MODEC SWOT Analysis

Your Strategic Toolkit Starts Here

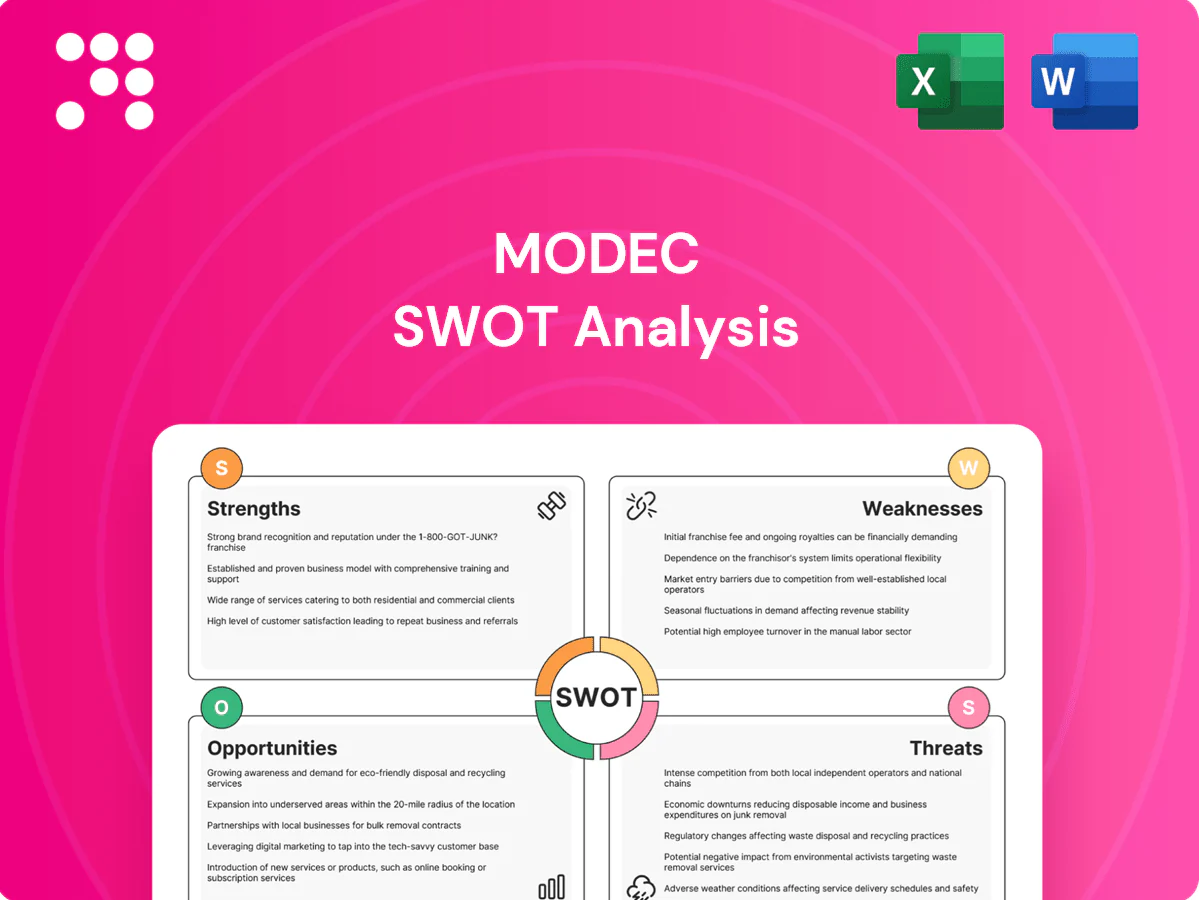

MODEC’s SWOT snapshot highlights its leading FPSO expertise, solid backlog, and offshore execution strengths, alongside exposure to oil cycle volatility and project execution risks. Want the full story behind MODEC’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis for a research-backed, editable report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

FPSO market leader

MODEC holds a top-tier position in FPSO design, build and operation, with continuous operations since 1968 and a multi-decade delivery track record that strengthens bid credibility and win rates on complex deepwater projects. Scale drives procurement leverage and learning-curve cost reductions. Strong operator references lower counterparty risk perceptions among NOCs and IOCs.

End-to-end EPCI + O&M

Integrated EPCI through lifecycle O&M delivers seamless execution and clear accountability, closing feedback loops from operations into design to boost reliability and uptime. One-stop offerings simplify client interfaces and concentrate risk allocation with a single contractual counterparty. Long-term O&M contracts, typically 10–20 years in the FPSO sector, anchor recurring revenue and support margin resilience.

Deepwater, harsh-environment expertise

MODEC (TSE:6269) differentiates with proven deepwater delivery in pre-salt Brazil and West Africa, backed by technical depth in mooring, topsides processing and turret systems that enable high throughput; proven reliability in high‑H2S and high‑pressure fields expands addressable markets, and complex FPSO contracts command premium day‑rates—often above $300,000/day in recent high-spec awards.

Long-term lease contracts

Long-term multi-year charter and O&M agreements (typically 10–20 years) give MODEC strong revenue visibility and cash-flow stability; availability-based contracts with escalation and uptime incentives support margins. Backlog of awarded projects smooths cyclicality in new awards and capex cycles, while counterparties are largely majors and NOCs, lowering receivables risk.

- Multi-year charters 10–20 years

- Availability incentives preserve margins

- Backlog smooths cycles

- Counterparties: majors/NOCs, lower credit risk

Partnerships and technology

Alliances with shipyards, OEMs and digital vendors accelerate MODEC delivery and innovation, supporting a fleet of more than 20 FPSO/FLNG projects worldwide and a multi‑billion dollar order backlog. Standardized hulls and modular topsides compress schedules—reducing build time by up to 30% and lowering CAPEX roughly 20%—while digital twins and predictive maintenance cut unplanned downtime by ~25–40%. Continuous tech upgrades align client decarbonization pathways, enabling emissions reductions through electrification and carbon management programs.

- Partnerships: fleet >20 projects, multi‑billion backlog

- Modularity: schedule −30%, CAPEX ~−20%

- Digital: downtime −25–40%

- Decarbonization: electrification & carbon management

Global FPSO leader — 20+ projects, multi-$B backlog, > $300k/day

MODEC is a global FPSO leader with 20+ projects, multi‑billion backlog, and decades of continuous operation, delivering premium day‑rates (often > $300k/day). Integrated EPCI+O&M yields recurring 10–20yr revenue, availability incentives protect margins, and modular design cuts build time ~30%.

| Metric | Value |

|---|---|

| Fleet / Backlog | 20+ / multi‑$B |

What is included in the product

Provides a concise SWOT analysis of MODEC, highlighting operational and technological strengths, key weaknesses, growth opportunities in offshore energy and decommissioning, and external threats from market volatility, regulatory shifts, and intensifying competition.

Provides a clear, company-specific SWOT matrix that simplifies MODEC’s risk and opportunity assessment, enabling rapid alignment across teams and faster stakeholder decision-making.

Weaknesses

Capital intensity

Capital intensity: FPSO projects require heavy upfront capex (new-builds commonly $700M–$1.5B) and complex financing. MODEC’s balance-sheet exposure can limit bid capacity in peak cycles as project commitments accumulate; award-to-FID timelines often stretch 18–36 months. Global rate hikes (US fed funds ~5.25–5.50% in 2024–25) raise hurdle rates and compress project IRRs.

Project concentration

Revenues can be concentrated in a handful of mega-projects and clients, with individual FPSO/FLNG contracts often exceeding $1bn, so delays or disputes on a single asset can materially hit cash flows and working capital. Geographic and client concentration amplifies political and counterparty risk, notably in high-risk basins. Portfolio diversification is structurally difficult in the niche FPSO market, where delivery cycles average 36–48 months (2024 industry data).

Execution risk

MODEC’s large EPCI scope concentrates schedule, cost and interface risk, with its 2024 order backlog around $10bn increasing exposure to multi-year delivery challenges. Supply-chain bottlenecks and yard congestion have led to liquidated damages on industry peers and could trigger similar LDs for MODEC. Technical integration of high-spec topsides elevates commissioning complexity and testing demands. Warranty and performance obligations compress margins on long-term FPSO contracts.

Cyclic award pipeline

MODEC faces a cyclic award pipeline: sanctioning hinges on oil and gas price outlooks and operator capex, and downturns can freeze new FPSO awards—backlogs thinned after the 2020–21 slump and only began recovering into 2023. Tendering is lengthy and resource-intensive with uncertain conversion, and competitive pricing in slow cycles compresses returns and margins.

- Sanction sensitivity: operator capex drives timing

- Backlog volatility: freezes in downturns thin order book

- Long, costly tenders with low conversion

- Price competition in slow cycles compresses returns

ESG perception gap

Association with hydrocarbons limits MODEC's appeal to sustainability-focused investors and lenders, especially as GFANZ members and other net-zero-aligned institutions collectively influence roughly $150 trillion in capital. Stricter ESG screens push tougher financing terms and can raise cost of capital for oil-and-gas-linked contractors. Public scrutiny of emissions and spill risks elevates reputational exposure, while MODEC's transition narrative trails pure-play renewables peers.

- Investor access: constrained vs net-zero capital (~$150T influence)

- Financing: stricter ESG screens → higher cost/conditions

- Reputation: emissions/spill scrutiny increases risk

- Positioning: transition narrative lags renewables peers

High capex, long delivery cycles, concentrated backlog and rate/ESG-driven financing squeeze

High upfront capex ($700M–$1.5B per new-build) and balance-sheet exposure limit bid capacity; award-to-FID often 18–36 months while delivery cycles run 36–48 months. Backlog concentration (~$10bn in 2024) and client/geographic concentration amplify counterparty and political risk. Rate hikes (US fed funds ~5.25–5.50% in 2024–25) and ESG-driven capital shifts (~$150T GFANZ influence) raise financing costs and constrain investor access.

| Metric | 2024–25 figure |

|---|---|

| New-build capex | $700M–$1.5B |

| Order backlog | ~$10bn (2024) |

| Delivery cycle | 36–48 months |

| Fed funds rate | 5.25–5.50% |

| Net-zero capital influence | ~$150T (GFANZ) |

Full Version Awaits

MODEC SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable version immediately after checkout.

Your Strategic Toolkit Starts Here

MODEC’s SWOT snapshot highlights its leading FPSO expertise, solid backlog, and offshore execution strengths, alongside exposure to oil cycle volatility and project execution risks. Want the full story behind MODEC’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis for a research-backed, editable report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

FPSO market leader

MODEC holds a top-tier position in FPSO design, build and operation, with continuous operations since 1968 and a multi-decade delivery track record that strengthens bid credibility and win rates on complex deepwater projects. Scale drives procurement leverage and learning-curve cost reductions. Strong operator references lower counterparty risk perceptions among NOCs and IOCs.

End-to-end EPCI + O&M

Integrated EPCI through lifecycle O&M delivers seamless execution and clear accountability, closing feedback loops from operations into design to boost reliability and uptime. One-stop offerings simplify client interfaces and concentrate risk allocation with a single contractual counterparty. Long-term O&M contracts, typically 10–20 years in the FPSO sector, anchor recurring revenue and support margin resilience.

Deepwater, harsh-environment expertise

MODEC (TSE:6269) differentiates with proven deepwater delivery in pre-salt Brazil and West Africa, backed by technical depth in mooring, topsides processing and turret systems that enable high throughput; proven reliability in high‑H2S and high‑pressure fields expands addressable markets, and complex FPSO contracts command premium day‑rates—often above $300,000/day in recent high-spec awards.

Long-term lease contracts

Long-term multi-year charter and O&M agreements (typically 10–20 years) give MODEC strong revenue visibility and cash-flow stability; availability-based contracts with escalation and uptime incentives support margins. Backlog of awarded projects smooths cyclicality in new awards and capex cycles, while counterparties are largely majors and NOCs, lowering receivables risk.

- Multi-year charters 10–20 years

- Availability incentives preserve margins

- Backlog smooths cycles

- Counterparties: majors/NOCs, lower credit risk

Partnerships and technology

Alliances with shipyards, OEMs and digital vendors accelerate MODEC delivery and innovation, supporting a fleet of more than 20 FPSO/FLNG projects worldwide and a multi‑billion dollar order backlog. Standardized hulls and modular topsides compress schedules—reducing build time by up to 30% and lowering CAPEX roughly 20%—while digital twins and predictive maintenance cut unplanned downtime by ~25–40%. Continuous tech upgrades align client decarbonization pathways, enabling emissions reductions through electrification and carbon management programs.

- Partnerships: fleet >20 projects, multi‑billion backlog

- Modularity: schedule −30%, CAPEX ~−20%

- Digital: downtime −25–40%

- Decarbonization: electrification & carbon management

Global FPSO leader — 20+ projects, multi-$B backlog, > $300k/day

MODEC is a global FPSO leader with 20+ projects, multi‑billion backlog, and decades of continuous operation, delivering premium day‑rates (often > $300k/day). Integrated EPCI+O&M yields recurring 10–20yr revenue, availability incentives protect margins, and modular design cuts build time ~30%.

| Metric | Value |

|---|---|

| Fleet / Backlog | 20+ / multi‑$B |

What is included in the product

Provides a concise SWOT analysis of MODEC, highlighting operational and technological strengths, key weaknesses, growth opportunities in offshore energy and decommissioning, and external threats from market volatility, regulatory shifts, and intensifying competition.

Provides a clear, company-specific SWOT matrix that simplifies MODEC’s risk and opportunity assessment, enabling rapid alignment across teams and faster stakeholder decision-making.

Weaknesses

Capital intensity

Capital intensity: FPSO projects require heavy upfront capex (new-builds commonly $700M–$1.5B) and complex financing. MODEC’s balance-sheet exposure can limit bid capacity in peak cycles as project commitments accumulate; award-to-FID timelines often stretch 18–36 months. Global rate hikes (US fed funds ~5.25–5.50% in 2024–25) raise hurdle rates and compress project IRRs.

Project concentration

Revenues can be concentrated in a handful of mega-projects and clients, with individual FPSO/FLNG contracts often exceeding $1bn, so delays or disputes on a single asset can materially hit cash flows and working capital. Geographic and client concentration amplifies political and counterparty risk, notably in high-risk basins. Portfolio diversification is structurally difficult in the niche FPSO market, where delivery cycles average 36–48 months (2024 industry data).

Execution risk

MODEC’s large EPCI scope concentrates schedule, cost and interface risk, with its 2024 order backlog around $10bn increasing exposure to multi-year delivery challenges. Supply-chain bottlenecks and yard congestion have led to liquidated damages on industry peers and could trigger similar LDs for MODEC. Technical integration of high-spec topsides elevates commissioning complexity and testing demands. Warranty and performance obligations compress margins on long-term FPSO contracts.

Cyclic award pipeline

MODEC faces a cyclic award pipeline: sanctioning hinges on oil and gas price outlooks and operator capex, and downturns can freeze new FPSO awards—backlogs thinned after the 2020–21 slump and only began recovering into 2023. Tendering is lengthy and resource-intensive with uncertain conversion, and competitive pricing in slow cycles compresses returns and margins.

- Sanction sensitivity: operator capex drives timing

- Backlog volatility: freezes in downturns thin order book

- Long, costly tenders with low conversion

- Price competition in slow cycles compresses returns

ESG perception gap

Association with hydrocarbons limits MODEC's appeal to sustainability-focused investors and lenders, especially as GFANZ members and other net-zero-aligned institutions collectively influence roughly $150 trillion in capital. Stricter ESG screens push tougher financing terms and can raise cost of capital for oil-and-gas-linked contractors. Public scrutiny of emissions and spill risks elevates reputational exposure, while MODEC's transition narrative trails pure-play renewables peers.

- Investor access: constrained vs net-zero capital (~$150T influence)

- Financing: stricter ESG screens → higher cost/conditions

- Reputation: emissions/spill scrutiny increases risk

- Positioning: transition narrative lags renewables peers

High capex, long delivery cycles, concentrated backlog and rate/ESG-driven financing squeeze

High upfront capex ($700M–$1.5B per new-build) and balance-sheet exposure limit bid capacity; award-to-FID often 18–36 months while delivery cycles run 36–48 months. Backlog concentration (~$10bn in 2024) and client/geographic concentration amplify counterparty and political risk. Rate hikes (US fed funds ~5.25–5.50% in 2024–25) and ESG-driven capital shifts (~$150T GFANZ influence) raise financing costs and constrain investor access.

| Metric | 2024–25 figure |

|---|---|

| New-build capex | $700M–$1.5B |

| Order backlog | ~$10bn (2024) |

| Delivery cycle | 36–48 months |

| Fed funds rate | 5.25–5.50% |

| Net-zero capital influence | ~$150T (GFANZ) |

Full Version Awaits

MODEC SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

MODEC’s SWOT snapshot highlights its leading FPSO expertise, solid backlog, and offshore execution strengths, alongside exposure to oil cycle volatility and project execution risks. Want the full story behind MODEC’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis for a research-backed, editable report and Excel matrix to plan, pitch, or invest with confidence.

Strengths

FPSO market leader

MODEC holds a top-tier position in FPSO design, build and operation, with continuous operations since 1968 and a multi-decade delivery track record that strengthens bid credibility and win rates on complex deepwater projects. Scale drives procurement leverage and learning-curve cost reductions. Strong operator references lower counterparty risk perceptions among NOCs and IOCs.

End-to-end EPCI + O&M

Integrated EPCI through lifecycle O&M delivers seamless execution and clear accountability, closing feedback loops from operations into design to boost reliability and uptime. One-stop offerings simplify client interfaces and concentrate risk allocation with a single contractual counterparty. Long-term O&M contracts, typically 10–20 years in the FPSO sector, anchor recurring revenue and support margin resilience.

Deepwater, harsh-environment expertise

MODEC (TSE:6269) differentiates with proven deepwater delivery in pre-salt Brazil and West Africa, backed by technical depth in mooring, topsides processing and turret systems that enable high throughput; proven reliability in high‑H2S and high‑pressure fields expands addressable markets, and complex FPSO contracts command premium day‑rates—often above $300,000/day in recent high-spec awards.

Long-term lease contracts

Long-term multi-year charter and O&M agreements (typically 10–20 years) give MODEC strong revenue visibility and cash-flow stability; availability-based contracts with escalation and uptime incentives support margins. Backlog of awarded projects smooths cyclicality in new awards and capex cycles, while counterparties are largely majors and NOCs, lowering receivables risk.

- Multi-year charters 10–20 years

- Availability incentives preserve margins

- Backlog smooths cycles

- Counterparties: majors/NOCs, lower credit risk

Partnerships and technology

Alliances with shipyards, OEMs and digital vendors accelerate MODEC delivery and innovation, supporting a fleet of more than 20 FPSO/FLNG projects worldwide and a multi‑billion dollar order backlog. Standardized hulls and modular topsides compress schedules—reducing build time by up to 30% and lowering CAPEX roughly 20%—while digital twins and predictive maintenance cut unplanned downtime by ~25–40%. Continuous tech upgrades align client decarbonization pathways, enabling emissions reductions through electrification and carbon management programs.

- Partnerships: fleet >20 projects, multi‑billion backlog

- Modularity: schedule −30%, CAPEX ~−20%

- Digital: downtime −25–40%

- Decarbonization: electrification & carbon management

Global FPSO leader — 20+ projects, multi-$B backlog, > $300k/day

MODEC is a global FPSO leader with 20+ projects, multi‑billion backlog, and decades of continuous operation, delivering premium day‑rates (often > $300k/day). Integrated EPCI+O&M yields recurring 10–20yr revenue, availability incentives protect margins, and modular design cuts build time ~30%.

| Metric | Value |

|---|---|

| Fleet / Backlog | 20+ / multi‑$B |

What is included in the product

Provides a concise SWOT analysis of MODEC, highlighting operational and technological strengths, key weaknesses, growth opportunities in offshore energy and decommissioning, and external threats from market volatility, regulatory shifts, and intensifying competition.

Provides a clear, company-specific SWOT matrix that simplifies MODEC’s risk and opportunity assessment, enabling rapid alignment across teams and faster stakeholder decision-making.

Weaknesses

Capital intensity

Capital intensity: FPSO projects require heavy upfront capex (new-builds commonly $700M–$1.5B) and complex financing. MODEC’s balance-sheet exposure can limit bid capacity in peak cycles as project commitments accumulate; award-to-FID timelines often stretch 18–36 months. Global rate hikes (US fed funds ~5.25–5.50% in 2024–25) raise hurdle rates and compress project IRRs.

Project concentration

Revenues can be concentrated in a handful of mega-projects and clients, with individual FPSO/FLNG contracts often exceeding $1bn, so delays or disputes on a single asset can materially hit cash flows and working capital. Geographic and client concentration amplifies political and counterparty risk, notably in high-risk basins. Portfolio diversification is structurally difficult in the niche FPSO market, where delivery cycles average 36–48 months (2024 industry data).

Execution risk

MODEC’s large EPCI scope concentrates schedule, cost and interface risk, with its 2024 order backlog around $10bn increasing exposure to multi-year delivery challenges. Supply-chain bottlenecks and yard congestion have led to liquidated damages on industry peers and could trigger similar LDs for MODEC. Technical integration of high-spec topsides elevates commissioning complexity and testing demands. Warranty and performance obligations compress margins on long-term FPSO contracts.

Cyclic award pipeline

MODEC faces a cyclic award pipeline: sanctioning hinges on oil and gas price outlooks and operator capex, and downturns can freeze new FPSO awards—backlogs thinned after the 2020–21 slump and only began recovering into 2023. Tendering is lengthy and resource-intensive with uncertain conversion, and competitive pricing in slow cycles compresses returns and margins.

- Sanction sensitivity: operator capex drives timing

- Backlog volatility: freezes in downturns thin order book

- Long, costly tenders with low conversion

- Price competition in slow cycles compresses returns

ESG perception gap

Association with hydrocarbons limits MODEC's appeal to sustainability-focused investors and lenders, especially as GFANZ members and other net-zero-aligned institutions collectively influence roughly $150 trillion in capital. Stricter ESG screens push tougher financing terms and can raise cost of capital for oil-and-gas-linked contractors. Public scrutiny of emissions and spill risks elevates reputational exposure, while MODEC's transition narrative trails pure-play renewables peers.

- Investor access: constrained vs net-zero capital (~$150T influence)

- Financing: stricter ESG screens → higher cost/conditions

- Reputation: emissions/spill scrutiny increases risk

- Positioning: transition narrative lags renewables peers

High capex, long delivery cycles, concentrated backlog and rate/ESG-driven financing squeeze

High upfront capex ($700M–$1.5B per new-build) and balance-sheet exposure limit bid capacity; award-to-FID often 18–36 months while delivery cycles run 36–48 months. Backlog concentration (~$10bn in 2024) and client/geographic concentration amplify counterparty and political risk. Rate hikes (US fed funds ~5.25–5.50% in 2024–25) and ESG-driven capital shifts (~$150T GFANZ influence) raise financing costs and constrain investor access.

| Metric | 2024–25 figure |

|---|---|

| New-build capex | $700M–$1.5B |

| Order backlog | ~$10bn (2024) |

| Delivery cycle | 36–48 months |

| Fed funds rate | 5.25–5.50% |

| Net-zero capital influence | ~$150T (GFANZ) |

Full Version Awaits

MODEC SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable version immediately after checkout.