Muthoot Finance Business Model Canvas

Gold-backed Lending Canvas: How Branch Networks and Micro-loans Drive Profits

Explore Muthoot Finance’s Business Model Canvas to see how gold-backed lending, dense branch network, and high-margin micro-loans combine to drive revenue and retain customers. This concise overview highlights key partners, cost drivers, and growth levers—download the full Word/Excel canvas for a detailed, actionable roadmap investors and strategists can use today.

Partnerships

Bank lenders and debt capital providers

Relationships with banks and institutional investors supply working capital and term funding that underpin Muthoot Finance’s loan growth; in FY2024 the company continued to rely on bank lines and institutional credit to scale disbursements. Diverse credit lines reduce liquidity risk and funding costs, while securitization and NCD issuances in FY2024 complemented traditional bank borrowings. Stable access to these sources enables competitive pricing and rapid loan disbursements across the network.

Gold appraisers, refiners, and auction houses

Certified appraisers standardize valuation and purity testing, supporting Muthoot Finance’s gold-led book (gold loans ≈95% of loan portfolio; AUM ~₹1.10 lakh crore as of Mar 2024). Refiners and auction partners enable efficient collateral liquidation when needed, cutting slippage. Strong SLAs target compressed recovery timelines, preserving realized prices and underpinning prudent LTVs and portfolio quality.

Insurance underwriters and custodial service providers

All-risk vault and transit insurance protects pledged jewelry—critical in India where households held about 25,000 tonnes of gold (World Gold Council 2023)—with partners offering tailored policies and expedited claims to reduce settlement times. Custodial vendors handle secure vaulting, logistics and regulatory compliance across branch networks. Combined, these partnerships strengthen customer trust and operational resilience.

Fintech, payments, and digital onboarding partners

- Instant payments: UPI/wallets/gateways

- Frictionless onboarding: eKYC/CKYC/video KYC

- Risk control: analytics & fraud tools

- Outcome: lower costs, higher scale

Regulators, credit bureaus, and compliance vendors

Close engagement with RBI, FIU and relevant SROs ensures Muthoot Finance meets licensing and prudential norms; compliance helped preserve its network of over 6,000 branches and a reported loan book ≈₹1.2 lakh crore in 2024. Bureau data underpins credit checks and cross-product underwriting; AML screening and audit partners strengthen governance and reputation protection.

- Regulatory ties: RBI, FIU, SROs

- Bureau reliance: credit & underwriting

- AML/audit partners: governance

- Outcome: license & reputation preservation

Bank-funded gold loans power ₹1.2L cr loan book in 2024; vaulted collateral, fintech rails

Bank and institutional credit (bank lines, NCDs, securitisation) funded rapid disbursements supporting a consolidated loan book ≈₹1.2 lakh crore in 2024. Certified appraisers, refiners and auction partners secure gold-led collateral (gold loans ≈95% of portfolio; AUM ~₹1.10 lakh crore Mar 2024). Vault/transit insurance and custodians protect pledged jewellery amid India gold stock ~25,000 tonnes (WGC 2023). Fintech rails (UPI, eKYC, analytics) cut cost-to-serve and speed onboarding.

| Partner type | Role | 2024 metric |

|---|---|---|

| Banks/Investors | Funding (lines, NCDs) | Loan book ≈₹1.2L cr |

| Appraisers/Refiners | Collateral valuation/liquidation | Gold loans ≈95% |

| Insurers/Custodians | Risk protection | Branches 6,000+ |

What is included in the product

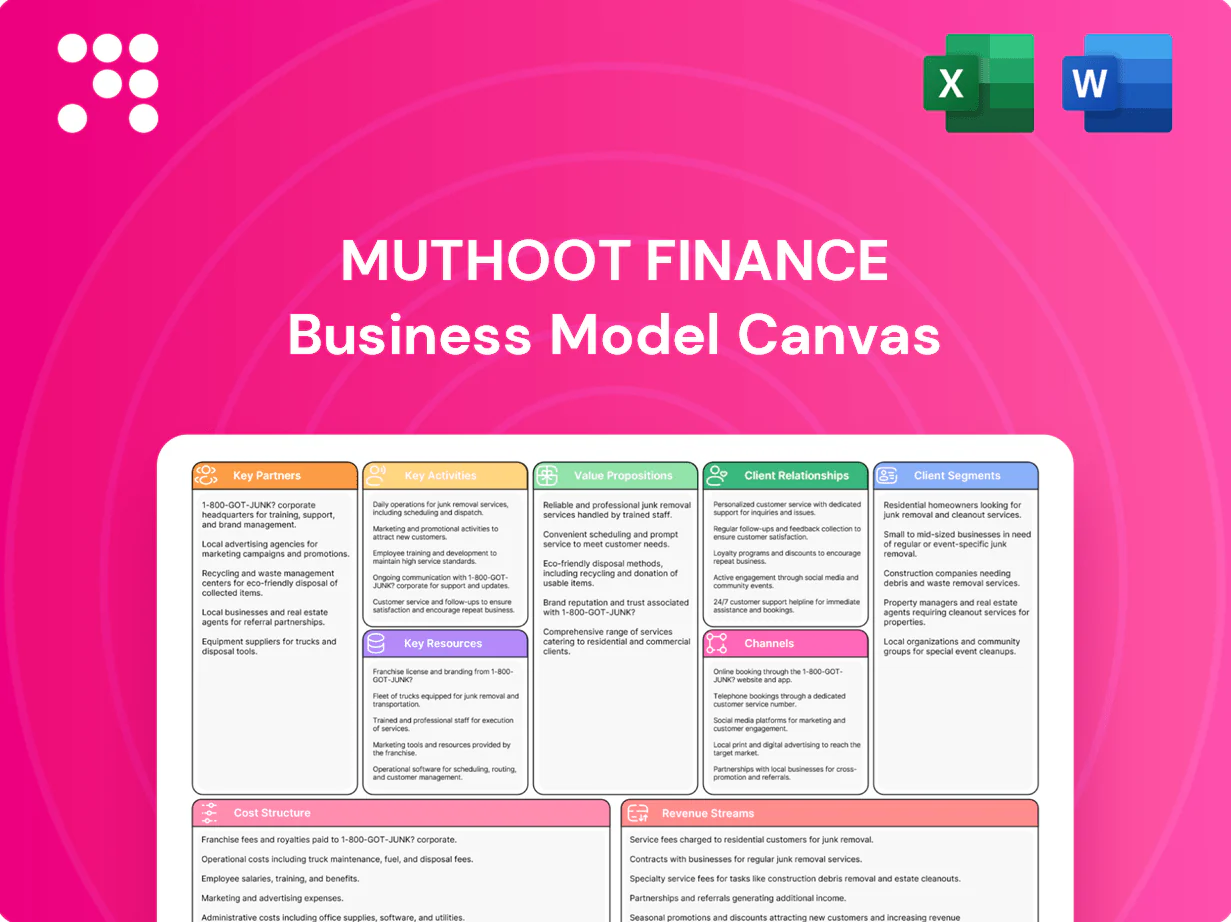

A comprehensive Business Model Canvas for Muthoot Finance covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with competitive advantages, SWOT-linked insights and polished design for investor or internal use.

Condenses Muthoot Finance’s gold-loan-centric value chain, branch network and credit processes into a single editable canvas to relieve time-consuming analysis and alignment pain points; ideal for quick strategy reviews and collaborative planning.

Activities

Loan origination, appraisal, and disbursal

Standardized SOPs enable swift valuation and LTV assessment—gold loans typically sanctioned up to 75% LTV—while digital workflows have compressed turnaround times from days to hours or minutes. Cashless disbursals via NEFT/IMPS/UPI and cash options are tailored to ticket size to balance convenience and risk. Documentation strictly follows KYC and PMLA/AML norms and RBI guidelines to ensure regulatory compliance.

Risk management, monitoring, and collections

Dynamic LTV management adjusts loan-to-value in real time to hedge gold price swings, preserving collateral cover as gold rallied ~8-10% in 2024. Automated reminders and analytics drive early cures, improving recovery timelines across Muthoots 2.7 crore customers (2024). Structured, transparent auctions activate on delinquency to maximize realization and maintain investor confidence. Quarterly portfolio reviews recalibrate policy and pricing based on vintage performance and GNPA trends.

Treasury, ALM, and liquidity management

Match-maturity funding limits interest rate and liquidity risks for Muthoot Finance’s gold loan book, which stood at about Rs 1.5 lakh crore as of March 2024, reducing rollover pressure. Hedging and duration management help stabilize NIMs by smoothing repricing gaps. Diversified funding—bank lines, NCDs, retail deposits—mitigates concentration risk, while regular stress testing sets capital/liquidity buffers and covenant triggers.

Branch operations, vaulting, and security

Branch operations, vaulting and security enforce controlled access, 24/7 surveillance and dual-custody protocols to protect gold assets; regular audits and SOPs drive process discipline across the network. Network planning—over 5,800 branches serving ~28 million customers in 2024—optimizes catchment coverage and throughput. Ongoing staff training raises customer experience and regulatory compliance.

- Controlled access & surveillance

- Dual-custody & audits

- Network planning: ~5,800 branches (2024)

- Training → CX & compliance

Digital platforms, cross-sell, and ecosystem integration

Self-service apps enable renewals, part-payments and closures, reducing branch traffic and turnaround time while boosting customer lifetime value; cross-selling insurance, FX and wealth services raises ARPU by broadening revenue per customer. APIs integrate partners to automate workflows and cut manual reconciliations; data-driven campaigns improve activation and retention through targeted offers and churn prediction.

- Digital renewals: faster closures

- Cross-sell: higher ARPU

- APIs: fewer manual tasks

- Data: better activation & retention

Sub-hour gold loans up to 75% LTV back a Rs 1.5 lakh crore book

Standardized SOPs and digital workflows enable sub-hour gold loan sanctioning up to 75% LTV; cashless disbursal options and strict KYC/PMLA compliance reduce operational risk. Dynamic LTV, auctions and automated collections protect collateral amid ~8–10% gold rally in 2024, supporting recovery across ~28 million customers. Match-maturity funding, hedging and diversified sources back a Rs 1.5 lakh crore loan book (Mar 2024).

| Metric | 2024 |

|---|---|

| Branches | ~5,800 |

| Customers | ~28 million |

| Gold loan book | Rs 1.5 lakh crore |

| Gold price move | ~8–10% |

Preview Before You Purchase

Business Model Canvas

The Muthoot Finance Business Model Canvas you’re previewing is the actual deliverable, not a mockup, and reflects the full structure, content, and formatting of the file you’ll receive after purchase. Upon ordering, you’ll get this exact document instantly—complete and ready to edit, present, or share in Word and Excel formats. No placeholders, no surprises—what you see is what you’ll own.

Gold-backed Lending Canvas: How Branch Networks and Micro-loans Drive Profits

Explore Muthoot Finance’s Business Model Canvas to see how gold-backed lending, dense branch network, and high-margin micro-loans combine to drive revenue and retain customers. This concise overview highlights key partners, cost drivers, and growth levers—download the full Word/Excel canvas for a detailed, actionable roadmap investors and strategists can use today.

Partnerships

Bank lenders and debt capital providers

Relationships with banks and institutional investors supply working capital and term funding that underpin Muthoot Finance’s loan growth; in FY2024 the company continued to rely on bank lines and institutional credit to scale disbursements. Diverse credit lines reduce liquidity risk and funding costs, while securitization and NCD issuances in FY2024 complemented traditional bank borrowings. Stable access to these sources enables competitive pricing and rapid loan disbursements across the network.

Gold appraisers, refiners, and auction houses

Certified appraisers standardize valuation and purity testing, supporting Muthoot Finance’s gold-led book (gold loans ≈95% of loan portfolio; AUM ~₹1.10 lakh crore as of Mar 2024). Refiners and auction partners enable efficient collateral liquidation when needed, cutting slippage. Strong SLAs target compressed recovery timelines, preserving realized prices and underpinning prudent LTVs and portfolio quality.

Insurance underwriters and custodial service providers

All-risk vault and transit insurance protects pledged jewelry—critical in India where households held about 25,000 tonnes of gold (World Gold Council 2023)—with partners offering tailored policies and expedited claims to reduce settlement times. Custodial vendors handle secure vaulting, logistics and regulatory compliance across branch networks. Combined, these partnerships strengthen customer trust and operational resilience.

Fintech, payments, and digital onboarding partners

- Instant payments: UPI/wallets/gateways

- Frictionless onboarding: eKYC/CKYC/video KYC

- Risk control: analytics & fraud tools

- Outcome: lower costs, higher scale

Regulators, credit bureaus, and compliance vendors

Close engagement with RBI, FIU and relevant SROs ensures Muthoot Finance meets licensing and prudential norms; compliance helped preserve its network of over 6,000 branches and a reported loan book ≈₹1.2 lakh crore in 2024. Bureau data underpins credit checks and cross-product underwriting; AML screening and audit partners strengthen governance and reputation protection.

- Regulatory ties: RBI, FIU, SROs

- Bureau reliance: credit & underwriting

- AML/audit partners: governance

- Outcome: license & reputation preservation

Bank-funded gold loans power ₹1.2L cr loan book in 2024; vaulted collateral, fintech rails

Bank and institutional credit (bank lines, NCDs, securitisation) funded rapid disbursements supporting a consolidated loan book ≈₹1.2 lakh crore in 2024. Certified appraisers, refiners and auction partners secure gold-led collateral (gold loans ≈95% of portfolio; AUM ~₹1.10 lakh crore Mar 2024). Vault/transit insurance and custodians protect pledged jewellery amid India gold stock ~25,000 tonnes (WGC 2023). Fintech rails (UPI, eKYC, analytics) cut cost-to-serve and speed onboarding.

| Partner type | Role | 2024 metric |

|---|---|---|

| Banks/Investors | Funding (lines, NCDs) | Loan book ≈₹1.2L cr |

| Appraisers/Refiners | Collateral valuation/liquidation | Gold loans ≈95% |

| Insurers/Custodians | Risk protection | Branches 6,000+ |

What is included in the product

A comprehensive Business Model Canvas for Muthoot Finance covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with competitive advantages, SWOT-linked insights and polished design for investor or internal use.

Condenses Muthoot Finance’s gold-loan-centric value chain, branch network and credit processes into a single editable canvas to relieve time-consuming analysis and alignment pain points; ideal for quick strategy reviews and collaborative planning.

Activities

Loan origination, appraisal, and disbursal

Standardized SOPs enable swift valuation and LTV assessment—gold loans typically sanctioned up to 75% LTV—while digital workflows have compressed turnaround times from days to hours or minutes. Cashless disbursals via NEFT/IMPS/UPI and cash options are tailored to ticket size to balance convenience and risk. Documentation strictly follows KYC and PMLA/AML norms and RBI guidelines to ensure regulatory compliance.

Risk management, monitoring, and collections

Dynamic LTV management adjusts loan-to-value in real time to hedge gold price swings, preserving collateral cover as gold rallied ~8-10% in 2024. Automated reminders and analytics drive early cures, improving recovery timelines across Muthoots 2.7 crore customers (2024). Structured, transparent auctions activate on delinquency to maximize realization and maintain investor confidence. Quarterly portfolio reviews recalibrate policy and pricing based on vintage performance and GNPA trends.

Treasury, ALM, and liquidity management

Match-maturity funding limits interest rate and liquidity risks for Muthoot Finance’s gold loan book, which stood at about Rs 1.5 lakh crore as of March 2024, reducing rollover pressure. Hedging and duration management help stabilize NIMs by smoothing repricing gaps. Diversified funding—bank lines, NCDs, retail deposits—mitigates concentration risk, while regular stress testing sets capital/liquidity buffers and covenant triggers.

Branch operations, vaulting, and security

Branch operations, vaulting and security enforce controlled access, 24/7 surveillance and dual-custody protocols to protect gold assets; regular audits and SOPs drive process discipline across the network. Network planning—over 5,800 branches serving ~28 million customers in 2024—optimizes catchment coverage and throughput. Ongoing staff training raises customer experience and regulatory compliance.

- Controlled access & surveillance

- Dual-custody & audits

- Network planning: ~5,800 branches (2024)

- Training → CX & compliance

Digital platforms, cross-sell, and ecosystem integration

Self-service apps enable renewals, part-payments and closures, reducing branch traffic and turnaround time while boosting customer lifetime value; cross-selling insurance, FX and wealth services raises ARPU by broadening revenue per customer. APIs integrate partners to automate workflows and cut manual reconciliations; data-driven campaigns improve activation and retention through targeted offers and churn prediction.

- Digital renewals: faster closures

- Cross-sell: higher ARPU

- APIs: fewer manual tasks

- Data: better activation & retention

Sub-hour gold loans up to 75% LTV back a Rs 1.5 lakh crore book

Standardized SOPs and digital workflows enable sub-hour gold loan sanctioning up to 75% LTV; cashless disbursal options and strict KYC/PMLA compliance reduce operational risk. Dynamic LTV, auctions and automated collections protect collateral amid ~8–10% gold rally in 2024, supporting recovery across ~28 million customers. Match-maturity funding, hedging and diversified sources back a Rs 1.5 lakh crore loan book (Mar 2024).

| Metric | 2024 |

|---|---|

| Branches | ~5,800 |

| Customers | ~28 million |

| Gold loan book | Rs 1.5 lakh crore |

| Gold price move | ~8–10% |

Preview Before You Purchase

Business Model Canvas

The Muthoot Finance Business Model Canvas you’re previewing is the actual deliverable, not a mockup, and reflects the full structure, content, and formatting of the file you’ll receive after purchase. Upon ordering, you’ll get this exact document instantly—complete and ready to edit, present, or share in Word and Excel formats. No placeholders, no surprises—what you see is what you’ll own.

Description

Gold-backed Lending Canvas: How Branch Networks and Micro-loans Drive Profits

Explore Muthoot Finance’s Business Model Canvas to see how gold-backed lending, dense branch network, and high-margin micro-loans combine to drive revenue and retain customers. This concise overview highlights key partners, cost drivers, and growth levers—download the full Word/Excel canvas for a detailed, actionable roadmap investors and strategists can use today.

Partnerships

Bank lenders and debt capital providers

Relationships with banks and institutional investors supply working capital and term funding that underpin Muthoot Finance’s loan growth; in FY2024 the company continued to rely on bank lines and institutional credit to scale disbursements. Diverse credit lines reduce liquidity risk and funding costs, while securitization and NCD issuances in FY2024 complemented traditional bank borrowings. Stable access to these sources enables competitive pricing and rapid loan disbursements across the network.

Gold appraisers, refiners, and auction houses

Certified appraisers standardize valuation and purity testing, supporting Muthoot Finance’s gold-led book (gold loans ≈95% of loan portfolio; AUM ~₹1.10 lakh crore as of Mar 2024). Refiners and auction partners enable efficient collateral liquidation when needed, cutting slippage. Strong SLAs target compressed recovery timelines, preserving realized prices and underpinning prudent LTVs and portfolio quality.

Insurance underwriters and custodial service providers

All-risk vault and transit insurance protects pledged jewelry—critical in India where households held about 25,000 tonnes of gold (World Gold Council 2023)—with partners offering tailored policies and expedited claims to reduce settlement times. Custodial vendors handle secure vaulting, logistics and regulatory compliance across branch networks. Combined, these partnerships strengthen customer trust and operational resilience.

Fintech, payments, and digital onboarding partners

- Instant payments: UPI/wallets/gateways

- Frictionless onboarding: eKYC/CKYC/video KYC

- Risk control: analytics & fraud tools

- Outcome: lower costs, higher scale

Regulators, credit bureaus, and compliance vendors

Close engagement with RBI, FIU and relevant SROs ensures Muthoot Finance meets licensing and prudential norms; compliance helped preserve its network of over 6,000 branches and a reported loan book ≈₹1.2 lakh crore in 2024. Bureau data underpins credit checks and cross-product underwriting; AML screening and audit partners strengthen governance and reputation protection.

- Regulatory ties: RBI, FIU, SROs

- Bureau reliance: credit & underwriting

- AML/audit partners: governance

- Outcome: license & reputation preservation

Bank-funded gold loans power ₹1.2L cr loan book in 2024; vaulted collateral, fintech rails

Bank and institutional credit (bank lines, NCDs, securitisation) funded rapid disbursements supporting a consolidated loan book ≈₹1.2 lakh crore in 2024. Certified appraisers, refiners and auction partners secure gold-led collateral (gold loans ≈95% of portfolio; AUM ~₹1.10 lakh crore Mar 2024). Vault/transit insurance and custodians protect pledged jewellery amid India gold stock ~25,000 tonnes (WGC 2023). Fintech rails (UPI, eKYC, analytics) cut cost-to-serve and speed onboarding.

| Partner type | Role | 2024 metric |

|---|---|---|

| Banks/Investors | Funding (lines, NCDs) | Loan book ≈₹1.2L cr |

| Appraisers/Refiners | Collateral valuation/liquidation | Gold loans ≈95% |

| Insurers/Custodians | Risk protection | Branches 6,000+ |

What is included in the product

A comprehensive Business Model Canvas for Muthoot Finance covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with competitive advantages, SWOT-linked insights and polished design for investor or internal use.

Condenses Muthoot Finance’s gold-loan-centric value chain, branch network and credit processes into a single editable canvas to relieve time-consuming analysis and alignment pain points; ideal for quick strategy reviews and collaborative planning.

Activities

Loan origination, appraisal, and disbursal

Standardized SOPs enable swift valuation and LTV assessment—gold loans typically sanctioned up to 75% LTV—while digital workflows have compressed turnaround times from days to hours or minutes. Cashless disbursals via NEFT/IMPS/UPI and cash options are tailored to ticket size to balance convenience and risk. Documentation strictly follows KYC and PMLA/AML norms and RBI guidelines to ensure regulatory compliance.

Risk management, monitoring, and collections

Dynamic LTV management adjusts loan-to-value in real time to hedge gold price swings, preserving collateral cover as gold rallied ~8-10% in 2024. Automated reminders and analytics drive early cures, improving recovery timelines across Muthoots 2.7 crore customers (2024). Structured, transparent auctions activate on delinquency to maximize realization and maintain investor confidence. Quarterly portfolio reviews recalibrate policy and pricing based on vintage performance and GNPA trends.

Treasury, ALM, and liquidity management

Match-maturity funding limits interest rate and liquidity risks for Muthoot Finance’s gold loan book, which stood at about Rs 1.5 lakh crore as of March 2024, reducing rollover pressure. Hedging and duration management help stabilize NIMs by smoothing repricing gaps. Diversified funding—bank lines, NCDs, retail deposits—mitigates concentration risk, while regular stress testing sets capital/liquidity buffers and covenant triggers.

Branch operations, vaulting, and security

Branch operations, vaulting and security enforce controlled access, 24/7 surveillance and dual-custody protocols to protect gold assets; regular audits and SOPs drive process discipline across the network. Network planning—over 5,800 branches serving ~28 million customers in 2024—optimizes catchment coverage and throughput. Ongoing staff training raises customer experience and regulatory compliance.

- Controlled access & surveillance

- Dual-custody & audits

- Network planning: ~5,800 branches (2024)

- Training → CX & compliance

Digital platforms, cross-sell, and ecosystem integration

Self-service apps enable renewals, part-payments and closures, reducing branch traffic and turnaround time while boosting customer lifetime value; cross-selling insurance, FX and wealth services raises ARPU by broadening revenue per customer. APIs integrate partners to automate workflows and cut manual reconciliations; data-driven campaigns improve activation and retention through targeted offers and churn prediction.

- Digital renewals: faster closures

- Cross-sell: higher ARPU

- APIs: fewer manual tasks

- Data: better activation & retention

Sub-hour gold loans up to 75% LTV back a Rs 1.5 lakh crore book

Standardized SOPs and digital workflows enable sub-hour gold loan sanctioning up to 75% LTV; cashless disbursal options and strict KYC/PMLA compliance reduce operational risk. Dynamic LTV, auctions and automated collections protect collateral amid ~8–10% gold rally in 2024, supporting recovery across ~28 million customers. Match-maturity funding, hedging and diversified sources back a Rs 1.5 lakh crore loan book (Mar 2024).

| Metric | 2024 |

|---|---|

| Branches | ~5,800 |

| Customers | ~28 million |

| Gold loan book | Rs 1.5 lakh crore |

| Gold price move | ~8–10% |

Preview Before You Purchase

Business Model Canvas

The Muthoot Finance Business Model Canvas you’re previewing is the actual deliverable, not a mockup, and reflects the full structure, content, and formatting of the file you’ll receive after purchase. Upon ordering, you’ll get this exact document instantly—complete and ready to edit, present, or share in Word and Excel formats. No placeholders, no surprises—what you see is what you’ll own.