Mount Gibson Iron SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Mount Gibson Iron’s strategic foothold in premium iron ore and low-cost operations masks exposure to price cycles and logistic bottlenecks; our full SWOT unpacks supply, ESG risks, and growth levers with actionable takeaways. Purchase the complete, editable SWOT report (Word + Excel) to plan, pitch, or invest with confidence.

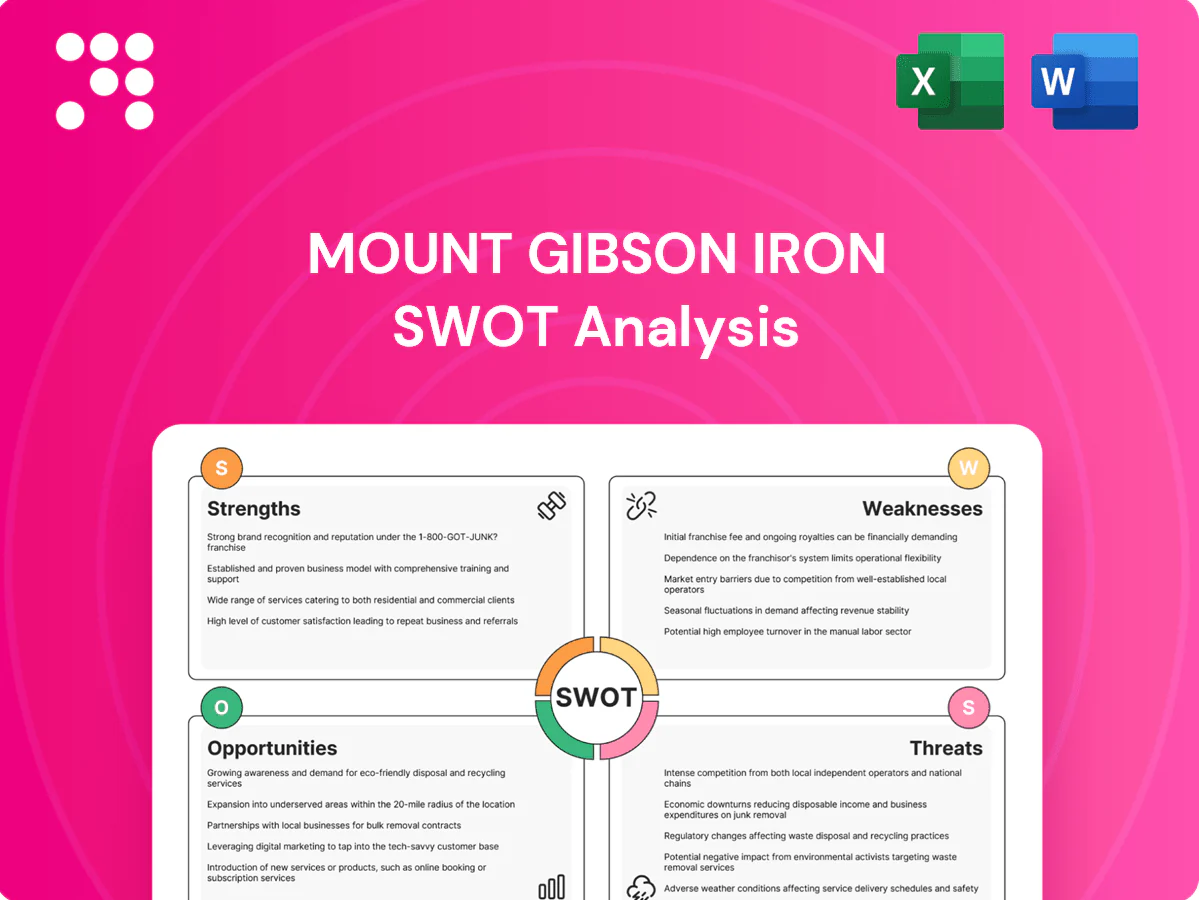

Strengths

High-grade ore focus

Mount Gibson’s emphasis on high-grade ore — aligned with the 62% Fe benchmark — supports premium pricing and blending value for Asian steel mills. Higher grades lower impurity penalties and reduce energy intensity in steelmaking, aiding mills’ net-zero-by-2050 decarbonization plans. This quality premium cushions margins in down cycles and deepens ties with efficiency-focused mills.

Cost-effective operations

Mount Gibson’s model emphasizes disciplined cost control across mining, processing and logistics, delivering competitive unit costs that bolster margins amid iron ore price swings; operational leanness improves responsiveness to market shifts and supports stronger cash generation for reinvestment and balance sheet resilience.

WA mining footprint

Operations in Western Australia give Mount Gibson access to established mining services, a skilled workforce and export infrastructure concentrated in WA, which underpins Australia’s position as the world’s largest iron ore exporter (~60% of seaborne trade in 2023). Proximity to deep‑water ports shortens shipping to Asia (typically 4–6 days to China), cutting freight costs and lead times. A proven, low‑sovereign‑risk jurisdiction versus many peers supports capital access, while WA’s mining ecosystem enables efficient expansions and maintenance.

Established Asian customer ties

Longstanding supply relationships across Asia, where China accounts for roughly 70% of seaborne iron ore demand (2024), underpin offtake certainty and clearer pricing signals; repeat business from key buyers improves demand visibility and vessel scheduling. These ties enable collaborative product optimisation and trial cargoes and help secure working capital and resilient contract terms through cycles.

- Offtake certainty: long-term Asian buyers

- Demand visibility: repeat cargoes aid scheduling

- Product R&D: trial cargoes with customers

- Finance stability: better working-capital terms

Execution track record

Mount Gibson Iron's execution track record in developing and operating iron ore mines reduces project and ramp-up risk, with institutional mine-planning and grade-control expertise improving recovery and product consistency; data-driven operations continually refine unit cost curves and underpin credibility for permitting, financing and stakeholder engagement.

High-grade 62% Fe drives premium pricing; WA supply, 4-6 day transit China

High‑grade 62% Fe product supports premium pricing and blending value for Asian mills. Disciplined cost control and data-led operations sustain competitive unit costs and margins. WA operations offer low sovereign risk, port access and ~4–6 day shipping to China, backed by long Asian offtake relationships (China ~70% seaborne demand, 2024).

| Metric | Fact |

|---|---|

| Grade | 62% Fe benchmark |

| China demand | ~70% seaborne, 2024 |

| Aus seaborne share | ~60%, 2023 |

| Transit | 4–6 days to China |

What is included in the product

Delivers a strategic overview of Mount Gibson Iron’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position in global iron ore markets.

Provides a concise Mount Gibson Iron SWOT matrix for fast, visual strategy alignment and investor-ready summaries, ideal for executives needing a snapshot of competitive positioning.

Weaknesses

Single-commodity exposure

ASX:MGX derives the vast majority of its income from iron ore, leaving earnings tightly correlated with the 62% Fe CFR China benchmark and amplifying volatility when that index weakens. Limited product mix reduces natural shock absorbers and leaves fewer hedging instruments compared with diversified base‑metal miners. Strategic flexibility is constrained versus multi‑commodity peers that can reallocate capital amid commodity cycles.

Scale disadvantage

Smaller production scale — roughly 2 Mtpa in 2024 versus majors producing >200 Mtpa — increases sensitivity to fixed costs and shipping-rate swings, magnifying per-ton cost volatility.

Limited scale reduces bargaining power with contractors and buyers, constraining contract leverage and premium capture.

Difficulty capturing economies of scale in rail, energy and procurement widens cost differentials in down markets, eroding margins faster than larger peers.

Geographic concentration

Operations concentrated in Western Australia concentrate Mount Gibson Iron’s risk: regional weather, labor shortages and local regulatory shifts can disrupt multiple sites simultaneously. WA accounts for roughly 90% of Australia’s iron ore export tonnage, and port hubs (Port Hedland ~550 Mtpa throughput) create single-point haulage/berth bottlenecks that magnify production shocks and limit jurisdictional shift options.

Reserve life and development risk

Shorter mine lives and variable orebody continuity at Mount Gibson can force stop-start production, increasing unit costs and margin volatility; Koolan Island operations have previously paused for remediation and sequencing. Replacement via exploration and development needs sustained capex and timely permitting, while project delays directly cut sales volumes and cashflow. Grade variability risks product specification breaches and lower price realizations.

- ASX: MGX listing exposes this operational concentration

- Mine sequencing causes stop-start output

- Sustained capex and permits needed for replacement

- Grade swings can reduce realized prices

Logistics dependence

Mount Gibson’s export model depends on port access, vessel availability and competitive freight; FY2024 shipments ~3.2 Mt underscore exposure to terminal congestion and ship queues.

Disruptions or demurrage — often exceeding US$50,000/day in peak cases — can erode margins versus a 2024 62% Fe index average near US$120/t.

Take-or-pay and capacity constraints limit shipping flexibility while rising fuel/charter costs compress netbacks.

- Export reliance

- Demurrage risk

- Take-or-pay limits

- Fuel/charter pressure

62% Fe exposure (~US$120/t), 2 Mtpa scale and demurrage raise margin risk

Mount Gibson is highly concentrated in 62% Fe spot price exposure (~US$120/t 2024), with small scale (~2 Mtpa production 2024; FY2024 shipments ~3.2 Mt) limiting bargaining power and raising per‑ton cost volatility versus majors (>200 Mtpa). Port/ship constraints (demurrage >US$50k/day) and short mine lives increase stop‑start risk and margin sensitivity.

| Metric | 2024 |

|---|---|

| Production | ~2 Mtpa |

| Shipments | ~3.2 Mt |

| 62% Fe index | ~US$120/t |

| Demurrage (peak) | >US$50,000/day |

Preview Before You Purchase

Mount Gibson Iron SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Mount Gibson Iron’s strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable version ready for immediate download.

Go Beyond the Preview—Access the Full Strategic Report

Mount Gibson Iron’s strategic foothold in premium iron ore and low-cost operations masks exposure to price cycles and logistic bottlenecks; our full SWOT unpacks supply, ESG risks, and growth levers with actionable takeaways. Purchase the complete, editable SWOT report (Word + Excel) to plan, pitch, or invest with confidence.

Strengths

High-grade ore focus

Mount Gibson’s emphasis on high-grade ore — aligned with the 62% Fe benchmark — supports premium pricing and blending value for Asian steel mills. Higher grades lower impurity penalties and reduce energy intensity in steelmaking, aiding mills’ net-zero-by-2050 decarbonization plans. This quality premium cushions margins in down cycles and deepens ties with efficiency-focused mills.

Cost-effective operations

Mount Gibson’s model emphasizes disciplined cost control across mining, processing and logistics, delivering competitive unit costs that bolster margins amid iron ore price swings; operational leanness improves responsiveness to market shifts and supports stronger cash generation for reinvestment and balance sheet resilience.

WA mining footprint

Operations in Western Australia give Mount Gibson access to established mining services, a skilled workforce and export infrastructure concentrated in WA, which underpins Australia’s position as the world’s largest iron ore exporter (~60% of seaborne trade in 2023). Proximity to deep‑water ports shortens shipping to Asia (typically 4–6 days to China), cutting freight costs and lead times. A proven, low‑sovereign‑risk jurisdiction versus many peers supports capital access, while WA’s mining ecosystem enables efficient expansions and maintenance.

Established Asian customer ties

Longstanding supply relationships across Asia, where China accounts for roughly 70% of seaborne iron ore demand (2024), underpin offtake certainty and clearer pricing signals; repeat business from key buyers improves demand visibility and vessel scheduling. These ties enable collaborative product optimisation and trial cargoes and help secure working capital and resilient contract terms through cycles.

- Offtake certainty: long-term Asian buyers

- Demand visibility: repeat cargoes aid scheduling

- Product R&D: trial cargoes with customers

- Finance stability: better working-capital terms

Execution track record

Mount Gibson Iron's execution track record in developing and operating iron ore mines reduces project and ramp-up risk, with institutional mine-planning and grade-control expertise improving recovery and product consistency; data-driven operations continually refine unit cost curves and underpin credibility for permitting, financing and stakeholder engagement.

High-grade 62% Fe drives premium pricing; WA supply, 4-6 day transit China

High‑grade 62% Fe product supports premium pricing and blending value for Asian mills. Disciplined cost control and data-led operations sustain competitive unit costs and margins. WA operations offer low sovereign risk, port access and ~4–6 day shipping to China, backed by long Asian offtake relationships (China ~70% seaborne demand, 2024).

| Metric | Fact |

|---|---|

| Grade | 62% Fe benchmark |

| China demand | ~70% seaborne, 2024 |

| Aus seaborne share | ~60%, 2023 |

| Transit | 4–6 days to China |

What is included in the product

Delivers a strategic overview of Mount Gibson Iron’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position in global iron ore markets.

Provides a concise Mount Gibson Iron SWOT matrix for fast, visual strategy alignment and investor-ready summaries, ideal for executives needing a snapshot of competitive positioning.

Weaknesses

Single-commodity exposure

ASX:MGX derives the vast majority of its income from iron ore, leaving earnings tightly correlated with the 62% Fe CFR China benchmark and amplifying volatility when that index weakens. Limited product mix reduces natural shock absorbers and leaves fewer hedging instruments compared with diversified base‑metal miners. Strategic flexibility is constrained versus multi‑commodity peers that can reallocate capital amid commodity cycles.

Scale disadvantage

Smaller production scale — roughly 2 Mtpa in 2024 versus majors producing >200 Mtpa — increases sensitivity to fixed costs and shipping-rate swings, magnifying per-ton cost volatility.

Limited scale reduces bargaining power with contractors and buyers, constraining contract leverage and premium capture.

Difficulty capturing economies of scale in rail, energy and procurement widens cost differentials in down markets, eroding margins faster than larger peers.

Geographic concentration

Operations concentrated in Western Australia concentrate Mount Gibson Iron’s risk: regional weather, labor shortages and local regulatory shifts can disrupt multiple sites simultaneously. WA accounts for roughly 90% of Australia’s iron ore export tonnage, and port hubs (Port Hedland ~550 Mtpa throughput) create single-point haulage/berth bottlenecks that magnify production shocks and limit jurisdictional shift options.

Reserve life and development risk

Shorter mine lives and variable orebody continuity at Mount Gibson can force stop-start production, increasing unit costs and margin volatility; Koolan Island operations have previously paused for remediation and sequencing. Replacement via exploration and development needs sustained capex and timely permitting, while project delays directly cut sales volumes and cashflow. Grade variability risks product specification breaches and lower price realizations.

- ASX: MGX listing exposes this operational concentration

- Mine sequencing causes stop-start output

- Sustained capex and permits needed for replacement

- Grade swings can reduce realized prices

Logistics dependence

Mount Gibson’s export model depends on port access, vessel availability and competitive freight; FY2024 shipments ~3.2 Mt underscore exposure to terminal congestion and ship queues.

Disruptions or demurrage — often exceeding US$50,000/day in peak cases — can erode margins versus a 2024 62% Fe index average near US$120/t.

Take-or-pay and capacity constraints limit shipping flexibility while rising fuel/charter costs compress netbacks.

- Export reliance

- Demurrage risk

- Take-or-pay limits

- Fuel/charter pressure

62% Fe exposure (~US$120/t), 2 Mtpa scale and demurrage raise margin risk

Mount Gibson is highly concentrated in 62% Fe spot price exposure (~US$120/t 2024), with small scale (~2 Mtpa production 2024; FY2024 shipments ~3.2 Mt) limiting bargaining power and raising per‑ton cost volatility versus majors (>200 Mtpa). Port/ship constraints (demurrage >US$50k/day) and short mine lives increase stop‑start risk and margin sensitivity.

| Metric | 2024 |

|---|---|

| Production | ~2 Mtpa |

| Shipments | ~3.2 Mt |

| 62% Fe index | ~US$120/t |

| Demurrage (peak) | >US$50,000/day |

Preview Before You Purchase

Mount Gibson Iron SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Mount Gibson Iron’s strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable version ready for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Mount Gibson Iron’s strategic foothold in premium iron ore and low-cost operations masks exposure to price cycles and logistic bottlenecks; our full SWOT unpacks supply, ESG risks, and growth levers with actionable takeaways. Purchase the complete, editable SWOT report (Word + Excel) to plan, pitch, or invest with confidence.

Strengths

High-grade ore focus

Mount Gibson’s emphasis on high-grade ore — aligned with the 62% Fe benchmark — supports premium pricing and blending value for Asian steel mills. Higher grades lower impurity penalties and reduce energy intensity in steelmaking, aiding mills’ net-zero-by-2050 decarbonization plans. This quality premium cushions margins in down cycles and deepens ties with efficiency-focused mills.

Cost-effective operations

Mount Gibson’s model emphasizes disciplined cost control across mining, processing and logistics, delivering competitive unit costs that bolster margins amid iron ore price swings; operational leanness improves responsiveness to market shifts and supports stronger cash generation for reinvestment and balance sheet resilience.

WA mining footprint

Operations in Western Australia give Mount Gibson access to established mining services, a skilled workforce and export infrastructure concentrated in WA, which underpins Australia’s position as the world’s largest iron ore exporter (~60% of seaborne trade in 2023). Proximity to deep‑water ports shortens shipping to Asia (typically 4–6 days to China), cutting freight costs and lead times. A proven, low‑sovereign‑risk jurisdiction versus many peers supports capital access, while WA’s mining ecosystem enables efficient expansions and maintenance.

Established Asian customer ties

Longstanding supply relationships across Asia, where China accounts for roughly 70% of seaborne iron ore demand (2024), underpin offtake certainty and clearer pricing signals; repeat business from key buyers improves demand visibility and vessel scheduling. These ties enable collaborative product optimisation and trial cargoes and help secure working capital and resilient contract terms through cycles.

- Offtake certainty: long-term Asian buyers

- Demand visibility: repeat cargoes aid scheduling

- Product R&D: trial cargoes with customers

- Finance stability: better working-capital terms

Execution track record

Mount Gibson Iron's execution track record in developing and operating iron ore mines reduces project and ramp-up risk, with institutional mine-planning and grade-control expertise improving recovery and product consistency; data-driven operations continually refine unit cost curves and underpin credibility for permitting, financing and stakeholder engagement.

High-grade 62% Fe drives premium pricing; WA supply, 4-6 day transit China

High‑grade 62% Fe product supports premium pricing and blending value for Asian mills. Disciplined cost control and data-led operations sustain competitive unit costs and margins. WA operations offer low sovereign risk, port access and ~4–6 day shipping to China, backed by long Asian offtake relationships (China ~70% seaborne demand, 2024).

| Metric | Fact |

|---|---|

| Grade | 62% Fe benchmark |

| China demand | ~70% seaborne, 2024 |

| Aus seaborne share | ~60%, 2023 |

| Transit | 4–6 days to China |

What is included in the product

Delivers a strategic overview of Mount Gibson Iron’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position in global iron ore markets.

Provides a concise Mount Gibson Iron SWOT matrix for fast, visual strategy alignment and investor-ready summaries, ideal for executives needing a snapshot of competitive positioning.

Weaknesses

Single-commodity exposure

ASX:MGX derives the vast majority of its income from iron ore, leaving earnings tightly correlated with the 62% Fe CFR China benchmark and amplifying volatility when that index weakens. Limited product mix reduces natural shock absorbers and leaves fewer hedging instruments compared with diversified base‑metal miners. Strategic flexibility is constrained versus multi‑commodity peers that can reallocate capital amid commodity cycles.

Scale disadvantage

Smaller production scale — roughly 2 Mtpa in 2024 versus majors producing >200 Mtpa — increases sensitivity to fixed costs and shipping-rate swings, magnifying per-ton cost volatility.

Limited scale reduces bargaining power with contractors and buyers, constraining contract leverage and premium capture.

Difficulty capturing economies of scale in rail, energy and procurement widens cost differentials in down markets, eroding margins faster than larger peers.

Geographic concentration

Operations concentrated in Western Australia concentrate Mount Gibson Iron’s risk: regional weather, labor shortages and local regulatory shifts can disrupt multiple sites simultaneously. WA accounts for roughly 90% of Australia’s iron ore export tonnage, and port hubs (Port Hedland ~550 Mtpa throughput) create single-point haulage/berth bottlenecks that magnify production shocks and limit jurisdictional shift options.

Reserve life and development risk

Shorter mine lives and variable orebody continuity at Mount Gibson can force stop-start production, increasing unit costs and margin volatility; Koolan Island operations have previously paused for remediation and sequencing. Replacement via exploration and development needs sustained capex and timely permitting, while project delays directly cut sales volumes and cashflow. Grade variability risks product specification breaches and lower price realizations.

- ASX: MGX listing exposes this operational concentration

- Mine sequencing causes stop-start output

- Sustained capex and permits needed for replacement

- Grade swings can reduce realized prices

Logistics dependence

Mount Gibson’s export model depends on port access, vessel availability and competitive freight; FY2024 shipments ~3.2 Mt underscore exposure to terminal congestion and ship queues.

Disruptions or demurrage — often exceeding US$50,000/day in peak cases — can erode margins versus a 2024 62% Fe index average near US$120/t.

Take-or-pay and capacity constraints limit shipping flexibility while rising fuel/charter costs compress netbacks.

- Export reliance

- Demurrage risk

- Take-or-pay limits

- Fuel/charter pressure

62% Fe exposure (~US$120/t), 2 Mtpa scale and demurrage raise margin risk

Mount Gibson is highly concentrated in 62% Fe spot price exposure (~US$120/t 2024), with small scale (~2 Mtpa production 2024; FY2024 shipments ~3.2 Mt) limiting bargaining power and raising per‑ton cost volatility versus majors (>200 Mtpa). Port/ship constraints (demurrage >US$50k/day) and short mine lives increase stop‑start risk and margin sensitivity.

| Metric | 2024 |

|---|---|

| Production | ~2 Mtpa |

| Shipments | ~3.2 Mt |

| 62% Fe index | ~US$120/t |

| Demurrage (peak) | >US$50,000/day |

Preview Before You Purchase

Mount Gibson Iron SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Mount Gibson Iron’s strengths, weaknesses, opportunities and threats. Purchase unlocks the complete, editable version ready for immediate download.