NAB - National Australia Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

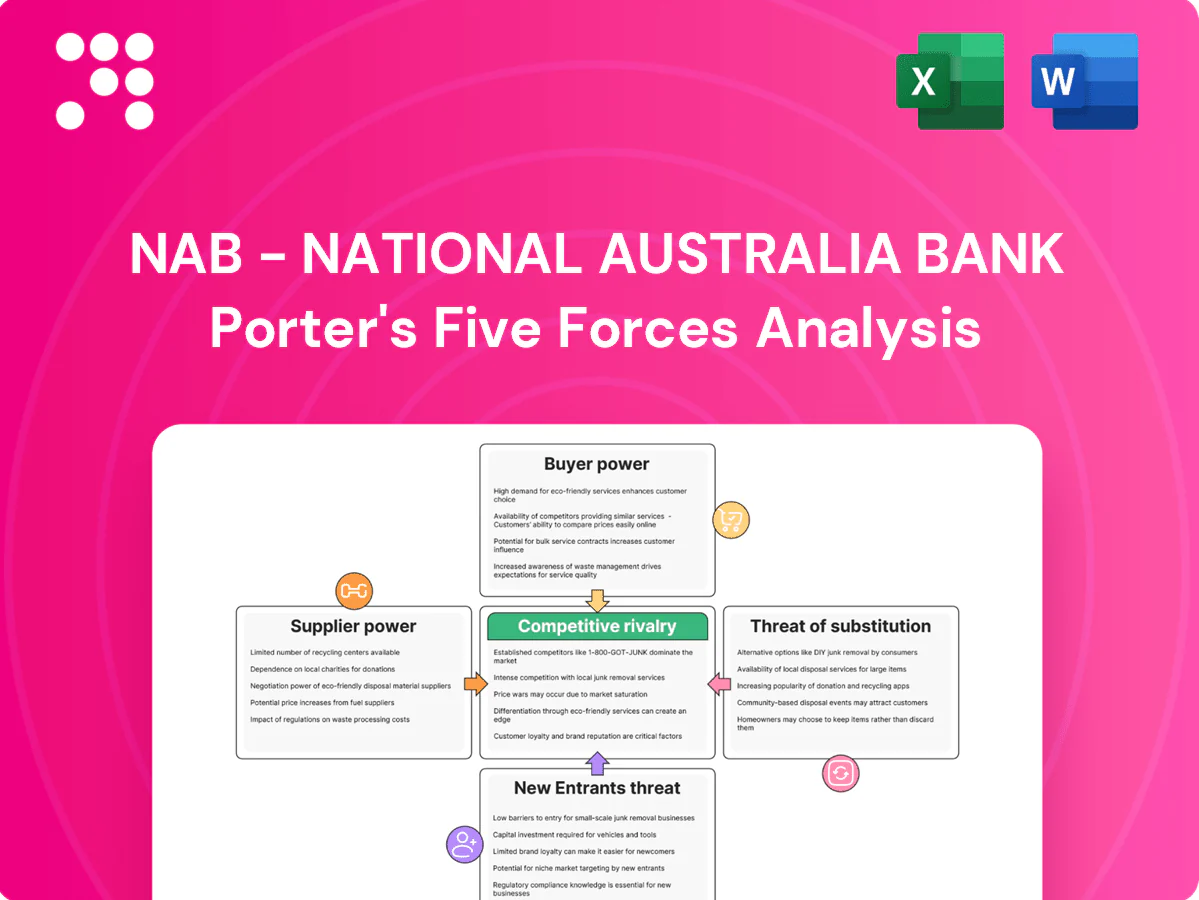

NAB faces fierce rivalry from major banks and fintechs, moderate buyer power as consumers demand digital value, and manageable supplier influence but rising regulatory and substitute threats; its scale and branch network remain key advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report for actionable insights tailored to NAB.

Suppliers Bargaining Power

Wholesale funding dependence

NAB relies on domestic and offshore wholesale markets for roughly 27% of its funding, supplying term funding beyond deposits. Large institutional investors can demand higher spreads in volatile conditions, lifting funding costs as seen in 2023–24 spread widenings. Central bank facilities (RBA/ESF) can temper spikes but are conditional and temporary. Diversification across tenors and currencies mitigates risk, though market liquidity concentration remains a leverage point.

Core tech and cloud vendors

NAB depends on a concentrated set of core banking, cloud and cybersecurity vendors for stability and scalability, creating supplier pricing power and contractual leverage. Hyperscalers AWS and Microsoft Azure held roughly 54% combined cloud market share in 2024 (AWS ~31%, Azure ~23%), amplifying switching complexity and lock-in from long implementation cycles. Strategic partnerships can trade price concessions for faster innovation and greater resilience.

Payment networks and rails

Card schemes (Visa/Mastercard, ~80% global card volume) and domestic rails like NPP and clearing systems are essential inputs for NAB, with scheme fee structures and rule changes directly affecting unit economics and merchant margins. Limited credible alternatives to these networks heighten supplier influence, though NAB’s seats in industry governance and scheme boards partially mitigate fee/rule pressure.

Specialist talent and contractors

Specialist risk, data, engineering and compliance talent markets are tight in Australia and New Zealand, giving suppliers leverage as wage inflation and retention premiums rise; Australia wage price index grew about 3.7% year to June 2024 and New Zealand WPI ~3.4% in Q2 2024. Outsourcing and nearshoring ease supply but add coordination and control risk, while automation and AI can gradually reduce dependency and unit labour costs.

- WPI: AUS 3.7% (y/y Jun 2024)

- NZ WPI: ~3.4% (Q2 2024)

- High retention premiums = supplier leverage

- Outsourcing helps but adds coordination risk

- Automation = medium-term dependency reduction

Data, analytics, and credit bureaus

Credit bureaus (Equifax, Experian, Illion), market data and analytics platforms underpin underwriting and monitoring for banks including NAB; proprietary scoring and unique datasets increase supplier leverage by differentiating risk models. Open Banking/Consumer Data Right rollout (2019–2020) broadened sources but integration and compliance costs remain material. Multi-sourcing reduces concentration risk yet curbs volume discounts and bargaining power.

- Three major bureaus: Equifax, Experian, Illion

- Open Banking (CDR) rollout 2019–2020 expanded data access

- Proprietary scores raise supplier leverage; multi-sourcing trades scale for resilience

Moderate supplier power: 27% wholesale funding, ~54% hyperscaler share, ~80% card volume

NAB faces moderate supplier power: 27% wholesale funding dependence raises sensitivity to market spreads; hyperscaler concentration (AWS ~31%, Azure ~23% = ~54% combined in 2024) and card schemes (~80% global volume) create switching costs; tight tech/compliance talent (AUS WPI 3.7% y/y Jun 2024, NZ WPI ~3.4% Q2 2024) increases wage pressure, while multi‑sourcing and central bank backstops limit extremes.

| Supplier | Metric | 2024 |

|---|---|---|

| Wholesale funding | Share of funding | 27% |

| Cloud hyperscalers | AWS+Azure | ~54% (AWS31/AZ23) |

| Card schemes | Global volume | ~80% |

| Wage pressure | WPI Australia/NZ | 3.7% / 3.4% |

| Credit bureaus | Major providers | Equifax, Experian, Illion |

What is included in the product

Tailored Porter's Five Forces analysis for NAB - National Australia Bank, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats to its profitability and strategic positioning.

A clear, one-sheet Porter's Five Forces summary for NAB—instantly highlights competitive pressures across rivals, suppliers, customers, new entrants and substitutes to speed strategic decisions and reduce analysis time.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can switch rapidly as the RBA cash rate rose to about 4.35% in 2024, squeezing net interest margins and forcing NAB to match higher term and bonus saver rates. Real-time onboarding and comparison sites increase price transparency, shortening switching cycles and elevating acquisition churn. Incentive cycles and term promotions raise short-term acquisition costs, while product innovation (features, digital tools) can partly shift competition away from pure rate.

Mortgage customers with options

Australians and New Zealanders refinance often, with the broker channel handling about 66% of new home loans (MFAA 2023), increasing switching. Cashback offers—commonly up to A$3,000 in 2023–24—and headline rate discounts drive price-based competition. Faster digital conditional approvals (often within 24 hours) compress decision windows and boost buyer leverage. Loyalty is fragile absent clear service differentiation.

SMEs and corporates via RFPs

Larger SMEs and corporates run competitive RFPs for lending, transaction banking and markets, shrinking NABs pricing power as bundled pricing and relationship limits cap margins. Sophisticated treasury teams routinely negotiate covenants and fees, leveraging market comparators. Modular platforms and APIs, reinforced by the 2024 expansion of Australias Consumer Data Right for banking, make switching and onboarding faster and cheaper.

Multi-banking and low switching costs

Customers increasingly multi-bank; NAB serves over 7 million customers (2024), and Open Banking via Australia's CDR exceeded 4 million consents by 2024, lowering switching friction. Buyers unbundle products, choosing best-in-class fintechs for payments, lending and wealth. Retention now hinges on deep ecosystem integration and data-driven personalization to raise switching costs despite low transactional barriers.

- Multi-banking prevalence — >7M NAB customers (2024)

- Open Banking impact — CDR >4M consents (2024)

- Unbundling — product-by-product buyer choice

- Retention drivers — ecosystem + personalization

Digital experience expectations

Users benchmark NAB against fintech and big-tech UX; outages or poor journeys drive churn even when NAB is competitively priced, as Australia’s big four banks hold about 80% of deposits and face intense digital comparison pressure.

- Self-service and 24/7 support are table stakes

- Superior app features can offset modest price gaps

- Digital reliability directly affects retention

Rising rates, broker dominance and CDR fuel mass switching, squeezing bank margins

Customers have high bargaining power: rate-sensitive depositors and over 7M NAB customers (2024) switch quickly as the RBA cash rate rose to ~4.35% in 2024, squeezing NIMs. Brokers handle ~66% of new home loans (MFAA 2023) and CDR consents exceeded 4M (2024), lowering switching costs. SMEs run competitive RFPs and unbundle services, forcing price and feature competition.

| Metric | 2023–24 |

|---|---|

| NAB customers | >7M |

| CDR consents | >4M |

| Broker share (home loans) | 66% |

| RBA cash rate | ≈4.35% |

| Typical cashback | up to A$3,000 |

Preview the Actual Deliverable

NAB - National Australia Bank Porter's Five Forces Analysis

This preview shows the exact NAB - National Australia Bank Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The document displayed is the final, professionally formatted file, ready for download and use the moment you buy. You’re viewing the same complete analysis that will be available to you instantly after payment.

Don't Miss the Bigger Picture

NAB faces fierce rivalry from major banks and fintechs, moderate buyer power as consumers demand digital value, and manageable supplier influence but rising regulatory and substitute threats; its scale and branch network remain key advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report for actionable insights tailored to NAB.

Suppliers Bargaining Power

Wholesale funding dependence

NAB relies on domestic and offshore wholesale markets for roughly 27% of its funding, supplying term funding beyond deposits. Large institutional investors can demand higher spreads in volatile conditions, lifting funding costs as seen in 2023–24 spread widenings. Central bank facilities (RBA/ESF) can temper spikes but are conditional and temporary. Diversification across tenors and currencies mitigates risk, though market liquidity concentration remains a leverage point.

Core tech and cloud vendors

NAB depends on a concentrated set of core banking, cloud and cybersecurity vendors for stability and scalability, creating supplier pricing power and contractual leverage. Hyperscalers AWS and Microsoft Azure held roughly 54% combined cloud market share in 2024 (AWS ~31%, Azure ~23%), amplifying switching complexity and lock-in from long implementation cycles. Strategic partnerships can trade price concessions for faster innovation and greater resilience.

Payment networks and rails

Card schemes (Visa/Mastercard, ~80% global card volume) and domestic rails like NPP and clearing systems are essential inputs for NAB, with scheme fee structures and rule changes directly affecting unit economics and merchant margins. Limited credible alternatives to these networks heighten supplier influence, though NAB’s seats in industry governance and scheme boards partially mitigate fee/rule pressure.

Specialist talent and contractors

Specialist risk, data, engineering and compliance talent markets are tight in Australia and New Zealand, giving suppliers leverage as wage inflation and retention premiums rise; Australia wage price index grew about 3.7% year to June 2024 and New Zealand WPI ~3.4% in Q2 2024. Outsourcing and nearshoring ease supply but add coordination and control risk, while automation and AI can gradually reduce dependency and unit labour costs.

- WPI: AUS 3.7% (y/y Jun 2024)

- NZ WPI: ~3.4% (Q2 2024)

- High retention premiums = supplier leverage

- Outsourcing helps but adds coordination risk

- Automation = medium-term dependency reduction

Data, analytics, and credit bureaus

Credit bureaus (Equifax, Experian, Illion), market data and analytics platforms underpin underwriting and monitoring for banks including NAB; proprietary scoring and unique datasets increase supplier leverage by differentiating risk models. Open Banking/Consumer Data Right rollout (2019–2020) broadened sources but integration and compliance costs remain material. Multi-sourcing reduces concentration risk yet curbs volume discounts and bargaining power.

- Three major bureaus: Equifax, Experian, Illion

- Open Banking (CDR) rollout 2019–2020 expanded data access

- Proprietary scores raise supplier leverage; multi-sourcing trades scale for resilience

Moderate supplier power: 27% wholesale funding, ~54% hyperscaler share, ~80% card volume

NAB faces moderate supplier power: 27% wholesale funding dependence raises sensitivity to market spreads; hyperscaler concentration (AWS ~31%, Azure ~23% = ~54% combined in 2024) and card schemes (~80% global volume) create switching costs; tight tech/compliance talent (AUS WPI 3.7% y/y Jun 2024, NZ WPI ~3.4% Q2 2024) increases wage pressure, while multi‑sourcing and central bank backstops limit extremes.

| Supplier | Metric | 2024 |

|---|---|---|

| Wholesale funding | Share of funding | 27% |

| Cloud hyperscalers | AWS+Azure | ~54% (AWS31/AZ23) |

| Card schemes | Global volume | ~80% |

| Wage pressure | WPI Australia/NZ | 3.7% / 3.4% |

| Credit bureaus | Major providers | Equifax, Experian, Illion |

What is included in the product

Tailored Porter's Five Forces analysis for NAB - National Australia Bank, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats to its profitability and strategic positioning.

A clear, one-sheet Porter's Five Forces summary for NAB—instantly highlights competitive pressures across rivals, suppliers, customers, new entrants and substitutes to speed strategic decisions and reduce analysis time.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can switch rapidly as the RBA cash rate rose to about 4.35% in 2024, squeezing net interest margins and forcing NAB to match higher term and bonus saver rates. Real-time onboarding and comparison sites increase price transparency, shortening switching cycles and elevating acquisition churn. Incentive cycles and term promotions raise short-term acquisition costs, while product innovation (features, digital tools) can partly shift competition away from pure rate.

Mortgage customers with options

Australians and New Zealanders refinance often, with the broker channel handling about 66% of new home loans (MFAA 2023), increasing switching. Cashback offers—commonly up to A$3,000 in 2023–24—and headline rate discounts drive price-based competition. Faster digital conditional approvals (often within 24 hours) compress decision windows and boost buyer leverage. Loyalty is fragile absent clear service differentiation.

SMEs and corporates via RFPs

Larger SMEs and corporates run competitive RFPs for lending, transaction banking and markets, shrinking NABs pricing power as bundled pricing and relationship limits cap margins. Sophisticated treasury teams routinely negotiate covenants and fees, leveraging market comparators. Modular platforms and APIs, reinforced by the 2024 expansion of Australias Consumer Data Right for banking, make switching and onboarding faster and cheaper.

Multi-banking and low switching costs

Customers increasingly multi-bank; NAB serves over 7 million customers (2024), and Open Banking via Australia's CDR exceeded 4 million consents by 2024, lowering switching friction. Buyers unbundle products, choosing best-in-class fintechs for payments, lending and wealth. Retention now hinges on deep ecosystem integration and data-driven personalization to raise switching costs despite low transactional barriers.

- Multi-banking prevalence — >7M NAB customers (2024)

- Open Banking impact — CDR >4M consents (2024)

- Unbundling — product-by-product buyer choice

- Retention drivers — ecosystem + personalization

Digital experience expectations

Users benchmark NAB against fintech and big-tech UX; outages or poor journeys drive churn even when NAB is competitively priced, as Australia’s big four banks hold about 80% of deposits and face intense digital comparison pressure.

- Self-service and 24/7 support are table stakes

- Superior app features can offset modest price gaps

- Digital reliability directly affects retention

Rising rates, broker dominance and CDR fuel mass switching, squeezing bank margins

Customers have high bargaining power: rate-sensitive depositors and over 7M NAB customers (2024) switch quickly as the RBA cash rate rose to ~4.35% in 2024, squeezing NIMs. Brokers handle ~66% of new home loans (MFAA 2023) and CDR consents exceeded 4M (2024), lowering switching costs. SMEs run competitive RFPs and unbundle services, forcing price and feature competition.

| Metric | 2023–24 |

|---|---|

| NAB customers | >7M |

| CDR consents | >4M |

| Broker share (home loans) | 66% |

| RBA cash rate | ≈4.35% |

| Typical cashback | up to A$3,000 |

Preview the Actual Deliverable

NAB - National Australia Bank Porter's Five Forces Analysis

This preview shows the exact NAB - National Australia Bank Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The document displayed is the final, professionally formatted file, ready for download and use the moment you buy. You’re viewing the same complete analysis that will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

NAB faces fierce rivalry from major banks and fintechs, moderate buyer power as consumers demand digital value, and manageable supplier influence but rising regulatory and substitute threats; its scale and branch network remain key advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report for actionable insights tailored to NAB.

Suppliers Bargaining Power

Wholesale funding dependence

NAB relies on domestic and offshore wholesale markets for roughly 27% of its funding, supplying term funding beyond deposits. Large institutional investors can demand higher spreads in volatile conditions, lifting funding costs as seen in 2023–24 spread widenings. Central bank facilities (RBA/ESF) can temper spikes but are conditional and temporary. Diversification across tenors and currencies mitigates risk, though market liquidity concentration remains a leverage point.

Core tech and cloud vendors

NAB depends on a concentrated set of core banking, cloud and cybersecurity vendors for stability and scalability, creating supplier pricing power and contractual leverage. Hyperscalers AWS and Microsoft Azure held roughly 54% combined cloud market share in 2024 (AWS ~31%, Azure ~23%), amplifying switching complexity and lock-in from long implementation cycles. Strategic partnerships can trade price concessions for faster innovation and greater resilience.

Payment networks and rails

Card schemes (Visa/Mastercard, ~80% global card volume) and domestic rails like NPP and clearing systems are essential inputs for NAB, with scheme fee structures and rule changes directly affecting unit economics and merchant margins. Limited credible alternatives to these networks heighten supplier influence, though NAB’s seats in industry governance and scheme boards partially mitigate fee/rule pressure.

Specialist talent and contractors

Specialist risk, data, engineering and compliance talent markets are tight in Australia and New Zealand, giving suppliers leverage as wage inflation and retention premiums rise; Australia wage price index grew about 3.7% year to June 2024 and New Zealand WPI ~3.4% in Q2 2024. Outsourcing and nearshoring ease supply but add coordination and control risk, while automation and AI can gradually reduce dependency and unit labour costs.

- WPI: AUS 3.7% (y/y Jun 2024)

- NZ WPI: ~3.4% (Q2 2024)

- High retention premiums = supplier leverage

- Outsourcing helps but adds coordination risk

- Automation = medium-term dependency reduction

Data, analytics, and credit bureaus

Credit bureaus (Equifax, Experian, Illion), market data and analytics platforms underpin underwriting and monitoring for banks including NAB; proprietary scoring and unique datasets increase supplier leverage by differentiating risk models. Open Banking/Consumer Data Right rollout (2019–2020) broadened sources but integration and compliance costs remain material. Multi-sourcing reduces concentration risk yet curbs volume discounts and bargaining power.

- Three major bureaus: Equifax, Experian, Illion

- Open Banking (CDR) rollout 2019–2020 expanded data access

- Proprietary scores raise supplier leverage; multi-sourcing trades scale for resilience

Moderate supplier power: 27% wholesale funding, ~54% hyperscaler share, ~80% card volume

NAB faces moderate supplier power: 27% wholesale funding dependence raises sensitivity to market spreads; hyperscaler concentration (AWS ~31%, Azure ~23% = ~54% combined in 2024) and card schemes (~80% global volume) create switching costs; tight tech/compliance talent (AUS WPI 3.7% y/y Jun 2024, NZ WPI ~3.4% Q2 2024) increases wage pressure, while multi‑sourcing and central bank backstops limit extremes.

| Supplier | Metric | 2024 |

|---|---|---|

| Wholesale funding | Share of funding | 27% |

| Cloud hyperscalers | AWS+Azure | ~54% (AWS31/AZ23) |

| Card schemes | Global volume | ~80% |

| Wage pressure | WPI Australia/NZ | 3.7% / 3.4% |

| Credit bureaus | Major providers | Equifax, Experian, Illion |

What is included in the product

Tailored Porter's Five Forces analysis for NAB - National Australia Bank, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats to its profitability and strategic positioning.

A clear, one-sheet Porter's Five Forces summary for NAB—instantly highlights competitive pressures across rivals, suppliers, customers, new entrants and substitutes to speed strategic decisions and reduce analysis time.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can switch rapidly as the RBA cash rate rose to about 4.35% in 2024, squeezing net interest margins and forcing NAB to match higher term and bonus saver rates. Real-time onboarding and comparison sites increase price transparency, shortening switching cycles and elevating acquisition churn. Incentive cycles and term promotions raise short-term acquisition costs, while product innovation (features, digital tools) can partly shift competition away from pure rate.

Mortgage customers with options

Australians and New Zealanders refinance often, with the broker channel handling about 66% of new home loans (MFAA 2023), increasing switching. Cashback offers—commonly up to A$3,000 in 2023–24—and headline rate discounts drive price-based competition. Faster digital conditional approvals (often within 24 hours) compress decision windows and boost buyer leverage. Loyalty is fragile absent clear service differentiation.

SMEs and corporates via RFPs

Larger SMEs and corporates run competitive RFPs for lending, transaction banking and markets, shrinking NABs pricing power as bundled pricing and relationship limits cap margins. Sophisticated treasury teams routinely negotiate covenants and fees, leveraging market comparators. Modular platforms and APIs, reinforced by the 2024 expansion of Australias Consumer Data Right for banking, make switching and onboarding faster and cheaper.

Multi-banking and low switching costs

Customers increasingly multi-bank; NAB serves over 7 million customers (2024), and Open Banking via Australia's CDR exceeded 4 million consents by 2024, lowering switching friction. Buyers unbundle products, choosing best-in-class fintechs for payments, lending and wealth. Retention now hinges on deep ecosystem integration and data-driven personalization to raise switching costs despite low transactional barriers.

- Multi-banking prevalence — >7M NAB customers (2024)

- Open Banking impact — CDR >4M consents (2024)

- Unbundling — product-by-product buyer choice

- Retention drivers — ecosystem + personalization

Digital experience expectations

Users benchmark NAB against fintech and big-tech UX; outages or poor journeys drive churn even when NAB is competitively priced, as Australia’s big four banks hold about 80% of deposits and face intense digital comparison pressure.

- Self-service and 24/7 support are table stakes

- Superior app features can offset modest price gaps

- Digital reliability directly affects retention

Rising rates, broker dominance and CDR fuel mass switching, squeezing bank margins

Customers have high bargaining power: rate-sensitive depositors and over 7M NAB customers (2024) switch quickly as the RBA cash rate rose to ~4.35% in 2024, squeezing NIMs. Brokers handle ~66% of new home loans (MFAA 2023) and CDR consents exceeded 4M (2024), lowering switching costs. SMEs run competitive RFPs and unbundle services, forcing price and feature competition.

| Metric | 2023–24 |

|---|---|

| NAB customers | >7M |

| CDR consents | >4M |

| Broker share (home loans) | 66% |

| RBA cash rate | ≈4.35% |

| Typical cashback | up to A$3,000 |

Preview the Actual Deliverable

NAB - National Australia Bank Porter's Five Forces Analysis

This preview shows the exact NAB - National Australia Bank Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The document displayed is the final, professionally formatted file, ready for download and use the moment you buy. You’re viewing the same complete analysis that will be available to you instantly after payment.