Murata Manufacturing Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

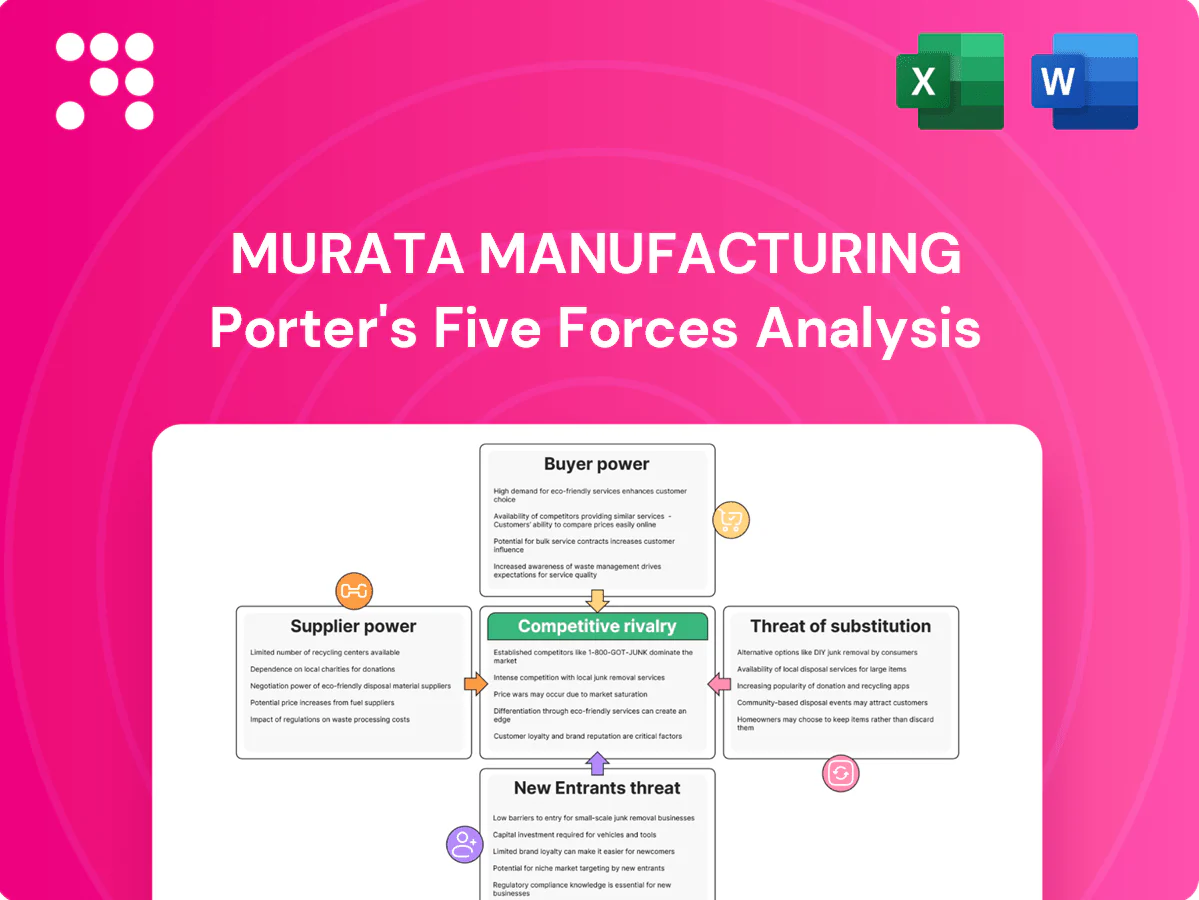

Murata Manufacturing faces intense supplier and buyer dynamics, rising substitute threats in electronics components, and significant scale-driven barriers for new entrants—this snapshot highlights these critical pressures. The full Porter's Five Forces Analysis dissects each force with ratings, visuals, and strategic implications. Unlock the complete report to convert insights into actionable strategy and investment decisions.

Suppliers Bargaining Power

Specialty ceramic inputs

Murata depends on advanced ceramic powders such as barium titanate with tight specs and a small pool of qualified suppliers, which raises supplier leverage over lead times and pricing. Qualification cycles for dielectric powders typically run 6–18 months, slowing vendor switches despite Murata’s in‑house materials science and multi‑sourcing efforts. Net effect: moderate supplier power on critical powders.

Precious and base metals

Palladium, nickel and silver in Murata electrodes expose costs to commodity volatility; silver averaged about $24/oz in 2024, illustrating price sensitivity. Tight purity and particle-size specs narrow qualified vendors, concentrating supply. Long-term contracts and hedging reduced spikes but could not eliminate pass-through cost pressure. In tight markets suppliers retain moderate bargaining power, driven by limited qualified capacity.

Capital equipment dependence

Thin-film, sputtering and high-temp sintering tools for passives come from a limited set of OEMs, with the global semiconductor equipment market ≈$100B in 2024. Unique process recipes and uptime requirements create vendor lock-in and high switching costs tied to customization and SLAs. Service, spares and upgrades—where top OEMs hold >60% share—give suppliers strong bargaining power over pricing and lead times.

Geopolitical and logistics risk

Inputs for Murata sourced across Japan, Europe and China face 2024-era export controls on advanced semiconductors and persistent shipping disruption risks; the Suez Canal remains a chokepoint carrying roughly 12 percent of global trade, any blockage can shift negotiating power to available suppliers. Murata’s diversified footprint across regions buffers shocks but cannot fully neutralize them, so suppliers can embed risk premiums into component pricing, squeezing margins.

- Export controls: 2024 tightening on advanced chip exports to China

- Logistics chokepoint: Suez ~12% global trade

- Diversification: mitigates but does not eliminate supplier leverage

- Pricing: observable risk premiums passed to buyers

Vertical integration buffers

Murata’s deep ceramic and process know-how and backward integration mean it sets specs rather than accepts them, lowering dependency on upstream suppliers and improving bargaining leverage; the company emphasized these strengths in FY2024 investor materials. In‑house R&D and manufacturing control drive better negotiation outcomes with raw‑material and equipment vendors, constraining overall supplier power.

- Backward integration: in‑house fabs and R&D

- Spec‑setting vs spec‑taking

- Reduced supplier dependence

- Stronger procurement leverage in FY2024

Component maker hit by supplier squeeze; tool vendors control >60%

Murata faces moderate supplier power for dielectric powders (6–18 month qualification) and commodities like silver (~$24/oz in 2024) that pass costs through.

Equipment vendors dominate (>60% share in key tool segments; semiconductor equipment market ≈$100B in 2024), raising switching costs.

Diversification and backward integration (FY2024) reduce but do not eliminate supplier leverage; risk premiums persist (Suez ~12% trade).

| Metric | Value |

|---|---|

| Silver price 2024 | $24/oz |

| Equip. market 2024 | $100B |

| Powder qual. time | 6–18 months |

| OEM share | >60% |

| Suez trade | ~12% |

What is included in the product

Tailored exclusively for Murata Manufacturing, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and barriers to entry, identifying substitutes and disruptive threats that shape pricing and profitability. Useable in investor materials or strategy decks, it provides strategic commentary grounded in industry dynamics.

A concise, one-sheet Porter’s Five Forces for Murata—clarifies supplier/customer bargaining power, competitive rivalry, substitutes and entry threats so teams quickly identify pressure points and prioritize mitigation actions for faster, smarter strategic decisions.

Customers Bargaining Power

Concentrated OEM buyers

Smartphone (~1.2 billion units in 2024), PC (~220 million) and automotive (~80 million vehicles) OEMs buy components in massive volume and push aggressive cost-downs; a handful of global accounts can account for double-digit percent revenue shares for suppliers. Their scale boosts negotiation leverage on price and contract terms, while Murata leverages performance differentiation and prioritized, secured supply to protect margins and customer ties.

Design-in switching costs

Passive components and modules undergo rigorous qualification—industry standard in 2024 is typically 12–36 months for automotive and medical applications—so once Murata parts are designed in buyers face high switching costs and reliability risk. This reduces price elasticity mid‑lifecycle as replacement requires requalification and validation. Buyer power weakens significantly after qualification but remains strong at the initial design‑win stage.

Multi-sourcing strategies

In 2024 most OEMs employ dual‑sourcing for MLCCs and modules to ensure continuity, keeping Murata under constant price and lead‑time pressure via approved vendor lists. Murata must align product roadmaps with rivals such as Samsung Electro‑Mechanics, TDK and Yageo to retain share. Buyer power increases when qualified alternative suppliers are readily available.

Performance vs price trade-offs

For high-frequency, miniaturized, and automotive‑grade parts, performance and reliability trump lowest price, allowing Murata to command premiums—Murata reported consolidated net sales of ¥1,352.6 billion in FY2023 (year ended March 2024), driven by advanced components. In commoditized passives buyers push aggressive cost reductions, so buyer power varies sharply by product tier.

- Premium tiers: strong pricing power, higher margins

- Commodities: intense price pressure

- Automotive/hi‑freq: reliability > price

Demand cyclicality

OEM scale squeezes prices; differentiated MLCCs and secure supply preserve margins

Large OEMs (smartphone 1.2bn, PC 220M, auto 80M in 2024) exert strong price and contract pressure; Murata defends margins via performance differentiation and secured supply. Long qualification (12–36 months) raises switching costs after design‑win, reducing buyer leverage mid‑lifecycle. Dual‑sourcing and commoditization boost buyer power in standard MLCCs, while automotive/hi‑freq parts allow Murata premiums (FY2024 revenue ~1.58T JPY).

| Metric | 2024 Value |

|---|---|

| Smartphones | 1.2bn units |

| PCs | 220M units |

| Vehicles | 80M units |

| Murata FY2024 rev | ~1.58T JPY |

Same Document Delivered

Murata Manufacturing Porter's Five Forces Analysis

This preview shows the exact Murata Manufacturing Porter's Five Forces analysis you'll receive upon purchase—complete, professionally formatted, and ready for immediate download. The document evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with concise, actionable insights. No placeholders, no mockups.

A Must-Have Tool for Decision-Makers

Murata Manufacturing faces intense supplier and buyer dynamics, rising substitute threats in electronics components, and significant scale-driven barriers for new entrants—this snapshot highlights these critical pressures. The full Porter's Five Forces Analysis dissects each force with ratings, visuals, and strategic implications. Unlock the complete report to convert insights into actionable strategy and investment decisions.

Suppliers Bargaining Power

Specialty ceramic inputs

Murata depends on advanced ceramic powders such as barium titanate with tight specs and a small pool of qualified suppliers, which raises supplier leverage over lead times and pricing. Qualification cycles for dielectric powders typically run 6–18 months, slowing vendor switches despite Murata’s in‑house materials science and multi‑sourcing efforts. Net effect: moderate supplier power on critical powders.

Precious and base metals

Palladium, nickel and silver in Murata electrodes expose costs to commodity volatility; silver averaged about $24/oz in 2024, illustrating price sensitivity. Tight purity and particle-size specs narrow qualified vendors, concentrating supply. Long-term contracts and hedging reduced spikes but could not eliminate pass-through cost pressure. In tight markets suppliers retain moderate bargaining power, driven by limited qualified capacity.

Capital equipment dependence

Thin-film, sputtering and high-temp sintering tools for passives come from a limited set of OEMs, with the global semiconductor equipment market ≈$100B in 2024. Unique process recipes and uptime requirements create vendor lock-in and high switching costs tied to customization and SLAs. Service, spares and upgrades—where top OEMs hold >60% share—give suppliers strong bargaining power over pricing and lead times.

Geopolitical and logistics risk

Inputs for Murata sourced across Japan, Europe and China face 2024-era export controls on advanced semiconductors and persistent shipping disruption risks; the Suez Canal remains a chokepoint carrying roughly 12 percent of global trade, any blockage can shift negotiating power to available suppliers. Murata’s diversified footprint across regions buffers shocks but cannot fully neutralize them, so suppliers can embed risk premiums into component pricing, squeezing margins.

- Export controls: 2024 tightening on advanced chip exports to China

- Logistics chokepoint: Suez ~12% global trade

- Diversification: mitigates but does not eliminate supplier leverage

- Pricing: observable risk premiums passed to buyers

Vertical integration buffers

Murata’s deep ceramic and process know-how and backward integration mean it sets specs rather than accepts them, lowering dependency on upstream suppliers and improving bargaining leverage; the company emphasized these strengths in FY2024 investor materials. In‑house R&D and manufacturing control drive better negotiation outcomes with raw‑material and equipment vendors, constraining overall supplier power.

- Backward integration: in‑house fabs and R&D

- Spec‑setting vs spec‑taking

- Reduced supplier dependence

- Stronger procurement leverage in FY2024

Component maker hit by supplier squeeze; tool vendors control >60%

Murata faces moderate supplier power for dielectric powders (6–18 month qualification) and commodities like silver (~$24/oz in 2024) that pass costs through.

Equipment vendors dominate (>60% share in key tool segments; semiconductor equipment market ≈$100B in 2024), raising switching costs.

Diversification and backward integration (FY2024) reduce but do not eliminate supplier leverage; risk premiums persist (Suez ~12% trade).

| Metric | Value |

|---|---|

| Silver price 2024 | $24/oz |

| Equip. market 2024 | $100B |

| Powder qual. time | 6–18 months |

| OEM share | >60% |

| Suez trade | ~12% |

What is included in the product

Tailored exclusively for Murata Manufacturing, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and barriers to entry, identifying substitutes and disruptive threats that shape pricing and profitability. Useable in investor materials or strategy decks, it provides strategic commentary grounded in industry dynamics.

A concise, one-sheet Porter’s Five Forces for Murata—clarifies supplier/customer bargaining power, competitive rivalry, substitutes and entry threats so teams quickly identify pressure points and prioritize mitigation actions for faster, smarter strategic decisions.

Customers Bargaining Power

Concentrated OEM buyers

Smartphone (~1.2 billion units in 2024), PC (~220 million) and automotive (~80 million vehicles) OEMs buy components in massive volume and push aggressive cost-downs; a handful of global accounts can account for double-digit percent revenue shares for suppliers. Their scale boosts negotiation leverage on price and contract terms, while Murata leverages performance differentiation and prioritized, secured supply to protect margins and customer ties.

Design-in switching costs

Passive components and modules undergo rigorous qualification—industry standard in 2024 is typically 12–36 months for automotive and medical applications—so once Murata parts are designed in buyers face high switching costs and reliability risk. This reduces price elasticity mid‑lifecycle as replacement requires requalification and validation. Buyer power weakens significantly after qualification but remains strong at the initial design‑win stage.

Multi-sourcing strategies

In 2024 most OEMs employ dual‑sourcing for MLCCs and modules to ensure continuity, keeping Murata under constant price and lead‑time pressure via approved vendor lists. Murata must align product roadmaps with rivals such as Samsung Electro‑Mechanics, TDK and Yageo to retain share. Buyer power increases when qualified alternative suppliers are readily available.

Performance vs price trade-offs

For high-frequency, miniaturized, and automotive‑grade parts, performance and reliability trump lowest price, allowing Murata to command premiums—Murata reported consolidated net sales of ¥1,352.6 billion in FY2023 (year ended March 2024), driven by advanced components. In commoditized passives buyers push aggressive cost reductions, so buyer power varies sharply by product tier.

- Premium tiers: strong pricing power, higher margins

- Commodities: intense price pressure

- Automotive/hi‑freq: reliability > price

Demand cyclicality

OEM scale squeezes prices; differentiated MLCCs and secure supply preserve margins

Large OEMs (smartphone 1.2bn, PC 220M, auto 80M in 2024) exert strong price and contract pressure; Murata defends margins via performance differentiation and secured supply. Long qualification (12–36 months) raises switching costs after design‑win, reducing buyer leverage mid‑lifecycle. Dual‑sourcing and commoditization boost buyer power in standard MLCCs, while automotive/hi‑freq parts allow Murata premiums (FY2024 revenue ~1.58T JPY).

| Metric | 2024 Value |

|---|---|

| Smartphones | 1.2bn units |

| PCs | 220M units |

| Vehicles | 80M units |

| Murata FY2024 rev | ~1.58T JPY |

Same Document Delivered

Murata Manufacturing Porter's Five Forces Analysis

This preview shows the exact Murata Manufacturing Porter's Five Forces analysis you'll receive upon purchase—complete, professionally formatted, and ready for immediate download. The document evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with concise, actionable insights. No placeholders, no mockups.

Description

A Must-Have Tool for Decision-Makers

Murata Manufacturing faces intense supplier and buyer dynamics, rising substitute threats in electronics components, and significant scale-driven barriers for new entrants—this snapshot highlights these critical pressures. The full Porter's Five Forces Analysis dissects each force with ratings, visuals, and strategic implications. Unlock the complete report to convert insights into actionable strategy and investment decisions.

Suppliers Bargaining Power

Specialty ceramic inputs

Murata depends on advanced ceramic powders such as barium titanate with tight specs and a small pool of qualified suppliers, which raises supplier leverage over lead times and pricing. Qualification cycles for dielectric powders typically run 6–18 months, slowing vendor switches despite Murata’s in‑house materials science and multi‑sourcing efforts. Net effect: moderate supplier power on critical powders.

Precious and base metals

Palladium, nickel and silver in Murata electrodes expose costs to commodity volatility; silver averaged about $24/oz in 2024, illustrating price sensitivity. Tight purity and particle-size specs narrow qualified vendors, concentrating supply. Long-term contracts and hedging reduced spikes but could not eliminate pass-through cost pressure. In tight markets suppliers retain moderate bargaining power, driven by limited qualified capacity.

Capital equipment dependence

Thin-film, sputtering and high-temp sintering tools for passives come from a limited set of OEMs, with the global semiconductor equipment market ≈$100B in 2024. Unique process recipes and uptime requirements create vendor lock-in and high switching costs tied to customization and SLAs. Service, spares and upgrades—where top OEMs hold >60% share—give suppliers strong bargaining power over pricing and lead times.

Geopolitical and logistics risk

Inputs for Murata sourced across Japan, Europe and China face 2024-era export controls on advanced semiconductors and persistent shipping disruption risks; the Suez Canal remains a chokepoint carrying roughly 12 percent of global trade, any blockage can shift negotiating power to available suppliers. Murata’s diversified footprint across regions buffers shocks but cannot fully neutralize them, so suppliers can embed risk premiums into component pricing, squeezing margins.

- Export controls: 2024 tightening on advanced chip exports to China

- Logistics chokepoint: Suez ~12% global trade

- Diversification: mitigates but does not eliminate supplier leverage

- Pricing: observable risk premiums passed to buyers

Vertical integration buffers

Murata’s deep ceramic and process know-how and backward integration mean it sets specs rather than accepts them, lowering dependency on upstream suppliers and improving bargaining leverage; the company emphasized these strengths in FY2024 investor materials. In‑house R&D and manufacturing control drive better negotiation outcomes with raw‑material and equipment vendors, constraining overall supplier power.

- Backward integration: in‑house fabs and R&D

- Spec‑setting vs spec‑taking

- Reduced supplier dependence

- Stronger procurement leverage in FY2024

Component maker hit by supplier squeeze; tool vendors control >60%

Murata faces moderate supplier power for dielectric powders (6–18 month qualification) and commodities like silver (~$24/oz in 2024) that pass costs through.

Equipment vendors dominate (>60% share in key tool segments; semiconductor equipment market ≈$100B in 2024), raising switching costs.

Diversification and backward integration (FY2024) reduce but do not eliminate supplier leverage; risk premiums persist (Suez ~12% trade).

| Metric | Value |

|---|---|

| Silver price 2024 | $24/oz |

| Equip. market 2024 | $100B |

| Powder qual. time | 6–18 months |

| OEM share | >60% |

| Suez trade | ~12% |

What is included in the product

Tailored exclusively for Murata Manufacturing, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, and barriers to entry, identifying substitutes and disruptive threats that shape pricing and profitability. Useable in investor materials or strategy decks, it provides strategic commentary grounded in industry dynamics.

A concise, one-sheet Porter’s Five Forces for Murata—clarifies supplier/customer bargaining power, competitive rivalry, substitutes and entry threats so teams quickly identify pressure points and prioritize mitigation actions for faster, smarter strategic decisions.

Customers Bargaining Power

Concentrated OEM buyers

Smartphone (~1.2 billion units in 2024), PC (~220 million) and automotive (~80 million vehicles) OEMs buy components in massive volume and push aggressive cost-downs; a handful of global accounts can account for double-digit percent revenue shares for suppliers. Their scale boosts negotiation leverage on price and contract terms, while Murata leverages performance differentiation and prioritized, secured supply to protect margins and customer ties.

Design-in switching costs

Passive components and modules undergo rigorous qualification—industry standard in 2024 is typically 12–36 months for automotive and medical applications—so once Murata parts are designed in buyers face high switching costs and reliability risk. This reduces price elasticity mid‑lifecycle as replacement requires requalification and validation. Buyer power weakens significantly after qualification but remains strong at the initial design‑win stage.

Multi-sourcing strategies

In 2024 most OEMs employ dual‑sourcing for MLCCs and modules to ensure continuity, keeping Murata under constant price and lead‑time pressure via approved vendor lists. Murata must align product roadmaps with rivals such as Samsung Electro‑Mechanics, TDK and Yageo to retain share. Buyer power increases when qualified alternative suppliers are readily available.

Performance vs price trade-offs

For high-frequency, miniaturized, and automotive‑grade parts, performance and reliability trump lowest price, allowing Murata to command premiums—Murata reported consolidated net sales of ¥1,352.6 billion in FY2023 (year ended March 2024), driven by advanced components. In commoditized passives buyers push aggressive cost reductions, so buyer power varies sharply by product tier.

- Premium tiers: strong pricing power, higher margins

- Commodities: intense price pressure

- Automotive/hi‑freq: reliability > price

Demand cyclicality

OEM scale squeezes prices; differentiated MLCCs and secure supply preserve margins

Large OEMs (smartphone 1.2bn, PC 220M, auto 80M in 2024) exert strong price and contract pressure; Murata defends margins via performance differentiation and secured supply. Long qualification (12–36 months) raises switching costs after design‑win, reducing buyer leverage mid‑lifecycle. Dual‑sourcing and commoditization boost buyer power in standard MLCCs, while automotive/hi‑freq parts allow Murata premiums (FY2024 revenue ~1.58T JPY).

| Metric | 2024 Value |

|---|---|

| Smartphones | 1.2bn units |

| PCs | 220M units |

| Vehicles | 80M units |

| Murata FY2024 rev | ~1.58T JPY |

Same Document Delivered

Murata Manufacturing Porter's Five Forces Analysis

This preview shows the exact Murata Manufacturing Porter's Five Forces analysis you'll receive upon purchase—complete, professionally formatted, and ready for immediate download. The document evaluates competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with concise, actionable insights. No placeholders, no mockups.