M.P. Evans Group Boston Consulting Group Matrix

Unlock Strategic Clarity

M.P. Evans Group’s BCG Matrix preview highlights which businesses are feeding growth, which are steady cash generators, and which need a rethink — all in the context of agri-commodities and timber. Want the full picture with quadrant-by-quadrant placements, actionable moves, and editable Word/Excel files? Purchase the complete BCG Matrix for a fast, practical roadmap to optimize capital and focus where it matters most.

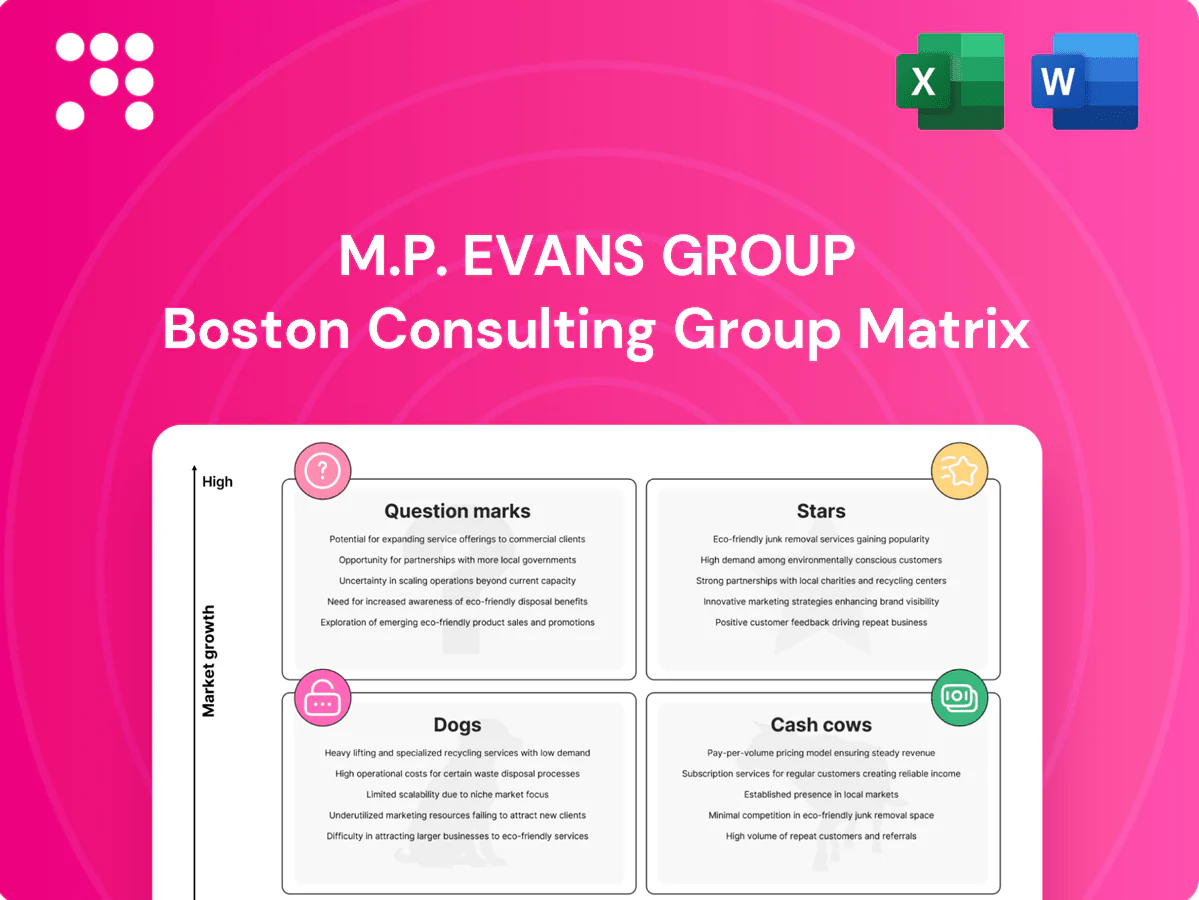

Stars

Flagship high-yield estates

Core Indonesian plantations deliver high fresh-fruit-bunch yields and lead locally while riding growing certified sustainable palm oil demand; intensive capex for upkeep, labour and replanting is absorbed because throughput and margins convert these estates into reliable cash machines if maintained. Lose focus and competitors capture supply and market share.

Modern mills with scale and recovery

High-capacity mills with strong oil-extraction rates anchor M.P. Evans market share in fast-growing Sabah catchments, leveraging palm oil’s ~36% share of global vegetable oil supply (2024). They require steady investment in uptime, logistics and digital mill tech to sustain OER gains and throughput. As volumes climb, unit processing costs fall—often materially—and margins widen, keeping capacity tight accelerates the growth flywheel.

RSPO/ISPO certified segregated supply

Premium-certified segregated CPO/PKO meets rising demand from the EU, brand owners and banks pushing ESG; certification costs (audits, training, monitoring) are material. Price uplifts typically run about $20–50/ton, while access to blue-chip buyers and green finance (sustainable debt issuance ~ $1.1tn in 2023) defend market share. Sustain investment and this star can become a premium cash cow.

Smallholder partnerships driving FFB inflow

Partner schemes expand FFB supply faster than planting alone and lock loyalty; smallholders supply roughly 40% of national FFB in major producing countries, so effective partnerships can rapidly lift catchment volumes while avoiding long lead times of replanting.

They require upfront financing, agronomy support, transparent fair-pricing mechanisms and traceability; done well mills stay full and catchment share can rise materially, done poorly volume leaks to traders.

- Financing: advance payments and credit

- Agronomy: yield uplift via training and inputs

- Pricing: clear, timely palm price settlement

- Risk: trader leakage if trust/prices fail

Biogas capture and energy-from-waste

Mill methane capture cuts potent methane (≈28x CO2 GWP over 100 years) and can power mills with surplus sometimes sold; capex-heavy and operationally fussy initially but reduces energy spend and boosts sustainability credentials, scaling with throughput to create a defensible edge in a growing energy-from-waste market.

- Emissions: methane ≈28x CO2 GWP

- Capex: high initial investment

- Ops: requires start-up expertise

- Benefits: lowers energy costs, potential revenue, ESG win

Indonesian estates lift margins; certified CPO gets $20-50/t premium

Core Indonesian estates deliver high FFB yields and margins, supporting growth as palm oil holds ~36% of global veg oil supply (2024); maintenance capex and replanting are essential. High-OER Sabah mills cut unit costs; scale lifts margins. Certified segregated CPO commands ~$20–50/t premium and access to buyers; smallholders supply ~40% of FFB. Methane from POME ≈28x CO2 GWP; biogas capex is high but offsets energy costs.

| Metric | Value | Impact |

|---|---|---|

| Veg oil share (2024) | 36% | Demand tailwind |

| Price premium | $20–50/ton | Revenue uplift |

| Smallholder FFB | ~40% | Supply growth |

| Sustainable debt (2023) | $1.1tn | Financing access |

| Methane GWP | ≈28x CO2 | ESG risk/opportunity |

What is included in the product

Concise BCG Matrix review of M.P. Evans Group: spots Stars, Cash Cows, Question Marks and Dogs with investment advice and trend context.

One-page BCG matrix for M.P. Evans Group—clarifies unit priorities fast, ready for exec meetings and slides.

Cash Cows

Mature estates with steady yields

Mature, well-managed estates deliver dependable fruit with modest upkeep, generating predictable cash flow even as growth remains flat. Costs are stable and minimal promotion is needed—discipline and operational efficiency sustain margins. Cash receipts cover operating bills, fund scheduled replanting programmes and support the dividend policy. These blocks act as the group’s financing backbone.

Recurring offtake to established refiners

Recurring offtake to established refiners converts M.P. Evans volume into low-friction cashflow; in 2024 this channel remained a primary cash generator for the plantation businesses. Margins are steady rather than spectacular, but predictable pricing and contract continuity keep working capital needs low. Maintain tight service levels and product specs and the stream funds investment in the next growth wave.

Palm kernel and meal by-products

Not glamorous but consistent, palm kernel and meal by-products in M.P. Evans Group act as reliable cash cows, converting residues into saleable feed and oil inputs throughout 2024. They monetize material that would otherwise sit idle, supporting gross margin resilience and improving working capital turnover. With limited growth potential but stable demand from feed and industrial buyers, they quietly underpin profitability and cash flow.

Mill biomass for in-house energy

Mill biomass (fiber and shell) fuels in-house boilers, cutting external diesel purchases and converting savings directly into operating cash flow; this is now standard mill operation rather than a growth driver. Continuous use keeps fuel cost volatility low; management focus should be on reliable maintenance, not heavy capex expansion.

- Operational status: routine energy source

- Financial impact: savings flow to cash

- Strategic stance: maintain, avoid over‑investment

Fully planted land bank

Fully planted land bank: planting is complete and heavy capex is behind the business; the focus is harvesting, yield optimisation and tight cost control rather than further acreage expansion. Cash conversion from fresh fruit bunches to free cash flow is the performance metric; milk returns and redeploy capital into higher-return opportunities.

- Operational focus: yield & cost per tonne

- Financial KPI: cash conversion

- Strategy: harvest, optimise, redeploy

Mature estates drive steady cash flow as biomass cuts fuel costs and refiners secure offtake

Mature estates and by‑products provided steady, low‑growth cash flow in 2024, funding replanting and dividends. Offtake agreements with refiners remained the primary cash generator. Mill biomass cut fuel bills, boosting operating cash. Fully planted land bank focuses on yield and cash conversion rather than expansion.

| Item | 2024 Status |

|---|---|

| Primary cash source | Offtake to refiners |

| By‑products | Stable demand, margin support |

| Energy | Biomass reduces fuel cost |

What You See Is What You Get

M.P. Evans Group BCG Matrix

The file you're previewing here is the exact M.P. Evans Group BCG Matrix you'll receive after purchase — no watermarks, no demo layers, just the finished report. It’s formatted for clarity and strategic use, ready to drop into presentations or planning sessions. Buy once and download immediately; the document is fully editable and print-ready. What you see is what you get — straightforward, professional, and no surprises.

Unlock Strategic Clarity

M.P. Evans Group’s BCG Matrix preview highlights which businesses are feeding growth, which are steady cash generators, and which need a rethink — all in the context of agri-commodities and timber. Want the full picture with quadrant-by-quadrant placements, actionable moves, and editable Word/Excel files? Purchase the complete BCG Matrix for a fast, practical roadmap to optimize capital and focus where it matters most.

Stars

Flagship high-yield estates

Core Indonesian plantations deliver high fresh-fruit-bunch yields and lead locally while riding growing certified sustainable palm oil demand; intensive capex for upkeep, labour and replanting is absorbed because throughput and margins convert these estates into reliable cash machines if maintained. Lose focus and competitors capture supply and market share.

Modern mills with scale and recovery

High-capacity mills with strong oil-extraction rates anchor M.P. Evans market share in fast-growing Sabah catchments, leveraging palm oil’s ~36% share of global vegetable oil supply (2024). They require steady investment in uptime, logistics and digital mill tech to sustain OER gains and throughput. As volumes climb, unit processing costs fall—often materially—and margins widen, keeping capacity tight accelerates the growth flywheel.

RSPO/ISPO certified segregated supply

Premium-certified segregated CPO/PKO meets rising demand from the EU, brand owners and banks pushing ESG; certification costs (audits, training, monitoring) are material. Price uplifts typically run about $20–50/ton, while access to blue-chip buyers and green finance (sustainable debt issuance ~ $1.1tn in 2023) defend market share. Sustain investment and this star can become a premium cash cow.

Smallholder partnerships driving FFB inflow

Partner schemes expand FFB supply faster than planting alone and lock loyalty; smallholders supply roughly 40% of national FFB in major producing countries, so effective partnerships can rapidly lift catchment volumes while avoiding long lead times of replanting.

They require upfront financing, agronomy support, transparent fair-pricing mechanisms and traceability; done well mills stay full and catchment share can rise materially, done poorly volume leaks to traders.

- Financing: advance payments and credit

- Agronomy: yield uplift via training and inputs

- Pricing: clear, timely palm price settlement

- Risk: trader leakage if trust/prices fail

Biogas capture and energy-from-waste

Mill methane capture cuts potent methane (≈28x CO2 GWP over 100 years) and can power mills with surplus sometimes sold; capex-heavy and operationally fussy initially but reduces energy spend and boosts sustainability credentials, scaling with throughput to create a defensible edge in a growing energy-from-waste market.

- Emissions: methane ≈28x CO2 GWP

- Capex: high initial investment

- Ops: requires start-up expertise

- Benefits: lowers energy costs, potential revenue, ESG win

Indonesian estates lift margins; certified CPO gets $20-50/t premium

Core Indonesian estates deliver high FFB yields and margins, supporting growth as palm oil holds ~36% of global veg oil supply (2024); maintenance capex and replanting are essential. High-OER Sabah mills cut unit costs; scale lifts margins. Certified segregated CPO commands ~$20–50/t premium and access to buyers; smallholders supply ~40% of FFB. Methane from POME ≈28x CO2 GWP; biogas capex is high but offsets energy costs.

| Metric | Value | Impact |

|---|---|---|

| Veg oil share (2024) | 36% | Demand tailwind |

| Price premium | $20–50/ton | Revenue uplift |

| Smallholder FFB | ~40% | Supply growth |

| Sustainable debt (2023) | $1.1tn | Financing access |

| Methane GWP | ≈28x CO2 | ESG risk/opportunity |

What is included in the product

Concise BCG Matrix review of M.P. Evans Group: spots Stars, Cash Cows, Question Marks and Dogs with investment advice and trend context.

One-page BCG matrix for M.P. Evans Group—clarifies unit priorities fast, ready for exec meetings and slides.

Cash Cows

Mature estates with steady yields

Mature, well-managed estates deliver dependable fruit with modest upkeep, generating predictable cash flow even as growth remains flat. Costs are stable and minimal promotion is needed—discipline and operational efficiency sustain margins. Cash receipts cover operating bills, fund scheduled replanting programmes and support the dividend policy. These blocks act as the group’s financing backbone.

Recurring offtake to established refiners

Recurring offtake to established refiners converts M.P. Evans volume into low-friction cashflow; in 2024 this channel remained a primary cash generator for the plantation businesses. Margins are steady rather than spectacular, but predictable pricing and contract continuity keep working capital needs low. Maintain tight service levels and product specs and the stream funds investment in the next growth wave.

Palm kernel and meal by-products

Not glamorous but consistent, palm kernel and meal by-products in M.P. Evans Group act as reliable cash cows, converting residues into saleable feed and oil inputs throughout 2024. They monetize material that would otherwise sit idle, supporting gross margin resilience and improving working capital turnover. With limited growth potential but stable demand from feed and industrial buyers, they quietly underpin profitability and cash flow.

Mill biomass for in-house energy

Mill biomass (fiber and shell) fuels in-house boilers, cutting external diesel purchases and converting savings directly into operating cash flow; this is now standard mill operation rather than a growth driver. Continuous use keeps fuel cost volatility low; management focus should be on reliable maintenance, not heavy capex expansion.

- Operational status: routine energy source

- Financial impact: savings flow to cash

- Strategic stance: maintain, avoid over‑investment

Fully planted land bank

Fully planted land bank: planting is complete and heavy capex is behind the business; the focus is harvesting, yield optimisation and tight cost control rather than further acreage expansion. Cash conversion from fresh fruit bunches to free cash flow is the performance metric; milk returns and redeploy capital into higher-return opportunities.

- Operational focus: yield & cost per tonne

- Financial KPI: cash conversion

- Strategy: harvest, optimise, redeploy

Mature estates drive steady cash flow as biomass cuts fuel costs and refiners secure offtake

Mature estates and by‑products provided steady, low‑growth cash flow in 2024, funding replanting and dividends. Offtake agreements with refiners remained the primary cash generator. Mill biomass cut fuel bills, boosting operating cash. Fully planted land bank focuses on yield and cash conversion rather than expansion.

| Item | 2024 Status |

|---|---|

| Primary cash source | Offtake to refiners |

| By‑products | Stable demand, margin support |

| Energy | Biomass reduces fuel cost |

What You See Is What You Get

M.P. Evans Group BCG Matrix

The file you're previewing here is the exact M.P. Evans Group BCG Matrix you'll receive after purchase — no watermarks, no demo layers, just the finished report. It’s formatted for clarity and strategic use, ready to drop into presentations or planning sessions. Buy once and download immediately; the document is fully editable and print-ready. What you see is what you get — straightforward, professional, and no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Unlock Strategic Clarity

M.P. Evans Group’s BCG Matrix preview highlights which businesses are feeding growth, which are steady cash generators, and which need a rethink — all in the context of agri-commodities and timber. Want the full picture with quadrant-by-quadrant placements, actionable moves, and editable Word/Excel files? Purchase the complete BCG Matrix for a fast, practical roadmap to optimize capital and focus where it matters most.

Stars

Flagship high-yield estates

Core Indonesian plantations deliver high fresh-fruit-bunch yields and lead locally while riding growing certified sustainable palm oil demand; intensive capex for upkeep, labour and replanting is absorbed because throughput and margins convert these estates into reliable cash machines if maintained. Lose focus and competitors capture supply and market share.

Modern mills with scale and recovery

High-capacity mills with strong oil-extraction rates anchor M.P. Evans market share in fast-growing Sabah catchments, leveraging palm oil’s ~36% share of global vegetable oil supply (2024). They require steady investment in uptime, logistics and digital mill tech to sustain OER gains and throughput. As volumes climb, unit processing costs fall—often materially—and margins widen, keeping capacity tight accelerates the growth flywheel.

RSPO/ISPO certified segregated supply

Premium-certified segregated CPO/PKO meets rising demand from the EU, brand owners and banks pushing ESG; certification costs (audits, training, monitoring) are material. Price uplifts typically run about $20–50/ton, while access to blue-chip buyers and green finance (sustainable debt issuance ~ $1.1tn in 2023) defend market share. Sustain investment and this star can become a premium cash cow.

Smallholder partnerships driving FFB inflow

Partner schemes expand FFB supply faster than planting alone and lock loyalty; smallholders supply roughly 40% of national FFB in major producing countries, so effective partnerships can rapidly lift catchment volumes while avoiding long lead times of replanting.

They require upfront financing, agronomy support, transparent fair-pricing mechanisms and traceability; done well mills stay full and catchment share can rise materially, done poorly volume leaks to traders.

- Financing: advance payments and credit

- Agronomy: yield uplift via training and inputs

- Pricing: clear, timely palm price settlement

- Risk: trader leakage if trust/prices fail

Biogas capture and energy-from-waste

Mill methane capture cuts potent methane (≈28x CO2 GWP over 100 years) and can power mills with surplus sometimes sold; capex-heavy and operationally fussy initially but reduces energy spend and boosts sustainability credentials, scaling with throughput to create a defensible edge in a growing energy-from-waste market.

- Emissions: methane ≈28x CO2 GWP

- Capex: high initial investment

- Ops: requires start-up expertise

- Benefits: lowers energy costs, potential revenue, ESG win

Indonesian estates lift margins; certified CPO gets $20-50/t premium

Core Indonesian estates deliver high FFB yields and margins, supporting growth as palm oil holds ~36% of global veg oil supply (2024); maintenance capex and replanting are essential. High-OER Sabah mills cut unit costs; scale lifts margins. Certified segregated CPO commands ~$20–50/t premium and access to buyers; smallholders supply ~40% of FFB. Methane from POME ≈28x CO2 GWP; biogas capex is high but offsets energy costs.

| Metric | Value | Impact |

|---|---|---|

| Veg oil share (2024) | 36% | Demand tailwind |

| Price premium | $20–50/ton | Revenue uplift |

| Smallholder FFB | ~40% | Supply growth |

| Sustainable debt (2023) | $1.1tn | Financing access |

| Methane GWP | ≈28x CO2 | ESG risk/opportunity |

What is included in the product

Concise BCG Matrix review of M.P. Evans Group: spots Stars, Cash Cows, Question Marks and Dogs with investment advice and trend context.

One-page BCG matrix for M.P. Evans Group—clarifies unit priorities fast, ready for exec meetings and slides.

Cash Cows

Mature estates with steady yields

Mature, well-managed estates deliver dependable fruit with modest upkeep, generating predictable cash flow even as growth remains flat. Costs are stable and minimal promotion is needed—discipline and operational efficiency sustain margins. Cash receipts cover operating bills, fund scheduled replanting programmes and support the dividend policy. These blocks act as the group’s financing backbone.

Recurring offtake to established refiners

Recurring offtake to established refiners converts M.P. Evans volume into low-friction cashflow; in 2024 this channel remained a primary cash generator for the plantation businesses. Margins are steady rather than spectacular, but predictable pricing and contract continuity keep working capital needs low. Maintain tight service levels and product specs and the stream funds investment in the next growth wave.

Palm kernel and meal by-products

Not glamorous but consistent, palm kernel and meal by-products in M.P. Evans Group act as reliable cash cows, converting residues into saleable feed and oil inputs throughout 2024. They monetize material that would otherwise sit idle, supporting gross margin resilience and improving working capital turnover. With limited growth potential but stable demand from feed and industrial buyers, they quietly underpin profitability and cash flow.

Mill biomass for in-house energy

Mill biomass (fiber and shell) fuels in-house boilers, cutting external diesel purchases and converting savings directly into operating cash flow; this is now standard mill operation rather than a growth driver. Continuous use keeps fuel cost volatility low; management focus should be on reliable maintenance, not heavy capex expansion.

- Operational status: routine energy source

- Financial impact: savings flow to cash

- Strategic stance: maintain, avoid over‑investment

Fully planted land bank

Fully planted land bank: planting is complete and heavy capex is behind the business; the focus is harvesting, yield optimisation and tight cost control rather than further acreage expansion. Cash conversion from fresh fruit bunches to free cash flow is the performance metric; milk returns and redeploy capital into higher-return opportunities.

- Operational focus: yield & cost per tonne

- Financial KPI: cash conversion

- Strategy: harvest, optimise, redeploy

Mature estates drive steady cash flow as biomass cuts fuel costs and refiners secure offtake

Mature estates and by‑products provided steady, low‑growth cash flow in 2024, funding replanting and dividends. Offtake agreements with refiners remained the primary cash generator. Mill biomass cut fuel bills, boosting operating cash. Fully planted land bank focuses on yield and cash conversion rather than expansion.

| Item | 2024 Status |

|---|---|

| Primary cash source | Offtake to refiners |

| By‑products | Stable demand, margin support |

| Energy | Biomass reduces fuel cost |

What You See Is What You Get

M.P. Evans Group BCG Matrix

The file you're previewing here is the exact M.P. Evans Group BCG Matrix you'll receive after purchase — no watermarks, no demo layers, just the finished report. It’s formatted for clarity and strategic use, ready to drop into presentations or planning sessions. Buy once and download immediately; the document is fully editable and print-ready. What you see is what you get — straightforward, professional, and no surprises.