JVM PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and tech disruption are reshaping JVM's strategic landscape in our concise PESTLE overview. Packed with actionable insights for investors and strategists, it highlights risks and opportunities you can act on immediately. Purchase the full PESTLE for the complete, downloadable analysis and make smarter, faster decisions.

Political factors

Healthcare policy priorities

National policies on patient safety, digital health and hospital modernization are driving public procurement for automation and dispensing solutions as the global digital health market is forecast to exceed $600bn by 2027; JVM stands to gain when governments target medication error reduction and pharmacy workflow efficiency. Budget shifts under new administrations can delay or accelerate multi-year procurement cycles; monitoring policy roadmaps enables timely product alignment and advocacy.

Public procurement dynamics

Government-run tenders—public procurement representing roughly 12% of GDP in many OECD countries—shape JVM pricing power via fixed margins, certification requirements, and binding service SLAs. Transparent bidding favors established vendors with local partners and references, with awarded contracts often spanning 3–5 years. Long tender cycles (typically 6–18 months) slow revenue recognition but give multi-year visibility; localization clauses increasingly mandate regional assembly or service footprints.

Reimbursement frameworks

Reimbursement for pharmacy services and medication packaging directly affects ROI for hospitals and retail chains, given medication nonadherence costs the US health system an estimated 100–300 billion USD annually. Enhanced reimbursement for adherence packaging has driven faster pouch-system uptake in pilots, while policy cuts or payment freezes can pause capital upgrades. Engaging payers helps quantify savings from reduced adverse drug events, which average ~13,000 USD per hospitalization.

Trade and industrial policy

Tariffs on electronics, steel and precision components — notably US steel Section 232 at 25% and Section 301 tariffs up to 25% on hundreds of billions in goods — raise JVM machine BOM costs and squeeze margins; CHIPS Act funding of ~52.7 billion supports onshore component supply and faster lead times. Tightened 2023/24 export controls on advanced semiconductors and standards equivalence delays market entry, so strategic sourcing and regional assembly reduce exposure to policy shocks.

- Tariffs: US steel 25%, Section 301 up to 25%

- Incentives: CHIPS Act ~52.7B

- Export controls: tightened 2023/24 (semiconductors)

- Mitigation: strategic sourcing, regional assembly

Geopolitical stability

- Regional tensions → supply-chain delays, higher logistics risk

- Healthcare resilient but vulnerable to sanctions and currency volatility

- Governments may ease customs for critical medical devices

- Mandatory multi-country business continuity planning

Public procurement, digital health boom and CHIPS reshape device sales, costs and ROI

Public procurement (~12% GDP in OECD) and national digital health targets (global market >600bn by 2027) drive JVM sales; tenders (6–18m, contracts 3–5y) favor established local partners. Tariffs (US steel 25%, Section 301 ~25%) and CHIPS Act 52.7B shape BOM costs and onshoring. Reimbursement shifts and adherence savings (US nonadherence 100–300B; ADE ~13,000/hospital) affect ROI.

| Metric | Value |

|---|---|

| Public procurement | ~12% GDP |

| Digital health | >$600bn (2027) |

| CHIPS Act | $52.7B |

What is included in the product

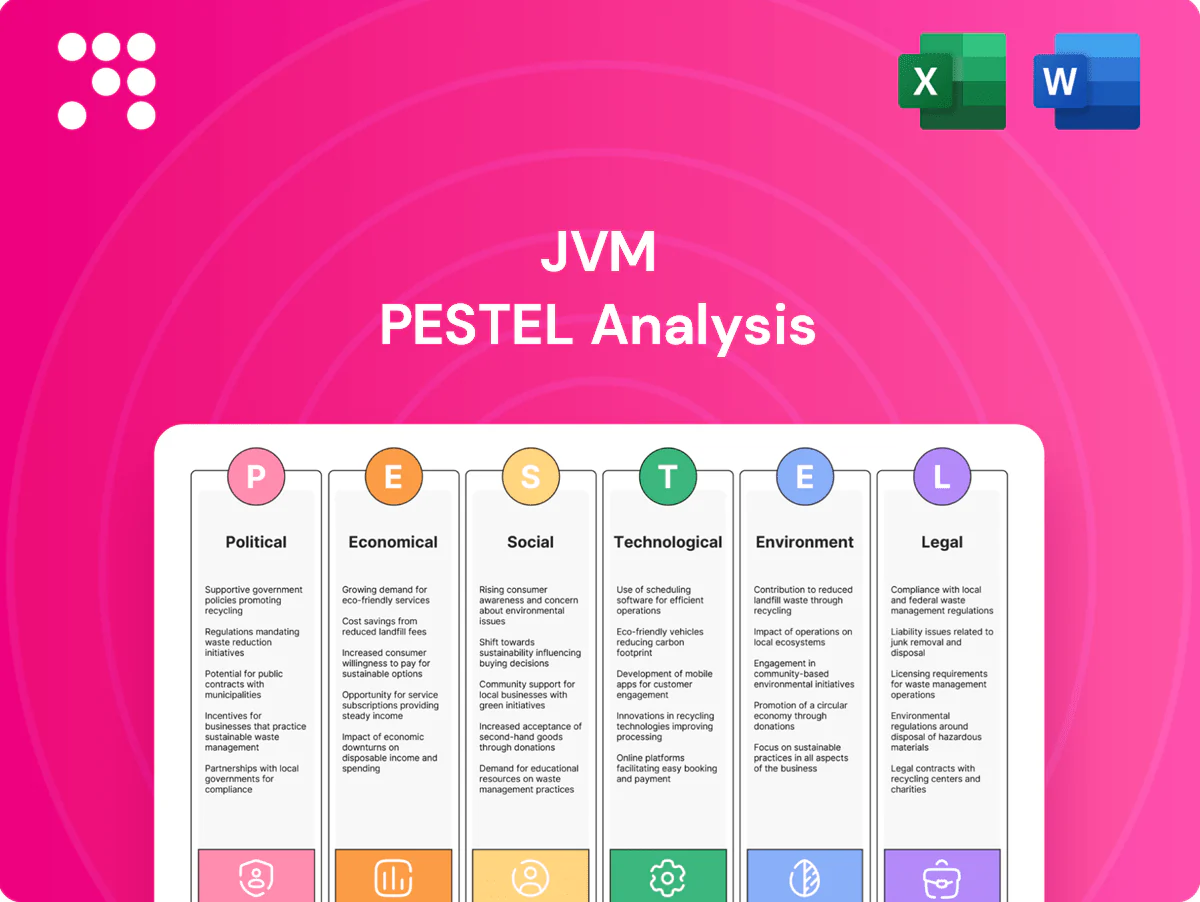

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the JVM, with each category expanded into data-backed subpoints and industry-specific examples. Designed for executives, investors and strategists, the analysis delivers forward-looking insights to identify risks, opportunities and scenarios ready for inclusion in business plans or pitch decks.

A compact JVM PESTLE summary that highlights regulatory, economic, technological and social impacts to quickly surface external risks, eliminate strategic blind spots, and streamline cross‑team decision‑making and planning.

Economic factors

Healthcare capex cycles

Hospital and pharmacy capex cycles drive demand for automated dispensing and packaging; with US healthcare spending at about 4.5 trillion in 2022, capital allocation shifts materially affect equipment upgrades. Economic slowdowns defer projects while stimulus can accelerate digitization, so JVM offering financing and modular rollouts smooths adoption and installed-base services cushion downturns.

Currency and input costs

FX swings (8–12% annualized on major pairs in 2023–24) force JVM to adjust export pricing and raise imported component costs; hedging and multi‑currency pricing have cut FX-driven margin erosion by around 3–6%. Long supplier frameworks (12–36 months) lock motor, sensor and semiconductor costs. Passing through post‑2022 inflation (peaked; global CPI ~3.5% in 2024) demands value‑based selling tied to measurable error reduction.

Labor market economics

Pharmacist shortages and rising wages (BLS median annual wage for pharmacists about 128,570 USD, May 2023) increase the ROI of automation. Time savings and error reductions translate directly to measurable cost avoidance in labor and adverse-event spend. JVM can quantify payback using workflow analytics to show hours saved, error-rate drops and weeks-to-months payback. Service models that reduce onsite labor are therefore highly attractive.

Market consolidation

Market consolidation: chain pharmacies and integrated delivery networks standardize platforms across sites, shifting buying power to fewer large buyers; by 2024 about 62% of US community hospitals were system-affiliated (AHA), increasing enterprise negotiation leverage while enabling scale deployments. JVM must deliver enterprise-wide interoperability, measurable SLAs, and turnkey reference wins to unlock regional rollouts.

- Consolidation: 62% hospital system affiliation (2024, AHA)

- Requirement: enterprise interoperability + SLAs

- Opportunity: reference wins enable regional expansion

Adherence and chronic disease spend

Rising chronic disease costs—CDC estimates chronic conditions drive about 90% of US health spending—push payers to fund adherence solutions as US health expenditures reached roughly $4.5 trillion in 2023. Pouch multi-dose packaging supports complex regimens and studies show adherence interventions can lower total cost of care by about 5–10%, improving outcomes. Economic evidence and health-outcomes studies accelerate payer adoption, enabling shared-savings partnerships.

- Tag: CDC – 90% of US health spending due to chronic disease

- Tag: NHCE 2023 – ~$4.5T total health spending

- Tag: Cost reduction – adherence programs ~5–10% lower total cost

- Tag: Payer models – shared-savings partnerships to align incentives

Public procurement, digital health boom and CHIPS reshape device sales, costs and ROI

Hospital/pharmacy capex cycles (US health spend ~$4.5T 2023) drive automation demand; financing and modular rollouts smooth adoption.

FX volatility (8–12% 2023–24) and CPI ~3.5% (2024) pressure margins; hedging and value-based pricing recover ~3–6%.

Pharmacist median wage $128,570 (May 2023) and 62% hospital system affiliation (2024) favor enterprise deals and service models.

| Metric | Value |

|---|---|

| US health spend | $4.5T (2023) |

| FX vol | 8–12% (2023–24) |

| CPI | ~3.5% (2024) |

| Pharmacist wage | $128,570 (May 2023) |

| Hosp system affiliation | 62% (2024) |

Same Document Delivered

JVM PESTLE Analysis

The preview shown here is the exact JVM PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains a comprehensive review of Political, Economic, Social, Technological, Legal, and Environmental factors affecting JVM, with structured insights and actionable implications. After checkout you’ll instantly download this identical, professionally prepared file.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and tech disruption are reshaping JVM's strategic landscape in our concise PESTLE overview. Packed with actionable insights for investors and strategists, it highlights risks and opportunities you can act on immediately. Purchase the full PESTLE for the complete, downloadable analysis and make smarter, faster decisions.

Political factors

Healthcare policy priorities

National policies on patient safety, digital health and hospital modernization are driving public procurement for automation and dispensing solutions as the global digital health market is forecast to exceed $600bn by 2027; JVM stands to gain when governments target medication error reduction and pharmacy workflow efficiency. Budget shifts under new administrations can delay or accelerate multi-year procurement cycles; monitoring policy roadmaps enables timely product alignment and advocacy.

Public procurement dynamics

Government-run tenders—public procurement representing roughly 12% of GDP in many OECD countries—shape JVM pricing power via fixed margins, certification requirements, and binding service SLAs. Transparent bidding favors established vendors with local partners and references, with awarded contracts often spanning 3–5 years. Long tender cycles (typically 6–18 months) slow revenue recognition but give multi-year visibility; localization clauses increasingly mandate regional assembly or service footprints.

Reimbursement frameworks

Reimbursement for pharmacy services and medication packaging directly affects ROI for hospitals and retail chains, given medication nonadherence costs the US health system an estimated 100–300 billion USD annually. Enhanced reimbursement for adherence packaging has driven faster pouch-system uptake in pilots, while policy cuts or payment freezes can pause capital upgrades. Engaging payers helps quantify savings from reduced adverse drug events, which average ~13,000 USD per hospitalization.

Trade and industrial policy

Tariffs on electronics, steel and precision components — notably US steel Section 232 at 25% and Section 301 tariffs up to 25% on hundreds of billions in goods — raise JVM machine BOM costs and squeeze margins; CHIPS Act funding of ~52.7 billion supports onshore component supply and faster lead times. Tightened 2023/24 export controls on advanced semiconductors and standards equivalence delays market entry, so strategic sourcing and regional assembly reduce exposure to policy shocks.

- Tariffs: US steel 25%, Section 301 up to 25%

- Incentives: CHIPS Act ~52.7B

- Export controls: tightened 2023/24 (semiconductors)

- Mitigation: strategic sourcing, regional assembly

Geopolitical stability

- Regional tensions → supply-chain delays, higher logistics risk

- Healthcare resilient but vulnerable to sanctions and currency volatility

- Governments may ease customs for critical medical devices

- Mandatory multi-country business continuity planning

Public procurement, digital health boom and CHIPS reshape device sales, costs and ROI

Public procurement (~12% GDP in OECD) and national digital health targets (global market >600bn by 2027) drive JVM sales; tenders (6–18m, contracts 3–5y) favor established local partners. Tariffs (US steel 25%, Section 301 ~25%) and CHIPS Act 52.7B shape BOM costs and onshoring. Reimbursement shifts and adherence savings (US nonadherence 100–300B; ADE ~13,000/hospital) affect ROI.

| Metric | Value |

|---|---|

| Public procurement | ~12% GDP |

| Digital health | >$600bn (2027) |

| CHIPS Act | $52.7B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the JVM, with each category expanded into data-backed subpoints and industry-specific examples. Designed for executives, investors and strategists, the analysis delivers forward-looking insights to identify risks, opportunities and scenarios ready for inclusion in business plans or pitch decks.

A compact JVM PESTLE summary that highlights regulatory, economic, technological and social impacts to quickly surface external risks, eliminate strategic blind spots, and streamline cross‑team decision‑making and planning.

Economic factors

Healthcare capex cycles

Hospital and pharmacy capex cycles drive demand for automated dispensing and packaging; with US healthcare spending at about 4.5 trillion in 2022, capital allocation shifts materially affect equipment upgrades. Economic slowdowns defer projects while stimulus can accelerate digitization, so JVM offering financing and modular rollouts smooths adoption and installed-base services cushion downturns.

Currency and input costs

FX swings (8–12% annualized on major pairs in 2023–24) force JVM to adjust export pricing and raise imported component costs; hedging and multi‑currency pricing have cut FX-driven margin erosion by around 3–6%. Long supplier frameworks (12–36 months) lock motor, sensor and semiconductor costs. Passing through post‑2022 inflation (peaked; global CPI ~3.5% in 2024) demands value‑based selling tied to measurable error reduction.

Labor market economics

Pharmacist shortages and rising wages (BLS median annual wage for pharmacists about 128,570 USD, May 2023) increase the ROI of automation. Time savings and error reductions translate directly to measurable cost avoidance in labor and adverse-event spend. JVM can quantify payback using workflow analytics to show hours saved, error-rate drops and weeks-to-months payback. Service models that reduce onsite labor are therefore highly attractive.

Market consolidation

Market consolidation: chain pharmacies and integrated delivery networks standardize platforms across sites, shifting buying power to fewer large buyers; by 2024 about 62% of US community hospitals were system-affiliated (AHA), increasing enterprise negotiation leverage while enabling scale deployments. JVM must deliver enterprise-wide interoperability, measurable SLAs, and turnkey reference wins to unlock regional rollouts.

- Consolidation: 62% hospital system affiliation (2024, AHA)

- Requirement: enterprise interoperability + SLAs

- Opportunity: reference wins enable regional expansion

Adherence and chronic disease spend

Rising chronic disease costs—CDC estimates chronic conditions drive about 90% of US health spending—push payers to fund adherence solutions as US health expenditures reached roughly $4.5 trillion in 2023. Pouch multi-dose packaging supports complex regimens and studies show adherence interventions can lower total cost of care by about 5–10%, improving outcomes. Economic evidence and health-outcomes studies accelerate payer adoption, enabling shared-savings partnerships.

- Tag: CDC – 90% of US health spending due to chronic disease

- Tag: NHCE 2023 – ~$4.5T total health spending

- Tag: Cost reduction – adherence programs ~5–10% lower total cost

- Tag: Payer models – shared-savings partnerships to align incentives

Public procurement, digital health boom and CHIPS reshape device sales, costs and ROI

Hospital/pharmacy capex cycles (US health spend ~$4.5T 2023) drive automation demand; financing and modular rollouts smooth adoption.

FX volatility (8–12% 2023–24) and CPI ~3.5% (2024) pressure margins; hedging and value-based pricing recover ~3–6%.

Pharmacist median wage $128,570 (May 2023) and 62% hospital system affiliation (2024) favor enterprise deals and service models.

| Metric | Value |

|---|---|

| US health spend | $4.5T (2023) |

| FX vol | 8–12% (2023–24) |

| CPI | ~3.5% (2024) |

| Pharmacist wage | $128,570 (May 2023) |

| Hosp system affiliation | 62% (2024) |

Same Document Delivered

JVM PESTLE Analysis

The preview shown here is the exact JVM PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains a comprehensive review of Political, Economic, Social, Technological, Legal, and Environmental factors affecting JVM, with structured insights and actionable implications. After checkout you’ll instantly download this identical, professionally prepared file.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and tech disruption are reshaping JVM's strategic landscape in our concise PESTLE overview. Packed with actionable insights for investors and strategists, it highlights risks and opportunities you can act on immediately. Purchase the full PESTLE for the complete, downloadable analysis and make smarter, faster decisions.

Political factors

Healthcare policy priorities

National policies on patient safety, digital health and hospital modernization are driving public procurement for automation and dispensing solutions as the global digital health market is forecast to exceed $600bn by 2027; JVM stands to gain when governments target medication error reduction and pharmacy workflow efficiency. Budget shifts under new administrations can delay or accelerate multi-year procurement cycles; monitoring policy roadmaps enables timely product alignment and advocacy.

Public procurement dynamics

Government-run tenders—public procurement representing roughly 12% of GDP in many OECD countries—shape JVM pricing power via fixed margins, certification requirements, and binding service SLAs. Transparent bidding favors established vendors with local partners and references, with awarded contracts often spanning 3–5 years. Long tender cycles (typically 6–18 months) slow revenue recognition but give multi-year visibility; localization clauses increasingly mandate regional assembly or service footprints.

Reimbursement frameworks

Reimbursement for pharmacy services and medication packaging directly affects ROI for hospitals and retail chains, given medication nonadherence costs the US health system an estimated 100–300 billion USD annually. Enhanced reimbursement for adherence packaging has driven faster pouch-system uptake in pilots, while policy cuts or payment freezes can pause capital upgrades. Engaging payers helps quantify savings from reduced adverse drug events, which average ~13,000 USD per hospitalization.

Trade and industrial policy

Tariffs on electronics, steel and precision components — notably US steel Section 232 at 25% and Section 301 tariffs up to 25% on hundreds of billions in goods — raise JVM machine BOM costs and squeeze margins; CHIPS Act funding of ~52.7 billion supports onshore component supply and faster lead times. Tightened 2023/24 export controls on advanced semiconductors and standards equivalence delays market entry, so strategic sourcing and regional assembly reduce exposure to policy shocks.

- Tariffs: US steel 25%, Section 301 up to 25%

- Incentives: CHIPS Act ~52.7B

- Export controls: tightened 2023/24 (semiconductors)

- Mitigation: strategic sourcing, regional assembly

Geopolitical stability

- Regional tensions → supply-chain delays, higher logistics risk

- Healthcare resilient but vulnerable to sanctions and currency volatility

- Governments may ease customs for critical medical devices

- Mandatory multi-country business continuity planning

Public procurement, digital health boom and CHIPS reshape device sales, costs and ROI

Public procurement (~12% GDP in OECD) and national digital health targets (global market >600bn by 2027) drive JVM sales; tenders (6–18m, contracts 3–5y) favor established local partners. Tariffs (US steel 25%, Section 301 ~25%) and CHIPS Act 52.7B shape BOM costs and onshoring. Reimbursement shifts and adherence savings (US nonadherence 100–300B; ADE ~13,000/hospital) affect ROI.

| Metric | Value |

|---|---|

| Public procurement | ~12% GDP |

| Digital health | >$600bn (2027) |

| CHIPS Act | $52.7B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the JVM, with each category expanded into data-backed subpoints and industry-specific examples. Designed for executives, investors and strategists, the analysis delivers forward-looking insights to identify risks, opportunities and scenarios ready for inclusion in business plans or pitch decks.

A compact JVM PESTLE summary that highlights regulatory, economic, technological and social impacts to quickly surface external risks, eliminate strategic blind spots, and streamline cross‑team decision‑making and planning.

Economic factors

Healthcare capex cycles

Hospital and pharmacy capex cycles drive demand for automated dispensing and packaging; with US healthcare spending at about 4.5 trillion in 2022, capital allocation shifts materially affect equipment upgrades. Economic slowdowns defer projects while stimulus can accelerate digitization, so JVM offering financing and modular rollouts smooths adoption and installed-base services cushion downturns.

Currency and input costs

FX swings (8–12% annualized on major pairs in 2023–24) force JVM to adjust export pricing and raise imported component costs; hedging and multi‑currency pricing have cut FX-driven margin erosion by around 3–6%. Long supplier frameworks (12–36 months) lock motor, sensor and semiconductor costs. Passing through post‑2022 inflation (peaked; global CPI ~3.5% in 2024) demands value‑based selling tied to measurable error reduction.

Labor market economics

Pharmacist shortages and rising wages (BLS median annual wage for pharmacists about 128,570 USD, May 2023) increase the ROI of automation. Time savings and error reductions translate directly to measurable cost avoidance in labor and adverse-event spend. JVM can quantify payback using workflow analytics to show hours saved, error-rate drops and weeks-to-months payback. Service models that reduce onsite labor are therefore highly attractive.

Market consolidation

Market consolidation: chain pharmacies and integrated delivery networks standardize platforms across sites, shifting buying power to fewer large buyers; by 2024 about 62% of US community hospitals were system-affiliated (AHA), increasing enterprise negotiation leverage while enabling scale deployments. JVM must deliver enterprise-wide interoperability, measurable SLAs, and turnkey reference wins to unlock regional rollouts.

- Consolidation: 62% hospital system affiliation (2024, AHA)

- Requirement: enterprise interoperability + SLAs

- Opportunity: reference wins enable regional expansion

Adherence and chronic disease spend

Rising chronic disease costs—CDC estimates chronic conditions drive about 90% of US health spending—push payers to fund adherence solutions as US health expenditures reached roughly $4.5 trillion in 2023. Pouch multi-dose packaging supports complex regimens and studies show adherence interventions can lower total cost of care by about 5–10%, improving outcomes. Economic evidence and health-outcomes studies accelerate payer adoption, enabling shared-savings partnerships.

- Tag: CDC – 90% of US health spending due to chronic disease

- Tag: NHCE 2023 – ~$4.5T total health spending

- Tag: Cost reduction – adherence programs ~5–10% lower total cost

- Tag: Payer models – shared-savings partnerships to align incentives

Public procurement, digital health boom and CHIPS reshape device sales, costs and ROI

Hospital/pharmacy capex cycles (US health spend ~$4.5T 2023) drive automation demand; financing and modular rollouts smooth adoption.

FX volatility (8–12% 2023–24) and CPI ~3.5% (2024) pressure margins; hedging and value-based pricing recover ~3–6%.

Pharmacist median wage $128,570 (May 2023) and 62% hospital system affiliation (2024) favor enterprise deals and service models.

| Metric | Value |

|---|---|

| US health spend | $4.5T (2023) |

| FX vol | 8–12% (2023–24) |

| CPI | ~3.5% (2024) |

| Pharmacist wage | $128,570 (May 2023) |

| Hosp system affiliation | 62% (2024) |

Same Document Delivered

JVM PESTLE Analysis

The preview shown here is the exact JVM PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains a comprehensive review of Political, Economic, Social, Technological, Legal, and Environmental factors affecting JVM, with structured insights and actionable implications. After checkout you’ll instantly download this identical, professionally prepared file.