Nanto Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and evolving tech trends are shaping Nanto Bank’s strategic outlook in our concise PESTLE snapshot. This analysis highlights regulatory risks, market opportunities, and social drivers affecting profitability. Ideal for investors and strategists—buy the full PESTLE to access the complete, actionable breakdown instantly.

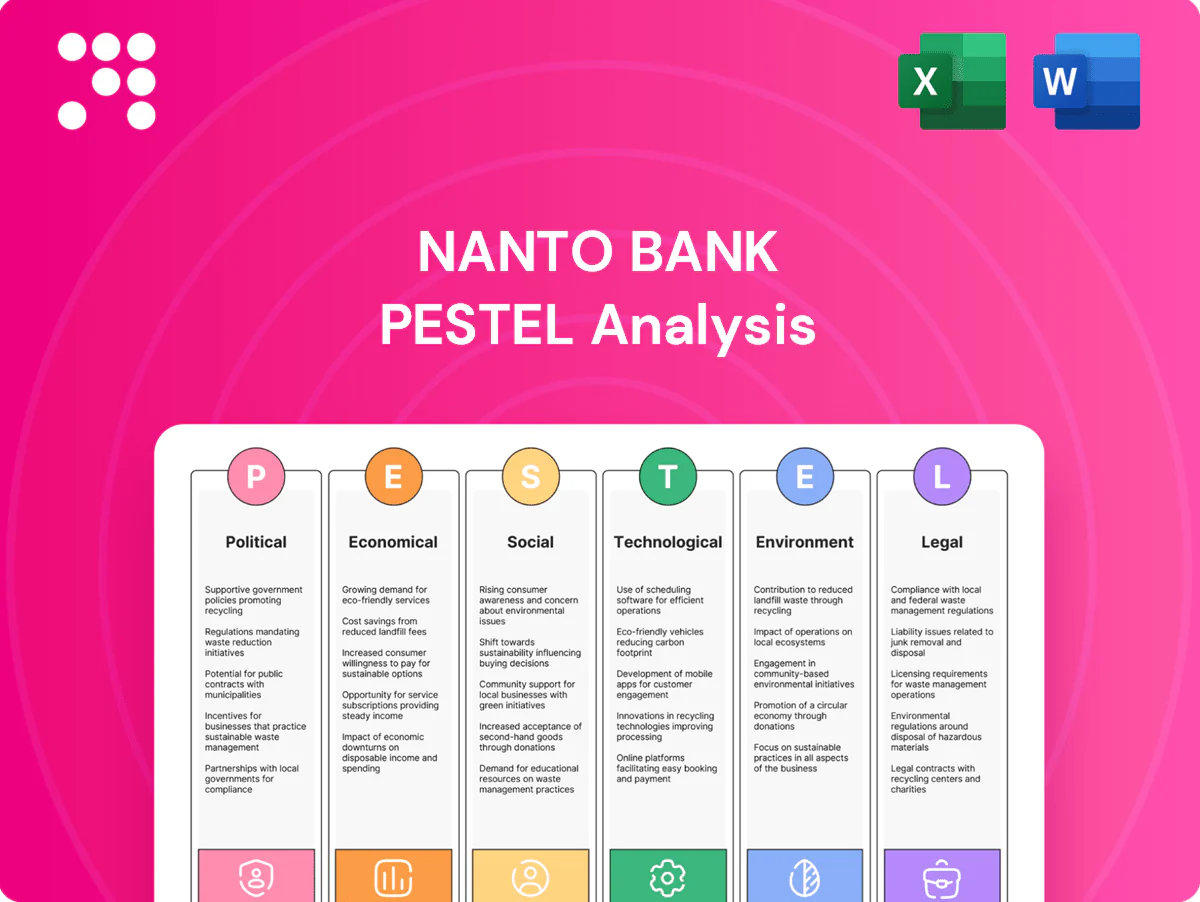

Political factors

BOJ policy shifts

BOJ's exit from negative rates in July 2023 and evolving yield-curve guidance pushed 10-year JGB yields to an average near 0.6% in 2024, raising wholesale funding costs and pressuring loan pricing. A steeper curve can expand net interest margins but intensifies deposit competition and cost of retail funding. Nanto Bank must tighten asset-liability management, increase hedging and run scenario planning across multiple rate paths.

Regional revitalization agendas

National and prefectural revitalization programs—targeting SMEs, tourism, and infrastructure—drive loan demand in Nara, a prefecture of about 1.3 million residents. Subsidies and public credit guarantees lower community-lending risk and improve Nanto Bank’s underwriting capacity. Aligning loan products with prefectural priorities opens partnerships with local governments and developers, reinforcing regional banks’ politically favored role.

Geopolitical currency pressures

External rate differentials and geopolitical tensions have driven yen volatility, with USD/JPY trading roughly in the 150–160 range across 2024–mid‑2025, raising hedging premia and stressing portfolios. FX swings are altering client export/import financing demand as working capital and letter‑of‑credit needs shift. Policy interventions remain possible and can be sudden and material. Prudent FX risk governance is therefore essential.

Public finance and municipal ties

Public finance and municipal ties drive Nanto Bank’s local government deposit flows and project financing through FY2024 budget cycles; changes in intergovernmental transfers have reduced liquidity visibility for regional banks, while deep public-sector relationships sustain predictable fee income and mandate higher oversight when handling public funds.

- Local deposits tied to annual budget cycles

- Intergovernmental transfers affect liquidity and pipeline

- Public-sector ties = stable fee income

- Heightened oversight for public money handling

Digital yen and policy pilots

Potential CBDC experiments, including Bank for International Settlements data showing over 100 jurisdictions exploring CBDCs by 2024, could materially reshape payments and deposit behaviors; pilots may shift liquidity from traditional deposit accounts into digital wallets. Early engagement lets Nanto Bank influence design, capture fee pools and ensure service readiness, while policy-driven standards will likely alter KYC and settlement rails. Operational readiness lowers risk of settlement disruptions and compliance costs during rollouts.

- BIS: 100+ jurisdictions exploring CBDCs (2024)

- Early pilot participation = influence over technical/standards stack

- Policy shifts expected in KYC, AML, settlement rails

- Operational readiness reduces disruption and compliance expense

BOJ exit, JGB ~0.6% and USD/JPY 150-160 tighten regional bank margins

BOJ exit from negative rates (10y JGB ~0.6% in 2024) raised wholesale funding costs and deposit competition, pressing Nanto Bank’s margins. Prefectural revitalization in Nara (pop ~1.3M) boosts SME and infrastructure lending with public guarantees. FX volatility (USD/JPY ~150–160 in 2024–mid‑2025) and CBDC exploration (BIS: 100+ jurisdictions by 2024) require stronger ALM, hedging and digital readiness.

| Indicator | Value |

|---|---|

| 10y JGB (2024) | ~0.6% |

| USD/JPY (2024–mid‑2025) | 150–160 |

| Nara population | ~1.3M |

| BIS CBDC count (2024) | 100+ |

What is included in the product

Provides a concise PESTLE review of how political, economic, social, technological, environmental and legal forces shape Nanto Bank’s operating risks and opportunities, with data-driven, region-specific insights and forward-looking implications tailored for executives, investors and strategists.

Provides a clean, summarized PESTLE of Nanto Bank, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Slow growth and inflation mix

Japan’s modest real GDP growth of about 1.6% in 2024 combined with CPI near 3.2% has mixed effects on real borrower incomes and credit demand. Rising wages—Shunto average base pay gains around 3.6% in 2024—support consumption but squeeze SME margins. Pricing power varies across Nara’s service and manufacturing firms, so credit underwriting must reflect clear sector dispersion.

SME health and capex cycles

Regional SMEs—which make up 99.7% of Japanese firms—drive Nanto Bank’s loan book dynamics, with credit demand concentrated in tourism, retail and light manufacturing hubs; Japan saw 31.88 million inbound tourists in 2023, affecting local cashflows. Supply‑chain reconfiguration and automation trends are increasing equipment finance and leasing needs, while tailored advisory services have proven effective at lifting cross‑sell and client retention.

Interest margin compression risk

Competition and rising deposit betas may cap NIM expansion for Nanto Bank despite a higher rate backdrop; regional deposit betas averaged near 40% in 2024, limiting pass-through. Securities portfolio valuations are sensitive to rate moves as 10‑year JGB yields climbed toward 0.7% in 2024, creating unrealized mark-to-market risk. Repricing gaps demand disciplined duration management across asset and liability books. Fee income diversification—now roughly 20% of many regional banks’ revenues in 2024—helps mitigate margin volatility.

Demographics and deposit base

Aging households (65+ = 29.1% of Japan’s population in 2024) hold higher deposit ratios and buoy regional balances, but drawdowns rise on retirement, pressuring liquidity; Japan household financial assets were about ¥2,030 trillion at end‑2023, highlighting stored liquidity that may convert to consumption or withdrawals. Younger outflow to urban centers shrinks local loan and deposit growth, so product design must balance steady income with ready liquidity while wealth management can stabilize deposits.

Tourism and local commerce

Nara’s heritage tourism drives pronounced seasonal cash flow for SMEs; Nara Prefecture attracted about 10.5 million visitors in 2019, concentrating revenue in spring and autumn. Currency-driven inbound cycles tied to JPY swings and Japan’s ~32 million inbound tourists in 2023 create measurable card and merchant acquiring volatility. Targeted working-capital, POS solutions and transaction-data-led underwriting can smooth seasonality and optimize lending limits.

- Seasonal revenue spikes: Nara 2019 ~10.5M visitors

- Inbound driver: Japan ~32M tourists (2023)

- Product response: working capital, POS

- Data use: dynamic lending limits

BOJ exit, JGB ~0.6% and USD/JPY 150-160 tighten regional bank margins

Japan GDP ~1.6% (2024) and CPI ~3.2% slow but inflationary; Shunto wage gains ~3.6% support consumption but squeeze SME margins. Regional SMEs (99.7% of firms) drive loans; tourism (Nara 2019 10.5M; Japan ~32M tourists 2023) fuels seasonality. Deposit beta ~40% and 10y JGB ~0.7% constrain NIM; household assets ~¥2,030tn (end‑2023).

| Metric | Value |

|---|---|

| GDP (2024) | 1.6% |

| CPI (2024) | 3.2% |

| Shunto wage gain (2024) | 3.6% |

| Household assets (end‑2023) | ¥2,030tn |

| 10y JGB (2024) | ~0.7% |

| Deposit beta | ~40% |

Preview Before You Purchase

Nanto Bank PESTLE Analysis

The Nanto Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment for Nanto Bank with no placeholders. The layout, content, and structure visible are exactly what you’ll download immediately after buying.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and evolving tech trends are shaping Nanto Bank’s strategic outlook in our concise PESTLE snapshot. This analysis highlights regulatory risks, market opportunities, and social drivers affecting profitability. Ideal for investors and strategists—buy the full PESTLE to access the complete, actionable breakdown instantly.

Political factors

BOJ policy shifts

BOJ's exit from negative rates in July 2023 and evolving yield-curve guidance pushed 10-year JGB yields to an average near 0.6% in 2024, raising wholesale funding costs and pressuring loan pricing. A steeper curve can expand net interest margins but intensifies deposit competition and cost of retail funding. Nanto Bank must tighten asset-liability management, increase hedging and run scenario planning across multiple rate paths.

Regional revitalization agendas

National and prefectural revitalization programs—targeting SMEs, tourism, and infrastructure—drive loan demand in Nara, a prefecture of about 1.3 million residents. Subsidies and public credit guarantees lower community-lending risk and improve Nanto Bank’s underwriting capacity. Aligning loan products with prefectural priorities opens partnerships with local governments and developers, reinforcing regional banks’ politically favored role.

Geopolitical currency pressures

External rate differentials and geopolitical tensions have driven yen volatility, with USD/JPY trading roughly in the 150–160 range across 2024–mid‑2025, raising hedging premia and stressing portfolios. FX swings are altering client export/import financing demand as working capital and letter‑of‑credit needs shift. Policy interventions remain possible and can be sudden and material. Prudent FX risk governance is therefore essential.

Public finance and municipal ties

Public finance and municipal ties drive Nanto Bank’s local government deposit flows and project financing through FY2024 budget cycles; changes in intergovernmental transfers have reduced liquidity visibility for regional banks, while deep public-sector relationships sustain predictable fee income and mandate higher oversight when handling public funds.

- Local deposits tied to annual budget cycles

- Intergovernmental transfers affect liquidity and pipeline

- Public-sector ties = stable fee income

- Heightened oversight for public money handling

Digital yen and policy pilots

Potential CBDC experiments, including Bank for International Settlements data showing over 100 jurisdictions exploring CBDCs by 2024, could materially reshape payments and deposit behaviors; pilots may shift liquidity from traditional deposit accounts into digital wallets. Early engagement lets Nanto Bank influence design, capture fee pools and ensure service readiness, while policy-driven standards will likely alter KYC and settlement rails. Operational readiness lowers risk of settlement disruptions and compliance costs during rollouts.

- BIS: 100+ jurisdictions exploring CBDCs (2024)

- Early pilot participation = influence over technical/standards stack

- Policy shifts expected in KYC, AML, settlement rails

- Operational readiness reduces disruption and compliance expense

BOJ exit, JGB ~0.6% and USD/JPY 150-160 tighten regional bank margins

BOJ exit from negative rates (10y JGB ~0.6% in 2024) raised wholesale funding costs and deposit competition, pressing Nanto Bank’s margins. Prefectural revitalization in Nara (pop ~1.3M) boosts SME and infrastructure lending with public guarantees. FX volatility (USD/JPY ~150–160 in 2024–mid‑2025) and CBDC exploration (BIS: 100+ jurisdictions by 2024) require stronger ALM, hedging and digital readiness.

| Indicator | Value |

|---|---|

| 10y JGB (2024) | ~0.6% |

| USD/JPY (2024–mid‑2025) | 150–160 |

| Nara population | ~1.3M |

| BIS CBDC count (2024) | 100+ |

What is included in the product

Provides a concise PESTLE review of how political, economic, social, technological, environmental and legal forces shape Nanto Bank’s operating risks and opportunities, with data-driven, region-specific insights and forward-looking implications tailored for executives, investors and strategists.

Provides a clean, summarized PESTLE of Nanto Bank, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Slow growth and inflation mix

Japan’s modest real GDP growth of about 1.6% in 2024 combined with CPI near 3.2% has mixed effects on real borrower incomes and credit demand. Rising wages—Shunto average base pay gains around 3.6% in 2024—support consumption but squeeze SME margins. Pricing power varies across Nara’s service and manufacturing firms, so credit underwriting must reflect clear sector dispersion.

SME health and capex cycles

Regional SMEs—which make up 99.7% of Japanese firms—drive Nanto Bank’s loan book dynamics, with credit demand concentrated in tourism, retail and light manufacturing hubs; Japan saw 31.88 million inbound tourists in 2023, affecting local cashflows. Supply‑chain reconfiguration and automation trends are increasing equipment finance and leasing needs, while tailored advisory services have proven effective at lifting cross‑sell and client retention.

Interest margin compression risk

Competition and rising deposit betas may cap NIM expansion for Nanto Bank despite a higher rate backdrop; regional deposit betas averaged near 40% in 2024, limiting pass-through. Securities portfolio valuations are sensitive to rate moves as 10‑year JGB yields climbed toward 0.7% in 2024, creating unrealized mark-to-market risk. Repricing gaps demand disciplined duration management across asset and liability books. Fee income diversification—now roughly 20% of many regional banks’ revenues in 2024—helps mitigate margin volatility.

Demographics and deposit base

Aging households (65+ = 29.1% of Japan’s population in 2024) hold higher deposit ratios and buoy regional balances, but drawdowns rise on retirement, pressuring liquidity; Japan household financial assets were about ¥2,030 trillion at end‑2023, highlighting stored liquidity that may convert to consumption or withdrawals. Younger outflow to urban centers shrinks local loan and deposit growth, so product design must balance steady income with ready liquidity while wealth management can stabilize deposits.

Tourism and local commerce

Nara’s heritage tourism drives pronounced seasonal cash flow for SMEs; Nara Prefecture attracted about 10.5 million visitors in 2019, concentrating revenue in spring and autumn. Currency-driven inbound cycles tied to JPY swings and Japan’s ~32 million inbound tourists in 2023 create measurable card and merchant acquiring volatility. Targeted working-capital, POS solutions and transaction-data-led underwriting can smooth seasonality and optimize lending limits.

- Seasonal revenue spikes: Nara 2019 ~10.5M visitors

- Inbound driver: Japan ~32M tourists (2023)

- Product response: working capital, POS

- Data use: dynamic lending limits

BOJ exit, JGB ~0.6% and USD/JPY 150-160 tighten regional bank margins

Japan GDP ~1.6% (2024) and CPI ~3.2% slow but inflationary; Shunto wage gains ~3.6% support consumption but squeeze SME margins. Regional SMEs (99.7% of firms) drive loans; tourism (Nara 2019 10.5M; Japan ~32M tourists 2023) fuels seasonality. Deposit beta ~40% and 10y JGB ~0.7% constrain NIM; household assets ~¥2,030tn (end‑2023).

| Metric | Value |

|---|---|

| GDP (2024) | 1.6% |

| CPI (2024) | 3.2% |

| Shunto wage gain (2024) | 3.6% |

| Household assets (end‑2023) | ¥2,030tn |

| 10y JGB (2024) | ~0.7% |

| Deposit beta | ~40% |

Preview Before You Purchase

Nanto Bank PESTLE Analysis

The Nanto Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment for Nanto Bank with no placeholders. The layout, content, and structure visible are exactly what you’ll download immediately after buying.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and evolving tech trends are shaping Nanto Bank’s strategic outlook in our concise PESTLE snapshot. This analysis highlights regulatory risks, market opportunities, and social drivers affecting profitability. Ideal for investors and strategists—buy the full PESTLE to access the complete, actionable breakdown instantly.

Political factors

BOJ policy shifts

BOJ's exit from negative rates in July 2023 and evolving yield-curve guidance pushed 10-year JGB yields to an average near 0.6% in 2024, raising wholesale funding costs and pressuring loan pricing. A steeper curve can expand net interest margins but intensifies deposit competition and cost of retail funding. Nanto Bank must tighten asset-liability management, increase hedging and run scenario planning across multiple rate paths.

Regional revitalization agendas

National and prefectural revitalization programs—targeting SMEs, tourism, and infrastructure—drive loan demand in Nara, a prefecture of about 1.3 million residents. Subsidies and public credit guarantees lower community-lending risk and improve Nanto Bank’s underwriting capacity. Aligning loan products with prefectural priorities opens partnerships with local governments and developers, reinforcing regional banks’ politically favored role.

Geopolitical currency pressures

External rate differentials and geopolitical tensions have driven yen volatility, with USD/JPY trading roughly in the 150–160 range across 2024–mid‑2025, raising hedging premia and stressing portfolios. FX swings are altering client export/import financing demand as working capital and letter‑of‑credit needs shift. Policy interventions remain possible and can be sudden and material. Prudent FX risk governance is therefore essential.

Public finance and municipal ties

Public finance and municipal ties drive Nanto Bank’s local government deposit flows and project financing through FY2024 budget cycles; changes in intergovernmental transfers have reduced liquidity visibility for regional banks, while deep public-sector relationships sustain predictable fee income and mandate higher oversight when handling public funds.

- Local deposits tied to annual budget cycles

- Intergovernmental transfers affect liquidity and pipeline

- Public-sector ties = stable fee income

- Heightened oversight for public money handling

Digital yen and policy pilots

Potential CBDC experiments, including Bank for International Settlements data showing over 100 jurisdictions exploring CBDCs by 2024, could materially reshape payments and deposit behaviors; pilots may shift liquidity from traditional deposit accounts into digital wallets. Early engagement lets Nanto Bank influence design, capture fee pools and ensure service readiness, while policy-driven standards will likely alter KYC and settlement rails. Operational readiness lowers risk of settlement disruptions and compliance costs during rollouts.

- BIS: 100+ jurisdictions exploring CBDCs (2024)

- Early pilot participation = influence over technical/standards stack

- Policy shifts expected in KYC, AML, settlement rails

- Operational readiness reduces disruption and compliance expense

BOJ exit, JGB ~0.6% and USD/JPY 150-160 tighten regional bank margins

BOJ exit from negative rates (10y JGB ~0.6% in 2024) raised wholesale funding costs and deposit competition, pressing Nanto Bank’s margins. Prefectural revitalization in Nara (pop ~1.3M) boosts SME and infrastructure lending with public guarantees. FX volatility (USD/JPY ~150–160 in 2024–mid‑2025) and CBDC exploration (BIS: 100+ jurisdictions by 2024) require stronger ALM, hedging and digital readiness.

| Indicator | Value |

|---|---|

| 10y JGB (2024) | ~0.6% |

| USD/JPY (2024–mid‑2025) | 150–160 |

| Nara population | ~1.3M |

| BIS CBDC count (2024) | 100+ |

What is included in the product

Provides a concise PESTLE review of how political, economic, social, technological, environmental and legal forces shape Nanto Bank’s operating risks and opportunities, with data-driven, region-specific insights and forward-looking implications tailored for executives, investors and strategists.

Provides a clean, summarized PESTLE of Nanto Bank, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Slow growth and inflation mix

Japan’s modest real GDP growth of about 1.6% in 2024 combined with CPI near 3.2% has mixed effects on real borrower incomes and credit demand. Rising wages—Shunto average base pay gains around 3.6% in 2024—support consumption but squeeze SME margins. Pricing power varies across Nara’s service and manufacturing firms, so credit underwriting must reflect clear sector dispersion.

SME health and capex cycles

Regional SMEs—which make up 99.7% of Japanese firms—drive Nanto Bank’s loan book dynamics, with credit demand concentrated in tourism, retail and light manufacturing hubs; Japan saw 31.88 million inbound tourists in 2023, affecting local cashflows. Supply‑chain reconfiguration and automation trends are increasing equipment finance and leasing needs, while tailored advisory services have proven effective at lifting cross‑sell and client retention.

Interest margin compression risk

Competition and rising deposit betas may cap NIM expansion for Nanto Bank despite a higher rate backdrop; regional deposit betas averaged near 40% in 2024, limiting pass-through. Securities portfolio valuations are sensitive to rate moves as 10‑year JGB yields climbed toward 0.7% in 2024, creating unrealized mark-to-market risk. Repricing gaps demand disciplined duration management across asset and liability books. Fee income diversification—now roughly 20% of many regional banks’ revenues in 2024—helps mitigate margin volatility.

Demographics and deposit base

Aging households (65+ = 29.1% of Japan’s population in 2024) hold higher deposit ratios and buoy regional balances, but drawdowns rise on retirement, pressuring liquidity; Japan household financial assets were about ¥2,030 trillion at end‑2023, highlighting stored liquidity that may convert to consumption or withdrawals. Younger outflow to urban centers shrinks local loan and deposit growth, so product design must balance steady income with ready liquidity while wealth management can stabilize deposits.

Tourism and local commerce

Nara’s heritage tourism drives pronounced seasonal cash flow for SMEs; Nara Prefecture attracted about 10.5 million visitors in 2019, concentrating revenue in spring and autumn. Currency-driven inbound cycles tied to JPY swings and Japan’s ~32 million inbound tourists in 2023 create measurable card and merchant acquiring volatility. Targeted working-capital, POS solutions and transaction-data-led underwriting can smooth seasonality and optimize lending limits.

- Seasonal revenue spikes: Nara 2019 ~10.5M visitors

- Inbound driver: Japan ~32M tourists (2023)

- Product response: working capital, POS

- Data use: dynamic lending limits

BOJ exit, JGB ~0.6% and USD/JPY 150-160 tighten regional bank margins

Japan GDP ~1.6% (2024) and CPI ~3.2% slow but inflationary; Shunto wage gains ~3.6% support consumption but squeeze SME margins. Regional SMEs (99.7% of firms) drive loans; tourism (Nara 2019 10.5M; Japan ~32M tourists 2023) fuels seasonality. Deposit beta ~40% and 10y JGB ~0.7% constrain NIM; household assets ~¥2,030tn (end‑2023).

| Metric | Value |

|---|---|

| GDP (2024) | 1.6% |

| CPI (2024) | 3.2% |

| Shunto wage gain (2024) | 3.6% |

| Household assets (end‑2023) | ¥2,030tn |

| 10y JGB (2024) | ~0.7% |

| Deposit beta | ~40% |

Preview Before You Purchase

Nanto Bank PESTLE Analysis

The Nanto Bank PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment for Nanto Bank with no placeholders. The layout, content, and structure visible are exactly what you’ll download immediately after buying.