JVM Porter's Five Forces Analysis

Don't Miss the Bigger Picture

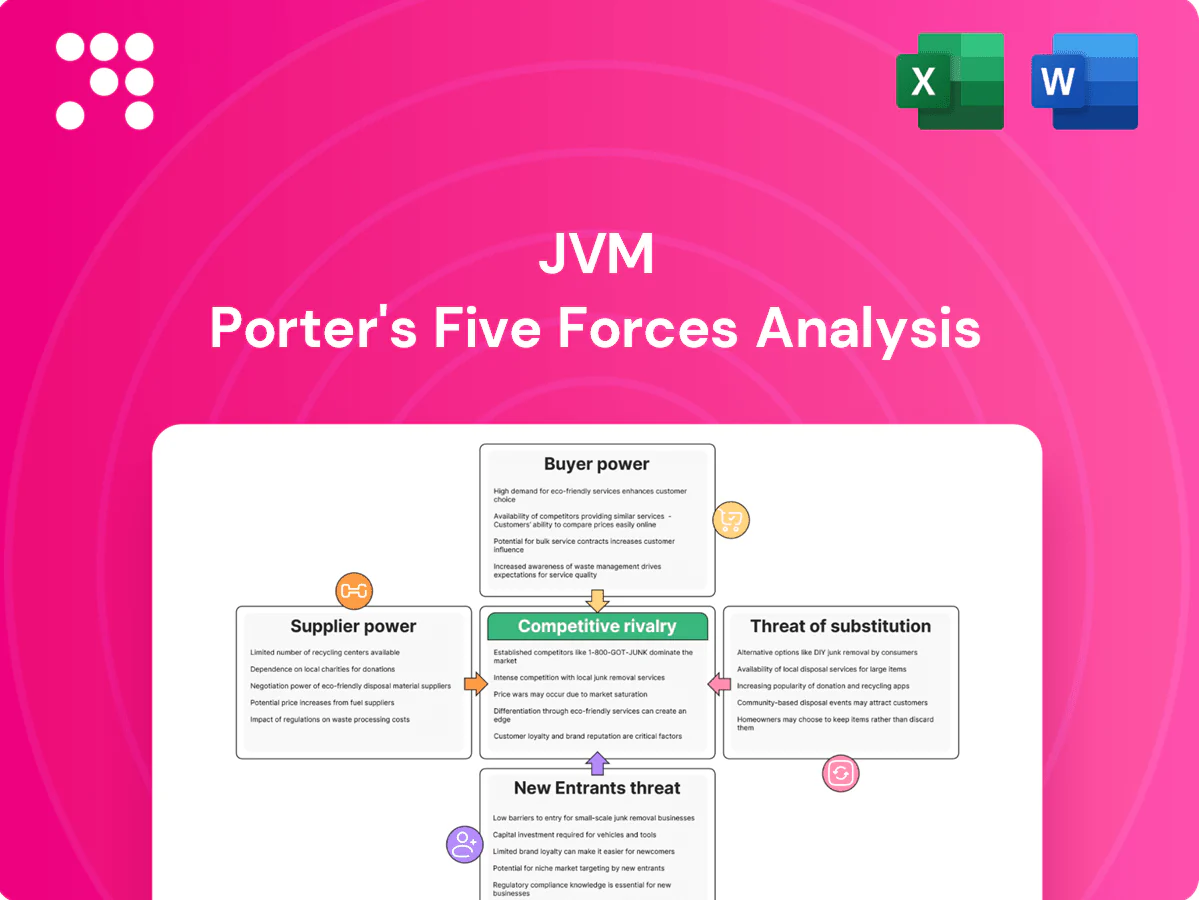

JVM’s Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, threat of substitutes, and barriers to entry, revealing where margins and market share are most vulnerable. This brief overview surfaces strategic pressure points but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore JVM’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components concentration

Precision sensors, robotic actuators, machine-vision systems and pharma-grade plastics come from a concentrated set of qualified vendors, creating supply bottlenecks. In 2024 this concentration has kept input prices elevated and extended lead times; dual-sourcing is feasible but medical validation typically adds 6–12 months and $50,000–$250,000 in revalidation costs. Long-term agreements and volume commitments mitigate price and delivery volatility.

Electronic and semiconductor cycles

Controllers, PCBs, and chips tie JVM to semiconductor cycles; lead-time spikes (peaks >30–40 weeks in 2021–22) and episodic shortages persisted into 2024, delaying deliveries and raising component costs that are hard to pass through quickly. Design-for-substitution and buffer inventory mitigate risk, but certification timelines (often 6–12 months for safety-critical parts) slow changes. Strong supplier partnerships and forecast accuracy are critical levers.

Software dependencies

Embedded OS, databases and middleware licenses create lock-in and compliance costs, with vendor upgrades and audits often driving unplanned spend and effort. Security patches and compatibility updates frequently impose emergency work and can halt releases when critical bugs appear. Enterprise licensing negotiations commonly lower per-unit fees but concentrate risk on vendors. By 2024, ~93% of codebases used open-source components, and open standards plus modular architecture reduce single-vendor power.

Compliance-grade materials

Materials contacting medications must meet FDA cGMP, USP and ISO standards, constraining eligible suppliers and increasing their leverage via approved supplier lists; requalifying new materials requires extensive validation documentation and protocol-driven timelines. Bulk purchasing and early supplier involvement (ESI) can distribute validation costs and reduce individual supplier power.

- Regulatory constraints: FDA cGMP, USP, ISO

- Approved lists raise supplier leverage

- Requalification demands validation docs

- Bulk buys/ESI share validation burden

Logistics and service parts

Global JVM installations demand timely spare parts and consumables; in 2024 aftermarket parts accounted for roughly 28% of industrial OEM revenue while the 3PL market reached about 1.3 trillion USD, making regional distributors and logistics partners pivotal to cost-to-serve. Delays that extend lead times beyond the 9–14 day industry average materially breach uptime SLAs and depress customer satisfaction; multi-hub inventories and predictive parts planning cut exposure and restore service levels.

- Spare-parts share: ~28% of OEM revenue (2024)

- 3PL market size: ~$1.3T (2024)

- Typical lead times: 9–14 days; multi-hub + predictive planning reduces SLA breaches

Concentrated suppliers raise costs and lead times; dual-sourcing and contracts mitigate

Supplier power is high due to concentrated qualified vendors for sensors, pharma-grade materials and semiconductors, keeping prices and lead times elevated in 2024. Certification/revalidation (6–12 months, $50k–$250k) and vendor lock-in for software raise switching costs. Long-term contracts, dual-sourcing where feasible, buffer stock and supplier partnerships are key mitigants.

| Metric | 2024 |

|---|---|

| Aftermarket share | ~28% |

| 3PL market | $1.3T |

| Revalidation cost | $50k–$250k |

What is included in the product

Provides a focused Porter's Five Forces assessment of JVM, identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and data-backed strategic implications for JVM’s market share, pricing power, and profitability.

JVM Porter's Five Forces gives a one-sheet, customizable view of competitive pressures—complete with an instant spider chart—for fast, board-ready decisions without macros or complex code.

Customers Bargaining Power

Consolidated buyers and GPOs

Hospital systems, retail chains, and group purchasing organizations negotiate aggressively, with the top five GPOs covering roughly 90% of GPO-managed spend.

Large volumes enable steep price concessions and extended payment terms; GPO purchasing power exceeds $100 billion annually.

Contract standards and SLAs shift operational and financial risk to vendors, so differentiated clinical outcomes and documented ROI in case studies are critical to defend premium pricing.

High switching costs

Installed base integration with pharmacy workflows and HIS/EMR reduces buyer power by embedding JVM into core operations. Data migration, retraining, and weeks of downtime often mean six-figure migration costs that deter switching. Competitive trade-in programs and vendor credits can offset those costs and restore some buyer leverage. Sticky software modules and analytics (prescription decision support, inventory forecasting) deepen lock-in and raise lifetime value.

Outcome-driven procurement

Outcome-driven procurement forces buyers to demand error reduction, higher throughput, and labor savings tied to strict KPIs; in 2024 about 62% of enterprise procurement teams required pilots or POCs before purchase, elongating sales cycles and raising selling costs.

Regulatory and safety demands

By 2024 medication safety regimes mandate serialization, audit trails and 21 CFR Part 11 alignment; buyers routinely require validation reports and cybersecurity attestations. These demands raise vendor compliance costs and shift negotiations toward documented risk controls, reducing pure price haggling. Robust quality systems make vendors sell risk reduction, not just price.

- Mandatory: serialization, audit trails, 21 CFR Part 11

- Buyer demands: validations, cybersecurity attestations

- Effect: higher vendor compliance costs, less price pressure

Alternative financing expectations

Hospitals and pharmacies increasingly demand leasing, RaaS, or outcome-based models, turning financing flexibility into a key negotiation lever and shifting price sensitivity toward payment structure rather than unit cost. Vendors often assume utilization risk to win contracts, compressing margins but protecting market access. Bundling consumables and long-term service contracts preserves lifetime value and offsets financing concessions.

- Demand: alternative financing

- Leverage: payment structure

- Risk: vendor-borne utilization

- Retention: consumable+service bundles

GPOs wield ≈90% spend; ≈62% require pilots; leasing shifts payment risk

Large hospital systems, retail chains and the top five GPOs (≈90% of GPO-managed spend) exert strong price and payment leverage; GPO purchasing exceeds $100B annually. Buyers demand pilots (≈62% of enterprise teams in 2024), validations and cybersecurity attestations, raising vendor compliance costs and reducing pure price pressure. Leasing, RaaS and outcome-based models shift sensitivity to payment structure and utilization risk.

| Metric | 2024 Value |

|---|---|

| Top-5 GPO coverage | ≈90% |

| GPO-managed spend | >$100B |

| POC requirement | ≈62% |

Preview the Actual Deliverable

JVM Porter's Five Forces Analysis

This preview displays the JVM Porter's Five Forces Analysis exactly as you'll receive it after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use the moment you complete payment. You're viewing the final deliverable in its entirety.

Don't Miss the Bigger Picture

JVM’s Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, threat of substitutes, and barriers to entry, revealing where margins and market share are most vulnerable. This brief overview surfaces strategic pressure points but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore JVM’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components concentration

Precision sensors, robotic actuators, machine-vision systems and pharma-grade plastics come from a concentrated set of qualified vendors, creating supply bottlenecks. In 2024 this concentration has kept input prices elevated and extended lead times; dual-sourcing is feasible but medical validation typically adds 6–12 months and $50,000–$250,000 in revalidation costs. Long-term agreements and volume commitments mitigate price and delivery volatility.

Electronic and semiconductor cycles

Controllers, PCBs, and chips tie JVM to semiconductor cycles; lead-time spikes (peaks >30–40 weeks in 2021–22) and episodic shortages persisted into 2024, delaying deliveries and raising component costs that are hard to pass through quickly. Design-for-substitution and buffer inventory mitigate risk, but certification timelines (often 6–12 months for safety-critical parts) slow changes. Strong supplier partnerships and forecast accuracy are critical levers.

Software dependencies

Embedded OS, databases and middleware licenses create lock-in and compliance costs, with vendor upgrades and audits often driving unplanned spend and effort. Security patches and compatibility updates frequently impose emergency work and can halt releases when critical bugs appear. Enterprise licensing negotiations commonly lower per-unit fees but concentrate risk on vendors. By 2024, ~93% of codebases used open-source components, and open standards plus modular architecture reduce single-vendor power.

Compliance-grade materials

Materials contacting medications must meet FDA cGMP, USP and ISO standards, constraining eligible suppliers and increasing their leverage via approved supplier lists; requalifying new materials requires extensive validation documentation and protocol-driven timelines. Bulk purchasing and early supplier involvement (ESI) can distribute validation costs and reduce individual supplier power.

- Regulatory constraints: FDA cGMP, USP, ISO

- Approved lists raise supplier leverage

- Requalification demands validation docs

- Bulk buys/ESI share validation burden

Logistics and service parts

Global JVM installations demand timely spare parts and consumables; in 2024 aftermarket parts accounted for roughly 28% of industrial OEM revenue while the 3PL market reached about 1.3 trillion USD, making regional distributors and logistics partners pivotal to cost-to-serve. Delays that extend lead times beyond the 9–14 day industry average materially breach uptime SLAs and depress customer satisfaction; multi-hub inventories and predictive parts planning cut exposure and restore service levels.

- Spare-parts share: ~28% of OEM revenue (2024)

- 3PL market size: ~$1.3T (2024)

- Typical lead times: 9–14 days; multi-hub + predictive planning reduces SLA breaches

Concentrated suppliers raise costs and lead times; dual-sourcing and contracts mitigate

Supplier power is high due to concentrated qualified vendors for sensors, pharma-grade materials and semiconductors, keeping prices and lead times elevated in 2024. Certification/revalidation (6–12 months, $50k–$250k) and vendor lock-in for software raise switching costs. Long-term contracts, dual-sourcing where feasible, buffer stock and supplier partnerships are key mitigants.

| Metric | 2024 |

|---|---|

| Aftermarket share | ~28% |

| 3PL market | $1.3T |

| Revalidation cost | $50k–$250k |

What is included in the product

Provides a focused Porter's Five Forces assessment of JVM, identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and data-backed strategic implications for JVM’s market share, pricing power, and profitability.

JVM Porter's Five Forces gives a one-sheet, customizable view of competitive pressures—complete with an instant spider chart—for fast, board-ready decisions without macros or complex code.

Customers Bargaining Power

Consolidated buyers and GPOs

Hospital systems, retail chains, and group purchasing organizations negotiate aggressively, with the top five GPOs covering roughly 90% of GPO-managed spend.

Large volumes enable steep price concessions and extended payment terms; GPO purchasing power exceeds $100 billion annually.

Contract standards and SLAs shift operational and financial risk to vendors, so differentiated clinical outcomes and documented ROI in case studies are critical to defend premium pricing.

High switching costs

Installed base integration with pharmacy workflows and HIS/EMR reduces buyer power by embedding JVM into core operations. Data migration, retraining, and weeks of downtime often mean six-figure migration costs that deter switching. Competitive trade-in programs and vendor credits can offset those costs and restore some buyer leverage. Sticky software modules and analytics (prescription decision support, inventory forecasting) deepen lock-in and raise lifetime value.

Outcome-driven procurement

Outcome-driven procurement forces buyers to demand error reduction, higher throughput, and labor savings tied to strict KPIs; in 2024 about 62% of enterprise procurement teams required pilots or POCs before purchase, elongating sales cycles and raising selling costs.

Regulatory and safety demands

By 2024 medication safety regimes mandate serialization, audit trails and 21 CFR Part 11 alignment; buyers routinely require validation reports and cybersecurity attestations. These demands raise vendor compliance costs and shift negotiations toward documented risk controls, reducing pure price haggling. Robust quality systems make vendors sell risk reduction, not just price.

- Mandatory: serialization, audit trails, 21 CFR Part 11

- Buyer demands: validations, cybersecurity attestations

- Effect: higher vendor compliance costs, less price pressure

Alternative financing expectations

Hospitals and pharmacies increasingly demand leasing, RaaS, or outcome-based models, turning financing flexibility into a key negotiation lever and shifting price sensitivity toward payment structure rather than unit cost. Vendors often assume utilization risk to win contracts, compressing margins but protecting market access. Bundling consumables and long-term service contracts preserves lifetime value and offsets financing concessions.

- Demand: alternative financing

- Leverage: payment structure

- Risk: vendor-borne utilization

- Retention: consumable+service bundles

GPOs wield ≈90% spend; ≈62% require pilots; leasing shifts payment risk

Large hospital systems, retail chains and the top five GPOs (≈90% of GPO-managed spend) exert strong price and payment leverage; GPO purchasing exceeds $100B annually. Buyers demand pilots (≈62% of enterprise teams in 2024), validations and cybersecurity attestations, raising vendor compliance costs and reducing pure price pressure. Leasing, RaaS and outcome-based models shift sensitivity to payment structure and utilization risk.

| Metric | 2024 Value |

|---|---|

| Top-5 GPO coverage | ≈90% |

| GPO-managed spend | >$100B |

| POC requirement | ≈62% |

Preview the Actual Deliverable

JVM Porter's Five Forces Analysis

This preview displays the JVM Porter's Five Forces Analysis exactly as you'll receive it after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use the moment you complete payment. You're viewing the final deliverable in its entirety.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

JVM’s Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, threat of substitutes, and barriers to entry, revealing where margins and market share are most vulnerable. This brief overview surfaces strategic pressure points but only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore JVM’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components concentration

Precision sensors, robotic actuators, machine-vision systems and pharma-grade plastics come from a concentrated set of qualified vendors, creating supply bottlenecks. In 2024 this concentration has kept input prices elevated and extended lead times; dual-sourcing is feasible but medical validation typically adds 6–12 months and $50,000–$250,000 in revalidation costs. Long-term agreements and volume commitments mitigate price and delivery volatility.

Electronic and semiconductor cycles

Controllers, PCBs, and chips tie JVM to semiconductor cycles; lead-time spikes (peaks >30–40 weeks in 2021–22) and episodic shortages persisted into 2024, delaying deliveries and raising component costs that are hard to pass through quickly. Design-for-substitution and buffer inventory mitigate risk, but certification timelines (often 6–12 months for safety-critical parts) slow changes. Strong supplier partnerships and forecast accuracy are critical levers.

Software dependencies

Embedded OS, databases and middleware licenses create lock-in and compliance costs, with vendor upgrades and audits often driving unplanned spend and effort. Security patches and compatibility updates frequently impose emergency work and can halt releases when critical bugs appear. Enterprise licensing negotiations commonly lower per-unit fees but concentrate risk on vendors. By 2024, ~93% of codebases used open-source components, and open standards plus modular architecture reduce single-vendor power.

Compliance-grade materials

Materials contacting medications must meet FDA cGMP, USP and ISO standards, constraining eligible suppliers and increasing their leverage via approved supplier lists; requalifying new materials requires extensive validation documentation and protocol-driven timelines. Bulk purchasing and early supplier involvement (ESI) can distribute validation costs and reduce individual supplier power.

- Regulatory constraints: FDA cGMP, USP, ISO

- Approved lists raise supplier leverage

- Requalification demands validation docs

- Bulk buys/ESI share validation burden

Logistics and service parts

Global JVM installations demand timely spare parts and consumables; in 2024 aftermarket parts accounted for roughly 28% of industrial OEM revenue while the 3PL market reached about 1.3 trillion USD, making regional distributors and logistics partners pivotal to cost-to-serve. Delays that extend lead times beyond the 9–14 day industry average materially breach uptime SLAs and depress customer satisfaction; multi-hub inventories and predictive parts planning cut exposure and restore service levels.

- Spare-parts share: ~28% of OEM revenue (2024)

- 3PL market size: ~$1.3T (2024)

- Typical lead times: 9–14 days; multi-hub + predictive planning reduces SLA breaches

Concentrated suppliers raise costs and lead times; dual-sourcing and contracts mitigate

Supplier power is high due to concentrated qualified vendors for sensors, pharma-grade materials and semiconductors, keeping prices and lead times elevated in 2024. Certification/revalidation (6–12 months, $50k–$250k) and vendor lock-in for software raise switching costs. Long-term contracts, dual-sourcing where feasible, buffer stock and supplier partnerships are key mitigants.

| Metric | 2024 |

|---|---|

| Aftermarket share | ~28% |

| 3PL market | $1.3T |

| Revalidation cost | $50k–$250k |

What is included in the product

Provides a focused Porter's Five Forces assessment of JVM, identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and data-backed strategic implications for JVM’s market share, pricing power, and profitability.

JVM Porter's Five Forces gives a one-sheet, customizable view of competitive pressures—complete with an instant spider chart—for fast, board-ready decisions without macros or complex code.

Customers Bargaining Power

Consolidated buyers and GPOs

Hospital systems, retail chains, and group purchasing organizations negotiate aggressively, with the top five GPOs covering roughly 90% of GPO-managed spend.

Large volumes enable steep price concessions and extended payment terms; GPO purchasing power exceeds $100 billion annually.

Contract standards and SLAs shift operational and financial risk to vendors, so differentiated clinical outcomes and documented ROI in case studies are critical to defend premium pricing.

High switching costs

Installed base integration with pharmacy workflows and HIS/EMR reduces buyer power by embedding JVM into core operations. Data migration, retraining, and weeks of downtime often mean six-figure migration costs that deter switching. Competitive trade-in programs and vendor credits can offset those costs and restore some buyer leverage. Sticky software modules and analytics (prescription decision support, inventory forecasting) deepen lock-in and raise lifetime value.

Outcome-driven procurement

Outcome-driven procurement forces buyers to demand error reduction, higher throughput, and labor savings tied to strict KPIs; in 2024 about 62% of enterprise procurement teams required pilots or POCs before purchase, elongating sales cycles and raising selling costs.

Regulatory and safety demands

By 2024 medication safety regimes mandate serialization, audit trails and 21 CFR Part 11 alignment; buyers routinely require validation reports and cybersecurity attestations. These demands raise vendor compliance costs and shift negotiations toward documented risk controls, reducing pure price haggling. Robust quality systems make vendors sell risk reduction, not just price.

- Mandatory: serialization, audit trails, 21 CFR Part 11

- Buyer demands: validations, cybersecurity attestations

- Effect: higher vendor compliance costs, less price pressure

Alternative financing expectations

Hospitals and pharmacies increasingly demand leasing, RaaS, or outcome-based models, turning financing flexibility into a key negotiation lever and shifting price sensitivity toward payment structure rather than unit cost. Vendors often assume utilization risk to win contracts, compressing margins but protecting market access. Bundling consumables and long-term service contracts preserves lifetime value and offsets financing concessions.

- Demand: alternative financing

- Leverage: payment structure

- Risk: vendor-borne utilization

- Retention: consumable+service bundles

GPOs wield ≈90% spend; ≈62% require pilots; leasing shifts payment risk

Large hospital systems, retail chains and the top five GPOs (≈90% of GPO-managed spend) exert strong price and payment leverage; GPO purchasing exceeds $100B annually. Buyers demand pilots (≈62% of enterprise teams in 2024), validations and cybersecurity attestations, raising vendor compliance costs and reducing pure price pressure. Leasing, RaaS and outcome-based models shift sensitivity to payment structure and utilization risk.

| Metric | 2024 Value |

|---|---|

| Top-5 GPO coverage | ≈90% |

| GPO-managed spend | >$100B |

| POC requirement | ≈62% |

Preview the Actual Deliverable

JVM Porter's Five Forces Analysis

This preview displays the JVM Porter's Five Forces Analysis exactly as you'll receive it after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use the moment you complete payment. You're viewing the final deliverable in its entirety.