Mohawk Industries PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, and sustainability trends are reshaping Mohawk Industries and where opportunities and risks lie; our concise PESTLE pinpoints implications for strategy and valuation. Purchase the full analysis to access actionable insights, data tables, and downloadable templates for immediate use.

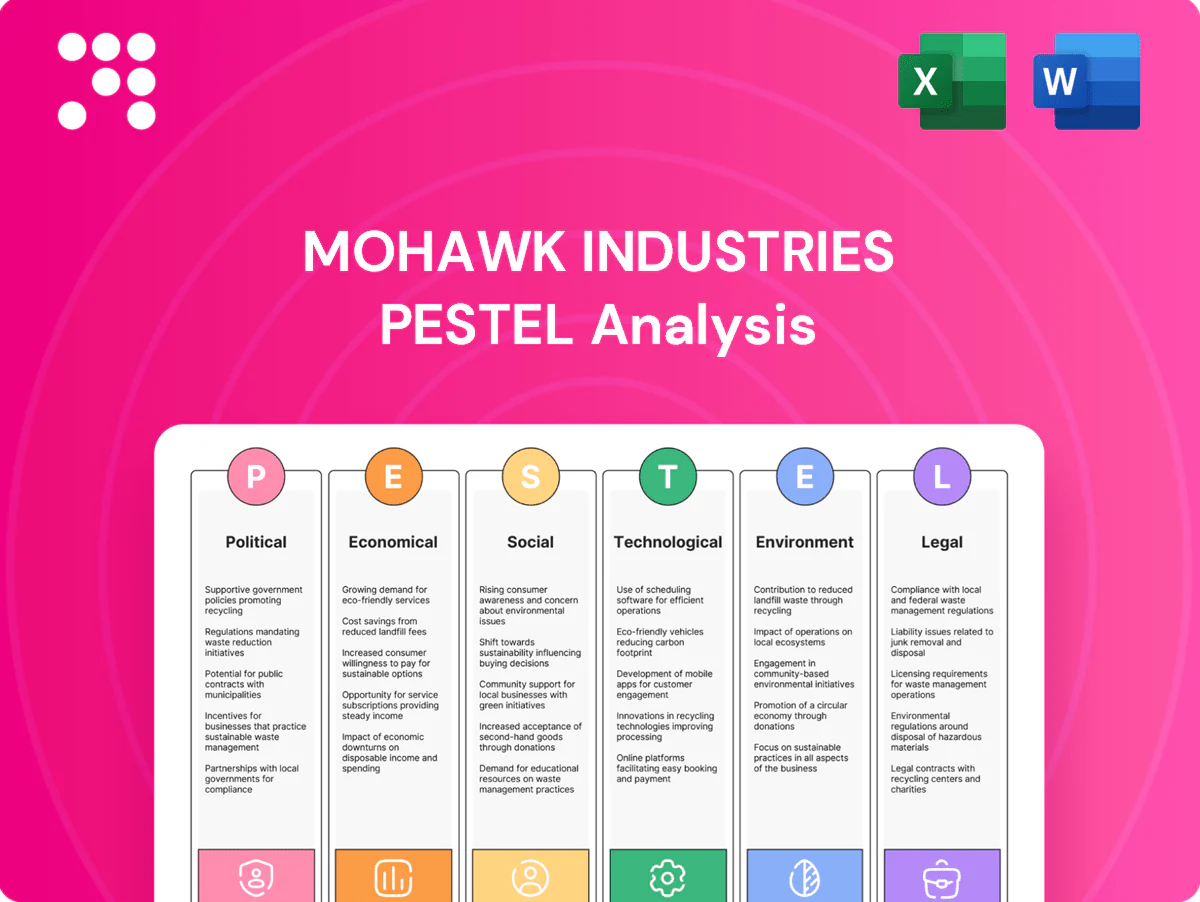

Political factors

Trade policy and tariffs

Import duties, including US Section 301 measures covering roughly $250 billion of Chinese goods with rates up to 25%, can swing Mohawk Industries’ input costs and pricing power across carpet, LVT and ceramic segments. Recent tariffs on vinyl/LVT from Asia have already forced shifts in sourcing and capacity allocation toward North America and Mexico. Changes in US–EU–China relations drive reshoring or dual‑sourcing strategies; policy stability reduces inventory and hedging needs while volatility raises both.

Infrastructure and housing incentives

Federal stimulus and infrastructure packages—IIJA’s roughly 1.2 trillion total with ~550 billion in new spending and the Inflation Reduction Act’s ~369 billion climate/energy funding—boost commercial and multifamily flooring demand; IRA tax credits and energy-efficiency incentives accelerate replacement cycles; tightened Buy American/local-content rules raise spec and sourcing constraints; multi-month gaps between appropriations and project starts reduce order visibility.

Building codes and standards

National and local building codes set fire, slip-resistance and indoor air quality thresholds that shape Mohawk Industries product specs and formulation choices. Code updates can advantage certain materials or finishes, shifting product mix and commercial specifying trends. Meeting evolving standards increases testing cycles and certification costs, making early alignment essential to capture specified commercial projects. Early compliance coordination improves win rates on architect and contractor specifications.

Energy and industrial policy

Policies on gas, electricity and carbon pricing materially affect Mohawk Industries’ plant operating costs: EU ETS averaged about €90/ton in 2024 and US industrial electricity ranged roughly $0.07–$0.11/kWh, driving variability in margins. Federal incentives under the IRA and CHIPS programs provide multibillion-dollar support for advanced manufacturing and automation, enabling capital projects. Regional energy shocks (2022–24) shifted site economics and force footprint optimization, while long-term policy clarity is key for investment timing.

- carbon-price: EU ETS ≈ €90/ton (2024)

- electricity-cost: US industrial ≈ $0.07–$0.11/kWh

- incentives: IRA/CHIPS = multibillion support for advanced manufacturing

- risk: regional energy shocks alter competitive cost positions

Geopolitical supply chain risk

Geopolitical conflicts, sanctions, and export controls can disrupt flows of resins, pigments, and flooring machinery, raising procurement risk for Mohawk Industries and increasing lead times and costs via tighter security and port controls. Port congestion and security rules add logistics delays and higher freight premiums, prompting Mohawk to diversify suppliers. Contingency inventories and nearshoring lessen single-country exposure and operational shocks.

- Conflict, sanctions: supply interruptions

- Port congestion: higher lead-time/logistics costs

- Diversified sourcing: lowers single-country risk

- Contingency stock & nearshoring: shock mitigation

Tariffs on $250B, IIJA/$1.2T, IRA lift flooring demand

Tariffs (US Section 301 covering ~$250B of Chinese goods, rates to 25%) and recent vinyl/LVT duties shift sourcing to North America/Mexico, raising input costs. IIJA (~$1.2T; ~$550B new) and IRA (~$369B) lift commercial/multifamily flooring demand; code updates and Buy American rules increase spec constraints. Energy/carbon policy (EU ETS ≈ €90/t 2024; US ind. $0.07–$0.11/kWh) alters plant economics and investment timing.

| Factor | 2024/25 data |

|---|---|

| Tariffs | ~$250B scope; up to 25% |

| Infrastructure | IIJA $1.2T (~$550B new) |

| Climate funding | IRA ~$369B |

| Carbon price | EU ETS ≈ €90/t (2024) |

| Electricity | US ind. $0.07–$0.11/kWh |

What is included in the product

Explains how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Mohawk Industries, with data‑backed trends, forward‑looking insights and actionable subpoints to support executives, consultants and investors; formatted for direct inclusion in plans, decks and scenario planning.

A concise, PESTLE-segmented summary of Mohawk Industries' external risks and opportunities, ready to drop into presentations or planning sessions; editable notes and clear language make it easy to share across teams and tailor to regions or business lines.

Economic factors

Housing and construction cycles

New home starts (~1.4M annualized in 2024), existing-home sales (~4.1M in 2024) and a remodeling market near $450B drive Mohawk's core volumes. Higher 30-year mortgage rates (around 6.8% in 2024–25) suppress turnover and discretionary renovations. Commercial demand tracks office, hospitality, healthcare and institutional pipelines, and shifts in regional mix alter product and price mix.

Input cost volatility

Mohawk's 2024 10-K flags volatility in PVC, wood, ceramic, energy and freight as key margin drivers, making price‑cost lag management critical to pass‑through. Supplier concentration for certain resins and specialty ceramics intensifies bargaining dynamics with suppliers. The company cites hedging and long‑term supply contracts as tools used to stabilize gross profit amid input swings.

Currency fluctuations

Mohawk’s global operations face translation and transaction FX risk as a strong USD compresses reported revenue and weakens export competitiveness; the US dollar averaged near 104 on the DXY in 2024, intensifying headwinds for multinational reporting. Local sourcing and regional production provide natural hedges, reducing transactional exposure in key markets. Pricing and sourcing strategies have been adjusted to persistent FX trends, including selective price increases and supplier diversification.

Labor markets and productivity

Tight labor markets have pushed wages and training costs higher for Mohawk’s plants and logistics, pressuring margins; Mohawk reported roughly 34,000 employees worldwide in FY2024, concentrating costs in manufacturing and distribution.

- Wage inflation: higher labor expense pressure

- Automation/lean: offsets skill gaps and inflation

- Attrition: affects retail/commercial service levels

- Safety/retention: boosts throughput reliability

Channel mix and retailer health

Channel mix matters as independent retailers, home centers and specification channels cycle differently: big-box retailers like Home Depot (FY24 sales ~157B) exert pricing pressure while specialty dealers sustain higher-service margins, squeezing Mohawk Industries margin mix. Distributor consolidation increases bargaining power with manufacturers; top distributors now control a larger share of trade sales, pressuring pricing and terms. Omnichannel readiness—digital sales and specification tools—allowed flooring suppliers to capture share during 2020–24 demand swings and remains critical for inventory turn and margin resilience.

Tariffs on $250B, IIJA/$1.2T, IRA lift flooring demand

Housing starts ~1.4M and existing-home sales ~4.1M underpin volumes while a ~$450B remodel market supports discretionary demand; 30-year mortgage rates ~6.8% curb turnover. Input volatility (PVC, ceramics, energy) and supplier concentration pressure margins. Strong USD (DXY ~104) and 34,000 employees raise translation and labor cost headwinds.

| Metric | 2024 value |

|---|---|

| Housing starts | ~1.4M |

| 30-yr mortgage | ~6.8% |

| Remodel market | ~$450B |

| DXY | ~104 |

| Employees | ~34,000 |

Full Version Awaits

Mohawk Industries PESTLE Analysis

The preview shown here is the exact Mohawk Industries PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete political, economic, social, technological, legal and environmental insights. No placeholders, no surprises; download is immediate.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, and sustainability trends are reshaping Mohawk Industries and where opportunities and risks lie; our concise PESTLE pinpoints implications for strategy and valuation. Purchase the full analysis to access actionable insights, data tables, and downloadable templates for immediate use.

Political factors

Trade policy and tariffs

Import duties, including US Section 301 measures covering roughly $250 billion of Chinese goods with rates up to 25%, can swing Mohawk Industries’ input costs and pricing power across carpet, LVT and ceramic segments. Recent tariffs on vinyl/LVT from Asia have already forced shifts in sourcing and capacity allocation toward North America and Mexico. Changes in US–EU–China relations drive reshoring or dual‑sourcing strategies; policy stability reduces inventory and hedging needs while volatility raises both.

Infrastructure and housing incentives

Federal stimulus and infrastructure packages—IIJA’s roughly 1.2 trillion total with ~550 billion in new spending and the Inflation Reduction Act’s ~369 billion climate/energy funding—boost commercial and multifamily flooring demand; IRA tax credits and energy-efficiency incentives accelerate replacement cycles; tightened Buy American/local-content rules raise spec and sourcing constraints; multi-month gaps between appropriations and project starts reduce order visibility.

Building codes and standards

National and local building codes set fire, slip-resistance and indoor air quality thresholds that shape Mohawk Industries product specs and formulation choices. Code updates can advantage certain materials or finishes, shifting product mix and commercial specifying trends. Meeting evolving standards increases testing cycles and certification costs, making early alignment essential to capture specified commercial projects. Early compliance coordination improves win rates on architect and contractor specifications.

Energy and industrial policy

Policies on gas, electricity and carbon pricing materially affect Mohawk Industries’ plant operating costs: EU ETS averaged about €90/ton in 2024 and US industrial electricity ranged roughly $0.07–$0.11/kWh, driving variability in margins. Federal incentives under the IRA and CHIPS programs provide multibillion-dollar support for advanced manufacturing and automation, enabling capital projects. Regional energy shocks (2022–24) shifted site economics and force footprint optimization, while long-term policy clarity is key for investment timing.

- carbon-price: EU ETS ≈ €90/ton (2024)

- electricity-cost: US industrial ≈ $0.07–$0.11/kWh

- incentives: IRA/CHIPS = multibillion support for advanced manufacturing

- risk: regional energy shocks alter competitive cost positions

Geopolitical supply chain risk

Geopolitical conflicts, sanctions, and export controls can disrupt flows of resins, pigments, and flooring machinery, raising procurement risk for Mohawk Industries and increasing lead times and costs via tighter security and port controls. Port congestion and security rules add logistics delays and higher freight premiums, prompting Mohawk to diversify suppliers. Contingency inventories and nearshoring lessen single-country exposure and operational shocks.

- Conflict, sanctions: supply interruptions

- Port congestion: higher lead-time/logistics costs

- Diversified sourcing: lowers single-country risk

- Contingency stock & nearshoring: shock mitigation

Tariffs on $250B, IIJA/$1.2T, IRA lift flooring demand

Tariffs (US Section 301 covering ~$250B of Chinese goods, rates to 25%) and recent vinyl/LVT duties shift sourcing to North America/Mexico, raising input costs. IIJA (~$1.2T; ~$550B new) and IRA (~$369B) lift commercial/multifamily flooring demand; code updates and Buy American rules increase spec constraints. Energy/carbon policy (EU ETS ≈ €90/t 2024; US ind. $0.07–$0.11/kWh) alters plant economics and investment timing.

| Factor | 2024/25 data |

|---|---|

| Tariffs | ~$250B scope; up to 25% |

| Infrastructure | IIJA $1.2T (~$550B new) |

| Climate funding | IRA ~$369B |

| Carbon price | EU ETS ≈ €90/t (2024) |

| Electricity | US ind. $0.07–$0.11/kWh |

What is included in the product

Explains how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Mohawk Industries, with data‑backed trends, forward‑looking insights and actionable subpoints to support executives, consultants and investors; formatted for direct inclusion in plans, decks and scenario planning.

A concise, PESTLE-segmented summary of Mohawk Industries' external risks and opportunities, ready to drop into presentations or planning sessions; editable notes and clear language make it easy to share across teams and tailor to regions or business lines.

Economic factors

Housing and construction cycles

New home starts (~1.4M annualized in 2024), existing-home sales (~4.1M in 2024) and a remodeling market near $450B drive Mohawk's core volumes. Higher 30-year mortgage rates (around 6.8% in 2024–25) suppress turnover and discretionary renovations. Commercial demand tracks office, hospitality, healthcare and institutional pipelines, and shifts in regional mix alter product and price mix.

Input cost volatility

Mohawk's 2024 10-K flags volatility in PVC, wood, ceramic, energy and freight as key margin drivers, making price‑cost lag management critical to pass‑through. Supplier concentration for certain resins and specialty ceramics intensifies bargaining dynamics with suppliers. The company cites hedging and long‑term supply contracts as tools used to stabilize gross profit amid input swings.

Currency fluctuations

Mohawk’s global operations face translation and transaction FX risk as a strong USD compresses reported revenue and weakens export competitiveness; the US dollar averaged near 104 on the DXY in 2024, intensifying headwinds for multinational reporting. Local sourcing and regional production provide natural hedges, reducing transactional exposure in key markets. Pricing and sourcing strategies have been adjusted to persistent FX trends, including selective price increases and supplier diversification.

Labor markets and productivity

Tight labor markets have pushed wages and training costs higher for Mohawk’s plants and logistics, pressuring margins; Mohawk reported roughly 34,000 employees worldwide in FY2024, concentrating costs in manufacturing and distribution.

- Wage inflation: higher labor expense pressure

- Automation/lean: offsets skill gaps and inflation

- Attrition: affects retail/commercial service levels

- Safety/retention: boosts throughput reliability

Channel mix and retailer health

Channel mix matters as independent retailers, home centers and specification channels cycle differently: big-box retailers like Home Depot (FY24 sales ~157B) exert pricing pressure while specialty dealers sustain higher-service margins, squeezing Mohawk Industries margin mix. Distributor consolidation increases bargaining power with manufacturers; top distributors now control a larger share of trade sales, pressuring pricing and terms. Omnichannel readiness—digital sales and specification tools—allowed flooring suppliers to capture share during 2020–24 demand swings and remains critical for inventory turn and margin resilience.

Tariffs on $250B, IIJA/$1.2T, IRA lift flooring demand

Housing starts ~1.4M and existing-home sales ~4.1M underpin volumes while a ~$450B remodel market supports discretionary demand; 30-year mortgage rates ~6.8% curb turnover. Input volatility (PVC, ceramics, energy) and supplier concentration pressure margins. Strong USD (DXY ~104) and 34,000 employees raise translation and labor cost headwinds.

| Metric | 2024 value |

|---|---|

| Housing starts | ~1.4M |

| 30-yr mortgage | ~6.8% |

| Remodel market | ~$450B |

| DXY | ~104 |

| Employees | ~34,000 |

Full Version Awaits

Mohawk Industries PESTLE Analysis

The preview shown here is the exact Mohawk Industries PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete political, economic, social, technological, legal and environmental insights. No placeholders, no surprises; download is immediate.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, and sustainability trends are reshaping Mohawk Industries and where opportunities and risks lie; our concise PESTLE pinpoints implications for strategy and valuation. Purchase the full analysis to access actionable insights, data tables, and downloadable templates for immediate use.

Political factors

Trade policy and tariffs

Import duties, including US Section 301 measures covering roughly $250 billion of Chinese goods with rates up to 25%, can swing Mohawk Industries’ input costs and pricing power across carpet, LVT and ceramic segments. Recent tariffs on vinyl/LVT from Asia have already forced shifts in sourcing and capacity allocation toward North America and Mexico. Changes in US–EU–China relations drive reshoring or dual‑sourcing strategies; policy stability reduces inventory and hedging needs while volatility raises both.

Infrastructure and housing incentives

Federal stimulus and infrastructure packages—IIJA’s roughly 1.2 trillion total with ~550 billion in new spending and the Inflation Reduction Act’s ~369 billion climate/energy funding—boost commercial and multifamily flooring demand; IRA tax credits and energy-efficiency incentives accelerate replacement cycles; tightened Buy American/local-content rules raise spec and sourcing constraints; multi-month gaps between appropriations and project starts reduce order visibility.

Building codes and standards

National and local building codes set fire, slip-resistance and indoor air quality thresholds that shape Mohawk Industries product specs and formulation choices. Code updates can advantage certain materials or finishes, shifting product mix and commercial specifying trends. Meeting evolving standards increases testing cycles and certification costs, making early alignment essential to capture specified commercial projects. Early compliance coordination improves win rates on architect and contractor specifications.

Energy and industrial policy

Policies on gas, electricity and carbon pricing materially affect Mohawk Industries’ plant operating costs: EU ETS averaged about €90/ton in 2024 and US industrial electricity ranged roughly $0.07–$0.11/kWh, driving variability in margins. Federal incentives under the IRA and CHIPS programs provide multibillion-dollar support for advanced manufacturing and automation, enabling capital projects. Regional energy shocks (2022–24) shifted site economics and force footprint optimization, while long-term policy clarity is key for investment timing.

- carbon-price: EU ETS ≈ €90/ton (2024)

- electricity-cost: US industrial ≈ $0.07–$0.11/kWh

- incentives: IRA/CHIPS = multibillion support for advanced manufacturing

- risk: regional energy shocks alter competitive cost positions

Geopolitical supply chain risk

Geopolitical conflicts, sanctions, and export controls can disrupt flows of resins, pigments, and flooring machinery, raising procurement risk for Mohawk Industries and increasing lead times and costs via tighter security and port controls. Port congestion and security rules add logistics delays and higher freight premiums, prompting Mohawk to diversify suppliers. Contingency inventories and nearshoring lessen single-country exposure and operational shocks.

- Conflict, sanctions: supply interruptions

- Port congestion: higher lead-time/logistics costs

- Diversified sourcing: lowers single-country risk

- Contingency stock & nearshoring: shock mitigation

Tariffs on $250B, IIJA/$1.2T, IRA lift flooring demand

Tariffs (US Section 301 covering ~$250B of Chinese goods, rates to 25%) and recent vinyl/LVT duties shift sourcing to North America/Mexico, raising input costs. IIJA (~$1.2T; ~$550B new) and IRA (~$369B) lift commercial/multifamily flooring demand; code updates and Buy American rules increase spec constraints. Energy/carbon policy (EU ETS ≈ €90/t 2024; US ind. $0.07–$0.11/kWh) alters plant economics and investment timing.

| Factor | 2024/25 data |

|---|---|

| Tariffs | ~$250B scope; up to 25% |

| Infrastructure | IIJA $1.2T (~$550B new) |

| Climate funding | IRA ~$369B |

| Carbon price | EU ETS ≈ €90/t (2024) |

| Electricity | US ind. $0.07–$0.11/kWh |

What is included in the product

Explains how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Mohawk Industries, with data‑backed trends, forward‑looking insights and actionable subpoints to support executives, consultants and investors; formatted for direct inclusion in plans, decks and scenario planning.

A concise, PESTLE-segmented summary of Mohawk Industries' external risks and opportunities, ready to drop into presentations or planning sessions; editable notes and clear language make it easy to share across teams and tailor to regions or business lines.

Economic factors

Housing and construction cycles

New home starts (~1.4M annualized in 2024), existing-home sales (~4.1M in 2024) and a remodeling market near $450B drive Mohawk's core volumes. Higher 30-year mortgage rates (around 6.8% in 2024–25) suppress turnover and discretionary renovations. Commercial demand tracks office, hospitality, healthcare and institutional pipelines, and shifts in regional mix alter product and price mix.

Input cost volatility

Mohawk's 2024 10-K flags volatility in PVC, wood, ceramic, energy and freight as key margin drivers, making price‑cost lag management critical to pass‑through. Supplier concentration for certain resins and specialty ceramics intensifies bargaining dynamics with suppliers. The company cites hedging and long‑term supply contracts as tools used to stabilize gross profit amid input swings.

Currency fluctuations

Mohawk’s global operations face translation and transaction FX risk as a strong USD compresses reported revenue and weakens export competitiveness; the US dollar averaged near 104 on the DXY in 2024, intensifying headwinds for multinational reporting. Local sourcing and regional production provide natural hedges, reducing transactional exposure in key markets. Pricing and sourcing strategies have been adjusted to persistent FX trends, including selective price increases and supplier diversification.

Labor markets and productivity

Tight labor markets have pushed wages and training costs higher for Mohawk’s plants and logistics, pressuring margins; Mohawk reported roughly 34,000 employees worldwide in FY2024, concentrating costs in manufacturing and distribution.

- Wage inflation: higher labor expense pressure

- Automation/lean: offsets skill gaps and inflation

- Attrition: affects retail/commercial service levels

- Safety/retention: boosts throughput reliability

Channel mix and retailer health

Channel mix matters as independent retailers, home centers and specification channels cycle differently: big-box retailers like Home Depot (FY24 sales ~157B) exert pricing pressure while specialty dealers sustain higher-service margins, squeezing Mohawk Industries margin mix. Distributor consolidation increases bargaining power with manufacturers; top distributors now control a larger share of trade sales, pressuring pricing and terms. Omnichannel readiness—digital sales and specification tools—allowed flooring suppliers to capture share during 2020–24 demand swings and remains critical for inventory turn and margin resilience.

Tariffs on $250B, IIJA/$1.2T, IRA lift flooring demand

Housing starts ~1.4M and existing-home sales ~4.1M underpin volumes while a ~$450B remodel market supports discretionary demand; 30-year mortgage rates ~6.8% curb turnover. Input volatility (PVC, ceramics, energy) and supplier concentration pressure margins. Strong USD (DXY ~104) and 34,000 employees raise translation and labor cost headwinds.

| Metric | 2024 value |

|---|---|

| Housing starts | ~1.4M |

| 30-yr mortgage | ~6.8% |

| Remodel market | ~$450B |

| DXY | ~104 |

| Employees | ~34,000 |

Full Version Awaits

Mohawk Industries PESTLE Analysis

The preview shown here is the exact Mohawk Industries PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete political, economic, social, technological, legal and environmental insights. No placeholders, no surprises; download is immediate.