Marsh & McLennan Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

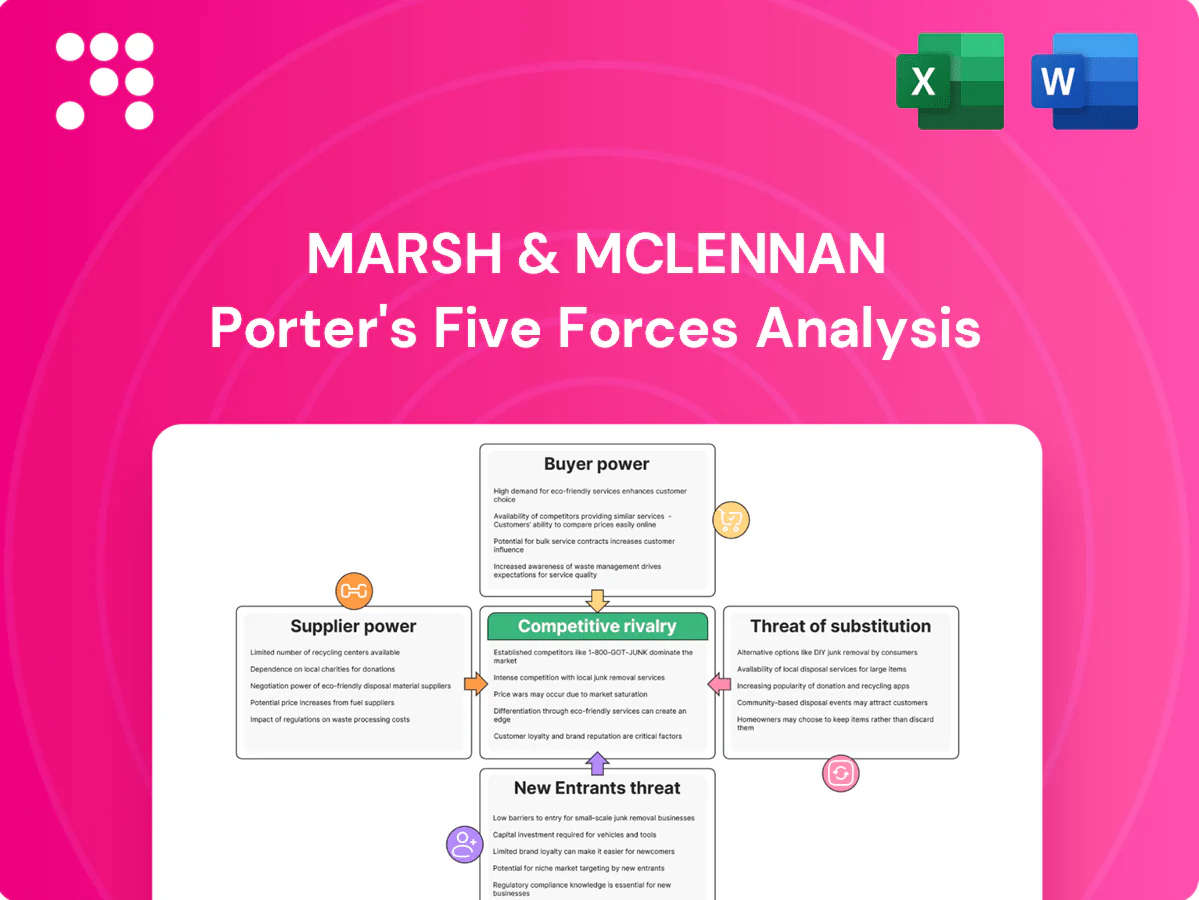

Marsh & McLennan’s Porter’s Five Forces reveal moderate buyer power, concentrated supplier relationships, high rivalry among diversified competitors, low threat of substitutes for core risk advisory services, and barriers that temper new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of insurance and reinsurance capacity

MMC’s broking arms depend on a finite pool of global carriers and reinsurers, concentrating supply power especially in hard markets. Capacity cycles let insurers tighten terms, limit coverage, and push commissions down, squeezing broker margins. Long-standing panel relationships temper extremities but cannot fully offset supply-side discipline that compresses broker economics. Diversifying markets and alternative capital provide relief but do not eliminate carrier leverage.

Specialized talent and expertise as critical inputs

Senior brokers, actuaries, catastrophe modelers and strategy consultants are scarce and mobile, giving suppliers bargaining power; MMC’s ~85,000 global workforce and 2024 revenue near $25B heighten exposure. Wage inflation and richer retention packages (comp increases in professional services up 8–12% in 2024) squeeze margins and delivery capacity. MMC uses brand, career paths and equity incentives, yet immigration caps and credentialing bottlenecks keep the pipeline tight.

Data, models, and analytics vendors

Proprietary and third-party risk data, catastrophe models and ESG datasets are concentrated among three dominant cat-model vendors—AIR, RMS and CoreLogic—creating supplier dependency in 2024. Long validation cycles and switching costs give these vendors pricing and contract leverage. MMC builds in-house analytics to mitigate exposure but must interoperate with industry-standard tools. Ongoing vendor consolidation in 2024 risks higher costs and reduced negotiating room.

Technology platforms and infrastructure

Cloud, cybersecurity, and workflow systems are concentrated (AWS ~32%, Azure ~23%, GCP ~11% in 2024), boosting supplier power; long implementations (3–18 months) and complex integrations raise switching costs. MMC leverages scale and multi-year enterprise deals (commonly 3–7 years) but remains exposed to price escalations and service-term risks, with regulatory and client-security mandates increasing dependence on top-tier vendors.

- Market concentration: AWS/Azure/GCP ~66%

- Contract length: 3–7 yrs

- Regulatory dependence: rising

Regulatory bodies and licensing authorities

Regulatory bodies and licensing authorities act as quasi-suppliers of market access for MMC: licenses, conduct rules, and compliance standards gatekeep client origination and product delivery, and shifts in solvency, fiduciary, or compensation rules can materially reprice risk and cost-to-serve. MMC’s scale in compliance and risk controls mitigates disruption, but regulatory rule changes can rapidly alter margins and process economics.

- Gatekeeping power: licenses = access constraint

- Rule shifts (solvency/fiduciary) reprice risk/cost

- MMC compliance scale reduces but does not eliminate impact

Suppliers squeeze major insurer: $25B, 85,000 staff, comp up 8–12%

Suppliers hold significant leverage over MMC: concentrated carriers/reinsurers tighten terms in hard markets, compressing broking margins; MMC revenue ~$25B and 85,000 staff increase exposure. Talent scarcity and 2024 comp inflation (8–12%) raise costs; cat-model and cloud vendor concentration (AIR/RMS/CoreLogic; AWS/Azure/GCP ~32/23/11%) add pricing and switching risk.

| Metric | 2024 Value |

|---|---|

| Revenue | $~25B |

| Employees | ~85,000 |

| Comp inflation | 8–12% |

| Cloud share (AWS/Azure/GCP) | 32%/23%/11% |

| Key cat-models | AIR, RMS, CoreLogic |

What is included in the product

Porter’s Five Forces analysis for Marsh & McLennan examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptors to assess impacts on pricing, margins, market share and strategic positioning.

A concise one-sheet summary of Marsh & McLennan's Five Forces that instantly highlights competitive pressure and strategic levers. Customizable pressure levels and an export-ready radar chart make it easy to update, present, and integrate into decks or dashboards.

Customers Bargaining Power

Large corporate and public-sector clients

Large corporate and public-sector clients run competitive RFPs, benchmark fees and demand bespoke solutions, elevating buyer power. Their premium volumes and multi-line needs give them pricing leverage against brokers. MMC counters with differentiated expertise, global placement reach and bundled offerings; as of 2024 MMC operates in 130+ countries with ~85,000 employees. Multi-year relationships reduce churn but do not eliminate fee pressure.

Price transparency and benchmarking

Clients increasingly scrutinize broker remuneration, commissions and contingent income, intensifying negotiations; MMC reported 2024 revenue of $22.4 billion, heightening focus on fee disclosure. Market data and peer benchmarking empower tougher asks on rates and scope, pressuring margin. MMC’s value narrative must emphasize loss-cost reductions and outcomes over hours, while outcome-based and fixed-fee models align interests but cap upside.

Switching and multi-homing behavior

Switching costs from data, policy history and program design create friction, yet many buyers alternate or split mandates and use co-broking/panels that dilute any single provider’s hold. MMC offsets this with industry specialization and analytics stickiness to raise switching frictions. Transitions cluster at annual renewals, concentrating risk into yearly cycles. MMC reported roughly $23.3 billion revenue in 2024, underscoring scale in panels and mandates.

Internalization of capabilities

Larger clients increasingly internalize risk, HR and investment capabilities, substituting external advisory and compressing fees; 2024 industry reports note a clear shift toward insourcing of routine advisory tasks. Insourcing leaves firms vying for complex, episodic work, forcing MMC to innovate to remain indispensable on high-impact matters while managing knowledge transfer that gradually empowers buyers.

- Clients insource routine advisory

- MMC competes for complex, episodic work

- Continuous innovation required to retain high-value mandates

Demand cyclicality and budget constraints

Macro slowdowns, rate cycles and rising benefits costs in 2024 intensified procurement discipline, prompting buyers to defer projects, cut scope or demand productivity guarantees; MMC’s four-business model and presence in over 130 countries (2024) help smooth volatility, though concentrated exposure in sectors like energy and CRE drives localized pricing concessions.

- Buyers defer/trim scope

- Demand guarantees

- MMC: four businesses, 130+ countries (2024)

- Sector concentration → local concessions

Clients insource and demand outcome-based fees, squeezing advisory margins despite scale

Large institutional buyers run RFPs and benchmark fees, giving them strong leverage; MMC counters with scale, specialization and analytics but faces persistent fee pressure. Clients increasingly insource routine work and demand outcome-based or fixed fees, compressing advisory margins. Annual renewal clustering and co-broking dilute single-vendor power despite MMC’s global reach.

| Metric | 2024 |

|---|---|

| Revenue | $22.4B |

| Employees | ~85,000 |

| Countries | 130+ |

| Buyer trend | Insourcing, fee pressure |

Full Version Awaits

Marsh & McLennan Porter's Five Forces Analysis

This preview shows the exact Marsh & McLennan Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders. The file is fully formatted and ready for download, containing the same comprehensive competitive assessment, evidence, and conclusions. Purchase grants instant access to this identical document for immediate use.

Go Beyond the Preview—Access the Full Strategic Report

Marsh & McLennan’s Porter’s Five Forces reveal moderate buyer power, concentrated supplier relationships, high rivalry among diversified competitors, low threat of substitutes for core risk advisory services, and barriers that temper new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of insurance and reinsurance capacity

MMC’s broking arms depend on a finite pool of global carriers and reinsurers, concentrating supply power especially in hard markets. Capacity cycles let insurers tighten terms, limit coverage, and push commissions down, squeezing broker margins. Long-standing panel relationships temper extremities but cannot fully offset supply-side discipline that compresses broker economics. Diversifying markets and alternative capital provide relief but do not eliminate carrier leverage.

Specialized talent and expertise as critical inputs

Senior brokers, actuaries, catastrophe modelers and strategy consultants are scarce and mobile, giving suppliers bargaining power; MMC’s ~85,000 global workforce and 2024 revenue near $25B heighten exposure. Wage inflation and richer retention packages (comp increases in professional services up 8–12% in 2024) squeeze margins and delivery capacity. MMC uses brand, career paths and equity incentives, yet immigration caps and credentialing bottlenecks keep the pipeline tight.

Data, models, and analytics vendors

Proprietary and third-party risk data, catastrophe models and ESG datasets are concentrated among three dominant cat-model vendors—AIR, RMS and CoreLogic—creating supplier dependency in 2024. Long validation cycles and switching costs give these vendors pricing and contract leverage. MMC builds in-house analytics to mitigate exposure but must interoperate with industry-standard tools. Ongoing vendor consolidation in 2024 risks higher costs and reduced negotiating room.

Technology platforms and infrastructure

Cloud, cybersecurity, and workflow systems are concentrated (AWS ~32%, Azure ~23%, GCP ~11% in 2024), boosting supplier power; long implementations (3–18 months) and complex integrations raise switching costs. MMC leverages scale and multi-year enterprise deals (commonly 3–7 years) but remains exposed to price escalations and service-term risks, with regulatory and client-security mandates increasing dependence on top-tier vendors.

- Market concentration: AWS/Azure/GCP ~66%

- Contract length: 3–7 yrs

- Regulatory dependence: rising

Regulatory bodies and licensing authorities

Regulatory bodies and licensing authorities act as quasi-suppliers of market access for MMC: licenses, conduct rules, and compliance standards gatekeep client origination and product delivery, and shifts in solvency, fiduciary, or compensation rules can materially reprice risk and cost-to-serve. MMC’s scale in compliance and risk controls mitigates disruption, but regulatory rule changes can rapidly alter margins and process economics.

- Gatekeeping power: licenses = access constraint

- Rule shifts (solvency/fiduciary) reprice risk/cost

- MMC compliance scale reduces but does not eliminate impact

Suppliers squeeze major insurer: $25B, 85,000 staff, comp up 8–12%

Suppliers hold significant leverage over MMC: concentrated carriers/reinsurers tighten terms in hard markets, compressing broking margins; MMC revenue ~$25B and 85,000 staff increase exposure. Talent scarcity and 2024 comp inflation (8–12%) raise costs; cat-model and cloud vendor concentration (AIR/RMS/CoreLogic; AWS/Azure/GCP ~32/23/11%) add pricing and switching risk.

| Metric | 2024 Value |

|---|---|

| Revenue | $~25B |

| Employees | ~85,000 |

| Comp inflation | 8–12% |

| Cloud share (AWS/Azure/GCP) | 32%/23%/11% |

| Key cat-models | AIR, RMS, CoreLogic |

What is included in the product

Porter’s Five Forces analysis for Marsh & McLennan examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptors to assess impacts on pricing, margins, market share and strategic positioning.

A concise one-sheet summary of Marsh & McLennan's Five Forces that instantly highlights competitive pressure and strategic levers. Customizable pressure levels and an export-ready radar chart make it easy to update, present, and integrate into decks or dashboards.

Customers Bargaining Power

Large corporate and public-sector clients

Large corporate and public-sector clients run competitive RFPs, benchmark fees and demand bespoke solutions, elevating buyer power. Their premium volumes and multi-line needs give them pricing leverage against brokers. MMC counters with differentiated expertise, global placement reach and bundled offerings; as of 2024 MMC operates in 130+ countries with ~85,000 employees. Multi-year relationships reduce churn but do not eliminate fee pressure.

Price transparency and benchmarking

Clients increasingly scrutinize broker remuneration, commissions and contingent income, intensifying negotiations; MMC reported 2024 revenue of $22.4 billion, heightening focus on fee disclosure. Market data and peer benchmarking empower tougher asks on rates and scope, pressuring margin. MMC’s value narrative must emphasize loss-cost reductions and outcomes over hours, while outcome-based and fixed-fee models align interests but cap upside.

Switching and multi-homing behavior

Switching costs from data, policy history and program design create friction, yet many buyers alternate or split mandates and use co-broking/panels that dilute any single provider’s hold. MMC offsets this with industry specialization and analytics stickiness to raise switching frictions. Transitions cluster at annual renewals, concentrating risk into yearly cycles. MMC reported roughly $23.3 billion revenue in 2024, underscoring scale in panels and mandates.

Internalization of capabilities

Larger clients increasingly internalize risk, HR and investment capabilities, substituting external advisory and compressing fees; 2024 industry reports note a clear shift toward insourcing of routine advisory tasks. Insourcing leaves firms vying for complex, episodic work, forcing MMC to innovate to remain indispensable on high-impact matters while managing knowledge transfer that gradually empowers buyers.

- Clients insource routine advisory

- MMC competes for complex, episodic work

- Continuous innovation required to retain high-value mandates

Demand cyclicality and budget constraints

Macro slowdowns, rate cycles and rising benefits costs in 2024 intensified procurement discipline, prompting buyers to defer projects, cut scope or demand productivity guarantees; MMC’s four-business model and presence in over 130 countries (2024) help smooth volatility, though concentrated exposure in sectors like energy and CRE drives localized pricing concessions.

- Buyers defer/trim scope

- Demand guarantees

- MMC: four businesses, 130+ countries (2024)

- Sector concentration → local concessions

Clients insource and demand outcome-based fees, squeezing advisory margins despite scale

Large institutional buyers run RFPs and benchmark fees, giving them strong leverage; MMC counters with scale, specialization and analytics but faces persistent fee pressure. Clients increasingly insource routine work and demand outcome-based or fixed fees, compressing advisory margins. Annual renewal clustering and co-broking dilute single-vendor power despite MMC’s global reach.

| Metric | 2024 |

|---|---|

| Revenue | $22.4B |

| Employees | ~85,000 |

| Countries | 130+ |

| Buyer trend | Insourcing, fee pressure |

Full Version Awaits

Marsh & McLennan Porter's Five Forces Analysis

This preview shows the exact Marsh & McLennan Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders. The file is fully formatted and ready for download, containing the same comprehensive competitive assessment, evidence, and conclusions. Purchase grants instant access to this identical document for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Marsh & McLennan’s Porter’s Five Forces reveal moderate buyer power, concentrated supplier relationships, high rivalry among diversified competitors, low threat of substitutes for core risk advisory services, and barriers that temper new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of insurance and reinsurance capacity

MMC’s broking arms depend on a finite pool of global carriers and reinsurers, concentrating supply power especially in hard markets. Capacity cycles let insurers tighten terms, limit coverage, and push commissions down, squeezing broker margins. Long-standing panel relationships temper extremities but cannot fully offset supply-side discipline that compresses broker economics. Diversifying markets and alternative capital provide relief but do not eliminate carrier leverage.

Specialized talent and expertise as critical inputs

Senior brokers, actuaries, catastrophe modelers and strategy consultants are scarce and mobile, giving suppliers bargaining power; MMC’s ~85,000 global workforce and 2024 revenue near $25B heighten exposure. Wage inflation and richer retention packages (comp increases in professional services up 8–12% in 2024) squeeze margins and delivery capacity. MMC uses brand, career paths and equity incentives, yet immigration caps and credentialing bottlenecks keep the pipeline tight.

Data, models, and analytics vendors

Proprietary and third-party risk data, catastrophe models and ESG datasets are concentrated among three dominant cat-model vendors—AIR, RMS and CoreLogic—creating supplier dependency in 2024. Long validation cycles and switching costs give these vendors pricing and contract leverage. MMC builds in-house analytics to mitigate exposure but must interoperate with industry-standard tools. Ongoing vendor consolidation in 2024 risks higher costs and reduced negotiating room.

Technology platforms and infrastructure

Cloud, cybersecurity, and workflow systems are concentrated (AWS ~32%, Azure ~23%, GCP ~11% in 2024), boosting supplier power; long implementations (3–18 months) and complex integrations raise switching costs. MMC leverages scale and multi-year enterprise deals (commonly 3–7 years) but remains exposed to price escalations and service-term risks, with regulatory and client-security mandates increasing dependence on top-tier vendors.

- Market concentration: AWS/Azure/GCP ~66%

- Contract length: 3–7 yrs

- Regulatory dependence: rising

Regulatory bodies and licensing authorities

Regulatory bodies and licensing authorities act as quasi-suppliers of market access for MMC: licenses, conduct rules, and compliance standards gatekeep client origination and product delivery, and shifts in solvency, fiduciary, or compensation rules can materially reprice risk and cost-to-serve. MMC’s scale in compliance and risk controls mitigates disruption, but regulatory rule changes can rapidly alter margins and process economics.

- Gatekeeping power: licenses = access constraint

- Rule shifts (solvency/fiduciary) reprice risk/cost

- MMC compliance scale reduces but does not eliminate impact

Suppliers squeeze major insurer: $25B, 85,000 staff, comp up 8–12%

Suppliers hold significant leverage over MMC: concentrated carriers/reinsurers tighten terms in hard markets, compressing broking margins; MMC revenue ~$25B and 85,000 staff increase exposure. Talent scarcity and 2024 comp inflation (8–12%) raise costs; cat-model and cloud vendor concentration (AIR/RMS/CoreLogic; AWS/Azure/GCP ~32/23/11%) add pricing and switching risk.

| Metric | 2024 Value |

|---|---|

| Revenue | $~25B |

| Employees | ~85,000 |

| Comp inflation | 8–12% |

| Cloud share (AWS/Azure/GCP) | 32%/23%/11% |

| Key cat-models | AIR, RMS, CoreLogic |

What is included in the product

Porter’s Five Forces analysis for Marsh & McLennan examines competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptors to assess impacts on pricing, margins, market share and strategic positioning.

A concise one-sheet summary of Marsh & McLennan's Five Forces that instantly highlights competitive pressure and strategic levers. Customizable pressure levels and an export-ready radar chart make it easy to update, present, and integrate into decks or dashboards.

Customers Bargaining Power

Large corporate and public-sector clients

Large corporate and public-sector clients run competitive RFPs, benchmark fees and demand bespoke solutions, elevating buyer power. Their premium volumes and multi-line needs give them pricing leverage against brokers. MMC counters with differentiated expertise, global placement reach and bundled offerings; as of 2024 MMC operates in 130+ countries with ~85,000 employees. Multi-year relationships reduce churn but do not eliminate fee pressure.

Price transparency and benchmarking

Clients increasingly scrutinize broker remuneration, commissions and contingent income, intensifying negotiations; MMC reported 2024 revenue of $22.4 billion, heightening focus on fee disclosure. Market data and peer benchmarking empower tougher asks on rates and scope, pressuring margin. MMC’s value narrative must emphasize loss-cost reductions and outcomes over hours, while outcome-based and fixed-fee models align interests but cap upside.

Switching and multi-homing behavior

Switching costs from data, policy history and program design create friction, yet many buyers alternate or split mandates and use co-broking/panels that dilute any single provider’s hold. MMC offsets this with industry specialization and analytics stickiness to raise switching frictions. Transitions cluster at annual renewals, concentrating risk into yearly cycles. MMC reported roughly $23.3 billion revenue in 2024, underscoring scale in panels and mandates.

Internalization of capabilities

Larger clients increasingly internalize risk, HR and investment capabilities, substituting external advisory and compressing fees; 2024 industry reports note a clear shift toward insourcing of routine advisory tasks. Insourcing leaves firms vying for complex, episodic work, forcing MMC to innovate to remain indispensable on high-impact matters while managing knowledge transfer that gradually empowers buyers.

- Clients insource routine advisory

- MMC competes for complex, episodic work

- Continuous innovation required to retain high-value mandates

Demand cyclicality and budget constraints

Macro slowdowns, rate cycles and rising benefits costs in 2024 intensified procurement discipline, prompting buyers to defer projects, cut scope or demand productivity guarantees; MMC’s four-business model and presence in over 130 countries (2024) help smooth volatility, though concentrated exposure in sectors like energy and CRE drives localized pricing concessions.

- Buyers defer/trim scope

- Demand guarantees

- MMC: four businesses, 130+ countries (2024)

- Sector concentration → local concessions

Clients insource and demand outcome-based fees, squeezing advisory margins despite scale

Large institutional buyers run RFPs and benchmark fees, giving them strong leverage; MMC counters with scale, specialization and analytics but faces persistent fee pressure. Clients increasingly insource routine work and demand outcome-based or fixed fees, compressing advisory margins. Annual renewal clustering and co-broking dilute single-vendor power despite MMC’s global reach.

| Metric | 2024 |

|---|---|

| Revenue | $22.4B |

| Employees | ~85,000 |

| Countries | 130+ |

| Buyer trend | Insourcing, fee pressure |

Full Version Awaits

Marsh & McLennan Porter's Five Forces Analysis

This preview shows the exact Marsh & McLennan Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders. The file is fully formatted and ready for download, containing the same comprehensive competitive assessment, evidence, and conclusions. Purchase grants instant access to this identical document for immediate use.