes and fintechs enable Mizrahi Tefahot to deliver seamless transactions and digital wallets, supporting Israel’s shift to cashless payments in 2024. APIs and embedded banking tie the bank into merchants and apps, expanding distribution and transaction volume. Co-developing user journeys improves UX and retention, with partners reporting up to 30% faster adoption. These partnerships cut time-to-market for new services, accelerating product launches.

Institutional investors and capital markets

Tapping institutional partners supports securitizations, covered bonds and wholesale funding, enabling Mizrahi Tefahot to convert mortgage exposures into liquid instruments. Syndication relationships with banks and investors allow the bank to underwrite larger corporate and real estate transactions. Market makers and brokers improve secondary-market liquidity and pricing, collectively lowering funding costs and diversifying balance-sheet risk.

Technology vendors and cloud providers

Technology vendors for core banking, cybersecurity, analytics and cloud underpin Mizrahi Tefahot Bank’s digital transformation, enabling AI-driven underwriting, KYC/AML and CRM deployments with vendor ecosystems accelerating time-to-market.

- Cloud market share 2024: AWS ~32%, Azure ~22%, GCP ~11%

- Typical SLAs: 99.99% uptime and regulatory-grade controls

- Outcome: scalable, resilient infrastructure for growth

Regulators and industry associations

In 2024, constructive engagement with the Bank of Israel and compliance bodies sustains Mizrahi Tefahot Bank’s license integrity, reducing regulatory breach risk and operational surprises. Active participation in industry forums shapes standards for payments, open banking, and risk controls, aligning implementations ahead of enforcement. Early alignment strengthens trust with customers and investors by signaling robust governance.

- Regulator: Bank of Israel engagement

- Standards: payments and open banking

- Risk: proactive compliance reduces surprises

- Trust: improved investor and customer confidence

Partners expand mortgage reach, ~30% share; fintech cuts close 15–25%

Partners—mortgage brokers, developers, fintechs, card schemes, institutional investors and tech vendors—expand distribution and product delivery, supporting Mizrahi Tefahot’s ~30% mortgage market share in 2024.

Co-marketing and preferred-lender deals cut time-to-close ~15–25% and lift conversion; fintech integrations speed adoption ~30% faster.

Institutional ties enable securitizations/covered bonds to lower funding costs; cloud/tech vendors (AWS 32%, Azure 22%, GCP 11% in 2024) underpin digital scale.

| Partner | Role | KPI (2024) |

|---|---|---|

| Mortgage brokers/devs | Origination | ~30% market share |

| Fintechs/cards | Distribution/UX | +30% adoption, 15–25% faster close |

| Institutional investors | Wholesale funding | Enables securitizations |

| Tech vendors | Infrastructure | AWS 32%/Azure 22%/GCP 11% |

What is included in the product

A concise, pre-written Business Model Canvas for Mizrahi Tefahot Bank detailing customer segments, value propositions, channels, revenue streams and key resources across the 9 BMC blocks, reflecting real-world banking operations, competitive advantages, SWOT linkages and strategic insights for investors and analysts.

High-level view of Mizrahi Tefahot Bank’s business model with editable cells, relieving the pain of fragmented strategic planning by condensing lending, retail, and digital initiatives into a single, actionable page for fast decision-making and team alignment.

Activities

Retail and mortgage lending

Originating, underwriting and servicing home loans is Mizrahi Tefahot’s core franchise; as of 2024 the bank’s mortgage portfolio exceeded NIS 160 billion with roughly 22% market share. Pipeline management actively balances credit appetite against demand and regulatory limits to control concentration and LTVs. Pricing and product design adapt to rate cycles and housing trends, using tiered spreads and fixed/variable mixes. Ongoing servicing focuses on arrears management to protect portfolio quality and customer lifetime value.

Commercial and corporate banking

Providing working capital, term loans and treasury services supports SMEs and large corporates, leveraging Mizrahi Tefahot’s position as Israel’s third-largest bank by assets as of 2024. Relationship banking drives cross-sell across cash management and FX, while active credit monitoring and covenants control concentration and sector risk. Syndication expands capacity for large transactions.

Wealth and private banking advisory

In 2024 Mizrahi Tefahot advisors deliver portfolio management, structured products and estate planning tailored to affluent and HNW clients. Suitability checks and fiduciary processes formally guide each recommendation. Offering both discretionary and advisory mandates diversifies fee and commission revenue. Personalized service and relationship managers deepen client retention and share of wallet.

Risk management and compliance

Risk management at Mizrahi Tefahot, one of Israel's largest mortgage banks, uses credit, market, liquidity and operational risk frameworks to protect capital under Bank of Israel supervision; AML/KYC, sanctions screening and transaction monitoring preserve integrity. Regular stress testing and ICAAP/ILAAP reporting meet regulatory expectations, and continuous model validation supports sound underwriting.

- credit risk frameworks

- market & liquidity controls

- AML/KYC + sanctions screening

- stress testing, ICAAP/ILAAP

- continuous model validation

Digital product development

Building mobile, web and API experiences enables self-service and scale, with Mizrahi Tefahot focusing digital channels to reduce branch load and speed transactions.

Agile delivery combined with data analytics drives continuous improvement in customer journeys and personalization.

Robust cybersecurity and fraud controls protect channels while iterative releases keep the bank competitive in a fast-moving market.

- Digital self-service

- Agile + analytics

- Cybersecurity & fraud

- Iterative releases

NIS 160+ bn, ~22% share — Israel's 3rd-largest bank

Originating, underwriting and servicing home loans is Mizrahi Tefahot’s core activity; as of 2024 the mortgage portfolio exceeded NIS 160 billion with ~22% market share. Pipeline management balances credit appetite, concentration and LTVs while pricing adapts to rate cycles. Corporate lending, cash management and syndication support SMEs and large clients as Israel’s third-largest bank by assets in 2024. Digital channels, risk frameworks and wealth advisory diversify revenue and protect capital.

| Metric | 2024 |

|---|---|

| Mortgage portfolio | NIS 160+ bn |

| Mortgage market share | ~22% |

| Bank rank by assets | 3rd in Israel |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the actual Mizrahi Tefahot Bank Business Model Canvas—not a mockup. When you purchase, you’ll receive this exact complete file, ready to edit and present in Word and Excel. No surprises: same content, pages, and formatting as shown.