Myriad SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Unpack Myriad’s competitive edge, vulnerabilities, and growth levers with our concise SWOT preview—then get the full, research-backed analysis to act with confidence. The complete report delivers detailed findings, strategic recommendations, and editable Word and Excel files for planning or pitching. Purchase now to access the investor-ready toolkit.

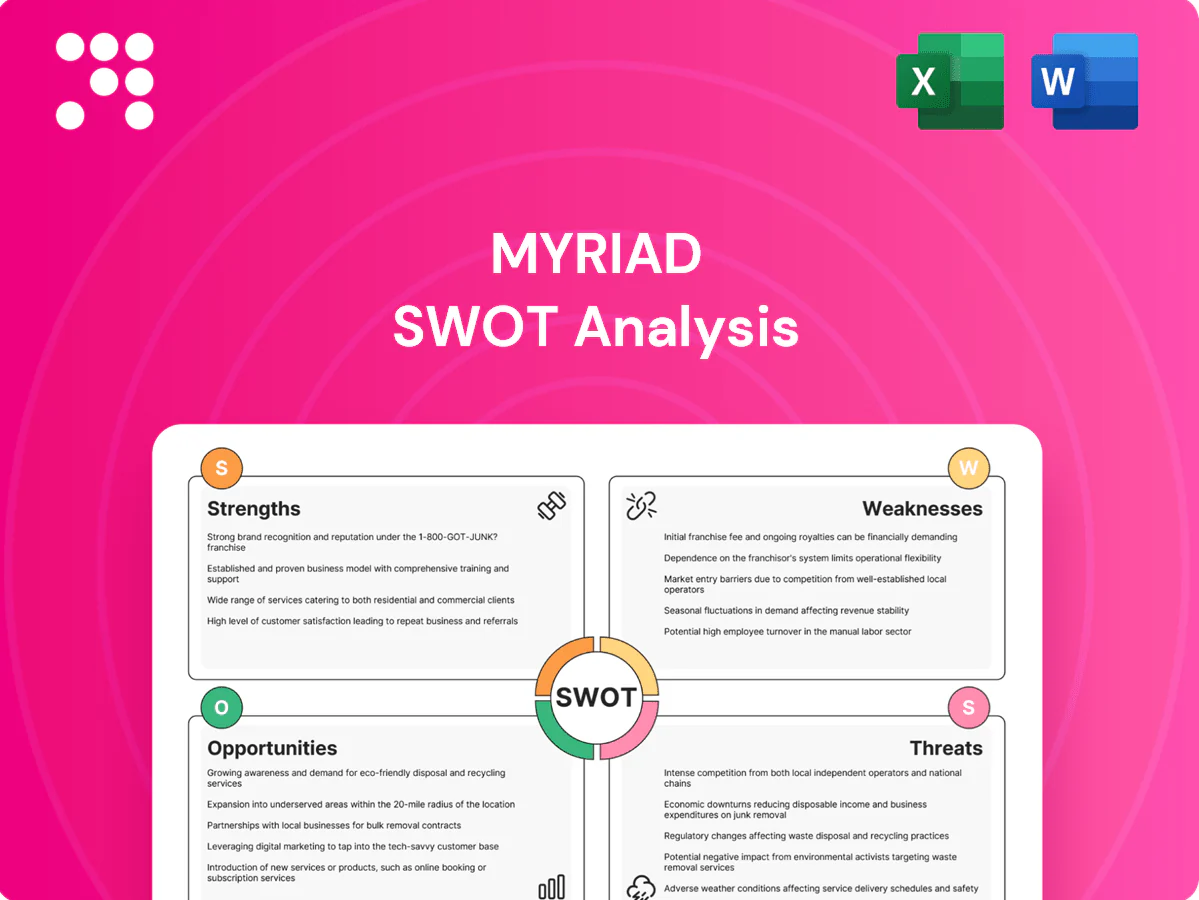

Strengths

Trusted brand in genetic testing

Myriad (NYSE:MYGN) has built a trusted oncology and women’s health brand over 30+ years, boosting clinician confidence and patient adoption. Decades of clinical use contribute to perceived reliability and support inclusion in clinical guidelines. Brand strength enhances payer negotiations and reduces customer acquisition costs in core segments.

Deep proprietary variant database

Myriad’s deep proprietary variant database improves interpretation accuracy and reporting speed by consolidating extensive curated evidence across genes, lowering VUS calls and reducing repeat testing. Superior call quality enhances clinical utility and provider satisfaction through clearer, actionable reports and faster turnaround. This accumulated data and clinician trust create a defensible moat that raises barriers for newer entrants.

Diversified portfolio across key indications

Myriad’s diversified portfolio across oncology, women’s health and pharmacogenomics smooths demand cycles, with FY2024 revenue of about $594 million reflecting broad-based income. Multiple revenue streams reduce dependence on any single test, lowering concentration risk. Cross-selling between divisions boosts account value and lifetime customer revenue. This mix enhances resilience amid policy changes or competitive pressure.

Established payer coverage and guidelines presence

Established payer coverage reduces patient out-of-pocket friction and boosts test volumes, with contracts spanning major commercial payers covering over 200 million U.S. lives, and inclusion in clinical guidelines standardizes ordering and drives steady referral patterns. Contracted rates with payers and health systems increase revenue visibility and reinforce partnerships with top IDNs.

- Lower OOP, higher volumes

- Guideline-driven ordering

- Contracted rates = revenue visibility

- Stronger HS/IDN relationships

Integrated lab operations and clinician support

Integrated end-to-end lab operations let Myriad control quality and turnaround, while embedded genetic counseling and provider education drive appropriate test utilization and referral growth; seamless ordering and reporting tools streamline clinician workflow and boost retention.

- Quality control: centralized lab processes

- Utilization: genetic counseling embedded

- Workflow: seamless ordering/reporting

- Business impact: higher retention and referrals

Clinically trusted genomics with $594M rev, covers ~200M

Myriad leverages 30+ years of clinical trust, driving clinician adoption and guideline inclusion. FY2024 revenue was about $594 million, reflecting diversified oncology, women’s health, and pharmacogenomics streams. Payer contracts cover ~200 million U.S. lives, improving access and volume. Proprietary variant database and in-house labs lower VUS rates and speed turnaround, strengthening provider loyalty.

| Metric | Value |

|---|---|

| FY2024 revenue | $594M |

| Payer-covered lives | ~200M |

| Market tenure | 30+ years |

What is included in the product

Delivers a strategic overview of Myriad’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess competitive position and inform strategic decisions about growth and risk management.

Myriad's SWOT Analysis delivers a compact, visual overview that quickly aligns teams, clarifies priorities, and reduces time spent on strategic debates, easing decision-making and coordination across units.

Weaknesses

Exposure to reimbursement variability

Coverage policy and coding changes materially affect Myriad’s test pricing and volumes, with shifting payer policies driving demand volatility. Prior authorization requirements slow clinical adoption and create access bottlenecks. Higher claim denials raise administrative costs and elongate cash conversion cycles. These factors keep margin predictability constrained.

Legacy patent and litigation overhang

Historic IP battles culminated in the 2013 Supreme Court decision (AMP v. Myriad) that invalidated key gene patents, diluting Myriad’s prior exclusivity. Competitors rapidly expanded BRCA and hereditary cancer panels once barriers fell, compressing pricing and market share. Ongoing legal costs and potential follow‑on disputes remain a recurring drain, and investors often price this litigation overhang into Myriad’s valuation.

Profitability sensitivity to volume mix

Myriad’s high fixed lab and staffing costs mean profitability hinges on volume scale, so downward mix shifts toward lower-ASP tests can materially compress margins. Volatile case mix has repeatedly pressured EBITDA in prior quarters, heightening reliance on steady demand and long-term test adoption rates. This sensitivity limits earnings leverage during reimbursement or demand softness.

Complex regulatory compliance footprint

Operating under CLIA and CAP while FDA continues to consider expanded LDT oversight increases costs through enhanced documentation, validation and QA; these processes are resource-intensive and raise per-test operating expenses. Multi-state and international regulatory variations complicate rollouts and revenue recognition, and any compliance lapse could trigger stoppages, fines or lab shutdowns that materially disrupt operations.

- Regulatory layers: CLIA/CAP plus potential FDA LDT changes

- Resource burden: extensive documentation, validation, QA

- Geographic complexity: divergent state and international rules

- Operational risk: lapses can halt lab services or invite penalties

Data integration and interoperability gaps

Data integration and interoperability gaps fragment EHR connectivity, hindering order placement and timely result delivery; 96% of US hospitals use certified EHRs (ONC 2022) yet exchange remains inconsistent. Limited workflow integration reduces provider stickiness and increases churn. Manual processes raise error risk and overhead, slowing scale-up in large health systems.

- Fragmented EHR connectivity — delays in orders/results

- Limited workflow integration — lower provider retention

- Manual processes — higher error rate and overhead

- Scale barrier — harder rollout across large systems

Prior auths, payer shifts and 2013 IP ruling pressure lab margins 96% EHRs

Payer policy shifts and prior authorization drive demand volatility and higher denials, constraining margin predictability. Loss of patent exclusivity after AMP v. Myriad (2013) enabled rapid competitor entry and pricing pressure. High fixed lab costs and regulatory/LDT uncertainty make profitability volume‑sensitive; EHR fragmentation (96% hospitals use certified EHRs, ONC 2022) limits workflow stickiness.

| Issue | Relevant fact |

|---|---|

| EHR reach | 96% hospitals use certified EHRs (ONC 2022) |

| IP watershed | AMP v. Myriad, 2013 |

| Volume risk | High fixed lab/staff costs |

Same Document Delivered

Myriad SWOT Analysis

This is the actual Myriad SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. The file shown is the real analysis you'll download post-purchase and is ready to use immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Unpack Myriad’s competitive edge, vulnerabilities, and growth levers with our concise SWOT preview—then get the full, research-backed analysis to act with confidence. The complete report delivers detailed findings, strategic recommendations, and editable Word and Excel files for planning or pitching. Purchase now to access the investor-ready toolkit.

Strengths

Trusted brand in genetic testing

Myriad (NYSE:MYGN) has built a trusted oncology and women’s health brand over 30+ years, boosting clinician confidence and patient adoption. Decades of clinical use contribute to perceived reliability and support inclusion in clinical guidelines. Brand strength enhances payer negotiations and reduces customer acquisition costs in core segments.

Deep proprietary variant database

Myriad’s deep proprietary variant database improves interpretation accuracy and reporting speed by consolidating extensive curated evidence across genes, lowering VUS calls and reducing repeat testing. Superior call quality enhances clinical utility and provider satisfaction through clearer, actionable reports and faster turnaround. This accumulated data and clinician trust create a defensible moat that raises barriers for newer entrants.

Diversified portfolio across key indications

Myriad’s diversified portfolio across oncology, women’s health and pharmacogenomics smooths demand cycles, with FY2024 revenue of about $594 million reflecting broad-based income. Multiple revenue streams reduce dependence on any single test, lowering concentration risk. Cross-selling between divisions boosts account value and lifetime customer revenue. This mix enhances resilience amid policy changes or competitive pressure.

Established payer coverage and guidelines presence

Established payer coverage reduces patient out-of-pocket friction and boosts test volumes, with contracts spanning major commercial payers covering over 200 million U.S. lives, and inclusion in clinical guidelines standardizes ordering and drives steady referral patterns. Contracted rates with payers and health systems increase revenue visibility and reinforce partnerships with top IDNs.

- Lower OOP, higher volumes

- Guideline-driven ordering

- Contracted rates = revenue visibility

- Stronger HS/IDN relationships

Integrated lab operations and clinician support

Integrated end-to-end lab operations let Myriad control quality and turnaround, while embedded genetic counseling and provider education drive appropriate test utilization and referral growth; seamless ordering and reporting tools streamline clinician workflow and boost retention.

- Quality control: centralized lab processes

- Utilization: genetic counseling embedded

- Workflow: seamless ordering/reporting

- Business impact: higher retention and referrals

Clinically trusted genomics with $594M rev, covers ~200M

Myriad leverages 30+ years of clinical trust, driving clinician adoption and guideline inclusion. FY2024 revenue was about $594 million, reflecting diversified oncology, women’s health, and pharmacogenomics streams. Payer contracts cover ~200 million U.S. lives, improving access and volume. Proprietary variant database and in-house labs lower VUS rates and speed turnaround, strengthening provider loyalty.

| Metric | Value |

|---|---|

| FY2024 revenue | $594M |

| Payer-covered lives | ~200M |

| Market tenure | 30+ years |

What is included in the product

Delivers a strategic overview of Myriad’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess competitive position and inform strategic decisions about growth and risk management.

Myriad's SWOT Analysis delivers a compact, visual overview that quickly aligns teams, clarifies priorities, and reduces time spent on strategic debates, easing decision-making and coordination across units.

Weaknesses

Exposure to reimbursement variability

Coverage policy and coding changes materially affect Myriad’s test pricing and volumes, with shifting payer policies driving demand volatility. Prior authorization requirements slow clinical adoption and create access bottlenecks. Higher claim denials raise administrative costs and elongate cash conversion cycles. These factors keep margin predictability constrained.

Legacy patent and litigation overhang

Historic IP battles culminated in the 2013 Supreme Court decision (AMP v. Myriad) that invalidated key gene patents, diluting Myriad’s prior exclusivity. Competitors rapidly expanded BRCA and hereditary cancer panels once barriers fell, compressing pricing and market share. Ongoing legal costs and potential follow‑on disputes remain a recurring drain, and investors often price this litigation overhang into Myriad’s valuation.

Profitability sensitivity to volume mix

Myriad’s high fixed lab and staffing costs mean profitability hinges on volume scale, so downward mix shifts toward lower-ASP tests can materially compress margins. Volatile case mix has repeatedly pressured EBITDA in prior quarters, heightening reliance on steady demand and long-term test adoption rates. This sensitivity limits earnings leverage during reimbursement or demand softness.

Complex regulatory compliance footprint

Operating under CLIA and CAP while FDA continues to consider expanded LDT oversight increases costs through enhanced documentation, validation and QA; these processes are resource-intensive and raise per-test operating expenses. Multi-state and international regulatory variations complicate rollouts and revenue recognition, and any compliance lapse could trigger stoppages, fines or lab shutdowns that materially disrupt operations.

- Regulatory layers: CLIA/CAP plus potential FDA LDT changes

- Resource burden: extensive documentation, validation, QA

- Geographic complexity: divergent state and international rules

- Operational risk: lapses can halt lab services or invite penalties

Data integration and interoperability gaps

Data integration and interoperability gaps fragment EHR connectivity, hindering order placement and timely result delivery; 96% of US hospitals use certified EHRs (ONC 2022) yet exchange remains inconsistent. Limited workflow integration reduces provider stickiness and increases churn. Manual processes raise error risk and overhead, slowing scale-up in large health systems.

- Fragmented EHR connectivity — delays in orders/results

- Limited workflow integration — lower provider retention

- Manual processes — higher error rate and overhead

- Scale barrier — harder rollout across large systems

Prior auths, payer shifts and 2013 IP ruling pressure lab margins 96% EHRs

Payer policy shifts and prior authorization drive demand volatility and higher denials, constraining margin predictability. Loss of patent exclusivity after AMP v. Myriad (2013) enabled rapid competitor entry and pricing pressure. High fixed lab costs and regulatory/LDT uncertainty make profitability volume‑sensitive; EHR fragmentation (96% hospitals use certified EHRs, ONC 2022) limits workflow stickiness.

| Issue | Relevant fact |

|---|---|

| EHR reach | 96% hospitals use certified EHRs (ONC 2022) |

| IP watershed | AMP v. Myriad, 2013 |

| Volume risk | High fixed lab/staff costs |

Same Document Delivered

Myriad SWOT Analysis

This is the actual Myriad SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. The file shown is the real analysis you'll download post-purchase and is ready to use immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Unpack Myriad’s competitive edge, vulnerabilities, and growth levers with our concise SWOT preview—then get the full, research-backed analysis to act with confidence. The complete report delivers detailed findings, strategic recommendations, and editable Word and Excel files for planning or pitching. Purchase now to access the investor-ready toolkit.

Strengths

Trusted brand in genetic testing

Myriad (NYSE:MYGN) has built a trusted oncology and women’s health brand over 30+ years, boosting clinician confidence and patient adoption. Decades of clinical use contribute to perceived reliability and support inclusion in clinical guidelines. Brand strength enhances payer negotiations and reduces customer acquisition costs in core segments.

Deep proprietary variant database

Myriad’s deep proprietary variant database improves interpretation accuracy and reporting speed by consolidating extensive curated evidence across genes, lowering VUS calls and reducing repeat testing. Superior call quality enhances clinical utility and provider satisfaction through clearer, actionable reports and faster turnaround. This accumulated data and clinician trust create a defensible moat that raises barriers for newer entrants.

Diversified portfolio across key indications

Myriad’s diversified portfolio across oncology, women’s health and pharmacogenomics smooths demand cycles, with FY2024 revenue of about $594 million reflecting broad-based income. Multiple revenue streams reduce dependence on any single test, lowering concentration risk. Cross-selling between divisions boosts account value and lifetime customer revenue. This mix enhances resilience amid policy changes or competitive pressure.

Established payer coverage and guidelines presence

Established payer coverage reduces patient out-of-pocket friction and boosts test volumes, with contracts spanning major commercial payers covering over 200 million U.S. lives, and inclusion in clinical guidelines standardizes ordering and drives steady referral patterns. Contracted rates with payers and health systems increase revenue visibility and reinforce partnerships with top IDNs.

- Lower OOP, higher volumes

- Guideline-driven ordering

- Contracted rates = revenue visibility

- Stronger HS/IDN relationships

Integrated lab operations and clinician support

Integrated end-to-end lab operations let Myriad control quality and turnaround, while embedded genetic counseling and provider education drive appropriate test utilization and referral growth; seamless ordering and reporting tools streamline clinician workflow and boost retention.

- Quality control: centralized lab processes

- Utilization: genetic counseling embedded

- Workflow: seamless ordering/reporting

- Business impact: higher retention and referrals

Clinically trusted genomics with $594M rev, covers ~200M

Myriad leverages 30+ years of clinical trust, driving clinician adoption and guideline inclusion. FY2024 revenue was about $594 million, reflecting diversified oncology, women’s health, and pharmacogenomics streams. Payer contracts cover ~200 million U.S. lives, improving access and volume. Proprietary variant database and in-house labs lower VUS rates and speed turnaround, strengthening provider loyalty.

| Metric | Value |

|---|---|

| FY2024 revenue | $594M |

| Payer-covered lives | ~200M |

| Market tenure | 30+ years |

What is included in the product

Delivers a strategic overview of Myriad’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess competitive position and inform strategic decisions about growth and risk management.

Myriad's SWOT Analysis delivers a compact, visual overview that quickly aligns teams, clarifies priorities, and reduces time spent on strategic debates, easing decision-making and coordination across units.

Weaknesses

Exposure to reimbursement variability

Coverage policy and coding changes materially affect Myriad’s test pricing and volumes, with shifting payer policies driving demand volatility. Prior authorization requirements slow clinical adoption and create access bottlenecks. Higher claim denials raise administrative costs and elongate cash conversion cycles. These factors keep margin predictability constrained.

Legacy patent and litigation overhang

Historic IP battles culminated in the 2013 Supreme Court decision (AMP v. Myriad) that invalidated key gene patents, diluting Myriad’s prior exclusivity. Competitors rapidly expanded BRCA and hereditary cancer panels once barriers fell, compressing pricing and market share. Ongoing legal costs and potential follow‑on disputes remain a recurring drain, and investors often price this litigation overhang into Myriad’s valuation.

Profitability sensitivity to volume mix

Myriad’s high fixed lab and staffing costs mean profitability hinges on volume scale, so downward mix shifts toward lower-ASP tests can materially compress margins. Volatile case mix has repeatedly pressured EBITDA in prior quarters, heightening reliance on steady demand and long-term test adoption rates. This sensitivity limits earnings leverage during reimbursement or demand softness.

Complex regulatory compliance footprint

Operating under CLIA and CAP while FDA continues to consider expanded LDT oversight increases costs through enhanced documentation, validation and QA; these processes are resource-intensive and raise per-test operating expenses. Multi-state and international regulatory variations complicate rollouts and revenue recognition, and any compliance lapse could trigger stoppages, fines or lab shutdowns that materially disrupt operations.

- Regulatory layers: CLIA/CAP plus potential FDA LDT changes

- Resource burden: extensive documentation, validation, QA

- Geographic complexity: divergent state and international rules

- Operational risk: lapses can halt lab services or invite penalties

Data integration and interoperability gaps

Data integration and interoperability gaps fragment EHR connectivity, hindering order placement and timely result delivery; 96% of US hospitals use certified EHRs (ONC 2022) yet exchange remains inconsistent. Limited workflow integration reduces provider stickiness and increases churn. Manual processes raise error risk and overhead, slowing scale-up in large health systems.

- Fragmented EHR connectivity — delays in orders/results

- Limited workflow integration — lower provider retention

- Manual processes — higher error rate and overhead

- Scale barrier — harder rollout across large systems

Prior auths, payer shifts and 2013 IP ruling pressure lab margins 96% EHRs

Payer policy shifts and prior authorization drive demand volatility and higher denials, constraining margin predictability. Loss of patent exclusivity after AMP v. Myriad (2013) enabled rapid competitor entry and pricing pressure. High fixed lab costs and regulatory/LDT uncertainty make profitability volume‑sensitive; EHR fragmentation (96% hospitals use certified EHRs, ONC 2022) limits workflow stickiness.

| Issue | Relevant fact |

|---|---|

| EHR reach | 96% hospitals use certified EHRs (ONC 2022) |

| IP watershed | AMP v. Myriad, 2013 |

| Volume risk | High fixed lab/staff costs |

Same Document Delivered

Myriad SWOT Analysis

This is the actual Myriad SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. The file shown is the real analysis you'll download post-purchase and is ready to use immediately after checkout.