Morita SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

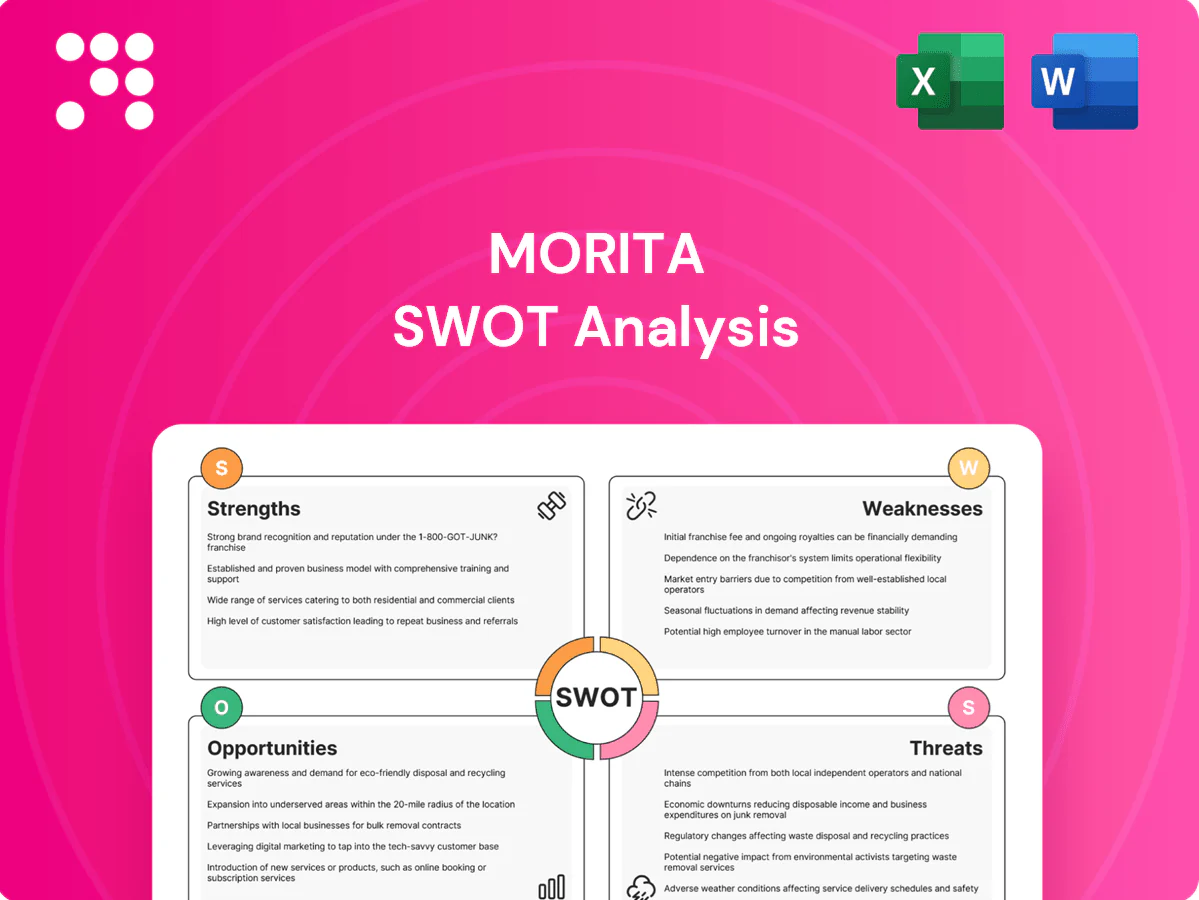

Uncover Morita’s competitive edge with our concise SWOT snapshot—highlighting core strengths, key vulnerabilities, market opportunities, and looming threats. The full SWOT delivers research-backed detail, expert commentary, and editable Word and Excel files. Purchase the complete analysis to plan, pitch, or invest with confidence.

Strengths

Broad specialized portfolio

Morita spans fire engines, extinguishing systems and environmental vehicles, cutting reliance on any single segment and enabling cross‑selling and bundled municipal/industrial contracts; with operations in about 25 countries and reported group sales near JPY 58.2 billion (FY2024), the mix balances cyclical demand across safety and waste‑management budgets, enhancing resilience and revenue stability.

Strong service and lifecycle support

Morita’s maintenance, repair and inspection services generate recurring revenue and deepen customer lock-in; aftermarket sales commonly deliver 30–50% gross margins in medical/dental equipment sectors (2024 industry reports). Long equipment lifecycles, often exceeding 10 years, make aftermarket a margin-accretive pillar. Field service data improves reliability and product design, raising client switching costs through integrated service-product ecosystems.

Reputation in safety-critical markets

Supplying mission-critical firefighting and emergency vehicles to public agencies has made Morita a trusted vendor, reflected in multi-year framework contracts with several municipal fire departments across Japan. Rigorous compliance and testing—backed by ISO certifications and a documented low field-failure rate—strengthen brand equity and simplify compliance review in new tenders. Large reference fleets and third-party certifications shorten procurement cycles and turn reliability into a durable competitive moat.

Disaster prevention consulting

Disaster prevention consulting elevates Morita from hardware to solutions, leveraging advisory services that tap the global emergency management market valued at about $11.7B in 2023 with ~8% CAGR, uncovering new equipment and recurring service revenue while differentiating bids through outcome-focused offerings and transferring knowledge to secure long-term client contracts.

- Value-chain: advisory-driven sales

- Market: $11.7B (2023), ~8% CAGR

- Growth: equipment + services upsell

- Differentiator: outcome-focused bids

- Retention: knowledge transfer → long-term clients

Global footprint and compliance know-how

Morita’s global footprint spreads revenue across diverse markets and builds standards expertise, reducing reliance on any single region. Mastery of varying regulations accelerates certifications and approvals, shortening time-to-market in major jurisdictions. Global sourcing and distribution enhance cost efficiency and delivery flexibility, while experience in international tenders widens the project pipeline.

- Geographic diversification

- Regulatory competence

- Cost and delivery agility

- Expanded tender pipeline

Diversified emergency equipment, 30-50% aftermarket margins

Morita’s diversified mix—fire engines, extinguishing systems, environmental vehicles—and presence in ~25 countries (group sales JPY58.2bn FY2024) reduce single-segment risk and enable bundled contracts. Aftermarket services (30–50% gross margins) and equipment lifecycles >10 years drive recurring, high-margin revenue and switching costs. ISO certifications, low field-failure rates and municipal frameworks reinforce trust and shorten procurement.

| Metric | Value |

|---|---|

| Sales (FY2024) | JPY58.2bn |

| Countries | ~25 |

| Aftermarket margin | 30–50% |

| Equipment life | >10 yrs |

| Emergency market (2023) | $11.7B, ~8% CAGR |

What is included in the product

Provides a clear SWOT framework identifying Morita’s internal strengths and weaknesses and external opportunities and threats to assess its strategic position and future risks.

Provides a focused Morita SWOT matrix that quickly reveals treatment-market fit and operational gaps, streamlining strategy adjustments.

Weaknesses

High dependence on public tenders

High dependence on public tenders means large portions of demand are tied to municipal and government budgets, which account for about 12% of GDP on average across OECD countries (OECD). Procurement cycles are lengthy and often exceed six months, creating revenue unpredictability. Price-based award rules commonly compress margins, and political shifts can quickly reprioritize spending away from Morita's product lines.

Capital- and engineering-intensive operations

Complex vehicle upfitting and specialized systems require significant capex and skilled labor, with mid‑sized upfitters reporting annual capex of roughly $5–15 million and specialized labor premiums of 20–40% above standard assembly rates in 2024.

Fixed‑cost absorption is highly sensitive to volume swings, with utilization drops of 10–25% translating to 15–30% margin erosion in recent industry cases.

High customization raises engineering hours and rework risk, lengthening lead times to 12–26 weeks and compressing cash conversion cycles amid rising WIP and inventory in 2024–2025.

Limited software monetization

Morita's hardware focus underutilizes telematics, analytics and SaaS layers, leaving digital revenues untapped while global telematics/software markets grew (telematics market ~ $52B in 2024). Missing digital income can cap customer lifetime value versus peers shifting to data platforms, who report materially higher LTV. Lack of a standardized data architecture slows feature rollout and weakens long-term differentiation.

Product complexity and long lead times

Tailored Morita configurations extend quoting, approval and build cycles so order-to-delivery often exceeds 12 weeks, limiting rapid response to demand; supply hiccups cascade into additional 10–30% delivery delays seen across medical-device supply chains in 2023–24. Customers increasingly prefer modular vendors offering 2–4 week lead times.

- Long cycles: >12 weeks

- Supply delays: +10–30%

- Competitive modular lead times: 2–4 weeks

Exposure to liability and warranty costs

Safety-critical failures expose Morita to significant legal and reputational risk, with high-severity product incidents driving multi-million-dollar lawsuits and regulatory scrutiny in 2024.

Recalls have proven costly and divert engineering resources; industry recall events remained elevated in 2024, increasing remediation spend and time-to-market delays.

Tight specs and harsh operating environments raise warranty claims and pushed product liability insurance premiums up about 10% in 2024.

- Legal/reputational risk

- High recall remediation costs

- Increased warranty claims

- Insurance premium inflation (~10% in 2024)

Tender concentration, prolonged procurement and $5–15M upfits compress margins

Morita is exposed to demand concentration in public tenders (~12% of GDP-linked budgets), long procurement cycles (>6 months) and price-driven margin compression; complex upfitting needs $5–15M capex and 20–40% labor premiums (2024). High customization and >12-week lead times vs 2–4 weeks competitors raise WIP and margin volatility; recalls/legal costs and insurance up ~10% (2024).

| Metric | 2024–25 Value |

|---|---|

| Telematics market | $52B |

| Capex (mid upfit) | $5–15M |

| Labor premium | 20–40% |

| Insurance inflation | ~10% |

Full Version Awaits

Morita SWOT Analysis

This is the actual Morita SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the complete, editable version becomes available after checkout. Buy now to download the full, detailed file.

Dive Deeper Into the Company’s Strategic Blueprint

Uncover Morita’s competitive edge with our concise SWOT snapshot—highlighting core strengths, key vulnerabilities, market opportunities, and looming threats. The full SWOT delivers research-backed detail, expert commentary, and editable Word and Excel files. Purchase the complete analysis to plan, pitch, or invest with confidence.

Strengths

Broad specialized portfolio

Morita spans fire engines, extinguishing systems and environmental vehicles, cutting reliance on any single segment and enabling cross‑selling and bundled municipal/industrial contracts; with operations in about 25 countries and reported group sales near JPY 58.2 billion (FY2024), the mix balances cyclical demand across safety and waste‑management budgets, enhancing resilience and revenue stability.

Strong service and lifecycle support

Morita’s maintenance, repair and inspection services generate recurring revenue and deepen customer lock-in; aftermarket sales commonly deliver 30–50% gross margins in medical/dental equipment sectors (2024 industry reports). Long equipment lifecycles, often exceeding 10 years, make aftermarket a margin-accretive pillar. Field service data improves reliability and product design, raising client switching costs through integrated service-product ecosystems.

Reputation in safety-critical markets

Supplying mission-critical firefighting and emergency vehicles to public agencies has made Morita a trusted vendor, reflected in multi-year framework contracts with several municipal fire departments across Japan. Rigorous compliance and testing—backed by ISO certifications and a documented low field-failure rate—strengthen brand equity and simplify compliance review in new tenders. Large reference fleets and third-party certifications shorten procurement cycles and turn reliability into a durable competitive moat.

Disaster prevention consulting

Disaster prevention consulting elevates Morita from hardware to solutions, leveraging advisory services that tap the global emergency management market valued at about $11.7B in 2023 with ~8% CAGR, uncovering new equipment and recurring service revenue while differentiating bids through outcome-focused offerings and transferring knowledge to secure long-term client contracts.

- Value-chain: advisory-driven sales

- Market: $11.7B (2023), ~8% CAGR

- Growth: equipment + services upsell

- Differentiator: outcome-focused bids

- Retention: knowledge transfer → long-term clients

Global footprint and compliance know-how

Morita’s global footprint spreads revenue across diverse markets and builds standards expertise, reducing reliance on any single region. Mastery of varying regulations accelerates certifications and approvals, shortening time-to-market in major jurisdictions. Global sourcing and distribution enhance cost efficiency and delivery flexibility, while experience in international tenders widens the project pipeline.

- Geographic diversification

- Regulatory competence

- Cost and delivery agility

- Expanded tender pipeline

Diversified emergency equipment, 30-50% aftermarket margins

Morita’s diversified mix—fire engines, extinguishing systems, environmental vehicles—and presence in ~25 countries (group sales JPY58.2bn FY2024) reduce single-segment risk and enable bundled contracts. Aftermarket services (30–50% gross margins) and equipment lifecycles >10 years drive recurring, high-margin revenue and switching costs. ISO certifications, low field-failure rates and municipal frameworks reinforce trust and shorten procurement.

| Metric | Value |

|---|---|

| Sales (FY2024) | JPY58.2bn |

| Countries | ~25 |

| Aftermarket margin | 30–50% |

| Equipment life | >10 yrs |

| Emergency market (2023) | $11.7B, ~8% CAGR |

What is included in the product

Provides a clear SWOT framework identifying Morita’s internal strengths and weaknesses and external opportunities and threats to assess its strategic position and future risks.

Provides a focused Morita SWOT matrix that quickly reveals treatment-market fit and operational gaps, streamlining strategy adjustments.

Weaknesses

High dependence on public tenders

High dependence on public tenders means large portions of demand are tied to municipal and government budgets, which account for about 12% of GDP on average across OECD countries (OECD). Procurement cycles are lengthy and often exceed six months, creating revenue unpredictability. Price-based award rules commonly compress margins, and political shifts can quickly reprioritize spending away from Morita's product lines.

Capital- and engineering-intensive operations

Complex vehicle upfitting and specialized systems require significant capex and skilled labor, with mid‑sized upfitters reporting annual capex of roughly $5–15 million and specialized labor premiums of 20–40% above standard assembly rates in 2024.

Fixed‑cost absorption is highly sensitive to volume swings, with utilization drops of 10–25% translating to 15–30% margin erosion in recent industry cases.

High customization raises engineering hours and rework risk, lengthening lead times to 12–26 weeks and compressing cash conversion cycles amid rising WIP and inventory in 2024–2025.

Limited software monetization

Morita's hardware focus underutilizes telematics, analytics and SaaS layers, leaving digital revenues untapped while global telematics/software markets grew (telematics market ~ $52B in 2024). Missing digital income can cap customer lifetime value versus peers shifting to data platforms, who report materially higher LTV. Lack of a standardized data architecture slows feature rollout and weakens long-term differentiation.

Product complexity and long lead times

Tailored Morita configurations extend quoting, approval and build cycles so order-to-delivery often exceeds 12 weeks, limiting rapid response to demand; supply hiccups cascade into additional 10–30% delivery delays seen across medical-device supply chains in 2023–24. Customers increasingly prefer modular vendors offering 2–4 week lead times.

- Long cycles: >12 weeks

- Supply delays: +10–30%

- Competitive modular lead times: 2–4 weeks

Exposure to liability and warranty costs

Safety-critical failures expose Morita to significant legal and reputational risk, with high-severity product incidents driving multi-million-dollar lawsuits and regulatory scrutiny in 2024.

Recalls have proven costly and divert engineering resources; industry recall events remained elevated in 2024, increasing remediation spend and time-to-market delays.

Tight specs and harsh operating environments raise warranty claims and pushed product liability insurance premiums up about 10% in 2024.

- Legal/reputational risk

- High recall remediation costs

- Increased warranty claims

- Insurance premium inflation (~10% in 2024)

Tender concentration, prolonged procurement and $5–15M upfits compress margins

Morita is exposed to demand concentration in public tenders (~12% of GDP-linked budgets), long procurement cycles (>6 months) and price-driven margin compression; complex upfitting needs $5–15M capex and 20–40% labor premiums (2024). High customization and >12-week lead times vs 2–4 weeks competitors raise WIP and margin volatility; recalls/legal costs and insurance up ~10% (2024).

| Metric | 2024–25 Value |

|---|---|

| Telematics market | $52B |

| Capex (mid upfit) | $5–15M |

| Labor premium | 20–40% |

| Insurance inflation | ~10% |

Full Version Awaits

Morita SWOT Analysis

This is the actual Morita SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the complete, editable version becomes available after checkout. Buy now to download the full, detailed file.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Uncover Morita’s competitive edge with our concise SWOT snapshot—highlighting core strengths, key vulnerabilities, market opportunities, and looming threats. The full SWOT delivers research-backed detail, expert commentary, and editable Word and Excel files. Purchase the complete analysis to plan, pitch, or invest with confidence.

Strengths

Broad specialized portfolio

Morita spans fire engines, extinguishing systems and environmental vehicles, cutting reliance on any single segment and enabling cross‑selling and bundled municipal/industrial contracts; with operations in about 25 countries and reported group sales near JPY 58.2 billion (FY2024), the mix balances cyclical demand across safety and waste‑management budgets, enhancing resilience and revenue stability.

Strong service and lifecycle support

Morita’s maintenance, repair and inspection services generate recurring revenue and deepen customer lock-in; aftermarket sales commonly deliver 30–50% gross margins in medical/dental equipment sectors (2024 industry reports). Long equipment lifecycles, often exceeding 10 years, make aftermarket a margin-accretive pillar. Field service data improves reliability and product design, raising client switching costs through integrated service-product ecosystems.

Reputation in safety-critical markets

Supplying mission-critical firefighting and emergency vehicles to public agencies has made Morita a trusted vendor, reflected in multi-year framework contracts with several municipal fire departments across Japan. Rigorous compliance and testing—backed by ISO certifications and a documented low field-failure rate—strengthen brand equity and simplify compliance review in new tenders. Large reference fleets and third-party certifications shorten procurement cycles and turn reliability into a durable competitive moat.

Disaster prevention consulting

Disaster prevention consulting elevates Morita from hardware to solutions, leveraging advisory services that tap the global emergency management market valued at about $11.7B in 2023 with ~8% CAGR, uncovering new equipment and recurring service revenue while differentiating bids through outcome-focused offerings and transferring knowledge to secure long-term client contracts.

- Value-chain: advisory-driven sales

- Market: $11.7B (2023), ~8% CAGR

- Growth: equipment + services upsell

- Differentiator: outcome-focused bids

- Retention: knowledge transfer → long-term clients

Global footprint and compliance know-how

Morita’s global footprint spreads revenue across diverse markets and builds standards expertise, reducing reliance on any single region. Mastery of varying regulations accelerates certifications and approvals, shortening time-to-market in major jurisdictions. Global sourcing and distribution enhance cost efficiency and delivery flexibility, while experience in international tenders widens the project pipeline.

- Geographic diversification

- Regulatory competence

- Cost and delivery agility

- Expanded tender pipeline

Diversified emergency equipment, 30-50% aftermarket margins

Morita’s diversified mix—fire engines, extinguishing systems, environmental vehicles—and presence in ~25 countries (group sales JPY58.2bn FY2024) reduce single-segment risk and enable bundled contracts. Aftermarket services (30–50% gross margins) and equipment lifecycles >10 years drive recurring, high-margin revenue and switching costs. ISO certifications, low field-failure rates and municipal frameworks reinforce trust and shorten procurement.

| Metric | Value |

|---|---|

| Sales (FY2024) | JPY58.2bn |

| Countries | ~25 |

| Aftermarket margin | 30–50% |

| Equipment life | >10 yrs |

| Emergency market (2023) | $11.7B, ~8% CAGR |

What is included in the product

Provides a clear SWOT framework identifying Morita’s internal strengths and weaknesses and external opportunities and threats to assess its strategic position and future risks.

Provides a focused Morita SWOT matrix that quickly reveals treatment-market fit and operational gaps, streamlining strategy adjustments.

Weaknesses

High dependence on public tenders

High dependence on public tenders means large portions of demand are tied to municipal and government budgets, which account for about 12% of GDP on average across OECD countries (OECD). Procurement cycles are lengthy and often exceed six months, creating revenue unpredictability. Price-based award rules commonly compress margins, and political shifts can quickly reprioritize spending away from Morita's product lines.

Capital- and engineering-intensive operations

Complex vehicle upfitting and specialized systems require significant capex and skilled labor, with mid‑sized upfitters reporting annual capex of roughly $5–15 million and specialized labor premiums of 20–40% above standard assembly rates in 2024.

Fixed‑cost absorption is highly sensitive to volume swings, with utilization drops of 10–25% translating to 15–30% margin erosion in recent industry cases.

High customization raises engineering hours and rework risk, lengthening lead times to 12–26 weeks and compressing cash conversion cycles amid rising WIP and inventory in 2024–2025.

Limited software monetization

Morita's hardware focus underutilizes telematics, analytics and SaaS layers, leaving digital revenues untapped while global telematics/software markets grew (telematics market ~ $52B in 2024). Missing digital income can cap customer lifetime value versus peers shifting to data platforms, who report materially higher LTV. Lack of a standardized data architecture slows feature rollout and weakens long-term differentiation.

Product complexity and long lead times

Tailored Morita configurations extend quoting, approval and build cycles so order-to-delivery often exceeds 12 weeks, limiting rapid response to demand; supply hiccups cascade into additional 10–30% delivery delays seen across medical-device supply chains in 2023–24. Customers increasingly prefer modular vendors offering 2–4 week lead times.

- Long cycles: >12 weeks

- Supply delays: +10–30%

- Competitive modular lead times: 2–4 weeks

Exposure to liability and warranty costs

Safety-critical failures expose Morita to significant legal and reputational risk, with high-severity product incidents driving multi-million-dollar lawsuits and regulatory scrutiny in 2024.

Recalls have proven costly and divert engineering resources; industry recall events remained elevated in 2024, increasing remediation spend and time-to-market delays.

Tight specs and harsh operating environments raise warranty claims and pushed product liability insurance premiums up about 10% in 2024.

- Legal/reputational risk

- High recall remediation costs

- Increased warranty claims

- Insurance premium inflation (~10% in 2024)

Tender concentration, prolonged procurement and $5–15M upfits compress margins

Morita is exposed to demand concentration in public tenders (~12% of GDP-linked budgets), long procurement cycles (>6 months) and price-driven margin compression; complex upfitting needs $5–15M capex and 20–40% labor premiums (2024). High customization and >12-week lead times vs 2–4 weeks competitors raise WIP and margin volatility; recalls/legal costs and insurance up ~10% (2024).

| Metric | 2024–25 Value |

|---|---|

| Telematics market | $52B |

| Capex (mid upfit) | $5–15M |

| Labor premium | 20–40% |

| Insurance inflation | ~10% |

Full Version Awaits

Morita SWOT Analysis

This is the actual Morita SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the complete, editable version becomes available after checkout. Buy now to download the full, detailed file.