MultiPlan Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

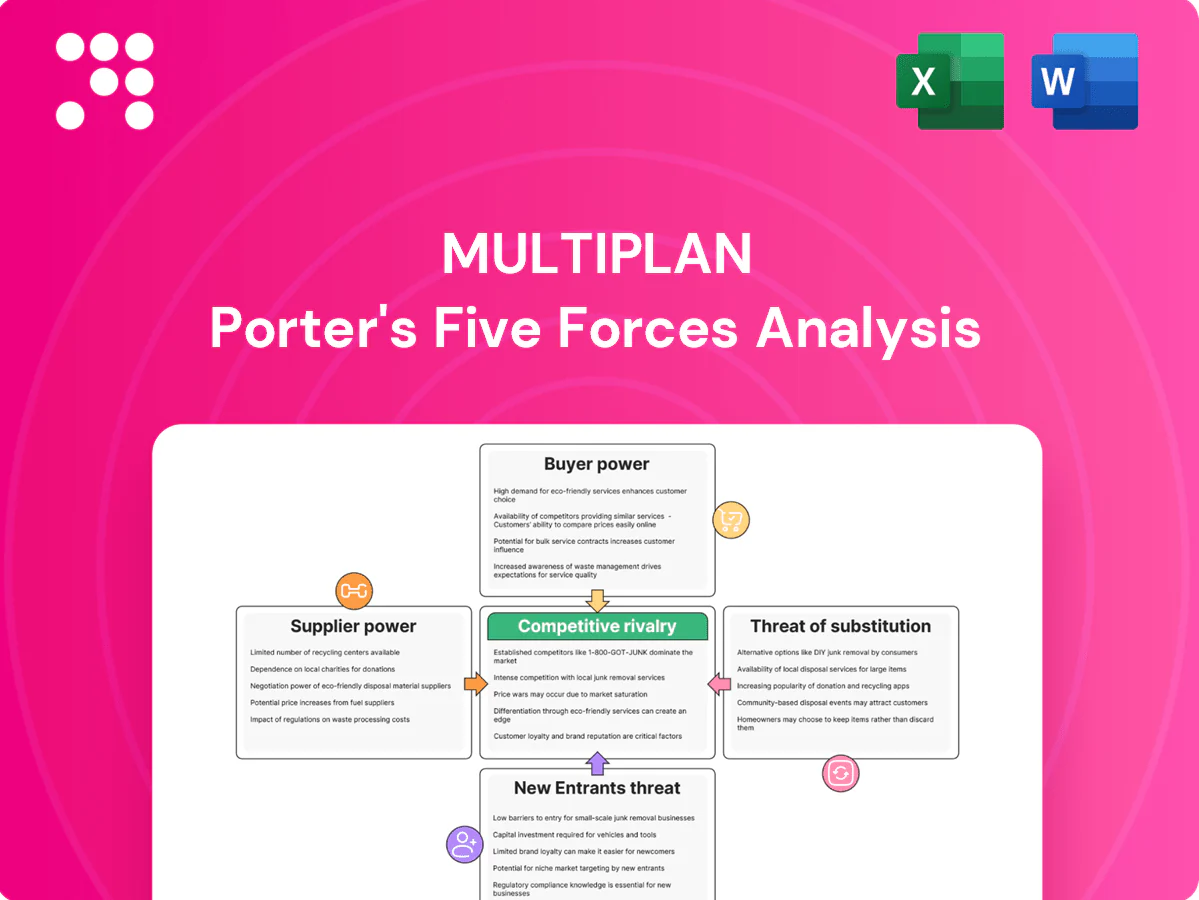

MultiPlan faces intense buyer bargaining and regulatory scrutiny amid a fragmented payer-provider market, while supplier leverage and threat of substitutes remain moderate due to proprietary analytics and network scale. Competitive rivalry is high as tech-enabled cost-management players innovate rapidly. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Concentrated provider systems

Large hospital systems and specialty groups can wield significant leverage over repricing and network terms, especially in concentrated regional markets where a dominant system often controls over half of acute-care beds. Their brands and must-have service lines reduce discount flexibility, pressuring savings yields and forcing MultiPlan into tailored, often facility-specific agreements. MultiPlan must balance access breadth with cost-containment targets.

Data and tech infrastructure vendors

Data and tech vendors exert high supplier power for MultiPlan as cloud, data pipelines and claims-clearing integrations create switching costs and lock-in; AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) dominated global cloud IaaS/PaaS in 2024, concentrating risk. Outages or vendor price hikes can materially disrupt service delivery and margins. Robust SLAs and multi-cloud architectures reduce exposure, but vendor concentration still elevates bargaining leverage.

Proprietary data sources

Proprietary benchmark and reference-price datasets are unique and scarce, and losing access can materially weaken MultiPlan models and client outcomes; market participants noted this risk in 2024 industry reviews. Long-dated licenses and continued in-house data enrichment lower supplier dependency and stabilize inputs. Nevertheless, scarcity preserves supplier negotiating leverage, keeping price and access terms favorable to data vendors.

Specialized analytics talent

Regulatory and arbitration services

Regulatory and arbitration services around the No Surprises Act, effective January 2022, and state IDR processes are niche, letting specialized vendors and legal teams command premium fees and priority access during disputes.

Regulatory change spikes reliance on these suppliers during transitions, while diversifying vendor panels and building internal regulatory and legal expertise reduce supplier leverage.

- No Surprises Act effective Jan 2022

- Specialists command premium advisory fees

- Diversify panels to lower dependency

Hospital leverage, cloud concentration (32%/23%/11%), rising talent costs

Hospitals (dominant systems >50% acute beds in some regions) and specialist groups drive high bargaining power, forcing facility-specific pricing and narrower savings. Cloud vendors concentrate risk (AWS 32%, Azure 23%, GCP 11% in 2024), raising switching costs. Talent and data scarcity (actuary median $111,030 2023; AI engineer median ~$142,000 2024) sustain supplier leverage.

| Supplier | 2024/2023 Metric | Impact |

|---|---|---|

| Hospitals | >50% beds (some markets) | High price leverage |

| Cloud | AWS32% AZ23% GCP11% | Switching cost, outage risk |

| Talent/Data | Actuary $111,030; AI $142k | Retention, cost pressure |

What is included in the product

Concise Porter’s Five Forces analysis tailored to MultiPlan that assesses competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive trends and regulatory risks shaping pricing power and profitability.

MultiPlan Porter's Five Forces Analysis delivers a concise, customizable one-sheet with radar visualization and easy drag-and-drop inputs—perfect for rapid strategic decisions, slide-ready summaries, and seamless integration into broader reports.

Customers Bargaining Power

Highly concentrated payors

National health plans, large TPAs and big self-insured employers—with employer-sponsored coverage covering about 155 million Americans in 2023—concentrate demand and extract pricing concessions from networks like MultiPlan. Their scale and alternative networks enhance pricing pressure and enable RFP-driven procurement that forces competitive concessions. Buyers frequently demand volume-based discounts and outcome guarantees, compressing margins and shifting risk to providers.

Multihoming and in-house builds

Buyers increasingly multihome or insource analytics, reducing switching frictions and boosting bargaining power versus MultiPlan; US health plan administrative costs were about 8% of premiums in 2023, incentivizing cost consolidation. Proof of incremental, non-overlapping savings is essential to justify fees. Recent vendor consolidation waves have driven mid-single-digit fee compression and tighter contract terms.

Performance-tied economics

Savings-based fees and SLAs shift significant revenue risk to MultiPlan, with contingent fees commonly 20–30% of recovered savings, making timely realization critical. Buyers now demand transparent methodologies and appeal outcomes; disputes over attribution can delay payments 60–90 days and raise working capital needs. Robust audit trails and clinical validation — shown to cut dispute rates by roughly 40% in industry studies — help defend the economics.

Interoperability expectations

Clients demand seamless integration with claims systems, EDI, and care management; complexity in these integrations is a common lever to negotiate pricing and SLAs. Industry momentum toward FHIR-based open APIs driven by the 21st Century Cures Act and CMS rules by 2024 has lowered integration friction for many payers. Poor interoperability remains a key churn driver, particularly among large clients with complex stacks.

- Integration complexity = negotiation leverage

- FHIR/open APIs reduce onboarding time

- Claims/EDI/care mgmt connectivity required

- Poor interoperability increases churn risk

Contract length and churn

Multi-year contracts (commonly 3-5 years as of 2024) stabilize MultiPlan revenue but include periodic repricing windows that create negotiating leverage for buyers; underperformance or regulatory shifts can trigger mid-cycle renegotiations and contract adjustments. Competitive pilot programs at renewal amplify buyer bargaining power, so demonstrable, durable savings are critical to retention.

- Contract length: 3-5 years (industry standard, 2024)

- Repricing windows: create renewal leverage

- Renewal pilots: increase competitive pressure

- Durable savings: key to reducing churn

National plans, 155M lives: RFPs drive mid-single-digit fee pressure

Large national plans, TPAs and ~155M employer-covered lives (2023) concentrate demand, driving RFPs and mid-single-digit fee compression. Buyers multihome/insource analytics, push transparency and outcome guarantees, shifting 20–30% contingent-fee risk to MultiPlan and causing 60–90 day payment disputes. FHIR/API adoption (post-2024) lowers integration friction but repricing windows in 3–5yr contracts sustain buyer leverage.

| Metric | Value |

|---|---|

| Employer-covered lives (2023) | ~155M |

| Admin costs of premiums (2023) | ~8% |

| Contingent fees | 20–30% |

| Payment dispute delays | 60–90 days |

| Dispute reduction via audits | ~40% |

Preview Before You Purchase

MultiPlan Porter's Five Forces Analysis

This preview shows the exact MultiPlan Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted analysis covering supplier power, buyer power, competitive rivalry, threats of entry and substitutes as they apply to MultiPlan. Once purchased, you’ll get instant access to this identical file, ready for download and use. No mockups; this is the deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

MultiPlan faces intense buyer bargaining and regulatory scrutiny amid a fragmented payer-provider market, while supplier leverage and threat of substitutes remain moderate due to proprietary analytics and network scale. Competitive rivalry is high as tech-enabled cost-management players innovate rapidly. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Concentrated provider systems

Large hospital systems and specialty groups can wield significant leverage over repricing and network terms, especially in concentrated regional markets where a dominant system often controls over half of acute-care beds. Their brands and must-have service lines reduce discount flexibility, pressuring savings yields and forcing MultiPlan into tailored, often facility-specific agreements. MultiPlan must balance access breadth with cost-containment targets.

Data and tech infrastructure vendors

Data and tech vendors exert high supplier power for MultiPlan as cloud, data pipelines and claims-clearing integrations create switching costs and lock-in; AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) dominated global cloud IaaS/PaaS in 2024, concentrating risk. Outages or vendor price hikes can materially disrupt service delivery and margins. Robust SLAs and multi-cloud architectures reduce exposure, but vendor concentration still elevates bargaining leverage.

Proprietary data sources

Proprietary benchmark and reference-price datasets are unique and scarce, and losing access can materially weaken MultiPlan models and client outcomes; market participants noted this risk in 2024 industry reviews. Long-dated licenses and continued in-house data enrichment lower supplier dependency and stabilize inputs. Nevertheless, scarcity preserves supplier negotiating leverage, keeping price and access terms favorable to data vendors.

Specialized analytics talent

Regulatory and arbitration services

Regulatory and arbitration services around the No Surprises Act, effective January 2022, and state IDR processes are niche, letting specialized vendors and legal teams command premium fees and priority access during disputes.

Regulatory change spikes reliance on these suppliers during transitions, while diversifying vendor panels and building internal regulatory and legal expertise reduce supplier leverage.

- No Surprises Act effective Jan 2022

- Specialists command premium advisory fees

- Diversify panels to lower dependency

Hospital leverage, cloud concentration (32%/23%/11%), rising talent costs

Hospitals (dominant systems >50% acute beds in some regions) and specialist groups drive high bargaining power, forcing facility-specific pricing and narrower savings. Cloud vendors concentrate risk (AWS 32%, Azure 23%, GCP 11% in 2024), raising switching costs. Talent and data scarcity (actuary median $111,030 2023; AI engineer median ~$142,000 2024) sustain supplier leverage.

| Supplier | 2024/2023 Metric | Impact |

|---|---|---|

| Hospitals | >50% beds (some markets) | High price leverage |

| Cloud | AWS32% AZ23% GCP11% | Switching cost, outage risk |

| Talent/Data | Actuary $111,030; AI $142k | Retention, cost pressure |

What is included in the product

Concise Porter’s Five Forces analysis tailored to MultiPlan that assesses competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive trends and regulatory risks shaping pricing power and profitability.

MultiPlan Porter's Five Forces Analysis delivers a concise, customizable one-sheet with radar visualization and easy drag-and-drop inputs—perfect for rapid strategic decisions, slide-ready summaries, and seamless integration into broader reports.

Customers Bargaining Power

Highly concentrated payors

National health plans, large TPAs and big self-insured employers—with employer-sponsored coverage covering about 155 million Americans in 2023—concentrate demand and extract pricing concessions from networks like MultiPlan. Their scale and alternative networks enhance pricing pressure and enable RFP-driven procurement that forces competitive concessions. Buyers frequently demand volume-based discounts and outcome guarantees, compressing margins and shifting risk to providers.

Multihoming and in-house builds

Buyers increasingly multihome or insource analytics, reducing switching frictions and boosting bargaining power versus MultiPlan; US health plan administrative costs were about 8% of premiums in 2023, incentivizing cost consolidation. Proof of incremental, non-overlapping savings is essential to justify fees. Recent vendor consolidation waves have driven mid-single-digit fee compression and tighter contract terms.

Performance-tied economics

Savings-based fees and SLAs shift significant revenue risk to MultiPlan, with contingent fees commonly 20–30% of recovered savings, making timely realization critical. Buyers now demand transparent methodologies and appeal outcomes; disputes over attribution can delay payments 60–90 days and raise working capital needs. Robust audit trails and clinical validation — shown to cut dispute rates by roughly 40% in industry studies — help defend the economics.

Interoperability expectations

Clients demand seamless integration with claims systems, EDI, and care management; complexity in these integrations is a common lever to negotiate pricing and SLAs. Industry momentum toward FHIR-based open APIs driven by the 21st Century Cures Act and CMS rules by 2024 has lowered integration friction for many payers. Poor interoperability remains a key churn driver, particularly among large clients with complex stacks.

- Integration complexity = negotiation leverage

- FHIR/open APIs reduce onboarding time

- Claims/EDI/care mgmt connectivity required

- Poor interoperability increases churn risk

Contract length and churn

Multi-year contracts (commonly 3-5 years as of 2024) stabilize MultiPlan revenue but include periodic repricing windows that create negotiating leverage for buyers; underperformance or regulatory shifts can trigger mid-cycle renegotiations and contract adjustments. Competitive pilot programs at renewal amplify buyer bargaining power, so demonstrable, durable savings are critical to retention.

- Contract length: 3-5 years (industry standard, 2024)

- Repricing windows: create renewal leverage

- Renewal pilots: increase competitive pressure

- Durable savings: key to reducing churn

National plans, 155M lives: RFPs drive mid-single-digit fee pressure

Large national plans, TPAs and ~155M employer-covered lives (2023) concentrate demand, driving RFPs and mid-single-digit fee compression. Buyers multihome/insource analytics, push transparency and outcome guarantees, shifting 20–30% contingent-fee risk to MultiPlan and causing 60–90 day payment disputes. FHIR/API adoption (post-2024) lowers integration friction but repricing windows in 3–5yr contracts sustain buyer leverage.

| Metric | Value |

|---|---|

| Employer-covered lives (2023) | ~155M |

| Admin costs of premiums (2023) | ~8% |

| Contingent fees | 20–30% |

| Payment dispute delays | 60–90 days |

| Dispute reduction via audits | ~40% |

Preview Before You Purchase

MultiPlan Porter's Five Forces Analysis

This preview shows the exact MultiPlan Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted analysis covering supplier power, buyer power, competitive rivalry, threats of entry and substitutes as they apply to MultiPlan. Once purchased, you’ll get instant access to this identical file, ready for download and use. No mockups; this is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

MultiPlan faces intense buyer bargaining and regulatory scrutiny amid a fragmented payer-provider market, while supplier leverage and threat of substitutes remain moderate due to proprietary analytics and network scale. Competitive rivalry is high as tech-enabled cost-management players innovate rapidly. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Concentrated provider systems

Large hospital systems and specialty groups can wield significant leverage over repricing and network terms, especially in concentrated regional markets where a dominant system often controls over half of acute-care beds. Their brands and must-have service lines reduce discount flexibility, pressuring savings yields and forcing MultiPlan into tailored, often facility-specific agreements. MultiPlan must balance access breadth with cost-containment targets.

Data and tech infrastructure vendors

Data and tech vendors exert high supplier power for MultiPlan as cloud, data pipelines and claims-clearing integrations create switching costs and lock-in; AWS (32%), Microsoft Azure (23%) and Google Cloud (11%) dominated global cloud IaaS/PaaS in 2024, concentrating risk. Outages or vendor price hikes can materially disrupt service delivery and margins. Robust SLAs and multi-cloud architectures reduce exposure, but vendor concentration still elevates bargaining leverage.

Proprietary data sources

Proprietary benchmark and reference-price datasets are unique and scarce, and losing access can materially weaken MultiPlan models and client outcomes; market participants noted this risk in 2024 industry reviews. Long-dated licenses and continued in-house data enrichment lower supplier dependency and stabilize inputs. Nevertheless, scarcity preserves supplier negotiating leverage, keeping price and access terms favorable to data vendors.

Specialized analytics talent

Regulatory and arbitration services

Regulatory and arbitration services around the No Surprises Act, effective January 2022, and state IDR processes are niche, letting specialized vendors and legal teams command premium fees and priority access during disputes.

Regulatory change spikes reliance on these suppliers during transitions, while diversifying vendor panels and building internal regulatory and legal expertise reduce supplier leverage.

- No Surprises Act effective Jan 2022

- Specialists command premium advisory fees

- Diversify panels to lower dependency

Hospital leverage, cloud concentration (32%/23%/11%), rising talent costs

Hospitals (dominant systems >50% acute beds in some regions) and specialist groups drive high bargaining power, forcing facility-specific pricing and narrower savings. Cloud vendors concentrate risk (AWS 32%, Azure 23%, GCP 11% in 2024), raising switching costs. Talent and data scarcity (actuary median $111,030 2023; AI engineer median ~$142,000 2024) sustain supplier leverage.

| Supplier | 2024/2023 Metric | Impact |

|---|---|---|

| Hospitals | >50% beds (some markets) | High price leverage |

| Cloud | AWS32% AZ23% GCP11% | Switching cost, outage risk |

| Talent/Data | Actuary $111,030; AI $142k | Retention, cost pressure |

What is included in the product

Concise Porter’s Five Forces analysis tailored to MultiPlan that assesses competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive trends and regulatory risks shaping pricing power and profitability.

MultiPlan Porter's Five Forces Analysis delivers a concise, customizable one-sheet with radar visualization and easy drag-and-drop inputs—perfect for rapid strategic decisions, slide-ready summaries, and seamless integration into broader reports.

Customers Bargaining Power

Highly concentrated payors

National health plans, large TPAs and big self-insured employers—with employer-sponsored coverage covering about 155 million Americans in 2023—concentrate demand and extract pricing concessions from networks like MultiPlan. Their scale and alternative networks enhance pricing pressure and enable RFP-driven procurement that forces competitive concessions. Buyers frequently demand volume-based discounts and outcome guarantees, compressing margins and shifting risk to providers.

Multihoming and in-house builds

Buyers increasingly multihome or insource analytics, reducing switching frictions and boosting bargaining power versus MultiPlan; US health plan administrative costs were about 8% of premiums in 2023, incentivizing cost consolidation. Proof of incremental, non-overlapping savings is essential to justify fees. Recent vendor consolidation waves have driven mid-single-digit fee compression and tighter contract terms.

Performance-tied economics

Savings-based fees and SLAs shift significant revenue risk to MultiPlan, with contingent fees commonly 20–30% of recovered savings, making timely realization critical. Buyers now demand transparent methodologies and appeal outcomes; disputes over attribution can delay payments 60–90 days and raise working capital needs. Robust audit trails and clinical validation — shown to cut dispute rates by roughly 40% in industry studies — help defend the economics.

Interoperability expectations

Clients demand seamless integration with claims systems, EDI, and care management; complexity in these integrations is a common lever to negotiate pricing and SLAs. Industry momentum toward FHIR-based open APIs driven by the 21st Century Cures Act and CMS rules by 2024 has lowered integration friction for many payers. Poor interoperability remains a key churn driver, particularly among large clients with complex stacks.

- Integration complexity = negotiation leverage

- FHIR/open APIs reduce onboarding time

- Claims/EDI/care mgmt connectivity required

- Poor interoperability increases churn risk

Contract length and churn

Multi-year contracts (commonly 3-5 years as of 2024) stabilize MultiPlan revenue but include periodic repricing windows that create negotiating leverage for buyers; underperformance or regulatory shifts can trigger mid-cycle renegotiations and contract adjustments. Competitive pilot programs at renewal amplify buyer bargaining power, so demonstrable, durable savings are critical to retention.

- Contract length: 3-5 years (industry standard, 2024)

- Repricing windows: create renewal leverage

- Renewal pilots: increase competitive pressure

- Durable savings: key to reducing churn

National plans, 155M lives: RFPs drive mid-single-digit fee pressure

Large national plans, TPAs and ~155M employer-covered lives (2023) concentrate demand, driving RFPs and mid-single-digit fee compression. Buyers multihome/insource analytics, push transparency and outcome guarantees, shifting 20–30% contingent-fee risk to MultiPlan and causing 60–90 day payment disputes. FHIR/API adoption (post-2024) lowers integration friction but repricing windows in 3–5yr contracts sustain buyer leverage.

| Metric | Value |

|---|---|

| Employer-covered lives (2023) | ~155M |

| Admin costs of premiums (2023) | ~8% |

| Contingent fees | 20–30% |

| Payment dispute delays | 60–90 days |

| Dispute reduction via audits | ~40% |

Preview Before You Purchase

MultiPlan Porter's Five Forces Analysis

This preview shows the exact MultiPlan Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted analysis covering supplier power, buyer power, competitive rivalry, threats of entry and substitutes as they apply to MultiPlan. Once purchased, you’ll get instant access to this identical file, ready for download and use. No mockups; this is the deliverable.