Musashi Porter's Five Forces Analysis

From Overview to Strategy Blueprint

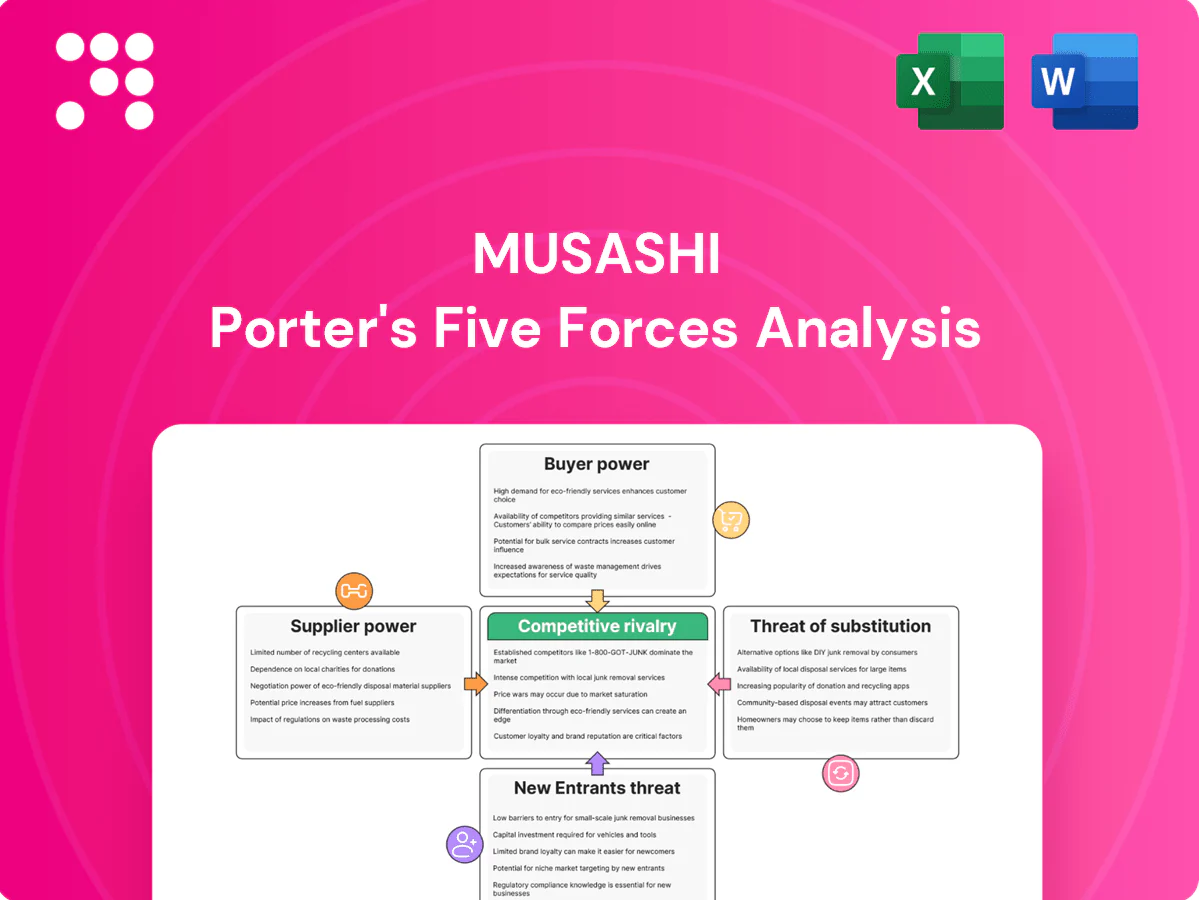

Musashi's Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, rivalry intensity, threat of entrants, and substitute pressures shaping its margins and growth prospects. This brief view identifies key vulnerabilities and strategic levers for management and investors. Unlock the full Porter's Five Forces Analysis to explore Musashi’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty steel dependence

Musashi depends on high-grade alloy and bearing steels supplied by a narrow pool of qualified mills; in 2024 the top five producers held roughly 60% of global bearing-steel capacity, increasing supplier leverage and upward pressure on input prices. Long-term contracts and hedging cut volatility but lock in terms and reduce purchasing flexibility. Any mill quality lapse can trigger recalls and strengthen suppliers via quality gatekeeping.

Tooling and forging dies

Precision forging and gear machining rely on bespoke dies and fixtures from niche toolmakers, with lead times commonly 8–16 weeks and tooling sometimes representing a material share of upfront cost. High switching costs and long delivery cycles give suppliers pricing leverage; co-development improves yield but deepens lock-in. Internal tool rooms and dual sourcing can materially reduce this supplier power by shortening lead times and spreading cost risk.

Energy and logistics intensity

Forging and heat treatment are energy-heavy, and LNG spot prices into Japan fell roughly 50% from 2022 peaks to 2024, but price volatility still exposes Musashi to swings in power and gas costs. Utilities and freight providers, with container rates down about 80% from 2021 peaks to 2024, can pass through costs during tight markets. Regional energy policy shifts alter plant cost curves, and long-term utility contracts plus nearshoring temper but do not eliminate exposure.

Digital/AI stack vendors

Expansion into AI ties Musashi to cloud, data platforms and chip suppliers—2024 Gartner IaaS shares: AWS 32.4%, Microsoft 22.8%, Google 11.7—while NVIDIA FY2024 revenue was $26.97B, underscoring concentrated supplier leverage. Usage-based pricing and vendor ecosystems raise recurring OpEx and margins pressure; interoperability limits and data portability raise switching costs. Internal MLOps lowers but does not eliminate supplier dependence.

- Concentration: major cloud vendors >65% combined (2024)

- Recurring cost: usage-based pricing increases OpEx volatility

- Switching barriers: data portability and proprietary APIs

- Mitigation: MLOps reduces but residual supplier power remains

Quality certifications gating

Automotive-grade materials and processes require IATF 16949 and relevant ISO certifications, which restrict approved inputs to certified suppliers. Certification requirements and PPAP (18 elements, submission levels 1–5) create multi-stage audits that slow supplier changes and increase switching costs. Approved vendor lists therefore institutionalize supplier leverage by narrowing the qualified pool.

- IATF 16949 mandatory for many OEMs

- PPAP: 18 elements, levels 1–5

- Audit/PPAP cycles lengthen onboarding

Concentrated suppliers and cloud concentration maintain high switching costs

Supplier power is high: bearing-steel top‑5 ≈60% capacity (2024), cloud IaaS >65% combined and NVIDIA FY2024 rev $26.97B; certification, long tooling lead times (8–16 weeks) and energy volatility (LNG spot -50% vs 2022) raise switching costs; long contracts, dual sourcing and internal toolrooms/MLOps mitigate but residual leverage persists.

| Supplier | 2024 metric | Mitigation |

|---|---|---|

| Bearing steel | Top‑5 60% | Dual sourcing |

| Cloud/AI | IaaS >65% | MLOps, multi‑cloud |

What is included in the product

Tailored exclusively for Musashi, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and barriers to entry that shape its profitability. It identifies disruptive threats, substitutes, and strategic levers to defend market share and inform investor or management decisions.

Musashi Porter's Five Forces delivers a concise one-sheet mapping of competitive pressures and targeted relief strategies—perfect for rapid decision-making and boardroom use; editable pressure levels and an instant radar chart let you compare scenarios and copy visuals straight into decks.

Customers Bargaining Power

OEM concentration

Automotive and motorcycle OEMs and Tier-1s are concentrated: the top 10 OEMs produce roughly two-thirds of global vehicle volumes, giving them outsized bargaining power over suppliers like Musashi. They routinely press for price-downs, strict quality and on-time delivery; multi-year platform awards provide revenue stability but intensify buyer leverage. Losing a platform can cut supplier volumes materially, often by double-digit percentages.

High switching costs

Once parts are PPAP-approved, buyers face months-long requalification and tooling costs typically $100k–$1M and 6–12 months of lead time, tempering their leverage during a program’s life. At 3–5 year re-sourcing cycles buyers reopen competition aggressively, with 2024 OEM contests leading to double-digit supplier churn in select modules. Performance KPIs still drive 2–5% annual cost reduction targets, keeping pressure despite switching frictions.

Customization and co-design

Customization and co-design of gears and differentials to platform specs strengthens buyers’ leverage since tailored components can be re-specified or sourced elsewhere; co-development embeds Musashi in vehicle architectures but also risks transferring manufacturing know-how to OEMs. Open-book costing and value analysis increase price transparency and intensify margin pressure. Robust engineering support acts as a bargaining chip, used by buyers to extract better terms while Musashi uses it to lock-in partnerships.

JIT and delivery penalties

Automakers enforce strict JIT delivery windows with contractual penalties and chargebacks, shifting variability costs onto suppliers and compressing their margins. Buyers leverage chargebacks and warranty claims—often ranging from tens to hundreds of dollars per incident—creating material cashflow and P&L risk for suppliers. Robust supply-chain execution and on-time delivery are essential to protect margins and avoid multi‑thousand to multi‑million dollar exposures.

- JIT windows enforceable by penalties

- Chargebacks/warranty claims: tens–hundreds USD per incident

- Operational variability cost borne by suppliers

- Strong SCE critical to margin protection

EV transition dynamics

EVs cut multi-speed gear content, letting large OEMs and fleet buyers re-scope modules and push Musashi toward lower-volume, higher-benchmarked parts; global EV sales reached about 14 million in 2024, ~14% of light-vehicle sales, amplifying buyer leverage. Buyers can steer integration to rival Tier-1 e-axles, while Musashi’s e-drive gear pivot can retain share but invites direct price benchmarking; early alignment on OEM EV roadmaps reduces this asymmetry.

- 2024 EV sales ~14M; EV share ~14%

- Risk: OEMs favor integrated e-axles from Tier-1 rivals

- Opportunity: Musashi e-drive gears preserve share but face price pressure

- Mitigation: early OEM roadmap alignment softens customer power

Top-10 OEMs ~66% share; 14% EVs and tooling keep supplier pressure

Top-10 OEMs produce ~66% of global volumes, giving buyers strong price and platform leverage; losing a platform can cut supplier volumes by double digits.

PPAP/tooling costs ($100k–$1M; 6–12 months) and 3–5 year re-sourcing cycles temper short-term switching but annual 2–5% cost targets keep pressure.

2024 EVs ~14M (≈14%); EV drivetrain shifts enable OEMs to re-scope modules, increasing benchmarking and price pressure on Musashi.

| Metric | 2024 |

|---|---|

| Top-10 OEM share | ~66% |

| EV sales | ~14M (14%) |

| Tooling cost | $100k–$1M |

| Cost reduction targets | 2–5% pa |

Same Document Delivered

Musashi Porter's Five Forces Analysis

This Musashi Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or mockups. It contains the complete competitive assessment, ready for download and use the moment you buy. What you see here is the final deliverable, professionally prepared and ready for your decision-making needs.

From Overview to Strategy Blueprint

Musashi's Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, rivalry intensity, threat of entrants, and substitute pressures shaping its margins and growth prospects. This brief view identifies key vulnerabilities and strategic levers for management and investors. Unlock the full Porter's Five Forces Analysis to explore Musashi’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty steel dependence

Musashi depends on high-grade alloy and bearing steels supplied by a narrow pool of qualified mills; in 2024 the top five producers held roughly 60% of global bearing-steel capacity, increasing supplier leverage and upward pressure on input prices. Long-term contracts and hedging cut volatility but lock in terms and reduce purchasing flexibility. Any mill quality lapse can trigger recalls and strengthen suppliers via quality gatekeeping.

Tooling and forging dies

Precision forging and gear machining rely on bespoke dies and fixtures from niche toolmakers, with lead times commonly 8–16 weeks and tooling sometimes representing a material share of upfront cost. High switching costs and long delivery cycles give suppliers pricing leverage; co-development improves yield but deepens lock-in. Internal tool rooms and dual sourcing can materially reduce this supplier power by shortening lead times and spreading cost risk.

Energy and logistics intensity

Forging and heat treatment are energy-heavy, and LNG spot prices into Japan fell roughly 50% from 2022 peaks to 2024, but price volatility still exposes Musashi to swings in power and gas costs. Utilities and freight providers, with container rates down about 80% from 2021 peaks to 2024, can pass through costs during tight markets. Regional energy policy shifts alter plant cost curves, and long-term utility contracts plus nearshoring temper but do not eliminate exposure.

Digital/AI stack vendors

Expansion into AI ties Musashi to cloud, data platforms and chip suppliers—2024 Gartner IaaS shares: AWS 32.4%, Microsoft 22.8%, Google 11.7—while NVIDIA FY2024 revenue was $26.97B, underscoring concentrated supplier leverage. Usage-based pricing and vendor ecosystems raise recurring OpEx and margins pressure; interoperability limits and data portability raise switching costs. Internal MLOps lowers but does not eliminate supplier dependence.

- Concentration: major cloud vendors >65% combined (2024)

- Recurring cost: usage-based pricing increases OpEx volatility

- Switching barriers: data portability and proprietary APIs

- Mitigation: MLOps reduces but residual supplier power remains

Quality certifications gating

Automotive-grade materials and processes require IATF 16949 and relevant ISO certifications, which restrict approved inputs to certified suppliers. Certification requirements and PPAP (18 elements, submission levels 1–5) create multi-stage audits that slow supplier changes and increase switching costs. Approved vendor lists therefore institutionalize supplier leverage by narrowing the qualified pool.

- IATF 16949 mandatory for many OEMs

- PPAP: 18 elements, levels 1–5

- Audit/PPAP cycles lengthen onboarding

Concentrated suppliers and cloud concentration maintain high switching costs

Supplier power is high: bearing-steel top‑5 ≈60% capacity (2024), cloud IaaS >65% combined and NVIDIA FY2024 rev $26.97B; certification, long tooling lead times (8–16 weeks) and energy volatility (LNG spot -50% vs 2022) raise switching costs; long contracts, dual sourcing and internal toolrooms/MLOps mitigate but residual leverage persists.

| Supplier | 2024 metric | Mitigation |

|---|---|---|

| Bearing steel | Top‑5 60% | Dual sourcing |

| Cloud/AI | IaaS >65% | MLOps, multi‑cloud |

What is included in the product

Tailored exclusively for Musashi, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and barriers to entry that shape its profitability. It identifies disruptive threats, substitutes, and strategic levers to defend market share and inform investor or management decisions.

Musashi Porter's Five Forces delivers a concise one-sheet mapping of competitive pressures and targeted relief strategies—perfect for rapid decision-making and boardroom use; editable pressure levels and an instant radar chart let you compare scenarios and copy visuals straight into decks.

Customers Bargaining Power

OEM concentration

Automotive and motorcycle OEMs and Tier-1s are concentrated: the top 10 OEMs produce roughly two-thirds of global vehicle volumes, giving them outsized bargaining power over suppliers like Musashi. They routinely press for price-downs, strict quality and on-time delivery; multi-year platform awards provide revenue stability but intensify buyer leverage. Losing a platform can cut supplier volumes materially, often by double-digit percentages.

High switching costs

Once parts are PPAP-approved, buyers face months-long requalification and tooling costs typically $100k–$1M and 6–12 months of lead time, tempering their leverage during a program’s life. At 3–5 year re-sourcing cycles buyers reopen competition aggressively, with 2024 OEM contests leading to double-digit supplier churn in select modules. Performance KPIs still drive 2–5% annual cost reduction targets, keeping pressure despite switching frictions.

Customization and co-design

Customization and co-design of gears and differentials to platform specs strengthens buyers’ leverage since tailored components can be re-specified or sourced elsewhere; co-development embeds Musashi in vehicle architectures but also risks transferring manufacturing know-how to OEMs. Open-book costing and value analysis increase price transparency and intensify margin pressure. Robust engineering support acts as a bargaining chip, used by buyers to extract better terms while Musashi uses it to lock-in partnerships.

JIT and delivery penalties

Automakers enforce strict JIT delivery windows with contractual penalties and chargebacks, shifting variability costs onto suppliers and compressing their margins. Buyers leverage chargebacks and warranty claims—often ranging from tens to hundreds of dollars per incident—creating material cashflow and P&L risk for suppliers. Robust supply-chain execution and on-time delivery are essential to protect margins and avoid multi‑thousand to multi‑million dollar exposures.

- JIT windows enforceable by penalties

- Chargebacks/warranty claims: tens–hundreds USD per incident

- Operational variability cost borne by suppliers

- Strong SCE critical to margin protection

EV transition dynamics

EVs cut multi-speed gear content, letting large OEMs and fleet buyers re-scope modules and push Musashi toward lower-volume, higher-benchmarked parts; global EV sales reached about 14 million in 2024, ~14% of light-vehicle sales, amplifying buyer leverage. Buyers can steer integration to rival Tier-1 e-axles, while Musashi’s e-drive gear pivot can retain share but invites direct price benchmarking; early alignment on OEM EV roadmaps reduces this asymmetry.

- 2024 EV sales ~14M; EV share ~14%

- Risk: OEMs favor integrated e-axles from Tier-1 rivals

- Opportunity: Musashi e-drive gears preserve share but face price pressure

- Mitigation: early OEM roadmap alignment softens customer power

Top-10 OEMs ~66% share; 14% EVs and tooling keep supplier pressure

Top-10 OEMs produce ~66% of global volumes, giving buyers strong price and platform leverage; losing a platform can cut supplier volumes by double digits.

PPAP/tooling costs ($100k–$1M; 6–12 months) and 3–5 year re-sourcing cycles temper short-term switching but annual 2–5% cost targets keep pressure.

2024 EVs ~14M (≈14%); EV drivetrain shifts enable OEMs to re-scope modules, increasing benchmarking and price pressure on Musashi.

| Metric | 2024 |

|---|---|

| Top-10 OEM share | ~66% |

| EV sales | ~14M (14%) |

| Tooling cost | $100k–$1M |

| Cost reduction targets | 2–5% pa |

Same Document Delivered

Musashi Porter's Five Forces Analysis

This Musashi Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or mockups. It contains the complete competitive assessment, ready for download and use the moment you buy. What you see here is the final deliverable, professionally prepared and ready for your decision-making needs.

Description

From Overview to Strategy Blueprint

Musashi's Porter's Five Forces snapshot highlights supplier leverage, buyer sensitivity, rivalry intensity, threat of entrants, and substitute pressures shaping its margins and growth prospects. This brief view identifies key vulnerabilities and strategic levers for management and investors. Unlock the full Porter's Five Forces Analysis to explore Musashi’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty steel dependence

Musashi depends on high-grade alloy and bearing steels supplied by a narrow pool of qualified mills; in 2024 the top five producers held roughly 60% of global bearing-steel capacity, increasing supplier leverage and upward pressure on input prices. Long-term contracts and hedging cut volatility but lock in terms and reduce purchasing flexibility. Any mill quality lapse can trigger recalls and strengthen suppliers via quality gatekeeping.

Tooling and forging dies

Precision forging and gear machining rely on bespoke dies and fixtures from niche toolmakers, with lead times commonly 8–16 weeks and tooling sometimes representing a material share of upfront cost. High switching costs and long delivery cycles give suppliers pricing leverage; co-development improves yield but deepens lock-in. Internal tool rooms and dual sourcing can materially reduce this supplier power by shortening lead times and spreading cost risk.

Energy and logistics intensity

Forging and heat treatment are energy-heavy, and LNG spot prices into Japan fell roughly 50% from 2022 peaks to 2024, but price volatility still exposes Musashi to swings in power and gas costs. Utilities and freight providers, with container rates down about 80% from 2021 peaks to 2024, can pass through costs during tight markets. Regional energy policy shifts alter plant cost curves, and long-term utility contracts plus nearshoring temper but do not eliminate exposure.

Digital/AI stack vendors

Expansion into AI ties Musashi to cloud, data platforms and chip suppliers—2024 Gartner IaaS shares: AWS 32.4%, Microsoft 22.8%, Google 11.7—while NVIDIA FY2024 revenue was $26.97B, underscoring concentrated supplier leverage. Usage-based pricing and vendor ecosystems raise recurring OpEx and margins pressure; interoperability limits and data portability raise switching costs. Internal MLOps lowers but does not eliminate supplier dependence.

- Concentration: major cloud vendors >65% combined (2024)

- Recurring cost: usage-based pricing increases OpEx volatility

- Switching barriers: data portability and proprietary APIs

- Mitigation: MLOps reduces but residual supplier power remains

Quality certifications gating

Automotive-grade materials and processes require IATF 16949 and relevant ISO certifications, which restrict approved inputs to certified suppliers. Certification requirements and PPAP (18 elements, submission levels 1–5) create multi-stage audits that slow supplier changes and increase switching costs. Approved vendor lists therefore institutionalize supplier leverage by narrowing the qualified pool.

- IATF 16949 mandatory for many OEMs

- PPAP: 18 elements, levels 1–5

- Audit/PPAP cycles lengthen onboarding

Concentrated suppliers and cloud concentration maintain high switching costs

Supplier power is high: bearing-steel top‑5 ≈60% capacity (2024), cloud IaaS >65% combined and NVIDIA FY2024 rev $26.97B; certification, long tooling lead times (8–16 weeks) and energy volatility (LNG spot -50% vs 2022) raise switching costs; long contracts, dual sourcing and internal toolrooms/MLOps mitigate but residual leverage persists.

| Supplier | 2024 metric | Mitigation |

|---|---|---|

| Bearing steel | Top‑5 60% | Dual sourcing |

| Cloud/AI | IaaS >65% | MLOps, multi‑cloud |

What is included in the product

Tailored exclusively for Musashi, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and barriers to entry that shape its profitability. It identifies disruptive threats, substitutes, and strategic levers to defend market share and inform investor or management decisions.

Musashi Porter's Five Forces delivers a concise one-sheet mapping of competitive pressures and targeted relief strategies—perfect for rapid decision-making and boardroom use; editable pressure levels and an instant radar chart let you compare scenarios and copy visuals straight into decks.

Customers Bargaining Power

OEM concentration

Automotive and motorcycle OEMs and Tier-1s are concentrated: the top 10 OEMs produce roughly two-thirds of global vehicle volumes, giving them outsized bargaining power over suppliers like Musashi. They routinely press for price-downs, strict quality and on-time delivery; multi-year platform awards provide revenue stability but intensify buyer leverage. Losing a platform can cut supplier volumes materially, often by double-digit percentages.

High switching costs

Once parts are PPAP-approved, buyers face months-long requalification and tooling costs typically $100k–$1M and 6–12 months of lead time, tempering their leverage during a program’s life. At 3–5 year re-sourcing cycles buyers reopen competition aggressively, with 2024 OEM contests leading to double-digit supplier churn in select modules. Performance KPIs still drive 2–5% annual cost reduction targets, keeping pressure despite switching frictions.

Customization and co-design

Customization and co-design of gears and differentials to platform specs strengthens buyers’ leverage since tailored components can be re-specified or sourced elsewhere; co-development embeds Musashi in vehicle architectures but also risks transferring manufacturing know-how to OEMs. Open-book costing and value analysis increase price transparency and intensify margin pressure. Robust engineering support acts as a bargaining chip, used by buyers to extract better terms while Musashi uses it to lock-in partnerships.

JIT and delivery penalties

Automakers enforce strict JIT delivery windows with contractual penalties and chargebacks, shifting variability costs onto suppliers and compressing their margins. Buyers leverage chargebacks and warranty claims—often ranging from tens to hundreds of dollars per incident—creating material cashflow and P&L risk for suppliers. Robust supply-chain execution and on-time delivery are essential to protect margins and avoid multi‑thousand to multi‑million dollar exposures.

- JIT windows enforceable by penalties

- Chargebacks/warranty claims: tens–hundreds USD per incident

- Operational variability cost borne by suppliers

- Strong SCE critical to margin protection

EV transition dynamics

EVs cut multi-speed gear content, letting large OEMs and fleet buyers re-scope modules and push Musashi toward lower-volume, higher-benchmarked parts; global EV sales reached about 14 million in 2024, ~14% of light-vehicle sales, amplifying buyer leverage. Buyers can steer integration to rival Tier-1 e-axles, while Musashi’s e-drive gear pivot can retain share but invites direct price benchmarking; early alignment on OEM EV roadmaps reduces this asymmetry.

- 2024 EV sales ~14M; EV share ~14%

- Risk: OEMs favor integrated e-axles from Tier-1 rivals

- Opportunity: Musashi e-drive gears preserve share but face price pressure

- Mitigation: early OEM roadmap alignment softens customer power

Top-10 OEMs ~66% share; 14% EVs and tooling keep supplier pressure

Top-10 OEMs produce ~66% of global volumes, giving buyers strong price and platform leverage; losing a platform can cut supplier volumes by double digits.

PPAP/tooling costs ($100k–$1M; 6–12 months) and 3–5 year re-sourcing cycles temper short-term switching but annual 2–5% cost targets keep pressure.

2024 EVs ~14M (≈14%); EV drivetrain shifts enable OEMs to re-scope modules, increasing benchmarking and price pressure on Musashi.

| Metric | 2024 |

|---|---|

| Top-10 OEM share | ~66% |

| EV sales | ~14M (14%) |

| Tooling cost | $100k–$1M |

| Cost reduction targets | 2–5% pa |

Same Document Delivered

Musashi Porter's Five Forces Analysis

This Musashi Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or mockups. It contains the complete competitive assessment, ready for download and use the moment you buy. What you see here is the final deliverable, professionally prepared and ready for your decision-making needs.