ModivCare SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Explore ModivCare’s strategic posture with our concise SWOT preview and see how operational scale, payer relationships, and regulatory exposure shape its outlook. The full SWOT delivers in-depth, research-backed analysis, financial context, and actionable recommendations. Ideal for investors, advisors, and operators seeking clarity. Purchase the complete report for editable Word and Excel deliverables to plan with confidence.

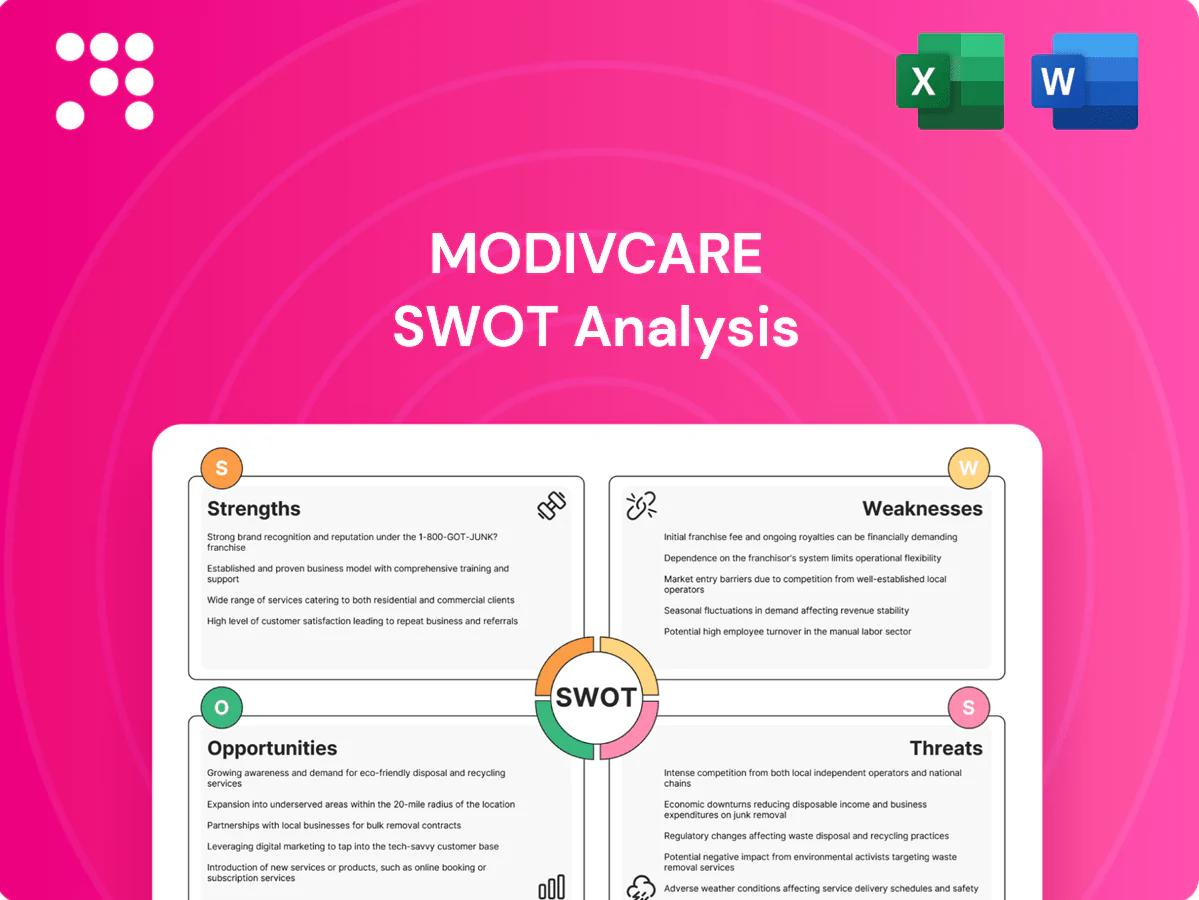

Strengths

Integrated supportive care platform

ModivCare combines NEMT, personal care, and remote monitoring into a coordinated offering that simplifies care delivery and, per company disclosures, serves millions of members across the US. This integration closes gaps between appointments, in-home support, and monitoring, strengthening data continuity and care coordination. The unified platform has driven improved patient adherence and measurable outcome gains in client programs, supporting utilization and retention metrics.

Deep payer and government relationships

Longstanding ties with Medicaid, Medicare Advantage and managed care organizations give ModivCare stable demand, tapping payer markets that cover over 100 million beneficiaries (CMS, 2024). Contracted networks provide visibility into volumes and pricing, supporting predictable revenue and lower customer acquisition costs. Multi-year agreements and payer trust enable pilot programs and transition to value-based payment structures, reducing churn and increasing lifetime value.

Technology-enabled logistics and analytics

Routing, scheduling and real-time monitoring boost NEMT utilization and on-time rates, with ModivCare’s tech underpinning its approximately $1.45 billion 2023 revenue. Data insights reduce no-shows and unnecessary ER visits, and analytics quantify payer cost savings to reinforce renewals. The platform scales rapidly across fragmented local markets, improving coverage and margin leverage.

Diversified revenue across service lines

- Reduces single-pool reliance

- Boosts customer lifetime value

- Buffers segment churn

- Enables higher-margin bundles

Outcomes and cost-reduction track record

ModivCare's documented outcomes—company-reported reductions in missed appointments and avoidable utilization of roughly 20–25%—translate into lower total cost of care and strengthen ROI cases for payers. Outcome metrics support risk-sharing and performance incentives, enabling ModivCare to cite over $100 million in annualized client savings in recent filings through 2023–2024. This performance positions the company strongly in value-based procurement.

- 20–25% reductions in avoidable utilization

- >$100M annualized client savings (2023–2024)

- Supports risk-sharing and value-based contracts

Integrated care saves >$100M, cuts avoidable use 20–25% across >100M

Integrated NEMT, RPM, pharmacy and behavioral services drive coordinated care, supporting improved adherence and retention across millions of members.

Strong payor relationships (Medicaid/MA reach >100M beneficiaries) and multi-year contracts underpin predictable revenue (≈$1.45B 2023; ≈$1.1B 2024).

Documented 20–25% reductions in avoidable utilization and >$100M annualized client savings bolster value-based contracting.

| Metric | 2023 | 2024 |

|---|---|---|

| Revenue | $1.45B | $1.1B |

| Beneficiary reach | >100M (CMS) | |

| Client savings | >$100M | |

| Avoidable utilization | 20–25% | |

What is included in the product

Provides a concise SWOT analysis of ModivCare, highlighting its operational strengths, financial and strategic weaknesses, growth opportunities in value-based care and technology, and external threats from regulatory changes, reimbursement risk, and competitive pressures.

Provides a concise ModivCare SWOT matrix that quickly highlights care-network strengths, operational risks, and market opportunities to streamline strategic alignment and decision-making.

Weaknesses

Thin margins in labor-heavy operations

NEMT and personal care depend on large frontline workforces and subcontractors, and wage inflation — BLS reported average hourly earnings rose about 4% year-over-year in 2024 — plus overtime compress margins. Regulated Medicaid contracts offer limited pricing power and few pass-through mechanisms, constraining the ability to recover labor cost increases. Thin margins make the business highly sensitive to execution missteps and cost overruns.

Dependence on public reimbursement

ModivCare’s dependence on public reimbursement leaves more than three quarters of net revenue tied to Medicaid and other government payors, exposing the company to policy-driven volatility. State budget cycles and annual rate resets have historically compressed margins, with several states implementing 3–6% temporary rate adjustments in recent budget rounds. Administrative approvals and claims processing delays routinely extend payment timelines by weeks to months, straining cash flow. Management must continually adapt contracts and operations to shifting statutory and regulatory requirements across 50 states.

Operational complexity and variability

Operating across multiple states exposes ModivCare to differing Medicaid rules, network requirements and service standards, making uniform quality control difficult. Daily variability in dispatch, driver availability and member acuity increases operational volatility and service-risk. This geographic and temporal complexity elevates oversight and compliance costs and complicates consistent care delivery.

Integration and system harmonization risks

ModivCare (NASDAQ: MODV) faces integration and system harmonization risks as acquisitions and new product layers require significant IT and process integration; disparate platforms can impede data flow and reporting and harmonization consumes capital and management bandwidth, delaying synergy capture and cross-selling.

- MODV ticker noted

- Acquisitions increase integration scope

- Disparate platforms hinder reporting

- Harmonization ties up capital and management

- Delays slow synergies and cross-sell

Customer service and brand perception issues

Customer service lapses in NEMT, such as late pickups or cancellations, erode member satisfaction and can quickly escalate via social and regulatory channels, harming ModivCare’s brand and payer relationships. Declines in service risk contract renewals and negatively affect payer quality metrics and star ratings, prompting costly remediation. Addressing this requires sustained investment in QA, driver training, and real-time performance monitoring.

- Late pickups/cancellations harm satisfaction

- Negative incidents amplify via social/regulatory channels

- Service dips threaten renewals and star ratings

- Remediation needs QA, training, tech investment

Medicaid-heavy NEMT: ~4% wage inflation and ±3–6% state rate shifts squeeze margins

Heavy reliance on large frontline workforces with BLS 2024 wage growth ~4% compresses margins; over 75% of net revenue tied to Medicaid limits pricing power and exposes ModivCare (MODV) to 3–6% state rate adjustments and policy volatility; multistate compliance and IT integration risks raise costs; NEMT service lapses threaten star ratings and contract renewals.

| Weakness | Metric/Value |

|---|---|

| Medicaid exposure | >75% revenue |

| Wage inflation | BLS 2024: ~4% YoY |

| State rate shifts | Temporary ±3–6% |

| Claims delays | Weeks–months |

Preview the Actual Deliverable

ModivCare SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version is unlocked after payment. Purchase now to download the entire, ready-to-use file.

Dive Deeper Into the Company’s Strategic Blueprint

Explore ModivCare’s strategic posture with our concise SWOT preview and see how operational scale, payer relationships, and regulatory exposure shape its outlook. The full SWOT delivers in-depth, research-backed analysis, financial context, and actionable recommendations. Ideal for investors, advisors, and operators seeking clarity. Purchase the complete report for editable Word and Excel deliverables to plan with confidence.

Strengths

Integrated supportive care platform

ModivCare combines NEMT, personal care, and remote monitoring into a coordinated offering that simplifies care delivery and, per company disclosures, serves millions of members across the US. This integration closes gaps between appointments, in-home support, and monitoring, strengthening data continuity and care coordination. The unified platform has driven improved patient adherence and measurable outcome gains in client programs, supporting utilization and retention metrics.

Deep payer and government relationships

Longstanding ties with Medicaid, Medicare Advantage and managed care organizations give ModivCare stable demand, tapping payer markets that cover over 100 million beneficiaries (CMS, 2024). Contracted networks provide visibility into volumes and pricing, supporting predictable revenue and lower customer acquisition costs. Multi-year agreements and payer trust enable pilot programs and transition to value-based payment structures, reducing churn and increasing lifetime value.

Technology-enabled logistics and analytics

Routing, scheduling and real-time monitoring boost NEMT utilization and on-time rates, with ModivCare’s tech underpinning its approximately $1.45 billion 2023 revenue. Data insights reduce no-shows and unnecessary ER visits, and analytics quantify payer cost savings to reinforce renewals. The platform scales rapidly across fragmented local markets, improving coverage and margin leverage.

Diversified revenue across service lines

- Reduces single-pool reliance

- Boosts customer lifetime value

- Buffers segment churn

- Enables higher-margin bundles

Outcomes and cost-reduction track record

ModivCare's documented outcomes—company-reported reductions in missed appointments and avoidable utilization of roughly 20–25%—translate into lower total cost of care and strengthen ROI cases for payers. Outcome metrics support risk-sharing and performance incentives, enabling ModivCare to cite over $100 million in annualized client savings in recent filings through 2023–2024. This performance positions the company strongly in value-based procurement.

- 20–25% reductions in avoidable utilization

- >$100M annualized client savings (2023–2024)

- Supports risk-sharing and value-based contracts

Integrated care saves >$100M, cuts avoidable use 20–25% across >100M

Integrated NEMT, RPM, pharmacy and behavioral services drive coordinated care, supporting improved adherence and retention across millions of members.

Strong payor relationships (Medicaid/MA reach >100M beneficiaries) and multi-year contracts underpin predictable revenue (≈$1.45B 2023; ≈$1.1B 2024).

Documented 20–25% reductions in avoidable utilization and >$100M annualized client savings bolster value-based contracting.

| Metric | 2023 | 2024 |

|---|---|---|

| Revenue | $1.45B | $1.1B |

| Beneficiary reach | >100M (CMS) | |

| Client savings | >$100M | |

| Avoidable utilization | 20–25% | |

What is included in the product

Provides a concise SWOT analysis of ModivCare, highlighting its operational strengths, financial and strategic weaknesses, growth opportunities in value-based care and technology, and external threats from regulatory changes, reimbursement risk, and competitive pressures.

Provides a concise ModivCare SWOT matrix that quickly highlights care-network strengths, operational risks, and market opportunities to streamline strategic alignment and decision-making.

Weaknesses

Thin margins in labor-heavy operations

NEMT and personal care depend on large frontline workforces and subcontractors, and wage inflation — BLS reported average hourly earnings rose about 4% year-over-year in 2024 — plus overtime compress margins. Regulated Medicaid contracts offer limited pricing power and few pass-through mechanisms, constraining the ability to recover labor cost increases. Thin margins make the business highly sensitive to execution missteps and cost overruns.

Dependence on public reimbursement

ModivCare’s dependence on public reimbursement leaves more than three quarters of net revenue tied to Medicaid and other government payors, exposing the company to policy-driven volatility. State budget cycles and annual rate resets have historically compressed margins, with several states implementing 3–6% temporary rate adjustments in recent budget rounds. Administrative approvals and claims processing delays routinely extend payment timelines by weeks to months, straining cash flow. Management must continually adapt contracts and operations to shifting statutory and regulatory requirements across 50 states.

Operational complexity and variability

Operating across multiple states exposes ModivCare to differing Medicaid rules, network requirements and service standards, making uniform quality control difficult. Daily variability in dispatch, driver availability and member acuity increases operational volatility and service-risk. This geographic and temporal complexity elevates oversight and compliance costs and complicates consistent care delivery.

Integration and system harmonization risks

ModivCare (NASDAQ: MODV) faces integration and system harmonization risks as acquisitions and new product layers require significant IT and process integration; disparate platforms can impede data flow and reporting and harmonization consumes capital and management bandwidth, delaying synergy capture and cross-selling.

- MODV ticker noted

- Acquisitions increase integration scope

- Disparate platforms hinder reporting

- Harmonization ties up capital and management

- Delays slow synergies and cross-sell

Customer service and brand perception issues

Customer service lapses in NEMT, such as late pickups or cancellations, erode member satisfaction and can quickly escalate via social and regulatory channels, harming ModivCare’s brand and payer relationships. Declines in service risk contract renewals and negatively affect payer quality metrics and star ratings, prompting costly remediation. Addressing this requires sustained investment in QA, driver training, and real-time performance monitoring.

- Late pickups/cancellations harm satisfaction

- Negative incidents amplify via social/regulatory channels

- Service dips threaten renewals and star ratings

- Remediation needs QA, training, tech investment

Medicaid-heavy NEMT: ~4% wage inflation and ±3–6% state rate shifts squeeze margins

Heavy reliance on large frontline workforces with BLS 2024 wage growth ~4% compresses margins; over 75% of net revenue tied to Medicaid limits pricing power and exposes ModivCare (MODV) to 3–6% state rate adjustments and policy volatility; multistate compliance and IT integration risks raise costs; NEMT service lapses threaten star ratings and contract renewals.

| Weakness | Metric/Value |

|---|---|

| Medicaid exposure | >75% revenue |

| Wage inflation | BLS 2024: ~4% YoY |

| State rate shifts | Temporary ±3–6% |

| Claims delays | Weeks–months |

Preview the Actual Deliverable

ModivCare SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version is unlocked after payment. Purchase now to download the entire, ready-to-use file.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Explore ModivCare’s strategic posture with our concise SWOT preview and see how operational scale, payer relationships, and regulatory exposure shape its outlook. The full SWOT delivers in-depth, research-backed analysis, financial context, and actionable recommendations. Ideal for investors, advisors, and operators seeking clarity. Purchase the complete report for editable Word and Excel deliverables to plan with confidence.

Strengths

Integrated supportive care platform

ModivCare combines NEMT, personal care, and remote monitoring into a coordinated offering that simplifies care delivery and, per company disclosures, serves millions of members across the US. This integration closes gaps between appointments, in-home support, and monitoring, strengthening data continuity and care coordination. The unified platform has driven improved patient adherence and measurable outcome gains in client programs, supporting utilization and retention metrics.

Deep payer and government relationships

Longstanding ties with Medicaid, Medicare Advantage and managed care organizations give ModivCare stable demand, tapping payer markets that cover over 100 million beneficiaries (CMS, 2024). Contracted networks provide visibility into volumes and pricing, supporting predictable revenue and lower customer acquisition costs. Multi-year agreements and payer trust enable pilot programs and transition to value-based payment structures, reducing churn and increasing lifetime value.

Technology-enabled logistics and analytics

Routing, scheduling and real-time monitoring boost NEMT utilization and on-time rates, with ModivCare’s tech underpinning its approximately $1.45 billion 2023 revenue. Data insights reduce no-shows and unnecessary ER visits, and analytics quantify payer cost savings to reinforce renewals. The platform scales rapidly across fragmented local markets, improving coverage and margin leverage.

Diversified revenue across service lines

- Reduces single-pool reliance

- Boosts customer lifetime value

- Buffers segment churn

- Enables higher-margin bundles

Outcomes and cost-reduction track record

ModivCare's documented outcomes—company-reported reductions in missed appointments and avoidable utilization of roughly 20–25%—translate into lower total cost of care and strengthen ROI cases for payers. Outcome metrics support risk-sharing and performance incentives, enabling ModivCare to cite over $100 million in annualized client savings in recent filings through 2023–2024. This performance positions the company strongly in value-based procurement.

- 20–25% reductions in avoidable utilization

- >$100M annualized client savings (2023–2024)

- Supports risk-sharing and value-based contracts

Integrated care saves >$100M, cuts avoidable use 20–25% across >100M

Integrated NEMT, RPM, pharmacy and behavioral services drive coordinated care, supporting improved adherence and retention across millions of members.

Strong payor relationships (Medicaid/MA reach >100M beneficiaries) and multi-year contracts underpin predictable revenue (≈$1.45B 2023; ≈$1.1B 2024).

Documented 20–25% reductions in avoidable utilization and >$100M annualized client savings bolster value-based contracting.

| Metric | 2023 | 2024 |

|---|---|---|

| Revenue | $1.45B | $1.1B |

| Beneficiary reach | >100M (CMS) | |

| Client savings | >$100M | |

| Avoidable utilization | 20–25% | |

What is included in the product

Provides a concise SWOT analysis of ModivCare, highlighting its operational strengths, financial and strategic weaknesses, growth opportunities in value-based care and technology, and external threats from regulatory changes, reimbursement risk, and competitive pressures.

Provides a concise ModivCare SWOT matrix that quickly highlights care-network strengths, operational risks, and market opportunities to streamline strategic alignment and decision-making.

Weaknesses

Thin margins in labor-heavy operations

NEMT and personal care depend on large frontline workforces and subcontractors, and wage inflation — BLS reported average hourly earnings rose about 4% year-over-year in 2024 — plus overtime compress margins. Regulated Medicaid contracts offer limited pricing power and few pass-through mechanisms, constraining the ability to recover labor cost increases. Thin margins make the business highly sensitive to execution missteps and cost overruns.

Dependence on public reimbursement

ModivCare’s dependence on public reimbursement leaves more than three quarters of net revenue tied to Medicaid and other government payors, exposing the company to policy-driven volatility. State budget cycles and annual rate resets have historically compressed margins, with several states implementing 3–6% temporary rate adjustments in recent budget rounds. Administrative approvals and claims processing delays routinely extend payment timelines by weeks to months, straining cash flow. Management must continually adapt contracts and operations to shifting statutory and regulatory requirements across 50 states.

Operational complexity and variability

Operating across multiple states exposes ModivCare to differing Medicaid rules, network requirements and service standards, making uniform quality control difficult. Daily variability in dispatch, driver availability and member acuity increases operational volatility and service-risk. This geographic and temporal complexity elevates oversight and compliance costs and complicates consistent care delivery.

Integration and system harmonization risks

ModivCare (NASDAQ: MODV) faces integration and system harmonization risks as acquisitions and new product layers require significant IT and process integration; disparate platforms can impede data flow and reporting and harmonization consumes capital and management bandwidth, delaying synergy capture and cross-selling.

- MODV ticker noted

- Acquisitions increase integration scope

- Disparate platforms hinder reporting

- Harmonization ties up capital and management

- Delays slow synergies and cross-sell

Customer service and brand perception issues

Customer service lapses in NEMT, such as late pickups or cancellations, erode member satisfaction and can quickly escalate via social and regulatory channels, harming ModivCare’s brand and payer relationships. Declines in service risk contract renewals and negatively affect payer quality metrics and star ratings, prompting costly remediation. Addressing this requires sustained investment in QA, driver training, and real-time performance monitoring.

- Late pickups/cancellations harm satisfaction

- Negative incidents amplify via social/regulatory channels

- Service dips threaten renewals and star ratings

- Remediation needs QA, training, tech investment

Medicaid-heavy NEMT: ~4% wage inflation and ±3–6% state rate shifts squeeze margins

Heavy reliance on large frontline workforces with BLS 2024 wage growth ~4% compresses margins; over 75% of net revenue tied to Medicaid limits pricing power and exposes ModivCare (MODV) to 3–6% state rate adjustments and policy volatility; multistate compliance and IT integration risks raise costs; NEMT service lapses threaten star ratings and contract renewals.

| Weakness | Metric/Value |

|---|---|

| Medicaid exposure | >75% revenue |

| Wage inflation | BLS 2024: ~4% YoY |

| State rate shifts | Temporary ±3–6% |

| Claims delays | Weeks–months |

Preview the Actual Deliverable

ModivCare SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version is unlocked after payment. Purchase now to download the entire, ready-to-use file.