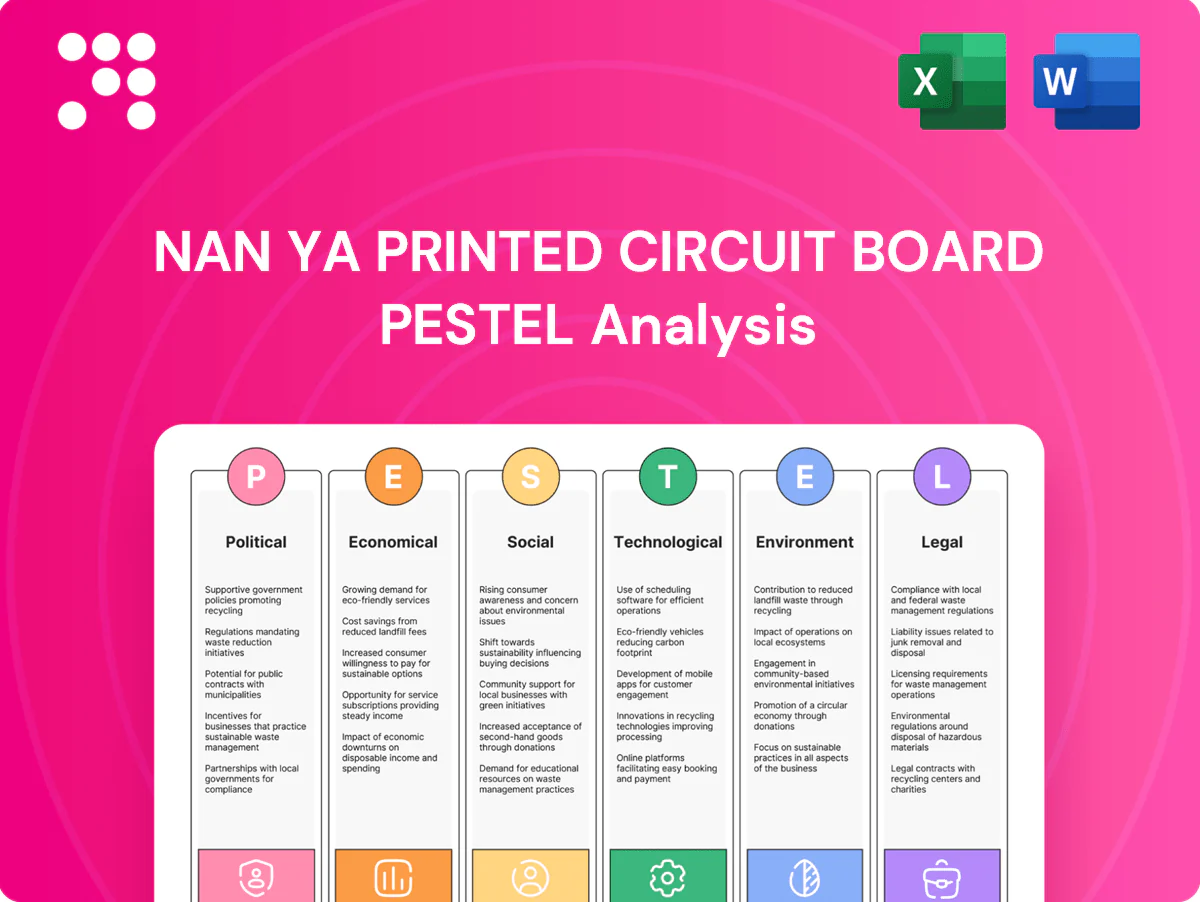

Nan Ya Printed Circuit Board PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, supply-chain economics, technological advances and environmental rules are shaping Nan Ya Printed Circuit Board’s outlook in our concise PESTLE snapshot. This analysis highlights key risks and opportunities to inform your strategy and investment case. Purchase the full PESTLE for the complete, actionable breakdown and downloadable resources.

Political factors

Cross-strait geopolitical risk

Heightened Taiwan–China tensions can disrupt logistics, capital flows and customer procurement, with Taiwan supplying over 60% of advanced PCB capacity in 2024, raising vulnerability for Nan Ya Printed Circuit Board. Contingency planning — dual‑site production and diversified shipping routes — is critical as insurance and risk premiums have risen (war‑risk and marine cover up to ~25% in 2023–24), squeezing margins. Customers increasingly demand supply‑assurance clauses and inventory buffers to mitigate disruption risk.

Trade policy and tariffs

US export controls on advanced tech since 2022 and lingering Section 301 tariffs (up to 25%) are shifting PCB sourcing away from China, forcing OEMs to re‑route orders; sudden tariff changes can reprice contracts mid‑cycle. Preferential treatment and supply‑chain incentives for Taiwan-origin goods via CHIPS-era policies help Nan Ya capture reallocating orders, but complex rules of origin and compliance add measurable administrative and duty risk. Long‑term contracts therefore require explicit tariff pass‑through mechanisms.

Industrial policy and incentives

Taiwan, the US and ASEAN offer subsidies for advanced manufacturing and green upgrades—US CHIPS Act provides $52.7 billion for semiconductor incentives and the Inflation Reduction Act earmarks roughly $369 billion for clean energy—capturing automation and energy-efficiency grants can lower unit costs materially. Conditionality on local content and hiring quotas often redirects footprint choices, while increased reporting and compliance raise administrative burden and operating costs.

Export controls on advanced tech

Export controls on high-end substrates and materials from the US, EU and Japan are tightening, pushing Nan Ya PCB to adjust its product mix toward lower-risk items and licensed technologies. Enhanced customer/end-use screening typically adds 1–4 weeks to sales cycles and increases working-capital needs. Missteps can lead to civil fines (up to about 307,922 USD) or criminal penalties and shipment seizures. Strong compliance systems now reduce disruption and serve as a competitive differentiator.

- Product-mix shift: higher compliance, lower-risk SKUs

- Sales-cycle impact: +1–4 weeks screening delays

- Risk: civil fines (~307,922 USD), criminal exposure, seizures

Energy and infrastructure governance

Policy on electricity pricing and grid reliability directly affects PCB plant uptime and operating costs; Taiwan targets 20% renewable electricity by 2025, shifting procurement incentives that can lower exposure to emerging carbon measures. Power rationing or outages force costly rescheduling, yield losses and supply-chain delays. Active engagement with local authorities speeds expansion permits and stable utilities access.

- Grid reliability: impacts uptime

- 20% renewables by 2025: procurement incentives

- Rationing: forces rescheduling, production loss

- Local engagement: eases permits and utilities access

Supply risk: Taiwan at ~60% PCB share, insurance rises to ~25%

Heightened Taiwan–China tensions (Taiwan ~60% of advanced PCB capacity in 2024) raise logistics and insurance costs (war‑risk marine up to ~25% in 2023–24), forcing dual‑site planning and inventory clauses. US export controls and tariffs reroute orders; screening adds 1–4 weeks and fines can reach ~307,922 USD. Subsidies (US CHIPS $52.7bn; IRA ~$369bn) and Taiwan renewables target 20% by 2025 reshape capex and site choices.

| Factor | Key metric |

|---|---|

| Taiwan PCB share (2024) | ~60% |

| War‑risk/marine insurance | up to ~25% (2023–24) |

| Export screening delay | +1–4 weeks |

| Max civil fine | ~307,922 USD |

| US subsidies | CHIPS $52.7bn |

| Clean energy funding | IRA ~$369bn; Taiwan 20% RE by 2025 |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Nan Ya Printed Circuit Board across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and region-specific examples. Designed for executives, consultants and investors, the analysis offers forward-looking insights to identify risks, opportunities and support strategic planning and funding decisions.

A concise, visually segmented PESTLE summary of Nan Ya Printed Circuit Board that streamlines external risk assessment and market positioning, making it easy to drop into presentations, share across teams, and customize with region- or product-specific notes for faster strategic decisions.

Economic factors

Electronics demand cyclicality

PCB demand tracks computing, telecom and consumer cycles, making Nan Ya's revenue volatile; the global PCB market was about USD 65 billion in 2023. Rapid growth in AI/data-center investment and rising 5G connections (approximately 1.6 billion by end-2024) can offset weak consumer-device demand. Flexible capacity and fast product-mix shifts help stabilize utilization. OEM/ODM inventory signals remain primary inputs for production planning.

Input cost volatility

Copper, laminates, chemicals and energy account for roughly 65% of Nan Ya PCB input costs and drive most COGS variance; LME copper swings and laminate supply tightness periodically spike margins. Hedging and multi‑sourcing reduce price shocks but introduce basis risk and execution costs, typically trimming realized volatility by ~25%. Long‑term vendor partnerships secure allocation in tight markets; contractual cost pass‑through preserves margins during inflationary periods.

Currency fluctuations

Revenue for Nan Ya Printed Circuit Board is often USD-linked while a portion of raw‑material and labor costs are in TWD and other local currencies, so FX swings directly affect gross margins and pricing competitiveness.

USD/TWD hovered near 31 in July 2025, and typical annual moves of 2–5% can materially shift margins for exporters.

Natural hedging by matching currency cash flows plus active hedging (forwards/options) is used to stabilize reported earnings.

Capital intensity and interest rates

Advanced multilayer and HDI lines demand sustained capex and tooling; higher policy rates in 2023–24 around 5% in major markets pushed WACC and internal hurdle rates materially higher, compressing NPV on greenfield expansions. Phased investments tied to customer LTAs reduce payback risk, while leasing and government-backed financing improve near-term cash flow.

- Capex intensity: sustained multi-year investment

- Rates impact: ~5% policy rates raised WACC

- Mitigation: phased builds + LTAs

- Cash optimization: leasing, govt-backed loans

Global supply-chain reconfiguration

China+1 strategies have shifted PCB demand toward Taiwan and Southeast Asia, shortening lead times by locating fabs near key customers; WTO data shows global goods trade fell 5.3% in 2020, highlighting vulnerability to disruptions. Shipping costs surged in 2021–22 and largely normalized by 2024, so logistics and trade lanes now strongly drive site selection while regional diversification reduces single-country exposure.

- China+1 demand shift: Taiwan, SE Asia

- Lead-time reduction via proximity

- Logistics/trade lanes shape siting

- WTO: goods trade -5.3% in 2020

- Regional diversification mitigates pandemic shocks

Supply risk: Taiwan at ~60% PCB share, insurance rises to ~25%

PCB demand tracks cyclic end markets; global PCB market ~USD 65bn (2023) while AI/data‑center capex and 5G (~1.6bn connections end‑2024) drive upside. Input costs (copper, laminates, chemicals, energy) ~65% of COGS; LME copper volatility and laminate tightness are primary margin drivers. USD/TWD ~31 (Jul 2025) so FX moves (±2–5% annually) materially affect margins; capex intensity and ~5% policy rates raise hurdle rates, favoring phased builds and LTAs.

| Metric | Value | Note |

|---|---|---|

| Global PCB market | USD 65bn (2023) | Source: industry data |

| 5G connections | ~1.6bn (end‑2024) | GSMA estimate |

| Input cost mix | ~65% of COGS | Copper/laminate/chemicals/energy |

| USD/TWD | ~31 (Jul 2025) | FX affects margins |

Preview Before You Purchase

Nan Ya Printed Circuit Board PESTLE Analysis

The Nan Ya Printed Circuit Board PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: this is the final, downloadable file.

Skip the Research. Get the Strategy.

Unlock how political shifts, supply-chain economics, technological advances and environmental rules are shaping Nan Ya Printed Circuit Board’s outlook in our concise PESTLE snapshot. This analysis highlights key risks and opportunities to inform your strategy and investment case. Purchase the full PESTLE for the complete, actionable breakdown and downloadable resources.

Political factors

Cross-strait geopolitical risk

Heightened Taiwan–China tensions can disrupt logistics, capital flows and customer procurement, with Taiwan supplying over 60% of advanced PCB capacity in 2024, raising vulnerability for Nan Ya Printed Circuit Board. Contingency planning — dual‑site production and diversified shipping routes — is critical as insurance and risk premiums have risen (war‑risk and marine cover up to ~25% in 2023–24), squeezing margins. Customers increasingly demand supply‑assurance clauses and inventory buffers to mitigate disruption risk.

Trade policy and tariffs

US export controls on advanced tech since 2022 and lingering Section 301 tariffs (up to 25%) are shifting PCB sourcing away from China, forcing OEMs to re‑route orders; sudden tariff changes can reprice contracts mid‑cycle. Preferential treatment and supply‑chain incentives for Taiwan-origin goods via CHIPS-era policies help Nan Ya capture reallocating orders, but complex rules of origin and compliance add measurable administrative and duty risk. Long‑term contracts therefore require explicit tariff pass‑through mechanisms.

Industrial policy and incentives

Taiwan, the US and ASEAN offer subsidies for advanced manufacturing and green upgrades—US CHIPS Act provides $52.7 billion for semiconductor incentives and the Inflation Reduction Act earmarks roughly $369 billion for clean energy—capturing automation and energy-efficiency grants can lower unit costs materially. Conditionality on local content and hiring quotas often redirects footprint choices, while increased reporting and compliance raise administrative burden and operating costs.

Export controls on advanced tech

Export controls on high-end substrates and materials from the US, EU and Japan are tightening, pushing Nan Ya PCB to adjust its product mix toward lower-risk items and licensed technologies. Enhanced customer/end-use screening typically adds 1–4 weeks to sales cycles and increases working-capital needs. Missteps can lead to civil fines (up to about 307,922 USD) or criminal penalties and shipment seizures. Strong compliance systems now reduce disruption and serve as a competitive differentiator.

- Product-mix shift: higher compliance, lower-risk SKUs

- Sales-cycle impact: +1–4 weeks screening delays

- Risk: civil fines (~307,922 USD), criminal exposure, seizures

Energy and infrastructure governance

Policy on electricity pricing and grid reliability directly affects PCB plant uptime and operating costs; Taiwan targets 20% renewable electricity by 2025, shifting procurement incentives that can lower exposure to emerging carbon measures. Power rationing or outages force costly rescheduling, yield losses and supply-chain delays. Active engagement with local authorities speeds expansion permits and stable utilities access.

- Grid reliability: impacts uptime

- 20% renewables by 2025: procurement incentives

- Rationing: forces rescheduling, production loss

- Local engagement: eases permits and utilities access

Supply risk: Taiwan at ~60% PCB share, insurance rises to ~25%

Heightened Taiwan–China tensions (Taiwan ~60% of advanced PCB capacity in 2024) raise logistics and insurance costs (war‑risk marine up to ~25% in 2023–24), forcing dual‑site planning and inventory clauses. US export controls and tariffs reroute orders; screening adds 1–4 weeks and fines can reach ~307,922 USD. Subsidies (US CHIPS $52.7bn; IRA ~$369bn) and Taiwan renewables target 20% by 2025 reshape capex and site choices.

| Factor | Key metric |

|---|---|

| Taiwan PCB share (2024) | ~60% |

| War‑risk/marine insurance | up to ~25% (2023–24) |

| Export screening delay | +1–4 weeks |

| Max civil fine | ~307,922 USD |

| US subsidies | CHIPS $52.7bn |

| Clean energy funding | IRA ~$369bn; Taiwan 20% RE by 2025 |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Nan Ya Printed Circuit Board across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and region-specific examples. Designed for executives, consultants and investors, the analysis offers forward-looking insights to identify risks, opportunities and support strategic planning and funding decisions.

A concise, visually segmented PESTLE summary of Nan Ya Printed Circuit Board that streamlines external risk assessment and market positioning, making it easy to drop into presentations, share across teams, and customize with region- or product-specific notes for faster strategic decisions.

Economic factors

Electronics demand cyclicality

PCB demand tracks computing, telecom and consumer cycles, making Nan Ya's revenue volatile; the global PCB market was about USD 65 billion in 2023. Rapid growth in AI/data-center investment and rising 5G connections (approximately 1.6 billion by end-2024) can offset weak consumer-device demand. Flexible capacity and fast product-mix shifts help stabilize utilization. OEM/ODM inventory signals remain primary inputs for production planning.

Input cost volatility

Copper, laminates, chemicals and energy account for roughly 65% of Nan Ya PCB input costs and drive most COGS variance; LME copper swings and laminate supply tightness periodically spike margins. Hedging and multi‑sourcing reduce price shocks but introduce basis risk and execution costs, typically trimming realized volatility by ~25%. Long‑term vendor partnerships secure allocation in tight markets; contractual cost pass‑through preserves margins during inflationary periods.

Currency fluctuations

Revenue for Nan Ya Printed Circuit Board is often USD-linked while a portion of raw‑material and labor costs are in TWD and other local currencies, so FX swings directly affect gross margins and pricing competitiveness.

USD/TWD hovered near 31 in July 2025, and typical annual moves of 2–5% can materially shift margins for exporters.

Natural hedging by matching currency cash flows plus active hedging (forwards/options) is used to stabilize reported earnings.

Capital intensity and interest rates

Advanced multilayer and HDI lines demand sustained capex and tooling; higher policy rates in 2023–24 around 5% in major markets pushed WACC and internal hurdle rates materially higher, compressing NPV on greenfield expansions. Phased investments tied to customer LTAs reduce payback risk, while leasing and government-backed financing improve near-term cash flow.

- Capex intensity: sustained multi-year investment

- Rates impact: ~5% policy rates raised WACC

- Mitigation: phased builds + LTAs

- Cash optimization: leasing, govt-backed loans

Global supply-chain reconfiguration

China+1 strategies have shifted PCB demand toward Taiwan and Southeast Asia, shortening lead times by locating fabs near key customers; WTO data shows global goods trade fell 5.3% in 2020, highlighting vulnerability to disruptions. Shipping costs surged in 2021–22 and largely normalized by 2024, so logistics and trade lanes now strongly drive site selection while regional diversification reduces single-country exposure.

- China+1 demand shift: Taiwan, SE Asia

- Lead-time reduction via proximity

- Logistics/trade lanes shape siting

- WTO: goods trade -5.3% in 2020

- Regional diversification mitigates pandemic shocks

Supply risk: Taiwan at ~60% PCB share, insurance rises to ~25%

PCB demand tracks cyclic end markets; global PCB market ~USD 65bn (2023) while AI/data‑center capex and 5G (~1.6bn connections end‑2024) drive upside. Input costs (copper, laminates, chemicals, energy) ~65% of COGS; LME copper volatility and laminate tightness are primary margin drivers. USD/TWD ~31 (Jul 2025) so FX moves (±2–5% annually) materially affect margins; capex intensity and ~5% policy rates raise hurdle rates, favoring phased builds and LTAs.

| Metric | Value | Note |

|---|---|---|

| Global PCB market | USD 65bn (2023) | Source: industry data |

| 5G connections | ~1.6bn (end‑2024) | GSMA estimate |

| Input cost mix | ~65% of COGS | Copper/laminate/chemicals/energy |

| USD/TWD | ~31 (Jul 2025) | FX affects margins |

Preview Before You Purchase

Nan Ya Printed Circuit Board PESTLE Analysis

The Nan Ya Printed Circuit Board PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: this is the final, downloadable file.

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, supply-chain economics, technological advances and environmental rules are shaping Nan Ya Printed Circuit Board’s outlook in our concise PESTLE snapshot. This analysis highlights key risks and opportunities to inform your strategy and investment case. Purchase the full PESTLE for the complete, actionable breakdown and downloadable resources.

Political factors

Cross-strait geopolitical risk

Heightened Taiwan–China tensions can disrupt logistics, capital flows and customer procurement, with Taiwan supplying over 60% of advanced PCB capacity in 2024, raising vulnerability for Nan Ya Printed Circuit Board. Contingency planning — dual‑site production and diversified shipping routes — is critical as insurance and risk premiums have risen (war‑risk and marine cover up to ~25% in 2023–24), squeezing margins. Customers increasingly demand supply‑assurance clauses and inventory buffers to mitigate disruption risk.

Trade policy and tariffs

US export controls on advanced tech since 2022 and lingering Section 301 tariffs (up to 25%) are shifting PCB sourcing away from China, forcing OEMs to re‑route orders; sudden tariff changes can reprice contracts mid‑cycle. Preferential treatment and supply‑chain incentives for Taiwan-origin goods via CHIPS-era policies help Nan Ya capture reallocating orders, but complex rules of origin and compliance add measurable administrative and duty risk. Long‑term contracts therefore require explicit tariff pass‑through mechanisms.

Industrial policy and incentives

Taiwan, the US and ASEAN offer subsidies for advanced manufacturing and green upgrades—US CHIPS Act provides $52.7 billion for semiconductor incentives and the Inflation Reduction Act earmarks roughly $369 billion for clean energy—capturing automation and energy-efficiency grants can lower unit costs materially. Conditionality on local content and hiring quotas often redirects footprint choices, while increased reporting and compliance raise administrative burden and operating costs.

Export controls on advanced tech

Export controls on high-end substrates and materials from the US, EU and Japan are tightening, pushing Nan Ya PCB to adjust its product mix toward lower-risk items and licensed technologies. Enhanced customer/end-use screening typically adds 1–4 weeks to sales cycles and increases working-capital needs. Missteps can lead to civil fines (up to about 307,922 USD) or criminal penalties and shipment seizures. Strong compliance systems now reduce disruption and serve as a competitive differentiator.

- Product-mix shift: higher compliance, lower-risk SKUs

- Sales-cycle impact: +1–4 weeks screening delays

- Risk: civil fines (~307,922 USD), criminal exposure, seizures

Energy and infrastructure governance

Policy on electricity pricing and grid reliability directly affects PCB plant uptime and operating costs; Taiwan targets 20% renewable electricity by 2025, shifting procurement incentives that can lower exposure to emerging carbon measures. Power rationing or outages force costly rescheduling, yield losses and supply-chain delays. Active engagement with local authorities speeds expansion permits and stable utilities access.

- Grid reliability: impacts uptime

- 20% renewables by 2025: procurement incentives

- Rationing: forces rescheduling, production loss

- Local engagement: eases permits and utilities access

Supply risk: Taiwan at ~60% PCB share, insurance rises to ~25%

Heightened Taiwan–China tensions (Taiwan ~60% of advanced PCB capacity in 2024) raise logistics and insurance costs (war‑risk marine up to ~25% in 2023–24), forcing dual‑site planning and inventory clauses. US export controls and tariffs reroute orders; screening adds 1–4 weeks and fines can reach ~307,922 USD. Subsidies (US CHIPS $52.7bn; IRA ~$369bn) and Taiwan renewables target 20% by 2025 reshape capex and site choices.

| Factor | Key metric |

|---|---|

| Taiwan PCB share (2024) | ~60% |

| War‑risk/marine insurance | up to ~25% (2023–24) |

| Export screening delay | +1–4 weeks |

| Max civil fine | ~307,922 USD |

| US subsidies | CHIPS $52.7bn |

| Clean energy funding | IRA ~$369bn; Taiwan 20% RE by 2025 |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Nan Ya Printed Circuit Board across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and region-specific examples. Designed for executives, consultants and investors, the analysis offers forward-looking insights to identify risks, opportunities and support strategic planning and funding decisions.

A concise, visually segmented PESTLE summary of Nan Ya Printed Circuit Board that streamlines external risk assessment and market positioning, making it easy to drop into presentations, share across teams, and customize with region- or product-specific notes for faster strategic decisions.

Economic factors

Electronics demand cyclicality

PCB demand tracks computing, telecom and consumer cycles, making Nan Ya's revenue volatile; the global PCB market was about USD 65 billion in 2023. Rapid growth in AI/data-center investment and rising 5G connections (approximately 1.6 billion by end-2024) can offset weak consumer-device demand. Flexible capacity and fast product-mix shifts help stabilize utilization. OEM/ODM inventory signals remain primary inputs for production planning.

Input cost volatility

Copper, laminates, chemicals and energy account for roughly 65% of Nan Ya PCB input costs and drive most COGS variance; LME copper swings and laminate supply tightness periodically spike margins. Hedging and multi‑sourcing reduce price shocks but introduce basis risk and execution costs, typically trimming realized volatility by ~25%. Long‑term vendor partnerships secure allocation in tight markets; contractual cost pass‑through preserves margins during inflationary periods.

Currency fluctuations

Revenue for Nan Ya Printed Circuit Board is often USD-linked while a portion of raw‑material and labor costs are in TWD and other local currencies, so FX swings directly affect gross margins and pricing competitiveness.

USD/TWD hovered near 31 in July 2025, and typical annual moves of 2–5% can materially shift margins for exporters.

Natural hedging by matching currency cash flows plus active hedging (forwards/options) is used to stabilize reported earnings.

Capital intensity and interest rates

Advanced multilayer and HDI lines demand sustained capex and tooling; higher policy rates in 2023–24 around 5% in major markets pushed WACC and internal hurdle rates materially higher, compressing NPV on greenfield expansions. Phased investments tied to customer LTAs reduce payback risk, while leasing and government-backed financing improve near-term cash flow.

- Capex intensity: sustained multi-year investment

- Rates impact: ~5% policy rates raised WACC

- Mitigation: phased builds + LTAs

- Cash optimization: leasing, govt-backed loans

Global supply-chain reconfiguration

China+1 strategies have shifted PCB demand toward Taiwan and Southeast Asia, shortening lead times by locating fabs near key customers; WTO data shows global goods trade fell 5.3% in 2020, highlighting vulnerability to disruptions. Shipping costs surged in 2021–22 and largely normalized by 2024, so logistics and trade lanes now strongly drive site selection while regional diversification reduces single-country exposure.

- China+1 demand shift: Taiwan, SE Asia

- Lead-time reduction via proximity

- Logistics/trade lanes shape siting

- WTO: goods trade -5.3% in 2020

- Regional diversification mitigates pandemic shocks

Supply risk: Taiwan at ~60% PCB share, insurance rises to ~25%

PCB demand tracks cyclic end markets; global PCB market ~USD 65bn (2023) while AI/data‑center capex and 5G (~1.6bn connections end‑2024) drive upside. Input costs (copper, laminates, chemicals, energy) ~65% of COGS; LME copper volatility and laminate tightness are primary margin drivers. USD/TWD ~31 (Jul 2025) so FX moves (±2–5% annually) materially affect margins; capex intensity and ~5% policy rates raise hurdle rates, favoring phased builds and LTAs.

| Metric | Value | Note |

|---|---|---|

| Global PCB market | USD 65bn (2023) | Source: industry data |

| 5G connections | ~1.6bn (end‑2024) | GSMA estimate |

| Input cost mix | ~65% of COGS | Copper/laminate/chemicals/energy |

| USD/TWD | ~31 (Jul 2025) | FX affects margins |

Preview Before You Purchase

Nan Ya Printed Circuit Board PESTLE Analysis

The Nan Ya Printed Circuit Board PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: this is the final, downloadable file.