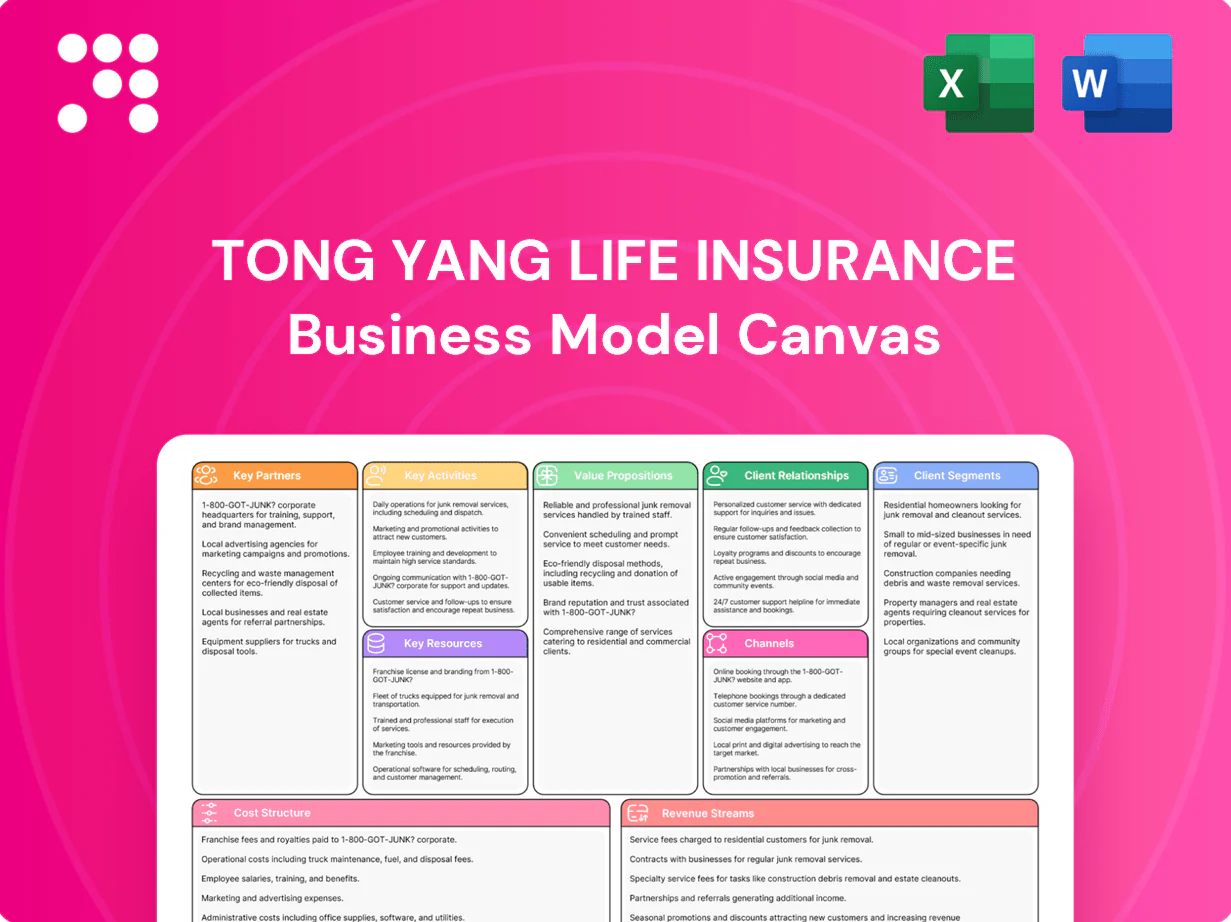

Tong Yang Life Insurance Business Model Canvas

Customer-centric protection via bancassurance, digital channels, and diversified premiums

Discover how Tong Yang Life Insurance creates customer-centric protection, leverages bancassurance and digital channels, and monetizes through diversified premium streams in our Business Model Canvas. This compact, actionable map highlights partnerships, key activities, and cost/revenue levers. Download the full Word/Excel canvas to benchmark strategy, model scenarios, and drive investment decisions.

Partnerships

Global reinsurers

Partnering with top-tier reinsurers spreads mortality, morbidity and catastrophe risk across a broader capital base, tapping into a global reinsurance market with roughly USD 320 billion in annual premiums (2023 Swiss Re estimate). This enables more competitive pricing and greater capacity for large cases, while reinsurers add underwriting expertise and co-develop products. The arrangement strengthens solvency and helps stabilize earnings through cycles.

Bancassurance alliances

Tying up with major Korean banks gives Tong Yang Life access to a retail market within Korea's 51.6 million population (2024) and extensive SME client pools. Bank branches and RM channels efficiently cross-sell protection and annuity products, lifting conversion rates versus direct channels. Regulated data-sharing enables better targeting and higher persistency. Co-branded offerings boost trust and speed to market.

Healthcare provider networks

Direct links with hospitals, clinics and diagnostic centers enable streamlined cashless claims processing, reducing settlement times and administrative costs; industry surveys in 2024 report cashless-network adoption rates above 70% among mid‑to‑large insurers. Preferential provider rates and standardized ICD coding cut loss costs and help detect fraud, lowering claim leakage by an estimated double‑digit percentage in comparable markets. Health‑program alliances deliver wellness and preventive services, improving clinical outcomes and boosting policyholder retention rates year‑over‑year.

Insurtech and IT vendors

- e-KYC / onboarding: faster issuance, lower churn

- Advanced analytics: better underwriting & lapse control

- Cloud/API: accelerated launches, integrations

- Cybersecurity: data protection & compliance

Asset managers and custodians

External asset managers expand Tong Yang Life’s investable universe across fixed income, equities and alternatives, with insurers’ average allocation to alternatives rising to about 8% industry-wide by 2023, enhancing yield and diversification while supporting ALM targets.

Custodians secure assets and enable IFRS 17 (effective 1 Jan 2023) and IFRS 9 reporting, underpinning guaranteed liabilities and bonus capacity via improved transparency and risk controls.

- External managers: broaden asset classes

- Alternatives ~8% (2023)

- Custodians: IFRS 17/9 support

- Outcomes: higher yield, diversification, ALM resilience

Reinsurers, banks & insurtech fuel Korea insurance — USD 320bn, 51.6m

Key partnerships with reinsurers (global reinsurance ~USD 320bn, 2023) bolster capacity and solvency; banks leverage Korea's 51.6m population (2024) for cross‑sell; provider networks (cashless adoption >70%, 2024) cut claims costs; insurtech/analytics (uptake ~65%, 2024) and external managers (alternatives ~8%, 2023) enhance distribution, underwriting, digital issuance and ALM.

| Partner | Role | Key metric |

|---|---|---|

| Reinsurers | Risk capacity | USD 320bn (2023) |

| Banks | Distribution | Population 51.6m (2024) |

| Providers | Claims | Cashless >70% (2024) |

| Insurtech | Digital/analytics | Uptake ~65% (2024) |

| Asset managers | ALM | Alternatives ~8% (2023) |

What is included in the product

A ready-made Business Model Canvas for Tong Yang Life Insurance detailing customer segments, value propositions, channels, revenue models, key activities, partners, resources, cost structure and distribution, with integrated competitive advantages and SWOT insights; ideal for investor presentations, strategic planning, and validation using real-world company context.

High-level view of Tong Yang Life Insurance’s business model with editable cells to pinpoint distribution, underwriting, and retention pain points. Perfect for teams to quickly align on fixes, save hours structuring strategy, and create fast, board-ready deliverables.

Activities

Risk underwriting

Assessing mortality, morbidity and financial risk ensures sustainable pricing by aligning premiums to expected claim patterns and reserve needs. Use of medical data, predictive scoring models and reinsurer guidelines improves risk selection and pricing accuracy. Automated underwriting accelerates issuance to minutes while preserving controls through rule-based overrides and audit trails, and continuous model refinement reduces anti-selection over time.

Product development

Designing life, health, accident and annuity solutions tailored to Korean needs, targeting an ageing population where 65+ reached about 17.5% in 2023. Products incorporate riders, guarantees and wellness benefits to differentiate and boost persistency. Pricing and testing are calibrated under IFRS 17 (effective 2023) and Korea’s regulatory solvency expectations (regulatory margin ratio benchmark ~100%). Rapid iteration is driven by monthly agent and customer feedback loops.

Distribution management

Recruiting, training and incentivizing a salaried and agency force focuses on quality sales through competency-based onboarding, regular certification and performance-linked commissions to reduce lapses.

Managing bancassurance ties emphasizes SLA-driven service standards, joint KPIs and monthly scorecards to sustain partner retention and referral flows.

Digital funnels are optimized via conversion-tracking, channel-level marketing ROI and A/B testing to lower acquisition cost and boost online lead-to-policy rates, while monitoring persistency, cross-sell and complaint ratios through dashboards and regulatory reporting.

Claims and servicing

Fast, fair claims settlement builds trust and reduced churn, with industry surveys in 2024 showing service speed drives retention; Tong Yang targets rapid resolution to protect persistency. Robust fraud detection and medical review—industry fraud estimates ~5–10% (2024)—safeguard loss ratios and margins. Omnichannel servicing handles endorsements, policy loans and surrenders; VOC loops (NPS/CSAT) feed continuous process improvement.

- Retention impact: speed-driven

- Fraud control: ~5–10% industry estimate (2024)

- Omnichannel: endorsements, loans, surrenders

- VOC: NPS/CSAT closed-loop

ALM and investment

ALM and investment match asset durations and cash flows to policy liabilities to stabilize solvency, aligning with the regulatory minimum risk-based capital ratio of 100% required by many Asian regulators in 2024.

Tactical allocation targets incremental yield within Tong Yang Life’s approved risk appetite, while hedging interest-rate and equity exposures reduces earnings volatility and protects surplus; governance ensures compliance with local rules and internal limits.

- Duration matching: liability-driven investments

- Tactical: yield-seeking within risk limits

- Hedging: IR and equity derivatives

- Governance: regulatory and internal oversight

Mortality pricing, IFRS 17 & ALM hedging to protect surplus — 17.5%

Underwriting, product design, distribution and claims operations focus on mortality/morbidity pricing, IFRS 17-compliant product testing, channel management and fast claims with fraud controls to protect persistency. ALM matches asset cash flows to liabilities while tactical allocation and hedging control surplus volatility. Recruitment, training and partner SLAs sustain sales quality and retention.

| Metric | Value |

|---|---|

| 65+ population (Korea, 2023) | 17.5% |

| IFRS 17 effective | 2023 |

| Industry fraud estimate (2024) | 5–10% |

| Regulatory margin ratio (benchmark, 2024) | ~100% |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual Tong Yang Life Insurance Business Model Canvas, not a mockup, and it contains the same structured content you’ll receive after purchase. Upon completing your order you’ll instantly get this exact file—fully editable and formatted for immediate use in Word and Excel. No placeholders, no changes: what you see is what you’ll own.

Customer-centric protection via bancassurance, digital channels, and diversified premiums

Discover how Tong Yang Life Insurance creates customer-centric protection, leverages bancassurance and digital channels, and monetizes through diversified premium streams in our Business Model Canvas. This compact, actionable map highlights partnerships, key activities, and cost/revenue levers. Download the full Word/Excel canvas to benchmark strategy, model scenarios, and drive investment decisions.

Partnerships

Global reinsurers

Partnering with top-tier reinsurers spreads mortality, morbidity and catastrophe risk across a broader capital base, tapping into a global reinsurance market with roughly USD 320 billion in annual premiums (2023 Swiss Re estimate). This enables more competitive pricing and greater capacity for large cases, while reinsurers add underwriting expertise and co-develop products. The arrangement strengthens solvency and helps stabilize earnings through cycles.

Bancassurance alliances

Tying up with major Korean banks gives Tong Yang Life access to a retail market within Korea's 51.6 million population (2024) and extensive SME client pools. Bank branches and RM channels efficiently cross-sell protection and annuity products, lifting conversion rates versus direct channels. Regulated data-sharing enables better targeting and higher persistency. Co-branded offerings boost trust and speed to market.

Healthcare provider networks

Direct links with hospitals, clinics and diagnostic centers enable streamlined cashless claims processing, reducing settlement times and administrative costs; industry surveys in 2024 report cashless-network adoption rates above 70% among mid‑to‑large insurers. Preferential provider rates and standardized ICD coding cut loss costs and help detect fraud, lowering claim leakage by an estimated double‑digit percentage in comparable markets. Health‑program alliances deliver wellness and preventive services, improving clinical outcomes and boosting policyholder retention rates year‑over‑year.

Insurtech and IT vendors

- e-KYC / onboarding: faster issuance, lower churn

- Advanced analytics: better underwriting & lapse control

- Cloud/API: accelerated launches, integrations

- Cybersecurity: data protection & compliance

Asset managers and custodians

External asset managers expand Tong Yang Life’s investable universe across fixed income, equities and alternatives, with insurers’ average allocation to alternatives rising to about 8% industry-wide by 2023, enhancing yield and diversification while supporting ALM targets.

Custodians secure assets and enable IFRS 17 (effective 1 Jan 2023) and IFRS 9 reporting, underpinning guaranteed liabilities and bonus capacity via improved transparency and risk controls.

- External managers: broaden asset classes

- Alternatives ~8% (2023)

- Custodians: IFRS 17/9 support

- Outcomes: higher yield, diversification, ALM resilience

Reinsurers, banks & insurtech fuel Korea insurance — USD 320bn, 51.6m

Key partnerships with reinsurers (global reinsurance ~USD 320bn, 2023) bolster capacity and solvency; banks leverage Korea's 51.6m population (2024) for cross‑sell; provider networks (cashless adoption >70%, 2024) cut claims costs; insurtech/analytics (uptake ~65%, 2024) and external managers (alternatives ~8%, 2023) enhance distribution, underwriting, digital issuance and ALM.

| Partner | Role | Key metric |

|---|---|---|

| Reinsurers | Risk capacity | USD 320bn (2023) |

| Banks | Distribution | Population 51.6m (2024) |

| Providers | Claims | Cashless >70% (2024) |

| Insurtech | Digital/analytics | Uptake ~65% (2024) |

| Asset managers | ALM | Alternatives ~8% (2023) |

What is included in the product

A ready-made Business Model Canvas for Tong Yang Life Insurance detailing customer segments, value propositions, channels, revenue models, key activities, partners, resources, cost structure and distribution, with integrated competitive advantages and SWOT insights; ideal for investor presentations, strategic planning, and validation using real-world company context.

High-level view of Tong Yang Life Insurance’s business model with editable cells to pinpoint distribution, underwriting, and retention pain points. Perfect for teams to quickly align on fixes, save hours structuring strategy, and create fast, board-ready deliverables.

Activities

Risk underwriting

Assessing mortality, morbidity and financial risk ensures sustainable pricing by aligning premiums to expected claim patterns and reserve needs. Use of medical data, predictive scoring models and reinsurer guidelines improves risk selection and pricing accuracy. Automated underwriting accelerates issuance to minutes while preserving controls through rule-based overrides and audit trails, and continuous model refinement reduces anti-selection over time.

Product development

Designing life, health, accident and annuity solutions tailored to Korean needs, targeting an ageing population where 65+ reached about 17.5% in 2023. Products incorporate riders, guarantees and wellness benefits to differentiate and boost persistency. Pricing and testing are calibrated under IFRS 17 (effective 2023) and Korea’s regulatory solvency expectations (regulatory margin ratio benchmark ~100%). Rapid iteration is driven by monthly agent and customer feedback loops.

Distribution management

Recruiting, training and incentivizing a salaried and agency force focuses on quality sales through competency-based onboarding, regular certification and performance-linked commissions to reduce lapses.

Managing bancassurance ties emphasizes SLA-driven service standards, joint KPIs and monthly scorecards to sustain partner retention and referral flows.

Digital funnels are optimized via conversion-tracking, channel-level marketing ROI and A/B testing to lower acquisition cost and boost online lead-to-policy rates, while monitoring persistency, cross-sell and complaint ratios through dashboards and regulatory reporting.

Claims and servicing

Fast, fair claims settlement builds trust and reduced churn, with industry surveys in 2024 showing service speed drives retention; Tong Yang targets rapid resolution to protect persistency. Robust fraud detection and medical review—industry fraud estimates ~5–10% (2024)—safeguard loss ratios and margins. Omnichannel servicing handles endorsements, policy loans and surrenders; VOC loops (NPS/CSAT) feed continuous process improvement.

- Retention impact: speed-driven

- Fraud control: ~5–10% industry estimate (2024)

- Omnichannel: endorsements, loans, surrenders

- VOC: NPS/CSAT closed-loop

ALM and investment

ALM and investment match asset durations and cash flows to policy liabilities to stabilize solvency, aligning with the regulatory minimum risk-based capital ratio of 100% required by many Asian regulators in 2024.

Tactical allocation targets incremental yield within Tong Yang Life’s approved risk appetite, while hedging interest-rate and equity exposures reduces earnings volatility and protects surplus; governance ensures compliance with local rules and internal limits.

- Duration matching: liability-driven investments

- Tactical: yield-seeking within risk limits

- Hedging: IR and equity derivatives

- Governance: regulatory and internal oversight

Mortality pricing, IFRS 17 & ALM hedging to protect surplus — 17.5%

Underwriting, product design, distribution and claims operations focus on mortality/morbidity pricing, IFRS 17-compliant product testing, channel management and fast claims with fraud controls to protect persistency. ALM matches asset cash flows to liabilities while tactical allocation and hedging control surplus volatility. Recruitment, training and partner SLAs sustain sales quality and retention.

| Metric | Value |

|---|---|

| 65+ population (Korea, 2023) | 17.5% |

| IFRS 17 effective | 2023 |

| Industry fraud estimate (2024) | 5–10% |

| Regulatory margin ratio (benchmark, 2024) | ~100% |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual Tong Yang Life Insurance Business Model Canvas, not a mockup, and it contains the same structured content you’ll receive after purchase. Upon completing your order you’ll instantly get this exact file—fully editable and formatted for immediate use in Word and Excel. No placeholders, no changes: what you see is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Customer-centric protection via bancassurance, digital channels, and diversified premiums

Discover how Tong Yang Life Insurance creates customer-centric protection, leverages bancassurance and digital channels, and monetizes through diversified premium streams in our Business Model Canvas. This compact, actionable map highlights partnerships, key activities, and cost/revenue levers. Download the full Word/Excel canvas to benchmark strategy, model scenarios, and drive investment decisions.

Partnerships

Global reinsurers

Partnering with top-tier reinsurers spreads mortality, morbidity and catastrophe risk across a broader capital base, tapping into a global reinsurance market with roughly USD 320 billion in annual premiums (2023 Swiss Re estimate). This enables more competitive pricing and greater capacity for large cases, while reinsurers add underwriting expertise and co-develop products. The arrangement strengthens solvency and helps stabilize earnings through cycles.

Bancassurance alliances

Tying up with major Korean banks gives Tong Yang Life access to a retail market within Korea's 51.6 million population (2024) and extensive SME client pools. Bank branches and RM channels efficiently cross-sell protection and annuity products, lifting conversion rates versus direct channels. Regulated data-sharing enables better targeting and higher persistency. Co-branded offerings boost trust and speed to market.

Healthcare provider networks

Direct links with hospitals, clinics and diagnostic centers enable streamlined cashless claims processing, reducing settlement times and administrative costs; industry surveys in 2024 report cashless-network adoption rates above 70% among mid‑to‑large insurers. Preferential provider rates and standardized ICD coding cut loss costs and help detect fraud, lowering claim leakage by an estimated double‑digit percentage in comparable markets. Health‑program alliances deliver wellness and preventive services, improving clinical outcomes and boosting policyholder retention rates year‑over‑year.

Insurtech and IT vendors

- e-KYC / onboarding: faster issuance, lower churn

- Advanced analytics: better underwriting & lapse control

- Cloud/API: accelerated launches, integrations

- Cybersecurity: data protection & compliance

Asset managers and custodians

External asset managers expand Tong Yang Life’s investable universe across fixed income, equities and alternatives, with insurers’ average allocation to alternatives rising to about 8% industry-wide by 2023, enhancing yield and diversification while supporting ALM targets.

Custodians secure assets and enable IFRS 17 (effective 1 Jan 2023) and IFRS 9 reporting, underpinning guaranteed liabilities and bonus capacity via improved transparency and risk controls.

- External managers: broaden asset classes

- Alternatives ~8% (2023)

- Custodians: IFRS 17/9 support

- Outcomes: higher yield, diversification, ALM resilience

Reinsurers, banks & insurtech fuel Korea insurance — USD 320bn, 51.6m

Key partnerships with reinsurers (global reinsurance ~USD 320bn, 2023) bolster capacity and solvency; banks leverage Korea's 51.6m population (2024) for cross‑sell; provider networks (cashless adoption >70%, 2024) cut claims costs; insurtech/analytics (uptake ~65%, 2024) and external managers (alternatives ~8%, 2023) enhance distribution, underwriting, digital issuance and ALM.

| Partner | Role | Key metric |

|---|---|---|

| Reinsurers | Risk capacity | USD 320bn (2023) |

| Banks | Distribution | Population 51.6m (2024) |

| Providers | Claims | Cashless >70% (2024) |

| Insurtech | Digital/analytics | Uptake ~65% (2024) |

| Asset managers | ALM | Alternatives ~8% (2023) |

What is included in the product

A ready-made Business Model Canvas for Tong Yang Life Insurance detailing customer segments, value propositions, channels, revenue models, key activities, partners, resources, cost structure and distribution, with integrated competitive advantages and SWOT insights; ideal for investor presentations, strategic planning, and validation using real-world company context.

High-level view of Tong Yang Life Insurance’s business model with editable cells to pinpoint distribution, underwriting, and retention pain points. Perfect for teams to quickly align on fixes, save hours structuring strategy, and create fast, board-ready deliverables.

Activities

Risk underwriting

Assessing mortality, morbidity and financial risk ensures sustainable pricing by aligning premiums to expected claim patterns and reserve needs. Use of medical data, predictive scoring models and reinsurer guidelines improves risk selection and pricing accuracy. Automated underwriting accelerates issuance to minutes while preserving controls through rule-based overrides and audit trails, and continuous model refinement reduces anti-selection over time.

Product development

Designing life, health, accident and annuity solutions tailored to Korean needs, targeting an ageing population where 65+ reached about 17.5% in 2023. Products incorporate riders, guarantees and wellness benefits to differentiate and boost persistency. Pricing and testing are calibrated under IFRS 17 (effective 2023) and Korea’s regulatory solvency expectations (regulatory margin ratio benchmark ~100%). Rapid iteration is driven by monthly agent and customer feedback loops.

Distribution management

Recruiting, training and incentivizing a salaried and agency force focuses on quality sales through competency-based onboarding, regular certification and performance-linked commissions to reduce lapses.

Managing bancassurance ties emphasizes SLA-driven service standards, joint KPIs and monthly scorecards to sustain partner retention and referral flows.

Digital funnels are optimized via conversion-tracking, channel-level marketing ROI and A/B testing to lower acquisition cost and boost online lead-to-policy rates, while monitoring persistency, cross-sell and complaint ratios through dashboards and regulatory reporting.

Claims and servicing

Fast, fair claims settlement builds trust and reduced churn, with industry surveys in 2024 showing service speed drives retention; Tong Yang targets rapid resolution to protect persistency. Robust fraud detection and medical review—industry fraud estimates ~5–10% (2024)—safeguard loss ratios and margins. Omnichannel servicing handles endorsements, policy loans and surrenders; VOC loops (NPS/CSAT) feed continuous process improvement.

- Retention impact: speed-driven

- Fraud control: ~5–10% industry estimate (2024)

- Omnichannel: endorsements, loans, surrenders

- VOC: NPS/CSAT closed-loop

ALM and investment

ALM and investment match asset durations and cash flows to policy liabilities to stabilize solvency, aligning with the regulatory minimum risk-based capital ratio of 100% required by many Asian regulators in 2024.

Tactical allocation targets incremental yield within Tong Yang Life’s approved risk appetite, while hedging interest-rate and equity exposures reduces earnings volatility and protects surplus; governance ensures compliance with local rules and internal limits.

- Duration matching: liability-driven investments

- Tactical: yield-seeking within risk limits

- Hedging: IR and equity derivatives

- Governance: regulatory and internal oversight

Mortality pricing, IFRS 17 & ALM hedging to protect surplus — 17.5%

Underwriting, product design, distribution and claims operations focus on mortality/morbidity pricing, IFRS 17-compliant product testing, channel management and fast claims with fraud controls to protect persistency. ALM matches asset cash flows to liabilities while tactical allocation and hedging control surplus volatility. Recruitment, training and partner SLAs sustain sales quality and retention.

| Metric | Value |

|---|---|

| 65+ population (Korea, 2023) | 17.5% |

| IFRS 17 effective | 2023 |

| Industry fraud estimate (2024) | 5–10% |

| Regulatory margin ratio (benchmark, 2024) | ~100% |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual Tong Yang Life Insurance Business Model Canvas, not a mockup, and it contains the same structured content you’ll receive after purchase. Upon completing your order you’ll instantly get this exact file—fully editable and formatted for immediate use in Word and Excel. No placeholders, no changes: what you see is what you’ll own.