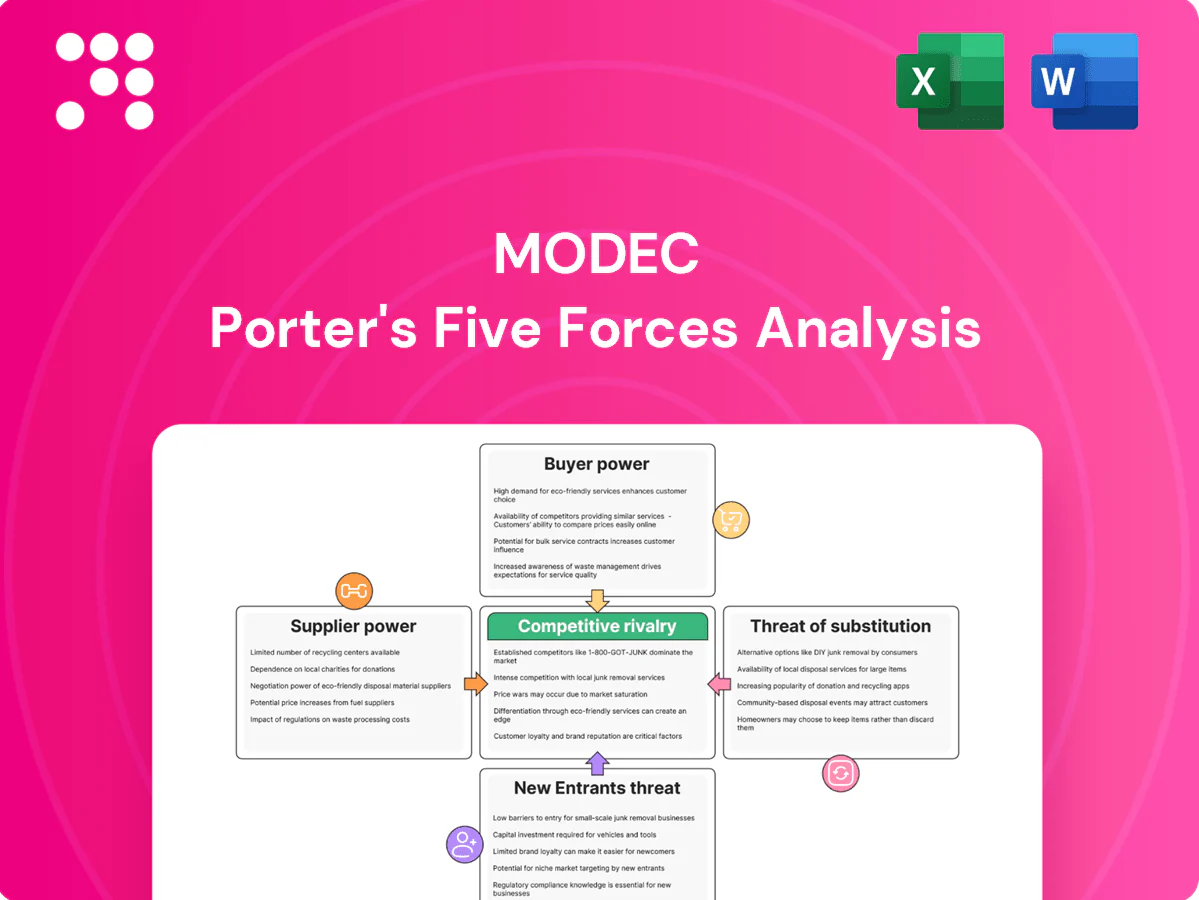

MODEC Porter's Five Forces Analysis

From Overview to Strategy Blueprint

MODEC faces moderate supplier power, high capital barriers deterring new entrants, and intense rivalry among specialized offshore contractors, while buyer negotiation and substitute threats vary by project type. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to MODEC.

Suppliers Bargaining Power

Concentrated critical equipment suppliers

High-spec topsides, subsea umbilicals, turret mooring systems and gas compression packages come from a handful of OEMs, leaving limited alternatives and high switching costs for floating-FPSO contractors like MODEC. Global lead times for complex topsides and subsea packages averaged 24–36 months in 2024, raising delivery risk. Suppliers can demand firmer pricing and extended schedules in upcycles. Strategic dual-sourcing and frame agreements mitigate but do not remove supplier leverage.

Shipyards and fabrication yard capacity constraints

FPSO hull conversions and newbuilds depend on a small set of qualified Asian shipyards and global fabrication yards, with the top Asian yards handling over 60% of complex offshore projects in 2024. Tight yard slots elevate supplier power and enable repricing of change orders. When offshore cycles heat up, queue priority can carry significant premiums. Long-term partnerships and early slot reservations remain essential mitigants.

Specialist labor and engineering talent

Marine, process and offshore engineering talent is scarce and globally mobile, with 69% of employers reporting technical talent shortages in 2024 (ManpowerGroup), pushing MODEC to absorb higher labor premiums; wage inflation and retention bonuses have increased project labor costs materially. Union rules and region-specific labor regulations add scheduling and cost rigidity. MODEC’s in-house training pipelines and global mobility programs partially offset supplier power by improving retention and redeployment.

Technology licensors and IP owners

Technology licensors and IP owners (eg UOP, Axens, Shell) control critical process units like gas treatment and sulphur recovery; as of 2024 these vendors remain few, sustaining leverage over fees, performance guarantees and audit rights. Limited proven-package substitutes reinforce pricing power, while enterprise-level master agreements can compress licensing cost and contractual exposure.

- Few dominant licensors (2024)

- Licensing governs fees, guarantees, audits

- Limited substitutes = higher supplier power

- Master agreements mitigate cost and risk

Commodity and logistics volatility

Commodity and logistics volatility materially affect FPSO economics: steel and specialty-alloy costs spiked in 2024 (premium alloy premiums up ~15–20%), while long-haul heavy-lift freight tightened, shifting bargaining power to material traders and logistics providers. Price spikes and freight tightness increase pass-through risk; hedging and early procurement mitigate exposure but add procurement complexity and cash-lock. Incoterms and pass-through clauses are increasingly used to allocate cost shocks to clients.

- Steel/alloys: premiums ~15–20% (2024)

- Freight: heavy-lift tightness, spot rate uplifts

- Mitigation: hedging, early buy, incoterms/pass-through

Concentrated suppliers, lead times 24-36 months, Asian yards >60%

Suppliers of topsides, subsea packages and licensors remain concentrated, giving them strong pricing and schedule leverage; lead times 24–36 months (2024) and limited OEMs raise switching costs. Asian yards handled >60% of complex projects (2024), tightening hull/newbuild availability and enabling change-order repricing. Steel/alloy premiums rose ~15–20% (2024), shifting cost risk to contractors and clients.

| Metric | 2024 |

|---|---|

| Topsides/subsea lead time | 24–36 months |

| Top Asian yard share | >60% |

| Alloy premiums | +15–20% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for MODEC, with detailed assessment of supplier and buyer power, substitutes, and competitive rivalry. Highlights disruptive threats, barriers protecting incumbents, and actionable insights for strategy and investor materials.

A compact, customizable Five Forces snapshot for MODEC—instantly highlights supplier, buyer and competitive pressures with a radar chart and clean layout ready for decks; duplicate scenarios, swap in your own data and notes, and integrate into wider reports without macros.

Customers Bargaining Power

Concentrated, sophisticated IOCs and NOCs

MODEC’s customers are concentrated IOCs and NOCs with deep technical and procurement teams that run competitive, often multi-billion-dollar tenders; individual FPSO contracts commonly exceed $1bn. They demand strict performance metrics, warranties and liquidated damages, enabling tough commercial terms and penalty regimes. Scale and procurement sophistication give customers strong bargaining power, so MODEC’s long-term relationships and execution track record are critical differentiators.

High deal size and long contract duration

As of 2024 FPSO projects are typically multi-billion-dollar commitments (commonly USD 1–3+ billion) with charter contracts of 10–20 years, concentrating buyer leverage at award and during negotiations. Clients increasingly demand turnkey EPC(I) scopes with extended warranties and availability-linked payments, shifting performance risk onto suppliers. Choice of financing (lease versus sale) materially alters pricing power and balance-sheet treatment, while robust risk allocation and transparent cost models have proven to ease negotiations.

Option of lease versus build-own-operate

In 2024 clients choosing lease consortia versus outright purchase create persistent pricing tension for MODEC. BOO and BOLease structures shift opex and uptime risk onto MODEC, prompting far tougher buyer due diligence and contract scrutiny. Buyers increasingly benchmark MODEC against peers SBM, BW and Yinson to compress margins. Flexible commercial offerings remain key to defending share.

Stringent ESG and local content demands

Operators now demand low-emission designs and high local content, tightening specs and raising compliance costs that buyers often do not fully offset; non-compliance can disqualify bids. Early ESG integration and local JV formation convert these constraints into competitive win themes, with many 2024 tenders setting local content targets above 30% and explicit 2030 emissions pathways.

Performance-based O&M terms

O&M contracts tie MODEC revenue to uptime and safety KPIs, commonly specifying 98–99.5% uptime; buyers levy liquidated damages for downtime, shifting operational risk to MODEC. Data transparency and digital monitoring increase buyer oversight and enable real-time performance deductions. Superior, consistent reliability builds client lock-in over multi-year charters, gradually reducing buyer bargaining power.

- Uptime targets: 98–99.5%

- Risk shift: liquidated damages for downtime

- Oversight: real-time digital monitoring

- Lock-in: reliability reduces buyer power

IOC/NOC FPSO tenders force turnkey risk shift, >30% local content & 98-99.5% uptime

MODEC’s buyers are concentrated IOCs/NOCs running competitive USD 1–3+bn FPSO tenders with 10–20 year charters, giving strong negotiation leverage. Clients push turnkey EPC(I), extended warranties and uptime-linked payments, shifting risk and compressing margins vs peers (SBM, BW, Yinson). 2024 tenders often require >30% local content and 98–99.5% uptime, with liquidated damages common.

| Metric | 2024 Benchmark |

|---|---|

| Typical FPSO CAPEX | USD 1–3+bn |

| Charter length | 10–20 years |

| Uptime target | 98–99.5% |

| Local content | >30% |

Preview Before You Purchase

MODEC Porter's Five Forces Analysis

This preview shows the exact MODEC Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted and ready to use. No mockups, placeholders, or partial samples; the file available for download after payment is identical to what you see here. Use it immediately for competitive assessment, strategic planning, or investment decisions.

From Overview to Strategy Blueprint

MODEC faces moderate supplier power, high capital barriers deterring new entrants, and intense rivalry among specialized offshore contractors, while buyer negotiation and substitute threats vary by project type. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to MODEC.

Suppliers Bargaining Power

Concentrated critical equipment suppliers

High-spec topsides, subsea umbilicals, turret mooring systems and gas compression packages come from a handful of OEMs, leaving limited alternatives and high switching costs for floating-FPSO contractors like MODEC. Global lead times for complex topsides and subsea packages averaged 24–36 months in 2024, raising delivery risk. Suppliers can demand firmer pricing and extended schedules in upcycles. Strategic dual-sourcing and frame agreements mitigate but do not remove supplier leverage.

Shipyards and fabrication yard capacity constraints

FPSO hull conversions and newbuilds depend on a small set of qualified Asian shipyards and global fabrication yards, with the top Asian yards handling over 60% of complex offshore projects in 2024. Tight yard slots elevate supplier power and enable repricing of change orders. When offshore cycles heat up, queue priority can carry significant premiums. Long-term partnerships and early slot reservations remain essential mitigants.

Specialist labor and engineering talent

Marine, process and offshore engineering talent is scarce and globally mobile, with 69% of employers reporting technical talent shortages in 2024 (ManpowerGroup), pushing MODEC to absorb higher labor premiums; wage inflation and retention bonuses have increased project labor costs materially. Union rules and region-specific labor regulations add scheduling and cost rigidity. MODEC’s in-house training pipelines and global mobility programs partially offset supplier power by improving retention and redeployment.

Technology licensors and IP owners

Technology licensors and IP owners (eg UOP, Axens, Shell) control critical process units like gas treatment and sulphur recovery; as of 2024 these vendors remain few, sustaining leverage over fees, performance guarantees and audit rights. Limited proven-package substitutes reinforce pricing power, while enterprise-level master agreements can compress licensing cost and contractual exposure.

- Few dominant licensors (2024)

- Licensing governs fees, guarantees, audits

- Limited substitutes = higher supplier power

- Master agreements mitigate cost and risk

Commodity and logistics volatility

Commodity and logistics volatility materially affect FPSO economics: steel and specialty-alloy costs spiked in 2024 (premium alloy premiums up ~15–20%), while long-haul heavy-lift freight tightened, shifting bargaining power to material traders and logistics providers. Price spikes and freight tightness increase pass-through risk; hedging and early procurement mitigate exposure but add procurement complexity and cash-lock. Incoterms and pass-through clauses are increasingly used to allocate cost shocks to clients.

- Steel/alloys: premiums ~15–20% (2024)

- Freight: heavy-lift tightness, spot rate uplifts

- Mitigation: hedging, early buy, incoterms/pass-through

Concentrated suppliers, lead times 24-36 months, Asian yards >60%

Suppliers of topsides, subsea packages and licensors remain concentrated, giving them strong pricing and schedule leverage; lead times 24–36 months (2024) and limited OEMs raise switching costs. Asian yards handled >60% of complex projects (2024), tightening hull/newbuild availability and enabling change-order repricing. Steel/alloy premiums rose ~15–20% (2024), shifting cost risk to contractors and clients.

| Metric | 2024 |

|---|---|

| Topsides/subsea lead time | 24–36 months |

| Top Asian yard share | >60% |

| Alloy premiums | +15–20% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for MODEC, with detailed assessment of supplier and buyer power, substitutes, and competitive rivalry. Highlights disruptive threats, barriers protecting incumbents, and actionable insights for strategy and investor materials.

A compact, customizable Five Forces snapshot for MODEC—instantly highlights supplier, buyer and competitive pressures with a radar chart and clean layout ready for decks; duplicate scenarios, swap in your own data and notes, and integrate into wider reports without macros.

Customers Bargaining Power

Concentrated, sophisticated IOCs and NOCs

MODEC’s customers are concentrated IOCs and NOCs with deep technical and procurement teams that run competitive, often multi-billion-dollar tenders; individual FPSO contracts commonly exceed $1bn. They demand strict performance metrics, warranties and liquidated damages, enabling tough commercial terms and penalty regimes. Scale and procurement sophistication give customers strong bargaining power, so MODEC’s long-term relationships and execution track record are critical differentiators.

High deal size and long contract duration

As of 2024 FPSO projects are typically multi-billion-dollar commitments (commonly USD 1–3+ billion) with charter contracts of 10–20 years, concentrating buyer leverage at award and during negotiations. Clients increasingly demand turnkey EPC(I) scopes with extended warranties and availability-linked payments, shifting performance risk onto suppliers. Choice of financing (lease versus sale) materially alters pricing power and balance-sheet treatment, while robust risk allocation and transparent cost models have proven to ease negotiations.

Option of lease versus build-own-operate

In 2024 clients choosing lease consortia versus outright purchase create persistent pricing tension for MODEC. BOO and BOLease structures shift opex and uptime risk onto MODEC, prompting far tougher buyer due diligence and contract scrutiny. Buyers increasingly benchmark MODEC against peers SBM, BW and Yinson to compress margins. Flexible commercial offerings remain key to defending share.

Stringent ESG and local content demands

Operators now demand low-emission designs and high local content, tightening specs and raising compliance costs that buyers often do not fully offset; non-compliance can disqualify bids. Early ESG integration and local JV formation convert these constraints into competitive win themes, with many 2024 tenders setting local content targets above 30% and explicit 2030 emissions pathways.

Performance-based O&M terms

O&M contracts tie MODEC revenue to uptime and safety KPIs, commonly specifying 98–99.5% uptime; buyers levy liquidated damages for downtime, shifting operational risk to MODEC. Data transparency and digital monitoring increase buyer oversight and enable real-time performance deductions. Superior, consistent reliability builds client lock-in over multi-year charters, gradually reducing buyer bargaining power.

- Uptime targets: 98–99.5%

- Risk shift: liquidated damages for downtime

- Oversight: real-time digital monitoring

- Lock-in: reliability reduces buyer power

IOC/NOC FPSO tenders force turnkey risk shift, >30% local content & 98-99.5% uptime

MODEC’s buyers are concentrated IOCs/NOCs running competitive USD 1–3+bn FPSO tenders with 10–20 year charters, giving strong negotiation leverage. Clients push turnkey EPC(I), extended warranties and uptime-linked payments, shifting risk and compressing margins vs peers (SBM, BW, Yinson). 2024 tenders often require >30% local content and 98–99.5% uptime, with liquidated damages common.

| Metric | 2024 Benchmark |

|---|---|

| Typical FPSO CAPEX | USD 1–3+bn |

| Charter length | 10–20 years |

| Uptime target | 98–99.5% |

| Local content | >30% |

Preview Before You Purchase

MODEC Porter's Five Forces Analysis

This preview shows the exact MODEC Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted and ready to use. No mockups, placeholders, or partial samples; the file available for download after payment is identical to what you see here. Use it immediately for competitive assessment, strategic planning, or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

MODEC faces moderate supplier power, high capital barriers deterring new entrants, and intense rivalry among specialized offshore contractors, while buyer negotiation and substitute threats vary by project type. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to MODEC.

Suppliers Bargaining Power

Concentrated critical equipment suppliers

High-spec topsides, subsea umbilicals, turret mooring systems and gas compression packages come from a handful of OEMs, leaving limited alternatives and high switching costs for floating-FPSO contractors like MODEC. Global lead times for complex topsides and subsea packages averaged 24–36 months in 2024, raising delivery risk. Suppliers can demand firmer pricing and extended schedules in upcycles. Strategic dual-sourcing and frame agreements mitigate but do not remove supplier leverage.

Shipyards and fabrication yard capacity constraints

FPSO hull conversions and newbuilds depend on a small set of qualified Asian shipyards and global fabrication yards, with the top Asian yards handling over 60% of complex offshore projects in 2024. Tight yard slots elevate supplier power and enable repricing of change orders. When offshore cycles heat up, queue priority can carry significant premiums. Long-term partnerships and early slot reservations remain essential mitigants.

Specialist labor and engineering talent

Marine, process and offshore engineering talent is scarce and globally mobile, with 69% of employers reporting technical talent shortages in 2024 (ManpowerGroup), pushing MODEC to absorb higher labor premiums; wage inflation and retention bonuses have increased project labor costs materially. Union rules and region-specific labor regulations add scheduling and cost rigidity. MODEC’s in-house training pipelines and global mobility programs partially offset supplier power by improving retention and redeployment.

Technology licensors and IP owners

Technology licensors and IP owners (eg UOP, Axens, Shell) control critical process units like gas treatment and sulphur recovery; as of 2024 these vendors remain few, sustaining leverage over fees, performance guarantees and audit rights. Limited proven-package substitutes reinforce pricing power, while enterprise-level master agreements can compress licensing cost and contractual exposure.

- Few dominant licensors (2024)

- Licensing governs fees, guarantees, audits

- Limited substitutes = higher supplier power

- Master agreements mitigate cost and risk

Commodity and logistics volatility

Commodity and logistics volatility materially affect FPSO economics: steel and specialty-alloy costs spiked in 2024 (premium alloy premiums up ~15–20%), while long-haul heavy-lift freight tightened, shifting bargaining power to material traders and logistics providers. Price spikes and freight tightness increase pass-through risk; hedging and early procurement mitigate exposure but add procurement complexity and cash-lock. Incoterms and pass-through clauses are increasingly used to allocate cost shocks to clients.

- Steel/alloys: premiums ~15–20% (2024)

- Freight: heavy-lift tightness, spot rate uplifts

- Mitigation: hedging, early buy, incoterms/pass-through

Concentrated suppliers, lead times 24-36 months, Asian yards >60%

Suppliers of topsides, subsea packages and licensors remain concentrated, giving them strong pricing and schedule leverage; lead times 24–36 months (2024) and limited OEMs raise switching costs. Asian yards handled >60% of complex projects (2024), tightening hull/newbuild availability and enabling change-order repricing. Steel/alloy premiums rose ~15–20% (2024), shifting cost risk to contractors and clients.

| Metric | 2024 |

|---|---|

| Topsides/subsea lead time | 24–36 months |

| Top Asian yard share | >60% |

| Alloy premiums | +15–20% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for MODEC, with detailed assessment of supplier and buyer power, substitutes, and competitive rivalry. Highlights disruptive threats, barriers protecting incumbents, and actionable insights for strategy and investor materials.

A compact, customizable Five Forces snapshot for MODEC—instantly highlights supplier, buyer and competitive pressures with a radar chart and clean layout ready for decks; duplicate scenarios, swap in your own data and notes, and integrate into wider reports without macros.

Customers Bargaining Power

Concentrated, sophisticated IOCs and NOCs

MODEC’s customers are concentrated IOCs and NOCs with deep technical and procurement teams that run competitive, often multi-billion-dollar tenders; individual FPSO contracts commonly exceed $1bn. They demand strict performance metrics, warranties and liquidated damages, enabling tough commercial terms and penalty regimes. Scale and procurement sophistication give customers strong bargaining power, so MODEC’s long-term relationships and execution track record are critical differentiators.

High deal size and long contract duration

As of 2024 FPSO projects are typically multi-billion-dollar commitments (commonly USD 1–3+ billion) with charter contracts of 10–20 years, concentrating buyer leverage at award and during negotiations. Clients increasingly demand turnkey EPC(I) scopes with extended warranties and availability-linked payments, shifting performance risk onto suppliers. Choice of financing (lease versus sale) materially alters pricing power and balance-sheet treatment, while robust risk allocation and transparent cost models have proven to ease negotiations.

Option of lease versus build-own-operate

In 2024 clients choosing lease consortia versus outright purchase create persistent pricing tension for MODEC. BOO and BOLease structures shift opex and uptime risk onto MODEC, prompting far tougher buyer due diligence and contract scrutiny. Buyers increasingly benchmark MODEC against peers SBM, BW and Yinson to compress margins. Flexible commercial offerings remain key to defending share.

Stringent ESG and local content demands

Operators now demand low-emission designs and high local content, tightening specs and raising compliance costs that buyers often do not fully offset; non-compliance can disqualify bids. Early ESG integration and local JV formation convert these constraints into competitive win themes, with many 2024 tenders setting local content targets above 30% and explicit 2030 emissions pathways.

Performance-based O&M terms

O&M contracts tie MODEC revenue to uptime and safety KPIs, commonly specifying 98–99.5% uptime; buyers levy liquidated damages for downtime, shifting operational risk to MODEC. Data transparency and digital monitoring increase buyer oversight and enable real-time performance deductions. Superior, consistent reliability builds client lock-in over multi-year charters, gradually reducing buyer bargaining power.

- Uptime targets: 98–99.5%

- Risk shift: liquidated damages for downtime

- Oversight: real-time digital monitoring

- Lock-in: reliability reduces buyer power

IOC/NOC FPSO tenders force turnkey risk shift, >30% local content & 98-99.5% uptime

MODEC’s buyers are concentrated IOCs/NOCs running competitive USD 1–3+bn FPSO tenders with 10–20 year charters, giving strong negotiation leverage. Clients push turnkey EPC(I), extended warranties and uptime-linked payments, shifting risk and compressing margins vs peers (SBM, BW, Yinson). 2024 tenders often require >30% local content and 98–99.5% uptime, with liquidated damages common.

| Metric | 2024 Benchmark |

|---|---|

| Typical FPSO CAPEX | USD 1–3+bn |

| Charter length | 10–20 years |

| Uptime target | 98–99.5% |

| Local content | >30% |

Preview Before You Purchase

MODEC Porter's Five Forces Analysis

This preview shows the exact MODEC Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted and ready to use. No mockups, placeholders, or partial samples; the file available for download after payment is identical to what you see here. Use it immediately for competitive assessment, strategic planning, or investment decisions.