Myers Industries PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, evolving regulations and technology trends are reshaping Myers Industries' strategic landscape in our concise PESTLE snapshot. This briefing highlights risks and growth levers—ideal for investors and strategists seeking quick, actionable intelligence. Purchase the full PESTLE analysis to get in-depth data, scenario planning, and editable insights ready for immediate use.

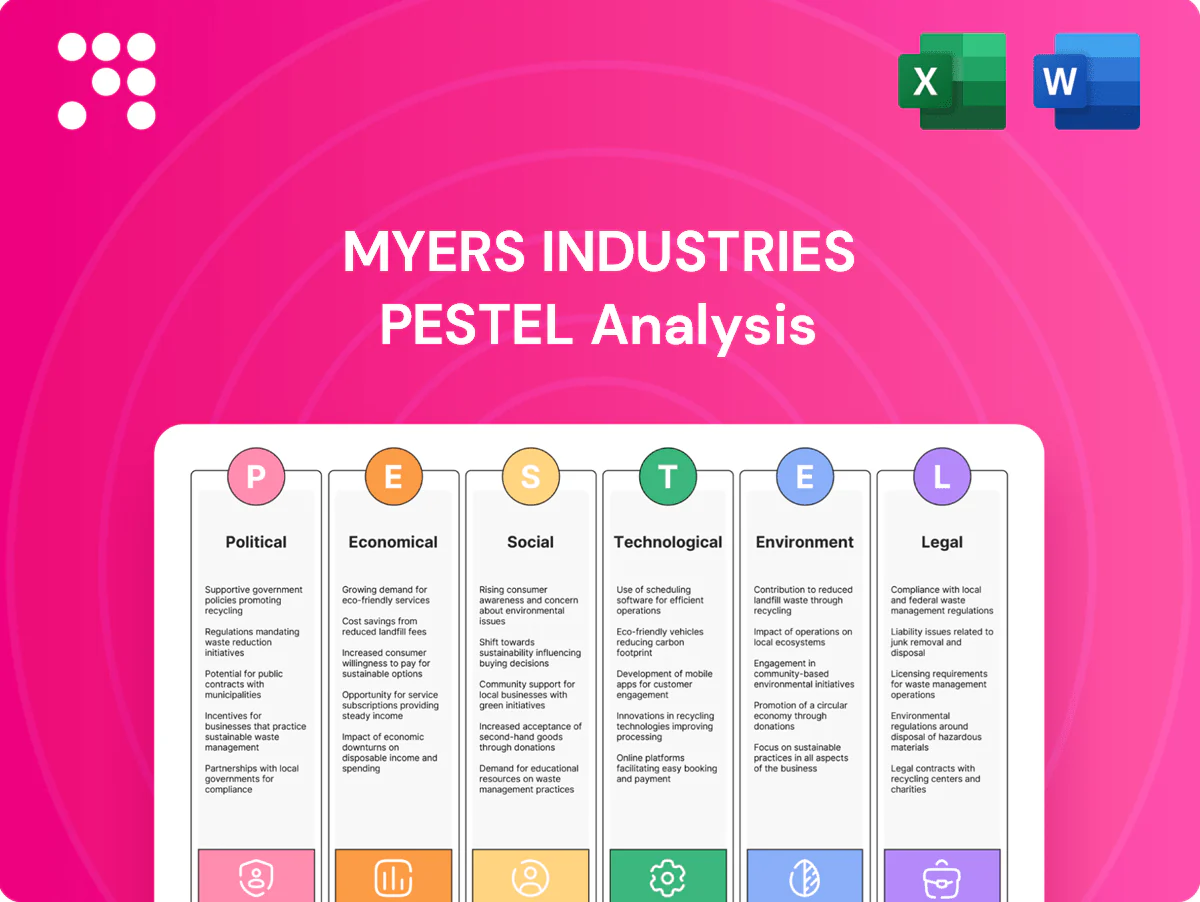

Political factors

Trade policy and tariffs on polymers

Import duties—including lingering 25% Section 301 tariffs on many Chinese industrial goods—can raise costs for resins, additives and molds, squeezing Myers Industries margins and adding volatility to input pricing.

Shifts in US-China and EU trade ties affect tooling and equipment sourcing and export competitiveness; US goods trade frictions with China contributed to a multiyear re‑shoring trend that raises supplier and capex planning complexity.

Proactive diversification, tariff engineering and continuous monitoring of trade negotiations are essential for pricing, inventory planning and mitigating tariff-driven cost shocks.

Infrastructure and industrial policy incentives

Government programs such as the Bipartisan Infrastructure Law's $1.2 trillion package and the Inflation Reduction Act's roughly $369 billion in clean energy and manufacturing support bolster capital investment in molding capacity and onshoring. Grants and tax credits under these laws improve ROI on automation, while public spending in agriculture and logistics raises demand for storage and transport solutions. Policy shifts can reallocate funds across sectors, reducing order visibility for Myers Industries.

Agricultural and automotive sector subsidies

Subsidies shape end-market demand for Myers Industries by bolstering ag and automotive customers' purchasing power. Farm support programs spur equipment and storage buys that raise demand for polymer bins and tires; EVs reached about 14% of global new-car sales in 2023 (IEA), with incentives altering fleet service cycles. Myers sees higher throughput when subsidies persist; withdrawal can cut orders and lengthen sales cycles.

Political stability and labor policy

Stable governance across North America supports predictable operations for Myers Industries, but labor policy shifts matter: US federal minimum wage remains $7.25 (2025) and union membership was 10.1% in 2024, affecting wage pressure and bargaining risk. Changes in minimum wage, collective bargaining or immigration policy can raise labor costs, alter shift structures and overtime strategies; local engagement reduces disruption risk.

- Federal minimum wage: $7.25 (2025)

- Union membership: 10.1% (2024)

- Impacts: wage pressure, staffing, overtime

- Mitigation: local policy engagement

Environmental policy and recycling mandates

Extended Producer Responsibility and circular economy agendas are driving adoption of recycled polymers; OECD reports 400+ EPR schemes worldwide (2023), and the EU requires all packaging to be recyclable by 2030, creating procurement advantages for compliant suppliers. Compliance can unlock public contracts and differentiate Myers' product lines, while plastics reduction policies may force material reformulation. Active engagement with policymakers can influence standards to favor scalable recycled-content solutions.

- 400+ EPR schemes (OECD, 2023)

- EU: all packaging recyclable by 2030

- Compliance = access to public contracts and product differentiation

Tariffs, IRA and infrastructure spur onshoring; EPR, EVs and rising wages reshape plastics supply

Tariffs (25% Section 301) and US-China frictions raise resin/tooling costs and capex uncertainty. Infrastructure ($1.2T) and IRA (~$369B) boost onshoring demand; EVs ~14% of new-car sales (2023) shift product mix. EPR/400+ schemes (OECD 2023) favor recycled-content suppliers. Labor: federal min wage $7.25 (2025); union rate 10.1% (2024) increase wage pressure.

| Metric | Value | Impact |

|---|---|---|

| Section 301 | 25% | Input cost ↑ |

| Infrastructure/IRA | $1.2T/$369B | Onshoring ↑ |

| EPR schemes | 400+ | Recycled demand ↑ |

What is included in the product

Explores how macro-environmental forces uniquely affect Myers Industries across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region- and industry-specific examples to identify risks and growth opportunities. Designed for executives, investors and consultants to support scenario planning, strategy and funding narratives.

A concise, visually segmented PESTLE summary of Myers Industries that can be dropped into presentations or shared across teams, enabling quick interpretation, customizable notes for region or business line, and supporting external-risk and market-positioning discussions during planning sessions.

Economic factors

Cyclical demand in industrial and consumer markets

Myers Industries (NASDAQ: MYE) faces cyclical demand as industrial and consumer spending swings directly affect orders for storage, organization, and transport products; downturns delay capital expenditures and cause destocking that reduces volumes, while expansions lift fill rates. Diversification across end markets such as agriculture, material handling and retail smooths volatility but does not remove cycle risk. Flexible manufacturing capacity and dynamic pricing help defend margins through downturns and recoveries.

Resin price volatility and pass-through

Polymer resin prices closely track oil and gas and moved roughly 20–30% between 2022–2024, driven by feedstock and global supply-demand imbalances. Myers Industries uses effective surcharge mechanisms and hedging to preserve gross margin when inputs swing, historically limiting pass-through lag. Timing mismatches can create temporary margin swings of several hundred basis points. Close supplier partnerships and disciplined inventory management are essential to mitigate volatility.

Automotive and tire service activity

Vehicle miles traveled in the US recovered to about 3.3 trillion miles in 2024, and higher fleet utilization drives tire wear and repeat service demand. Freight trucking tonnage rose roughly 2.5% in 2024, while e-commerce accounted for ~17–18% of retail sales, both extending maintenance cycles. Recessionary slowdowns can cut service throughput and delay retread purchases.

Interest rates and capital expenditure

Higher interest rates (federal funds 5.25–5.50% as of July 2025; 10‑yr Treasury ~4.1%) raise borrowing costs for plant upgrades, tooling and automation, increasing Myers Industries’ financing expense and pushing ROI hurdles higher. Customers’ higher financing costs similarly damp demand for durable storage and handling products, elongating approval timelines. Lower‑rate periods accelerate modernization and capacity additions.

- Rate level: Fed 5.25–5.50% (Jul 2025)

- Effect: higher ROI thresholds, delayed capex approvals

- Customer demand: financing headwinds slow orders

FX and cross-border sales

Currency moves affect competitiveness of Myers Industries' exports and the cost of imported components; a stronger US dollar (around 105 on the DXY in mid-2024) can pressure international sales while lowering input costs. Hedging programs and localized sourcing reduce exposure, and disciplined pricing helps maintain margins through FX volatility.

- FX impact on exports and input costs

- Hedging + localized sourcing lower FX risk

- Pricing discipline preserves margins

Tariffs, IRA and infrastructure spur onshoring; EPR, EVs and rising wages reshape plastics supply

Myers Industries faces cyclical demand tied to industrial and consumer capex, with downturns causing destocking and volume declines while recoveries lift fill rates. Polymer resin costs swung ~20–30% (2022–24), pressuring margins despite surcharges/hedges. Higher rates (Fed 5.25–5.50% Jul 2025; 10yr ~4.1%) raise capex costs and slow customer orders; US VMT ~3.3T (2024) supports aftermarket demand.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| 10‑yr Treasury | ~4.1% |

| Resin volatility | 20–30% (2022–24) |

| US VMT | ~3.3T (2024) |

| DXY | ~105 (mid‑2024) |

What You See Is What You Get

Myers Industries PESTLE Analysis

This Myers Industries PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are the final file delivered immediately after payment, with no placeholders or changes.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, evolving regulations and technology trends are reshaping Myers Industries' strategic landscape in our concise PESTLE snapshot. This briefing highlights risks and growth levers—ideal for investors and strategists seeking quick, actionable intelligence. Purchase the full PESTLE analysis to get in-depth data, scenario planning, and editable insights ready for immediate use.

Political factors

Trade policy and tariffs on polymers

Import duties—including lingering 25% Section 301 tariffs on many Chinese industrial goods—can raise costs for resins, additives and molds, squeezing Myers Industries margins and adding volatility to input pricing.

Shifts in US-China and EU trade ties affect tooling and equipment sourcing and export competitiveness; US goods trade frictions with China contributed to a multiyear re‑shoring trend that raises supplier and capex planning complexity.

Proactive diversification, tariff engineering and continuous monitoring of trade negotiations are essential for pricing, inventory planning and mitigating tariff-driven cost shocks.

Infrastructure and industrial policy incentives

Government programs such as the Bipartisan Infrastructure Law's $1.2 trillion package and the Inflation Reduction Act's roughly $369 billion in clean energy and manufacturing support bolster capital investment in molding capacity and onshoring. Grants and tax credits under these laws improve ROI on automation, while public spending in agriculture and logistics raises demand for storage and transport solutions. Policy shifts can reallocate funds across sectors, reducing order visibility for Myers Industries.

Agricultural and automotive sector subsidies

Subsidies shape end-market demand for Myers Industries by bolstering ag and automotive customers' purchasing power. Farm support programs spur equipment and storage buys that raise demand for polymer bins and tires; EVs reached about 14% of global new-car sales in 2023 (IEA), with incentives altering fleet service cycles. Myers sees higher throughput when subsidies persist; withdrawal can cut orders and lengthen sales cycles.

Political stability and labor policy

Stable governance across North America supports predictable operations for Myers Industries, but labor policy shifts matter: US federal minimum wage remains $7.25 (2025) and union membership was 10.1% in 2024, affecting wage pressure and bargaining risk. Changes in minimum wage, collective bargaining or immigration policy can raise labor costs, alter shift structures and overtime strategies; local engagement reduces disruption risk.

- Federal minimum wage: $7.25 (2025)

- Union membership: 10.1% (2024)

- Impacts: wage pressure, staffing, overtime

- Mitigation: local policy engagement

Environmental policy and recycling mandates

Extended Producer Responsibility and circular economy agendas are driving adoption of recycled polymers; OECD reports 400+ EPR schemes worldwide (2023), and the EU requires all packaging to be recyclable by 2030, creating procurement advantages for compliant suppliers. Compliance can unlock public contracts and differentiate Myers' product lines, while plastics reduction policies may force material reformulation. Active engagement with policymakers can influence standards to favor scalable recycled-content solutions.

- 400+ EPR schemes (OECD, 2023)

- EU: all packaging recyclable by 2030

- Compliance = access to public contracts and product differentiation

Tariffs, IRA and infrastructure spur onshoring; EPR, EVs and rising wages reshape plastics supply

Tariffs (25% Section 301) and US-China frictions raise resin/tooling costs and capex uncertainty. Infrastructure ($1.2T) and IRA (~$369B) boost onshoring demand; EVs ~14% of new-car sales (2023) shift product mix. EPR/400+ schemes (OECD 2023) favor recycled-content suppliers. Labor: federal min wage $7.25 (2025); union rate 10.1% (2024) increase wage pressure.

| Metric | Value | Impact |

|---|---|---|

| Section 301 | 25% | Input cost ↑ |

| Infrastructure/IRA | $1.2T/$369B | Onshoring ↑ |

| EPR schemes | 400+ | Recycled demand ↑ |

What is included in the product

Explores how macro-environmental forces uniquely affect Myers Industries across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region- and industry-specific examples to identify risks and growth opportunities. Designed for executives, investors and consultants to support scenario planning, strategy and funding narratives.

A concise, visually segmented PESTLE summary of Myers Industries that can be dropped into presentations or shared across teams, enabling quick interpretation, customizable notes for region or business line, and supporting external-risk and market-positioning discussions during planning sessions.

Economic factors

Cyclical demand in industrial and consumer markets

Myers Industries (NASDAQ: MYE) faces cyclical demand as industrial and consumer spending swings directly affect orders for storage, organization, and transport products; downturns delay capital expenditures and cause destocking that reduces volumes, while expansions lift fill rates. Diversification across end markets such as agriculture, material handling and retail smooths volatility but does not remove cycle risk. Flexible manufacturing capacity and dynamic pricing help defend margins through downturns and recoveries.

Resin price volatility and pass-through

Polymer resin prices closely track oil and gas and moved roughly 20–30% between 2022–2024, driven by feedstock and global supply-demand imbalances. Myers Industries uses effective surcharge mechanisms and hedging to preserve gross margin when inputs swing, historically limiting pass-through lag. Timing mismatches can create temporary margin swings of several hundred basis points. Close supplier partnerships and disciplined inventory management are essential to mitigate volatility.

Automotive and tire service activity

Vehicle miles traveled in the US recovered to about 3.3 trillion miles in 2024, and higher fleet utilization drives tire wear and repeat service demand. Freight trucking tonnage rose roughly 2.5% in 2024, while e-commerce accounted for ~17–18% of retail sales, both extending maintenance cycles. Recessionary slowdowns can cut service throughput and delay retread purchases.

Interest rates and capital expenditure

Higher interest rates (federal funds 5.25–5.50% as of July 2025; 10‑yr Treasury ~4.1%) raise borrowing costs for plant upgrades, tooling and automation, increasing Myers Industries’ financing expense and pushing ROI hurdles higher. Customers’ higher financing costs similarly damp demand for durable storage and handling products, elongating approval timelines. Lower‑rate periods accelerate modernization and capacity additions.

- Rate level: Fed 5.25–5.50% (Jul 2025)

- Effect: higher ROI thresholds, delayed capex approvals

- Customer demand: financing headwinds slow orders

FX and cross-border sales

Currency moves affect competitiveness of Myers Industries' exports and the cost of imported components; a stronger US dollar (around 105 on the DXY in mid-2024) can pressure international sales while lowering input costs. Hedging programs and localized sourcing reduce exposure, and disciplined pricing helps maintain margins through FX volatility.

- FX impact on exports and input costs

- Hedging + localized sourcing lower FX risk

- Pricing discipline preserves margins

Tariffs, IRA and infrastructure spur onshoring; EPR, EVs and rising wages reshape plastics supply

Myers Industries faces cyclical demand tied to industrial and consumer capex, with downturns causing destocking and volume declines while recoveries lift fill rates. Polymer resin costs swung ~20–30% (2022–24), pressuring margins despite surcharges/hedges. Higher rates (Fed 5.25–5.50% Jul 2025; 10yr ~4.1%) raise capex costs and slow customer orders; US VMT ~3.3T (2024) supports aftermarket demand.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| 10‑yr Treasury | ~4.1% |

| Resin volatility | 20–30% (2022–24) |

| US VMT | ~3.3T (2024) |

| DXY | ~105 (mid‑2024) |

What You See Is What You Get

Myers Industries PESTLE Analysis

This Myers Industries PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are the final file delivered immediately after payment, with no placeholders or changes.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, evolving regulations and technology trends are reshaping Myers Industries' strategic landscape in our concise PESTLE snapshot. This briefing highlights risks and growth levers—ideal for investors and strategists seeking quick, actionable intelligence. Purchase the full PESTLE analysis to get in-depth data, scenario planning, and editable insights ready for immediate use.

Political factors

Trade policy and tariffs on polymers

Import duties—including lingering 25% Section 301 tariffs on many Chinese industrial goods—can raise costs for resins, additives and molds, squeezing Myers Industries margins and adding volatility to input pricing.

Shifts in US-China and EU trade ties affect tooling and equipment sourcing and export competitiveness; US goods trade frictions with China contributed to a multiyear re‑shoring trend that raises supplier and capex planning complexity.

Proactive diversification, tariff engineering and continuous monitoring of trade negotiations are essential for pricing, inventory planning and mitigating tariff-driven cost shocks.

Infrastructure and industrial policy incentives

Government programs such as the Bipartisan Infrastructure Law's $1.2 trillion package and the Inflation Reduction Act's roughly $369 billion in clean energy and manufacturing support bolster capital investment in molding capacity and onshoring. Grants and tax credits under these laws improve ROI on automation, while public spending in agriculture and logistics raises demand for storage and transport solutions. Policy shifts can reallocate funds across sectors, reducing order visibility for Myers Industries.

Agricultural and automotive sector subsidies

Subsidies shape end-market demand for Myers Industries by bolstering ag and automotive customers' purchasing power. Farm support programs spur equipment and storage buys that raise demand for polymer bins and tires; EVs reached about 14% of global new-car sales in 2023 (IEA), with incentives altering fleet service cycles. Myers sees higher throughput when subsidies persist; withdrawal can cut orders and lengthen sales cycles.

Political stability and labor policy

Stable governance across North America supports predictable operations for Myers Industries, but labor policy shifts matter: US federal minimum wage remains $7.25 (2025) and union membership was 10.1% in 2024, affecting wage pressure and bargaining risk. Changes in minimum wage, collective bargaining or immigration policy can raise labor costs, alter shift structures and overtime strategies; local engagement reduces disruption risk.

- Federal minimum wage: $7.25 (2025)

- Union membership: 10.1% (2024)

- Impacts: wage pressure, staffing, overtime

- Mitigation: local policy engagement

Environmental policy and recycling mandates

Extended Producer Responsibility and circular economy agendas are driving adoption of recycled polymers; OECD reports 400+ EPR schemes worldwide (2023), and the EU requires all packaging to be recyclable by 2030, creating procurement advantages for compliant suppliers. Compliance can unlock public contracts and differentiate Myers' product lines, while plastics reduction policies may force material reformulation. Active engagement with policymakers can influence standards to favor scalable recycled-content solutions.

- 400+ EPR schemes (OECD, 2023)

- EU: all packaging recyclable by 2030

- Compliance = access to public contracts and product differentiation

Tariffs, IRA and infrastructure spur onshoring; EPR, EVs and rising wages reshape plastics supply

Tariffs (25% Section 301) and US-China frictions raise resin/tooling costs and capex uncertainty. Infrastructure ($1.2T) and IRA (~$369B) boost onshoring demand; EVs ~14% of new-car sales (2023) shift product mix. EPR/400+ schemes (OECD 2023) favor recycled-content suppliers. Labor: federal min wage $7.25 (2025); union rate 10.1% (2024) increase wage pressure.

| Metric | Value | Impact |

|---|---|---|

| Section 301 | 25% | Input cost ↑ |

| Infrastructure/IRA | $1.2T/$369B | Onshoring ↑ |

| EPR schemes | 400+ | Recycled demand ↑ |

What is included in the product

Explores how macro-environmental forces uniquely affect Myers Industries across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region- and industry-specific examples to identify risks and growth opportunities. Designed for executives, investors and consultants to support scenario planning, strategy and funding narratives.

A concise, visually segmented PESTLE summary of Myers Industries that can be dropped into presentations or shared across teams, enabling quick interpretation, customizable notes for region or business line, and supporting external-risk and market-positioning discussions during planning sessions.

Economic factors

Cyclical demand in industrial and consumer markets

Myers Industries (NASDAQ: MYE) faces cyclical demand as industrial and consumer spending swings directly affect orders for storage, organization, and transport products; downturns delay capital expenditures and cause destocking that reduces volumes, while expansions lift fill rates. Diversification across end markets such as agriculture, material handling and retail smooths volatility but does not remove cycle risk. Flexible manufacturing capacity and dynamic pricing help defend margins through downturns and recoveries.

Resin price volatility and pass-through

Polymer resin prices closely track oil and gas and moved roughly 20–30% between 2022–2024, driven by feedstock and global supply-demand imbalances. Myers Industries uses effective surcharge mechanisms and hedging to preserve gross margin when inputs swing, historically limiting pass-through lag. Timing mismatches can create temporary margin swings of several hundred basis points. Close supplier partnerships and disciplined inventory management are essential to mitigate volatility.

Automotive and tire service activity

Vehicle miles traveled in the US recovered to about 3.3 trillion miles in 2024, and higher fleet utilization drives tire wear and repeat service demand. Freight trucking tonnage rose roughly 2.5% in 2024, while e-commerce accounted for ~17–18% of retail sales, both extending maintenance cycles. Recessionary slowdowns can cut service throughput and delay retread purchases.

Interest rates and capital expenditure

Higher interest rates (federal funds 5.25–5.50% as of July 2025; 10‑yr Treasury ~4.1%) raise borrowing costs for plant upgrades, tooling and automation, increasing Myers Industries’ financing expense and pushing ROI hurdles higher. Customers’ higher financing costs similarly damp demand for durable storage and handling products, elongating approval timelines. Lower‑rate periods accelerate modernization and capacity additions.

- Rate level: Fed 5.25–5.50% (Jul 2025)

- Effect: higher ROI thresholds, delayed capex approvals

- Customer demand: financing headwinds slow orders

FX and cross-border sales

Currency moves affect competitiveness of Myers Industries' exports and the cost of imported components; a stronger US dollar (around 105 on the DXY in mid-2024) can pressure international sales while lowering input costs. Hedging programs and localized sourcing reduce exposure, and disciplined pricing helps maintain margins through FX volatility.

- FX impact on exports and input costs

- Hedging + localized sourcing lower FX risk

- Pricing discipline preserves margins

Tariffs, IRA and infrastructure spur onshoring; EPR, EVs and rising wages reshape plastics supply

Myers Industries faces cyclical demand tied to industrial and consumer capex, with downturns causing destocking and volume declines while recoveries lift fill rates. Polymer resin costs swung ~20–30% (2022–24), pressuring margins despite surcharges/hedges. Higher rates (Fed 5.25–5.50% Jul 2025; 10yr ~4.1%) raise capex costs and slow customer orders; US VMT ~3.3T (2024) supports aftermarket demand.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| 10‑yr Treasury | ~4.1% |

| Resin volatility | 20–30% (2022–24) |

| US VMT | ~3.3T (2024) |

| DXY | ~105 (mid‑2024) |

What You See Is What You Get

Myers Industries PESTLE Analysis

This Myers Industries PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are the final file delivered immediately after payment, with no placeholders or changes.