Mycronic Boston Consulting Group Matrix

Unlock Strategic Clarity

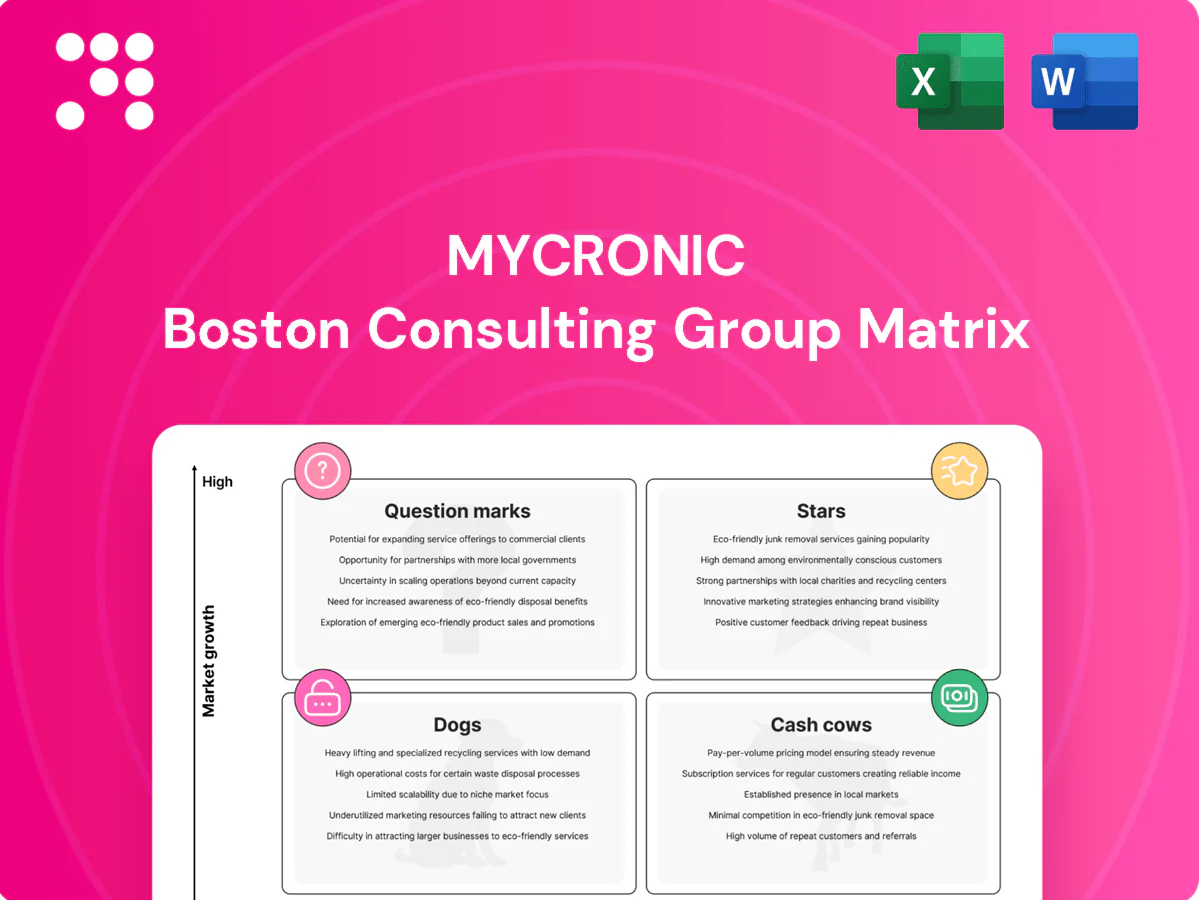

Get a clear snapshot of Mycronic’s product portfolio with this BCG Matrix preview—see where the Stars, Cash Cows, Dogs, and Question Marks sit and why it matters. The full BCG Matrix delivers quadrant-by-quadrant analysis, data-backed recommendations, and ready-to-use Word and Excel files so you can act fast. Purchase now for the complete strategic playbook and stop guessing where to invest your next dollar.

Stars

Jet printing platforms

Jet printing platforms hold high market share in high-mix, miniaturized SMT, addressing a segment projected to grow ~7% CAGR from 2024–2028; Mycronic (Nasdaq Stockholm) must keep investing in speed, software and application engineering to sustain leadership. The business is cash intensive today but momentum and adoption can turn it into a future cash cow; continue funding performance and customer rollouts.

Advanced dispensing systems

Electronics density and demand for adhesives/underfills (global advanced packaging market CAGR ~8% 2024–30) create clear tailwinds; Mycronic’s precision placement enables complex jobs and premium pricing. Rapid growth forces heavy cash use in application support and demo capacity, pressuring working capital. Continue aggressive investment in process capability and vertical solutions to capture high-margin pockets.

AI-driven automated optical inspection

Inspection demand scales with complexity and yield pressure—global AOI investment surged in 2024 as advanced packaging and IC yield control tightened, supporting double-digit growth in high-end AOI spending. Mycronic’s automation plus analytics can set the pace, but models, data, and UX need constant reinvestment to preserve differentiation. Revenues climb while cash needs rise in step; invest to lock in accuracy, speed, and closed-loop value.

Semiconductor mask writers (advanced)

Rising chip complexity and reticle precision push the frontier; in 2024 the advanced mask-writer niche counts only 2–3 main suppliers, signaling real growth potential.

High multi‑million‑dollar ASPs, long sales cycles and heavy R&D mean cash flow is net negative now — money in, money out — while Mycronic must sustain investments.

Protecting roadmap leadership and field performance in 2024 converts technology advantage into durable cash as wafer node demand expands.

- 2024: 2–3 dominant suppliers

- Multi‑million‑dollar ASPs

- Long sales cycles, heavy R&D

- Focus: roadmap + field performance

MicroLED/OLED display tooling

MicroLED/OLED display tooling sits as a Stars segment: premium OLED demand and microLED pilots are ramping with high technical barriers, where early leadership can secure share as adoption expands. Success requires substantial applications engineering and customer co-development, with Mycronic advised to double down where clear line-of-sight to volume exists.

- High barriers

- Early leadership wins

- Requires apps/co‑dev

- Invest where volume visible

Jet printing, AOI & mask writers lead — jet CAGR ~7%, AP ~8%

Jet printing, AOI, mask writers and display tooling are Stars for Mycronic: 2024 sees jet-market CAGR ~7% (2024–28), advanced packaging ~8% (2024–30), AOI spending rose double‑digit in 2024, mask-writer supply concentrated (2–3 suppliers).

High multi‑million ASPs, long sales cycles and heavy R&D keep cash negative today; sustained investment required to convert to future cash cows.

| Segment | 2024 metric |

|---|---|

| Jet printing | ~7% CAGR 2024–28 |

| Advanced packaging | ~8% CAGR 2024–30 |

| AOI | Double‑digit spend growth 2024 |

| Mask writers | 2–3 dominant suppliers 2024 |

What is included in the product

BCG review of Mycronic products, showing Stars, Cash Cows, Questions, Dogs with buy/hold/sell advice and trend context.

One-page Mycronic BCG Matrix placing each business unit in a quadrant to simplify strategy and speed decisions for management

Cash Cows

Installed-base service contracts

Installed-base service contracts leverage Mycronic’s large global footprint to generate recurring maintenance and uptime revenue, with service and spare parts contributing about 25% of 2024 group sales (SEK 6,064m). These contracts are mature, sticky and margin-rich, supporting group gross margins above hardware alone. Growth is low and requires little incremental CAPEX, so management can milk cash flows while investing in remote diagnostics to cut churn and uptime penalties.

Spare parts and consumables

Spare parts and consumables generate predictable pull-through from active lines, supporting service continuity and repeat revenue; in 2024 this segment delivered high contribution margins (~40%) and steady cashflow. Market demand is stable with moderate growth (~3% CAGR). Maintain operational discipline: optimize inventory turns and dynamic pricing to protect >95% service-level targets.

Legacy display mask writer upgrades

Legacy display mask writer upgrades extend lifecycles for existing Mycronic installations, delivering upgrade-kit revenue with high margin profiles and limited R&D spend. The mature display market showed low-single-digit growth in 2024 (≈1–3%), so unit growth is limited but dependable. Maintain a tight SKU roadmap and clear end-of-life plans to maximize aftermarket yield and service margins.

SMT placement platforms in mature segments

SMT placement platforms in mature segments are cash cows for Mycronic, with well-penetrated geographies and customers refreshing on predictable cycles; Mycronic reported 2024 net sales of SEK 3.2 billion, driven largely by mature SMT revenue streams. Competitive but defensible niches—high-precision optics and niche software—sustain share, while capex is light relative to returns. Focus on efficiency, uptime, and bundled software maintenance keeps installed-base churn low.

Production software licenses and maintenance

Production software licenses and maintenance tie line control, traceability and MES connectors to installed hardware, driving low churn and strong renewal economics; 2024 industry estimates show renewal rates above 85% and churn under 10%, with market growth steady at roughly 3–5% CAGR. Maintaining compatibility and a modest feature cadence preserves margins while leveraging installed base value.

- Line control + MES connectors

- Renewals >85% (2024)

- Churn <10% (2024)

- Market growth ~3–5% CAGR

- Focus: compatibility, modest feature cadence

Service & spares 25% (SEK 6,064m), SMT SEK 3.2bn, renewals > 85%

Installed-base services, spare parts and mature SMT/display product lines generated steady cash in 2024: service/spares ~25% of group sales (SEK 6,064m), mature SMT net sales SEK 3.2bn; high margins (~40% for spares), renewals >85% and churn <10%, low capex, stable growth ~1–5% CAGR.

| Metric | 2024 |

|---|---|

| Service/Spare % | 25% |

| Group sales | SEK 6,064m |

| SMT net sales | SEK 3.2bn |

| Spare margin | ~40% |

| Renewals | >85% |

Delivered as Shown

Mycronic BCG Matrix

The file you're previewing here is the exact Mycronic BCG Matrix you'll receive after purchase—no watermarks, no placeholders. It’s the final, fully formatted report ready for printing, editing, or presenting. Designed for clarity and strategic use, it arrives instantly to your inbox. Buy once, use immediately—no surprises.

Unlock Strategic Clarity

Get a clear snapshot of Mycronic’s product portfolio with this BCG Matrix preview—see where the Stars, Cash Cows, Dogs, and Question Marks sit and why it matters. The full BCG Matrix delivers quadrant-by-quadrant analysis, data-backed recommendations, and ready-to-use Word and Excel files so you can act fast. Purchase now for the complete strategic playbook and stop guessing where to invest your next dollar.

Stars

Jet printing platforms

Jet printing platforms hold high market share in high-mix, miniaturized SMT, addressing a segment projected to grow ~7% CAGR from 2024–2028; Mycronic (Nasdaq Stockholm) must keep investing in speed, software and application engineering to sustain leadership. The business is cash intensive today but momentum and adoption can turn it into a future cash cow; continue funding performance and customer rollouts.

Advanced dispensing systems

Electronics density and demand for adhesives/underfills (global advanced packaging market CAGR ~8% 2024–30) create clear tailwinds; Mycronic’s precision placement enables complex jobs and premium pricing. Rapid growth forces heavy cash use in application support and demo capacity, pressuring working capital. Continue aggressive investment in process capability and vertical solutions to capture high-margin pockets.

AI-driven automated optical inspection

Inspection demand scales with complexity and yield pressure—global AOI investment surged in 2024 as advanced packaging and IC yield control tightened, supporting double-digit growth in high-end AOI spending. Mycronic’s automation plus analytics can set the pace, but models, data, and UX need constant reinvestment to preserve differentiation. Revenues climb while cash needs rise in step; invest to lock in accuracy, speed, and closed-loop value.

Semiconductor mask writers (advanced)

Rising chip complexity and reticle precision push the frontier; in 2024 the advanced mask-writer niche counts only 2–3 main suppliers, signaling real growth potential.

High multi‑million‑dollar ASPs, long sales cycles and heavy R&D mean cash flow is net negative now — money in, money out — while Mycronic must sustain investments.

Protecting roadmap leadership and field performance in 2024 converts technology advantage into durable cash as wafer node demand expands.

- 2024: 2–3 dominant suppliers

- Multi‑million‑dollar ASPs

- Long sales cycles, heavy R&D

- Focus: roadmap + field performance

MicroLED/OLED display tooling

MicroLED/OLED display tooling sits as a Stars segment: premium OLED demand and microLED pilots are ramping with high technical barriers, where early leadership can secure share as adoption expands. Success requires substantial applications engineering and customer co-development, with Mycronic advised to double down where clear line-of-sight to volume exists.

- High barriers

- Early leadership wins

- Requires apps/co‑dev

- Invest where volume visible

Jet printing, AOI & mask writers lead — jet CAGR ~7%, AP ~8%

Jet printing, AOI, mask writers and display tooling are Stars for Mycronic: 2024 sees jet-market CAGR ~7% (2024–28), advanced packaging ~8% (2024–30), AOI spending rose double‑digit in 2024, mask-writer supply concentrated (2–3 suppliers).

High multi‑million ASPs, long sales cycles and heavy R&D keep cash negative today; sustained investment required to convert to future cash cows.

| Segment | 2024 metric |

|---|---|

| Jet printing | ~7% CAGR 2024–28 |

| Advanced packaging | ~8% CAGR 2024–30 |

| AOI | Double‑digit spend growth 2024 |

| Mask writers | 2–3 dominant suppliers 2024 |

What is included in the product

BCG review of Mycronic products, showing Stars, Cash Cows, Questions, Dogs with buy/hold/sell advice and trend context.

One-page Mycronic BCG Matrix placing each business unit in a quadrant to simplify strategy and speed decisions for management

Cash Cows

Installed-base service contracts

Installed-base service contracts leverage Mycronic’s large global footprint to generate recurring maintenance and uptime revenue, with service and spare parts contributing about 25% of 2024 group sales (SEK 6,064m). These contracts are mature, sticky and margin-rich, supporting group gross margins above hardware alone. Growth is low and requires little incremental CAPEX, so management can milk cash flows while investing in remote diagnostics to cut churn and uptime penalties.

Spare parts and consumables

Spare parts and consumables generate predictable pull-through from active lines, supporting service continuity and repeat revenue; in 2024 this segment delivered high contribution margins (~40%) and steady cashflow. Market demand is stable with moderate growth (~3% CAGR). Maintain operational discipline: optimize inventory turns and dynamic pricing to protect >95% service-level targets.

Legacy display mask writer upgrades

Legacy display mask writer upgrades extend lifecycles for existing Mycronic installations, delivering upgrade-kit revenue with high margin profiles and limited R&D spend. The mature display market showed low-single-digit growth in 2024 (≈1–3%), so unit growth is limited but dependable. Maintain a tight SKU roadmap and clear end-of-life plans to maximize aftermarket yield and service margins.

SMT placement platforms in mature segments

SMT placement platforms in mature segments are cash cows for Mycronic, with well-penetrated geographies and customers refreshing on predictable cycles; Mycronic reported 2024 net sales of SEK 3.2 billion, driven largely by mature SMT revenue streams. Competitive but defensible niches—high-precision optics and niche software—sustain share, while capex is light relative to returns. Focus on efficiency, uptime, and bundled software maintenance keeps installed-base churn low.

Production software licenses and maintenance

Production software licenses and maintenance tie line control, traceability and MES connectors to installed hardware, driving low churn and strong renewal economics; 2024 industry estimates show renewal rates above 85% and churn under 10%, with market growth steady at roughly 3–5% CAGR. Maintaining compatibility and a modest feature cadence preserves margins while leveraging installed base value.

- Line control + MES connectors

- Renewals >85% (2024)

- Churn <10% (2024)

- Market growth ~3–5% CAGR

- Focus: compatibility, modest feature cadence

Service & spares 25% (SEK 6,064m), SMT SEK 3.2bn, renewals > 85%

Installed-base services, spare parts and mature SMT/display product lines generated steady cash in 2024: service/spares ~25% of group sales (SEK 6,064m), mature SMT net sales SEK 3.2bn; high margins (~40% for spares), renewals >85% and churn <10%, low capex, stable growth ~1–5% CAGR.

| Metric | 2024 |

|---|---|

| Service/Spare % | 25% |

| Group sales | SEK 6,064m |

| SMT net sales | SEK 3.2bn |

| Spare margin | ~40% |

| Renewals | >85% |

Delivered as Shown

Mycronic BCG Matrix

The file you're previewing here is the exact Mycronic BCG Matrix you'll receive after purchase—no watermarks, no placeholders. It’s the final, fully formatted report ready for printing, editing, or presenting. Designed for clarity and strategic use, it arrives instantly to your inbox. Buy once, use immediately—no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Unlock Strategic Clarity

Get a clear snapshot of Mycronic’s product portfolio with this BCG Matrix preview—see where the Stars, Cash Cows, Dogs, and Question Marks sit and why it matters. The full BCG Matrix delivers quadrant-by-quadrant analysis, data-backed recommendations, and ready-to-use Word and Excel files so you can act fast. Purchase now for the complete strategic playbook and stop guessing where to invest your next dollar.

Stars

Jet printing platforms

Jet printing platforms hold high market share in high-mix, miniaturized SMT, addressing a segment projected to grow ~7% CAGR from 2024–2028; Mycronic (Nasdaq Stockholm) must keep investing in speed, software and application engineering to sustain leadership. The business is cash intensive today but momentum and adoption can turn it into a future cash cow; continue funding performance and customer rollouts.

Advanced dispensing systems

Electronics density and demand for adhesives/underfills (global advanced packaging market CAGR ~8% 2024–30) create clear tailwinds; Mycronic’s precision placement enables complex jobs and premium pricing. Rapid growth forces heavy cash use in application support and demo capacity, pressuring working capital. Continue aggressive investment in process capability and vertical solutions to capture high-margin pockets.

AI-driven automated optical inspection

Inspection demand scales with complexity and yield pressure—global AOI investment surged in 2024 as advanced packaging and IC yield control tightened, supporting double-digit growth in high-end AOI spending. Mycronic’s automation plus analytics can set the pace, but models, data, and UX need constant reinvestment to preserve differentiation. Revenues climb while cash needs rise in step; invest to lock in accuracy, speed, and closed-loop value.

Semiconductor mask writers (advanced)

Rising chip complexity and reticle precision push the frontier; in 2024 the advanced mask-writer niche counts only 2–3 main suppliers, signaling real growth potential.

High multi‑million‑dollar ASPs, long sales cycles and heavy R&D mean cash flow is net negative now — money in, money out — while Mycronic must sustain investments.

Protecting roadmap leadership and field performance in 2024 converts technology advantage into durable cash as wafer node demand expands.

- 2024: 2–3 dominant suppliers

- Multi‑million‑dollar ASPs

- Long sales cycles, heavy R&D

- Focus: roadmap + field performance

MicroLED/OLED display tooling

MicroLED/OLED display tooling sits as a Stars segment: premium OLED demand and microLED pilots are ramping with high technical barriers, where early leadership can secure share as adoption expands. Success requires substantial applications engineering and customer co-development, with Mycronic advised to double down where clear line-of-sight to volume exists.

- High barriers

- Early leadership wins

- Requires apps/co‑dev

- Invest where volume visible

Jet printing, AOI & mask writers lead — jet CAGR ~7%, AP ~8%

Jet printing, AOI, mask writers and display tooling are Stars for Mycronic: 2024 sees jet-market CAGR ~7% (2024–28), advanced packaging ~8% (2024–30), AOI spending rose double‑digit in 2024, mask-writer supply concentrated (2–3 suppliers).

High multi‑million ASPs, long sales cycles and heavy R&D keep cash negative today; sustained investment required to convert to future cash cows.

| Segment | 2024 metric |

|---|---|

| Jet printing | ~7% CAGR 2024–28 |

| Advanced packaging | ~8% CAGR 2024–30 |

| AOI | Double‑digit spend growth 2024 |

| Mask writers | 2–3 dominant suppliers 2024 |

What is included in the product

BCG review of Mycronic products, showing Stars, Cash Cows, Questions, Dogs with buy/hold/sell advice and trend context.

One-page Mycronic BCG Matrix placing each business unit in a quadrant to simplify strategy and speed decisions for management

Cash Cows

Installed-base service contracts

Installed-base service contracts leverage Mycronic’s large global footprint to generate recurring maintenance and uptime revenue, with service and spare parts contributing about 25% of 2024 group sales (SEK 6,064m). These contracts are mature, sticky and margin-rich, supporting group gross margins above hardware alone. Growth is low and requires little incremental CAPEX, so management can milk cash flows while investing in remote diagnostics to cut churn and uptime penalties.

Spare parts and consumables

Spare parts and consumables generate predictable pull-through from active lines, supporting service continuity and repeat revenue; in 2024 this segment delivered high contribution margins (~40%) and steady cashflow. Market demand is stable with moderate growth (~3% CAGR). Maintain operational discipline: optimize inventory turns and dynamic pricing to protect >95% service-level targets.

Legacy display mask writer upgrades

Legacy display mask writer upgrades extend lifecycles for existing Mycronic installations, delivering upgrade-kit revenue with high margin profiles and limited R&D spend. The mature display market showed low-single-digit growth in 2024 (≈1–3%), so unit growth is limited but dependable. Maintain a tight SKU roadmap and clear end-of-life plans to maximize aftermarket yield and service margins.

SMT placement platforms in mature segments

SMT placement platforms in mature segments are cash cows for Mycronic, with well-penetrated geographies and customers refreshing on predictable cycles; Mycronic reported 2024 net sales of SEK 3.2 billion, driven largely by mature SMT revenue streams. Competitive but defensible niches—high-precision optics and niche software—sustain share, while capex is light relative to returns. Focus on efficiency, uptime, and bundled software maintenance keeps installed-base churn low.

Production software licenses and maintenance

Production software licenses and maintenance tie line control, traceability and MES connectors to installed hardware, driving low churn and strong renewal economics; 2024 industry estimates show renewal rates above 85% and churn under 10%, with market growth steady at roughly 3–5% CAGR. Maintaining compatibility and a modest feature cadence preserves margins while leveraging installed base value.

- Line control + MES connectors

- Renewals >85% (2024)

- Churn <10% (2024)

- Market growth ~3–5% CAGR

- Focus: compatibility, modest feature cadence

Service & spares 25% (SEK 6,064m), SMT SEK 3.2bn, renewals > 85%

Installed-base services, spare parts and mature SMT/display product lines generated steady cash in 2024: service/spares ~25% of group sales (SEK 6,064m), mature SMT net sales SEK 3.2bn; high margins (~40% for spares), renewals >85% and churn <10%, low capex, stable growth ~1–5% CAGR.

| Metric | 2024 |

|---|---|

| Service/Spare % | 25% |

| Group sales | SEK 6,064m |

| SMT net sales | SEK 3.2bn |

| Spare margin | ~40% |

| Renewals | >85% |

Delivered as Shown

Mycronic BCG Matrix

The file you're previewing here is the exact Mycronic BCG Matrix you'll receive after purchase—no watermarks, no placeholders. It’s the final, fully formatted report ready for printing, editing, or presenting. Designed for clarity and strategic use, it arrives instantly to your inbox. Buy once, use immediately—no surprises.