Monolithic Power Systems Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Monolithic Power Systems faces nuanced supplier leverage, rising buyer expectations, and moderate substitution risk that shape its competitive outlook. Our snapshot highlights key pressures on margins and growth opportunities. Ready for decisive strategy or investment moves? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated foundry and OSAT base

Analog/mixed-signal ICs depend on a concentrated set of specialty foundries and OSATs (TSMC ~56% foundry share in 2024; ASE ~21% OSAT share in 2023), tightening capacity and raising supplier leverage in upcycles when fab utilization tops 90%. MPS mitigates via multi-sourcing, but full dual-qualification typically takes 12–18 months and adds significant cost. Leverage spikes for unique process options and automotive-grade flows.

Specialty materials and process IP

Access to GaN, SiC, high-voltage processes and proprietary PDKs is often gated by specialized fabs and IP licensors, so when MPS designs rely on unique device characteristics switching suppliers requires redesign and requalification, raising supplier leverage. This effect is acute for niche, high-performance lines where device differentiation is critical. For mainstream products built on broad, mature CMOS/BCD nodes the dependency and supplier power are materially lower.

Capacity cycles and lead-time risk

Semi capacity cycles shifted in 2024 with SEMI reporting wafer fab utilization above 85%, swinging bargaining power to suppliers during tight periods; wafer and substrate vendors often allocate to higher-priced or strategic customers. MPS relies on long-term agreements and rolling demand forecasts to secure slots; during allocations lead times can exceed 20 weeks. Expedited fees and larger inventory buffers raise working capital and compress gross margins.

Quality and reliability requirements

Automotive and industrial customers require AEC-Q, PPAP and zero-defect targets, which narrows the pool of suppliers that can scale for Monolithic Power Systems and raises supplier leverage. Fewer qualified sources increase pricing and delivery bargaining power. Audit, traceability and formal change-control typically make supplier qualification 6–12 months, so nonconformance risk markedly raises switching costs.

- AEC-Q/PPAP requirements limit supplier pool

- 6–12 month qualification & strict audits

- Traceability/change-control boost switching costs

Geopolitical and logistics exposure

Export controls and tariffs in 2024 tightened access to advanced foundry tooling and regional logistics, keeping global foundry utilization above 90% and constraining lead times. Suppliers with diversified geographies and compliance capabilities gained negotiating leverage, forcing MPS to dual-source regions and critical materials to buffer shocks. Freight-rate volatility through 2023–24, with swings exceeding 50% on some lanes, can shift contract terms toward suppliers during disruptions.

- Export controls impact: tighter 2024 rules on advanced nodes

- Foundry utilization: >90% in 2024

- Mitigation: dual-sourcing regions/materials

- Freight volatility: >50% swings 2023–24

Foundry/OSAT power tightens supply as utilization exceeds 90%

Supplier power is high for MPS where specialty foundries/OSATs dominate (TSMC ~56% foundry share 2024; ASE ~21% OSAT 2023) and utilization >90% in 2024, driving allocations and premium pricing. Qualification and AEC-Q/PPAP take 6–18 months, switching costs and lead times (>20 weeks) elevate supplier leverage. Dual-sourcing and long-term contracts partially mitigate risk.

| Supplier | Metric | 2023/24 |

|---|---|---|

| Foundries | Market share / util. | TSMC ~56% / >90% |

| OSATs | Market share | ASE ~21% (2023) |

| Lead times | Typical | >20 weeks |

| Qualify | Duration | 6–18 months |

What is included in the product

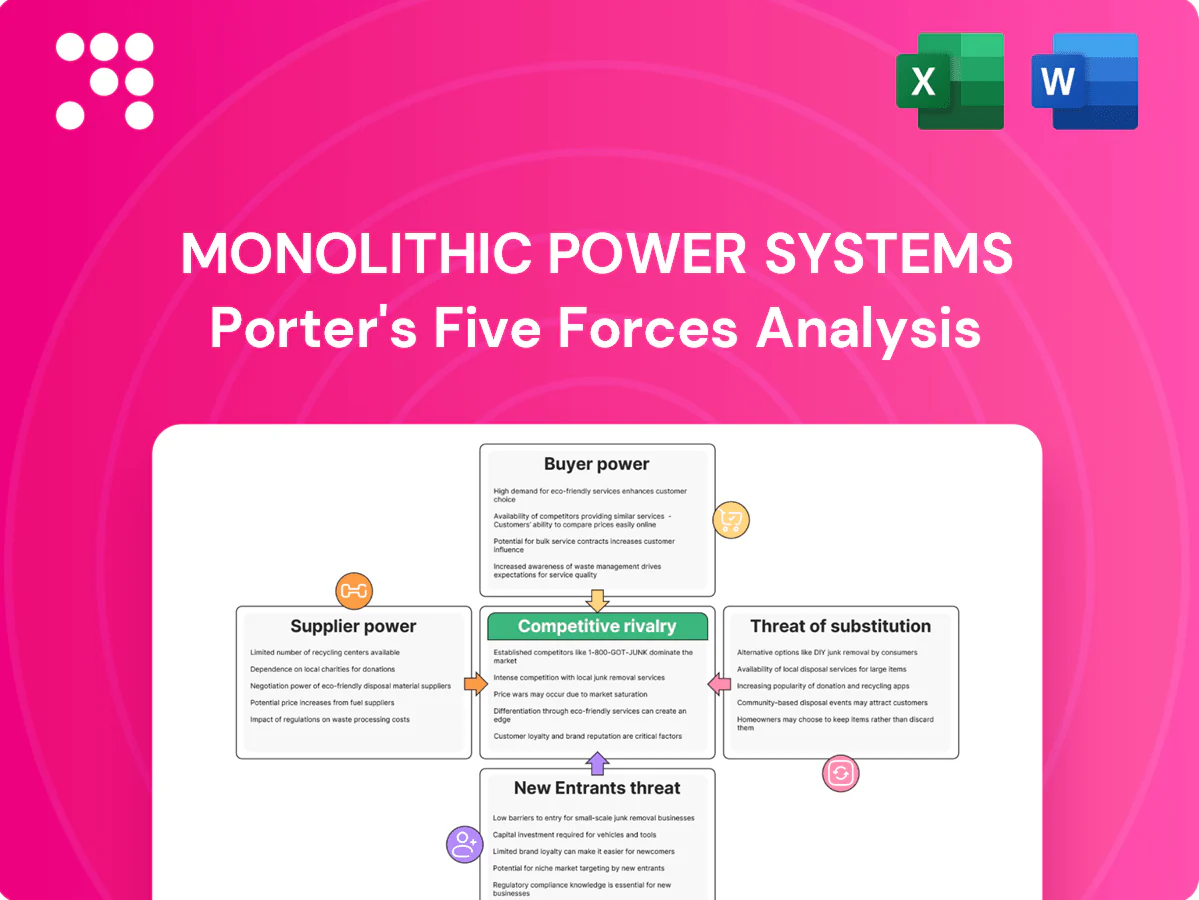

Tailored Porter's Five Forces analysis of Monolithic Power Systems, evaluating competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and emerging disruptive threats to pricing and profitability.

A one-sheet Porter's Five Forces for Monolithic Power Systems that visualizes supplier/customer power, threat of substitutes, entrant risk, and rivalry—ready to drop into decks and updated with your data for fast strategic decisions.

Customers Bargaining Power

Large OEMs and Tier-1s

Computing, automotive and communications customers are concentrated, sophisticated buyers whose scale and qualification processes force MPS to meet tight pricing and service terms; MPS reported roughly $2.8B revenue in 2024, reflecting exposure to large OEMs. These customers demand customization, long-term supply commitments and rigorous quality guarantees. Once MPS parts are designed-in, switching costs for OEMs are high, which tempers ongoing price pressure.

Design-in stickiness vs. bid-stage pressure

Pre-design wins expose MPS to competitive RFQs and dual-source strategies that commonly pressure ASPs by roughly 5–20% as buyers seek immediate cost reductions. Post-design win, industry-standard redesign costs of about $1–5M and 3–9 months of requalification plus field risk materially reduce buyer leverage. MPS’s high integration and reported mid-50s percent gross margins in 2024 let it justify premium ASPs while lifecycle support and component cost declines still force gradual cost-downs over product life.

Segment price sensitivity

Consumer and some industrial buyers are highly price elastic, increasing bargaining power and pressuring margin-sensitive MPWR offerings, while the automotive semiconductor market (~$68B in 2024) and enterprise customers prioritize reliability and total cost of ownership, softening price demands.

Buyers trade off BOM simplification and system efficiency versus unit cost, and MPWR uses value selling and platform reuse to retain ASPs and reduce negotiation leverage.

Demand volatility and forecasting

Demand volatility lets customers shift MPS orders rapidly with macro and inventory cycles, driving reschedules and cancellations that strengthen buyer leverage; MPS reported fiscal 2024 revenue of $2.56 billion, underscoring sensitivity to order timing. Flexible capacity and active backlog management are required to preserve contract terms, while take-or-pay long-term agreements exist but are not industry-wide.

- Order swings: buyers can reschedule/cancel

- Mitigation: flexible capacity, backlog controls

- Contracts: take-or-pay reduce buyer power but limited

Access to alternatives

Access to alternatives is strong as TI, ADI, Infineon, onsemi and Renesas—each reporting multi-billion-dollar revenues in 2024—offer comparable power ICs, boosting buyer leverage; reference designs and pin-to-pin drop-in parts increase swapability. Differentiated efficiency, thermal performance and integration lower substitutability, while software/tool ecosystems and evaluation support raise switching costs.

- Competitors: multi-billion revenues (2024)

- Reference designs: increase comparability

- Diff features: reduce substitution

- Software ecosystems: raise lock-in

OEM pre-design price pressure; $1–5M redesign locks buyers

Large OEMs (MPS rev $2.56B–$2.8B in 2024) exert strong pre-design price/service demands; post-design switching costs (redesign $1–5M, 3–9 months) reduce buyer leverage. Multi‑bn competitors (TI, ADI, Infineon, onsemi, Renesas in 2024) and elastic consumer segments sustain pressure. Long‑term contracts, platform reuse and margin cushions partially offset order volatility and reschedules.

| Metric | 2024 | Effect |

|---|---|---|

| MPS revenue | $2.56–2.8B | OEM exposure |

| Redesign cost/time | $1–5M, 3–9m | raises switching cost |

| Competitors | Multi‑bn revs | increases buyer options |

Preview the Actual Deliverable

Monolithic Power Systems Porter's Five Forces Analysis

This preview is the exact Monolithic Power Systems Porter's Five Forces Analysis you'll receive upon purchase—fully written, formatted, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No placeholders or samples—what you see is the final deliverable available instantly after payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Monolithic Power Systems faces nuanced supplier leverage, rising buyer expectations, and moderate substitution risk that shape its competitive outlook. Our snapshot highlights key pressures on margins and growth opportunities. Ready for decisive strategy or investment moves? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated foundry and OSAT base

Analog/mixed-signal ICs depend on a concentrated set of specialty foundries and OSATs (TSMC ~56% foundry share in 2024; ASE ~21% OSAT share in 2023), tightening capacity and raising supplier leverage in upcycles when fab utilization tops 90%. MPS mitigates via multi-sourcing, but full dual-qualification typically takes 12–18 months and adds significant cost. Leverage spikes for unique process options and automotive-grade flows.

Specialty materials and process IP

Access to GaN, SiC, high-voltage processes and proprietary PDKs is often gated by specialized fabs and IP licensors, so when MPS designs rely on unique device characteristics switching suppliers requires redesign and requalification, raising supplier leverage. This effect is acute for niche, high-performance lines where device differentiation is critical. For mainstream products built on broad, mature CMOS/BCD nodes the dependency and supplier power are materially lower.

Capacity cycles and lead-time risk

Semi capacity cycles shifted in 2024 with SEMI reporting wafer fab utilization above 85%, swinging bargaining power to suppliers during tight periods; wafer and substrate vendors often allocate to higher-priced or strategic customers. MPS relies on long-term agreements and rolling demand forecasts to secure slots; during allocations lead times can exceed 20 weeks. Expedited fees and larger inventory buffers raise working capital and compress gross margins.

Quality and reliability requirements

Automotive and industrial customers require AEC-Q, PPAP and zero-defect targets, which narrows the pool of suppliers that can scale for Monolithic Power Systems and raises supplier leverage. Fewer qualified sources increase pricing and delivery bargaining power. Audit, traceability and formal change-control typically make supplier qualification 6–12 months, so nonconformance risk markedly raises switching costs.

- AEC-Q/PPAP requirements limit supplier pool

- 6–12 month qualification & strict audits

- Traceability/change-control boost switching costs

Geopolitical and logistics exposure

Export controls and tariffs in 2024 tightened access to advanced foundry tooling and regional logistics, keeping global foundry utilization above 90% and constraining lead times. Suppliers with diversified geographies and compliance capabilities gained negotiating leverage, forcing MPS to dual-source regions and critical materials to buffer shocks. Freight-rate volatility through 2023–24, with swings exceeding 50% on some lanes, can shift contract terms toward suppliers during disruptions.

- Export controls impact: tighter 2024 rules on advanced nodes

- Foundry utilization: >90% in 2024

- Mitigation: dual-sourcing regions/materials

- Freight volatility: >50% swings 2023–24

Foundry/OSAT power tightens supply as utilization exceeds 90%

Supplier power is high for MPS where specialty foundries/OSATs dominate (TSMC ~56% foundry share 2024; ASE ~21% OSAT 2023) and utilization >90% in 2024, driving allocations and premium pricing. Qualification and AEC-Q/PPAP take 6–18 months, switching costs and lead times (>20 weeks) elevate supplier leverage. Dual-sourcing and long-term contracts partially mitigate risk.

| Supplier | Metric | 2023/24 |

|---|---|---|

| Foundries | Market share / util. | TSMC ~56% / >90% |

| OSATs | Market share | ASE ~21% (2023) |

| Lead times | Typical | >20 weeks |

| Qualify | Duration | 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis of Monolithic Power Systems, evaluating competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and emerging disruptive threats to pricing and profitability.

A one-sheet Porter's Five Forces for Monolithic Power Systems that visualizes supplier/customer power, threat of substitutes, entrant risk, and rivalry—ready to drop into decks and updated with your data for fast strategic decisions.

Customers Bargaining Power

Large OEMs and Tier-1s

Computing, automotive and communications customers are concentrated, sophisticated buyers whose scale and qualification processes force MPS to meet tight pricing and service terms; MPS reported roughly $2.8B revenue in 2024, reflecting exposure to large OEMs. These customers demand customization, long-term supply commitments and rigorous quality guarantees. Once MPS parts are designed-in, switching costs for OEMs are high, which tempers ongoing price pressure.

Design-in stickiness vs. bid-stage pressure

Pre-design wins expose MPS to competitive RFQs and dual-source strategies that commonly pressure ASPs by roughly 5–20% as buyers seek immediate cost reductions. Post-design win, industry-standard redesign costs of about $1–5M and 3–9 months of requalification plus field risk materially reduce buyer leverage. MPS’s high integration and reported mid-50s percent gross margins in 2024 let it justify premium ASPs while lifecycle support and component cost declines still force gradual cost-downs over product life.

Segment price sensitivity

Consumer and some industrial buyers are highly price elastic, increasing bargaining power and pressuring margin-sensitive MPWR offerings, while the automotive semiconductor market (~$68B in 2024) and enterprise customers prioritize reliability and total cost of ownership, softening price demands.

Buyers trade off BOM simplification and system efficiency versus unit cost, and MPWR uses value selling and platform reuse to retain ASPs and reduce negotiation leverage.

Demand volatility and forecasting

Demand volatility lets customers shift MPS orders rapidly with macro and inventory cycles, driving reschedules and cancellations that strengthen buyer leverage; MPS reported fiscal 2024 revenue of $2.56 billion, underscoring sensitivity to order timing. Flexible capacity and active backlog management are required to preserve contract terms, while take-or-pay long-term agreements exist but are not industry-wide.

- Order swings: buyers can reschedule/cancel

- Mitigation: flexible capacity, backlog controls

- Contracts: take-or-pay reduce buyer power but limited

Access to alternatives

Access to alternatives is strong as TI, ADI, Infineon, onsemi and Renesas—each reporting multi-billion-dollar revenues in 2024—offer comparable power ICs, boosting buyer leverage; reference designs and pin-to-pin drop-in parts increase swapability. Differentiated efficiency, thermal performance and integration lower substitutability, while software/tool ecosystems and evaluation support raise switching costs.

- Competitors: multi-billion revenues (2024)

- Reference designs: increase comparability

- Diff features: reduce substitution

- Software ecosystems: raise lock-in

OEM pre-design price pressure; $1–5M redesign locks buyers

Large OEMs (MPS rev $2.56B–$2.8B in 2024) exert strong pre-design price/service demands; post-design switching costs (redesign $1–5M, 3–9 months) reduce buyer leverage. Multi‑bn competitors (TI, ADI, Infineon, onsemi, Renesas in 2024) and elastic consumer segments sustain pressure. Long‑term contracts, platform reuse and margin cushions partially offset order volatility and reschedules.

| Metric | 2024 | Effect |

|---|---|---|

| MPS revenue | $2.56–2.8B | OEM exposure |

| Redesign cost/time | $1–5M, 3–9m | raises switching cost |

| Competitors | Multi‑bn revs | increases buyer options |

Preview the Actual Deliverable

Monolithic Power Systems Porter's Five Forces Analysis

This preview is the exact Monolithic Power Systems Porter's Five Forces Analysis you'll receive upon purchase—fully written, formatted, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No placeholders or samples—what you see is the final deliverable available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Monolithic Power Systems faces nuanced supplier leverage, rising buyer expectations, and moderate substitution risk that shape its competitive outlook. Our snapshot highlights key pressures on margins and growth opportunities. Ready for decisive strategy or investment moves? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated foundry and OSAT base

Analog/mixed-signal ICs depend on a concentrated set of specialty foundries and OSATs (TSMC ~56% foundry share in 2024; ASE ~21% OSAT share in 2023), tightening capacity and raising supplier leverage in upcycles when fab utilization tops 90%. MPS mitigates via multi-sourcing, but full dual-qualification typically takes 12–18 months and adds significant cost. Leverage spikes for unique process options and automotive-grade flows.

Specialty materials and process IP

Access to GaN, SiC, high-voltage processes and proprietary PDKs is often gated by specialized fabs and IP licensors, so when MPS designs rely on unique device characteristics switching suppliers requires redesign and requalification, raising supplier leverage. This effect is acute for niche, high-performance lines where device differentiation is critical. For mainstream products built on broad, mature CMOS/BCD nodes the dependency and supplier power are materially lower.

Capacity cycles and lead-time risk

Semi capacity cycles shifted in 2024 with SEMI reporting wafer fab utilization above 85%, swinging bargaining power to suppliers during tight periods; wafer and substrate vendors often allocate to higher-priced or strategic customers. MPS relies on long-term agreements and rolling demand forecasts to secure slots; during allocations lead times can exceed 20 weeks. Expedited fees and larger inventory buffers raise working capital and compress gross margins.

Quality and reliability requirements

Automotive and industrial customers require AEC-Q, PPAP and zero-defect targets, which narrows the pool of suppliers that can scale for Monolithic Power Systems and raises supplier leverage. Fewer qualified sources increase pricing and delivery bargaining power. Audit, traceability and formal change-control typically make supplier qualification 6–12 months, so nonconformance risk markedly raises switching costs.

- AEC-Q/PPAP requirements limit supplier pool

- 6–12 month qualification & strict audits

- Traceability/change-control boost switching costs

Geopolitical and logistics exposure

Export controls and tariffs in 2024 tightened access to advanced foundry tooling and regional logistics, keeping global foundry utilization above 90% and constraining lead times. Suppliers with diversified geographies and compliance capabilities gained negotiating leverage, forcing MPS to dual-source regions and critical materials to buffer shocks. Freight-rate volatility through 2023–24, with swings exceeding 50% on some lanes, can shift contract terms toward suppliers during disruptions.

- Export controls impact: tighter 2024 rules on advanced nodes

- Foundry utilization: >90% in 2024

- Mitigation: dual-sourcing regions/materials

- Freight volatility: >50% swings 2023–24

Foundry/OSAT power tightens supply as utilization exceeds 90%

Supplier power is high for MPS where specialty foundries/OSATs dominate (TSMC ~56% foundry share 2024; ASE ~21% OSAT 2023) and utilization >90% in 2024, driving allocations and premium pricing. Qualification and AEC-Q/PPAP take 6–18 months, switching costs and lead times (>20 weeks) elevate supplier leverage. Dual-sourcing and long-term contracts partially mitigate risk.

| Supplier | Metric | 2023/24 |

|---|---|---|

| Foundries | Market share / util. | TSMC ~56% / >90% |

| OSATs | Market share | ASE ~21% (2023) |

| Lead times | Typical | >20 weeks |

| Qualify | Duration | 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis of Monolithic Power Systems, evaluating competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and emerging disruptive threats to pricing and profitability.

A one-sheet Porter's Five Forces for Monolithic Power Systems that visualizes supplier/customer power, threat of substitutes, entrant risk, and rivalry—ready to drop into decks and updated with your data for fast strategic decisions.

Customers Bargaining Power

Large OEMs and Tier-1s

Computing, automotive and communications customers are concentrated, sophisticated buyers whose scale and qualification processes force MPS to meet tight pricing and service terms; MPS reported roughly $2.8B revenue in 2024, reflecting exposure to large OEMs. These customers demand customization, long-term supply commitments and rigorous quality guarantees. Once MPS parts are designed-in, switching costs for OEMs are high, which tempers ongoing price pressure.

Design-in stickiness vs. bid-stage pressure

Pre-design wins expose MPS to competitive RFQs and dual-source strategies that commonly pressure ASPs by roughly 5–20% as buyers seek immediate cost reductions. Post-design win, industry-standard redesign costs of about $1–5M and 3–9 months of requalification plus field risk materially reduce buyer leverage. MPS’s high integration and reported mid-50s percent gross margins in 2024 let it justify premium ASPs while lifecycle support and component cost declines still force gradual cost-downs over product life.

Segment price sensitivity

Consumer and some industrial buyers are highly price elastic, increasing bargaining power and pressuring margin-sensitive MPWR offerings, while the automotive semiconductor market (~$68B in 2024) and enterprise customers prioritize reliability and total cost of ownership, softening price demands.

Buyers trade off BOM simplification and system efficiency versus unit cost, and MPWR uses value selling and platform reuse to retain ASPs and reduce negotiation leverage.

Demand volatility and forecasting

Demand volatility lets customers shift MPS orders rapidly with macro and inventory cycles, driving reschedules and cancellations that strengthen buyer leverage; MPS reported fiscal 2024 revenue of $2.56 billion, underscoring sensitivity to order timing. Flexible capacity and active backlog management are required to preserve contract terms, while take-or-pay long-term agreements exist but are not industry-wide.

- Order swings: buyers can reschedule/cancel

- Mitigation: flexible capacity, backlog controls

- Contracts: take-or-pay reduce buyer power but limited

Access to alternatives

Access to alternatives is strong as TI, ADI, Infineon, onsemi and Renesas—each reporting multi-billion-dollar revenues in 2024—offer comparable power ICs, boosting buyer leverage; reference designs and pin-to-pin drop-in parts increase swapability. Differentiated efficiency, thermal performance and integration lower substitutability, while software/tool ecosystems and evaluation support raise switching costs.

- Competitors: multi-billion revenues (2024)

- Reference designs: increase comparability

- Diff features: reduce substitution

- Software ecosystems: raise lock-in

OEM pre-design price pressure; $1–5M redesign locks buyers

Large OEMs (MPS rev $2.56B–$2.8B in 2024) exert strong pre-design price/service demands; post-design switching costs (redesign $1–5M, 3–9 months) reduce buyer leverage. Multi‑bn competitors (TI, ADI, Infineon, onsemi, Renesas in 2024) and elastic consumer segments sustain pressure. Long‑term contracts, platform reuse and margin cushions partially offset order volatility and reschedules.

| Metric | 2024 | Effect |

|---|---|---|

| MPS revenue | $2.56–2.8B | OEM exposure |

| Redesign cost/time | $1–5M, 3–9m | raises switching cost |

| Competitors | Multi‑bn revs | increases buyer options |

Preview the Actual Deliverable

Monolithic Power Systems Porter's Five Forces Analysis

This preview is the exact Monolithic Power Systems Porter's Five Forces Analysis you'll receive upon purchase—fully written, formatted, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. No placeholders or samples—what you see is the final deliverable available instantly after payment.