NAPEC SWOT Analysis

Make Insightful Decisions Backed by Expert Research

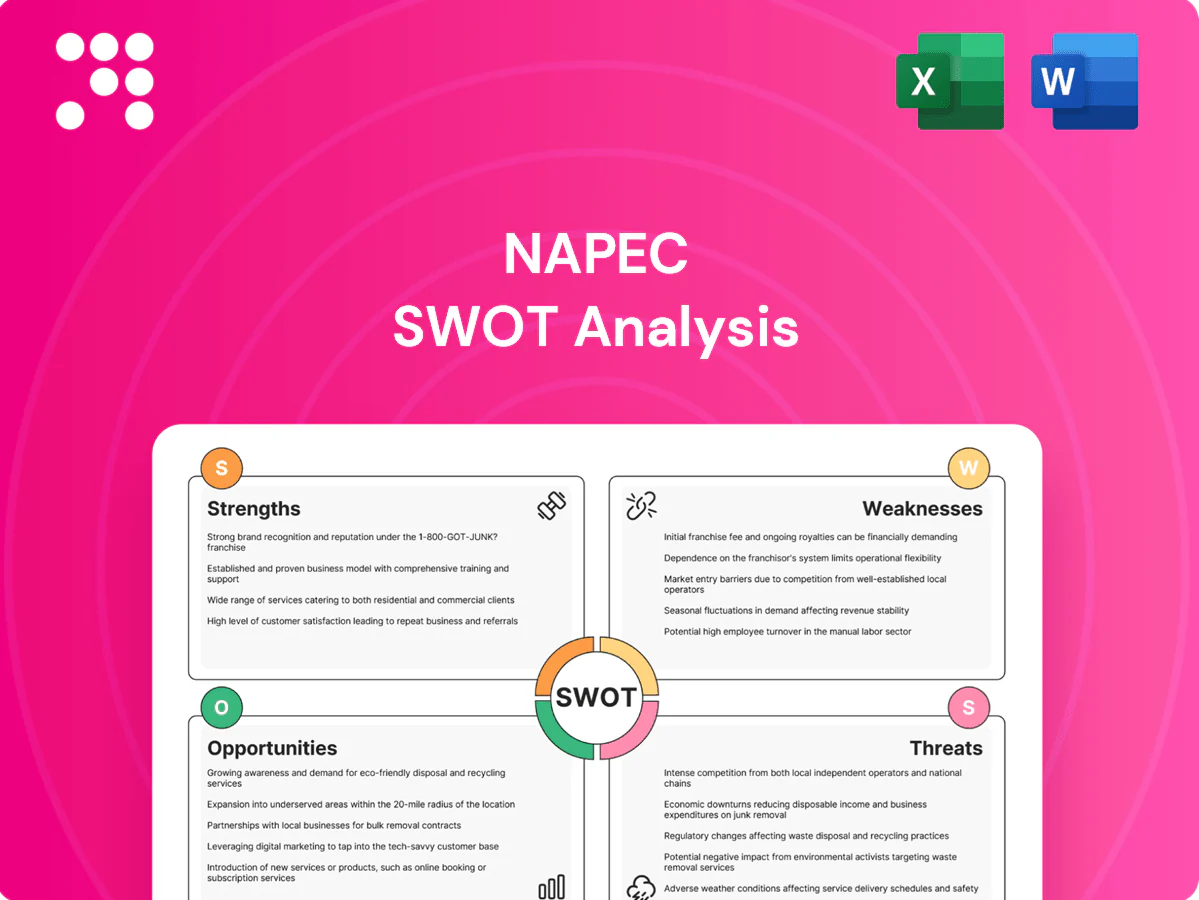

Explore key strengths, market threats, and growth levers in our concise NAPEC SWOT snapshot—then unlock the full strategic picture. Purchase the complete SWOT analysis for a research-backed, editable report with financial context and tactical recommendations to inform investor, advisor, or executive decisions.

Strengths

Deep T&D expertise

Decades of specialization in transmission, distribution and substations produce repeatable execution playbooks that lower field variance and commissioning risk. Proven field procedures reduce rework, outages and schedule slippage, supporting utility-focused reliability metrics such as SAIDI and SAIFI. That operational rigor drives measurable quality performance and enables higher win rates on complex, schedule-critical contracts.

Cross-border footprint

Operations across Canada and the U.S. diversify revenue and regulatory exposure, with NAPEC serving multiple provinces and states and a roughly 70/30 US‑to‑Canada revenue mix in 2024. The network provides proximity to major utility service territories covering key urban load centers. Cross‑border scale improves fleet utilization and crew deployment, supporting over 1,000 field personnel. It enhances bid credibility on multi‑jurisdiction programs.

Diversified service mix

NAPEC’s capabilities across line construction, maintenance, storm response, substations, public lighting and traffic systems smooth revenue volatility and enable bundled bids and multiyear master service agreements; municipal lighting and traffic work benefit from stable public-sector demand, with LED conversions typically cutting energy use 40–60%, supporting recurring retrofit and maintenance spend.

Long-term utility relationships

Long-term MSAs and recurring maintenance give NAPEC strong backlog visibility and predictable revenue, with utilities prioritizing safety, reliability and outage minimization which increases contract stickiness. Robust past-performance records enable negotiated scopes and streamlined change orders, lowering bid costs and stabilizing crew utilization across peak and off-peak cycles.

- MSAs underpin backlog visibility

- Utility emphasis on safety/reliability boosts retention

- Historical performance eases change orders

- Lower sales costs, steadier crew utilization

Safety and compliance culture

NAPEC's utility-grade safety programs lower incident risk and insurance exposure by aligning operations with OSHA, DOT and NERC standards, supporting bids for high-voltage projects; strong compliance reduces regulatory delays and claims. Credible safety records are a contractual prerequisite for utility and DOT work and differentiate NAPEC in prequalification screens.

- Utility-grade safety reduces incidents and insurance exposure

- Compliance with OSHA, DOT, NERC

- Safety records required for high-voltage work

- Differentiator in prequalification

Utility specialists — 70:30 US:CA, 1,000+ crews, 40–60% LED savings

Decades of utility-focused specialization yield repeatable execution, higher win rates on complex projects, and lower commissioning risk. Cross‑border scale (2024 revenue ~70/30 US:Canada) and >1,000 field personnel improve fleet utilization and bid credibility. Diversified services (line, substations, lighting) and long MSAs smooth volatility; LED work cuts energy 40–60% supporting recurring demand.

| Metric | 2024 |

|---|---|

| US:Canada revenue mix | 70:30 |

| Field personnel | >1,000 |

| LED energy reduction | 40–60% |

| Service lines | Line, substation, storm, lighting, traffic |

What is included in the product

Delivers a strategic overview of NAPEC’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and guide strategic decision-making.

Provides a concise, editable NAPEC SWOT matrix for fast strategy alignment and easy updates, helping teams quickly identify and relieve policy, regulatory, and operational pain points.

Weaknesses

Project margin volatility

Unit-price and lump-sum contracts expose NAPEC to execution risk, transferring cost overruns to the firm. Weather delays, permitting holdups and change-order friction routinely erode margins. Industry net margins are low single-digit, typically 1–4% in pipeline and energy construction. Small productivity misses of 1–3% can materially eliminate profitability.

Capital-intensive operations

Specialized fleets, tooling, and recurrent training force ongoing capex; fleet refreshes often require hundreds of millions in outlay. Idle equipment in shoulder seasons can cut utilization by roughly 15–25%, dragging returns. Depreciation and maintenance commonly consume about 10–15% of operating cash flow. Refresh cycles may clash with market slowdowns, amplifying liquidity strain.

Client concentration

Revenue is highly concentrated among a handful of large utilities and municipalities, exposing NAPEC to client-specific volatility. Rebid risk on MSAs creates step-down scenarios that can erode margins and contract volume. Pricing leverage tends to favor incumbents and larger primes, limiting NAPEC’s negotiating power. Loss of a top client would meaningfully reduce backlog and utilization.

Labor constraints

- Scarce specialists

- 3–4 year pipelines

- Training >$20,000

- Wages +~7% (2022–24)

- Union scheduling limits

Brand transition to NRB

Post-acquisition rebranding to NRB risks diluting NAPEC legacy recognition and client recall, with procurement databases and prequal lists commonly lagging updates by 30–90 days. Mixed branding complicates referrals and past-performance validation, creating compliance gaps, and adds integration overhead that can extend IT and HR alignment timelines by an estimated 20–40%.

- Brand dilution: legacy recognition loss

- Procurement lag: 30–90 days

- Referrals/validation: mixed-brand gaps

- Integration overhead: +20–40% timelines

Low 1-4% margins + 15-25% idle, rising wages +7% squeeze liquidity

Unit-price contracts, weather/permitting delays and 1–4% industry margins make 1–3% productivity misses fatal; equipment capex (hundreds $M) and 15–25% seasonal idle reduce returns; revenue concentration to few clients and rebid risk threaten backlog and utilization; labor shortages (3–4yr apprenticeships, >$20k training), wages +7% (2022–24) and brand/integration lags (30–90d, +20–40% timelines) amplify liquidity strain.

| Metric | Value |

|---|---|

| Industry margins | 1–4% |

| Idle utilization | 15–25% |

| Depreciation/Opex | 10–15% OCF |

| Training | >$20,000 |

| Wage inflation | +7% (2022–24) |

| Procurement lag | 30–90 days |

| Integration timeline | +20–40% |

Same Document Delivered

NAPEC SWOT Analysis

This is the actual NAPEC SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing the real file and will download the identical, full document after checkout.

Make Insightful Decisions Backed by Expert Research

Explore key strengths, market threats, and growth levers in our concise NAPEC SWOT snapshot—then unlock the full strategic picture. Purchase the complete SWOT analysis for a research-backed, editable report with financial context and tactical recommendations to inform investor, advisor, or executive decisions.

Strengths

Deep T&D expertise

Decades of specialization in transmission, distribution and substations produce repeatable execution playbooks that lower field variance and commissioning risk. Proven field procedures reduce rework, outages and schedule slippage, supporting utility-focused reliability metrics such as SAIDI and SAIFI. That operational rigor drives measurable quality performance and enables higher win rates on complex, schedule-critical contracts.

Cross-border footprint

Operations across Canada and the U.S. diversify revenue and regulatory exposure, with NAPEC serving multiple provinces and states and a roughly 70/30 US‑to‑Canada revenue mix in 2024. The network provides proximity to major utility service territories covering key urban load centers. Cross‑border scale improves fleet utilization and crew deployment, supporting over 1,000 field personnel. It enhances bid credibility on multi‑jurisdiction programs.

Diversified service mix

NAPEC’s capabilities across line construction, maintenance, storm response, substations, public lighting and traffic systems smooth revenue volatility and enable bundled bids and multiyear master service agreements; municipal lighting and traffic work benefit from stable public-sector demand, with LED conversions typically cutting energy use 40–60%, supporting recurring retrofit and maintenance spend.

Long-term utility relationships

Long-term MSAs and recurring maintenance give NAPEC strong backlog visibility and predictable revenue, with utilities prioritizing safety, reliability and outage minimization which increases contract stickiness. Robust past-performance records enable negotiated scopes and streamlined change orders, lowering bid costs and stabilizing crew utilization across peak and off-peak cycles.

- MSAs underpin backlog visibility

- Utility emphasis on safety/reliability boosts retention

- Historical performance eases change orders

- Lower sales costs, steadier crew utilization

Safety and compliance culture

NAPEC's utility-grade safety programs lower incident risk and insurance exposure by aligning operations with OSHA, DOT and NERC standards, supporting bids for high-voltage projects; strong compliance reduces regulatory delays and claims. Credible safety records are a contractual prerequisite for utility and DOT work and differentiate NAPEC in prequalification screens.

- Utility-grade safety reduces incidents and insurance exposure

- Compliance with OSHA, DOT, NERC

- Safety records required for high-voltage work

- Differentiator in prequalification

Utility specialists — 70:30 US:CA, 1,000+ crews, 40–60% LED savings

Decades of utility-focused specialization yield repeatable execution, higher win rates on complex projects, and lower commissioning risk. Cross‑border scale (2024 revenue ~70/30 US:Canada) and >1,000 field personnel improve fleet utilization and bid credibility. Diversified services (line, substations, lighting) and long MSAs smooth volatility; LED work cuts energy 40–60% supporting recurring demand.

| Metric | 2024 |

|---|---|

| US:Canada revenue mix | 70:30 |

| Field personnel | >1,000 |

| LED energy reduction | 40–60% |

| Service lines | Line, substation, storm, lighting, traffic |

What is included in the product

Delivers a strategic overview of NAPEC’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and guide strategic decision-making.

Provides a concise, editable NAPEC SWOT matrix for fast strategy alignment and easy updates, helping teams quickly identify and relieve policy, regulatory, and operational pain points.

Weaknesses

Project margin volatility

Unit-price and lump-sum contracts expose NAPEC to execution risk, transferring cost overruns to the firm. Weather delays, permitting holdups and change-order friction routinely erode margins. Industry net margins are low single-digit, typically 1–4% in pipeline and energy construction. Small productivity misses of 1–3% can materially eliminate profitability.

Capital-intensive operations

Specialized fleets, tooling, and recurrent training force ongoing capex; fleet refreshes often require hundreds of millions in outlay. Idle equipment in shoulder seasons can cut utilization by roughly 15–25%, dragging returns. Depreciation and maintenance commonly consume about 10–15% of operating cash flow. Refresh cycles may clash with market slowdowns, amplifying liquidity strain.

Client concentration

Revenue is highly concentrated among a handful of large utilities and municipalities, exposing NAPEC to client-specific volatility. Rebid risk on MSAs creates step-down scenarios that can erode margins and contract volume. Pricing leverage tends to favor incumbents and larger primes, limiting NAPEC’s negotiating power. Loss of a top client would meaningfully reduce backlog and utilization.

Labor constraints

- Scarce specialists

- 3–4 year pipelines

- Training >$20,000

- Wages +~7% (2022–24)

- Union scheduling limits

Brand transition to NRB

Post-acquisition rebranding to NRB risks diluting NAPEC legacy recognition and client recall, with procurement databases and prequal lists commonly lagging updates by 30–90 days. Mixed branding complicates referrals and past-performance validation, creating compliance gaps, and adds integration overhead that can extend IT and HR alignment timelines by an estimated 20–40%.

- Brand dilution: legacy recognition loss

- Procurement lag: 30–90 days

- Referrals/validation: mixed-brand gaps

- Integration overhead: +20–40% timelines

Low 1-4% margins + 15-25% idle, rising wages +7% squeeze liquidity

Unit-price contracts, weather/permitting delays and 1–4% industry margins make 1–3% productivity misses fatal; equipment capex (hundreds $M) and 15–25% seasonal idle reduce returns; revenue concentration to few clients and rebid risk threaten backlog and utilization; labor shortages (3–4yr apprenticeships, >$20k training), wages +7% (2022–24) and brand/integration lags (30–90d, +20–40% timelines) amplify liquidity strain.

| Metric | Value |

|---|---|

| Industry margins | 1–4% |

| Idle utilization | 15–25% |

| Depreciation/Opex | 10–15% OCF |

| Training | >$20,000 |

| Wage inflation | +7% (2022–24) |

| Procurement lag | 30–90 days |

| Integration timeline | +20–40% |

Same Document Delivered

NAPEC SWOT Analysis

This is the actual NAPEC SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing the real file and will download the identical, full document after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Explore key strengths, market threats, and growth levers in our concise NAPEC SWOT snapshot—then unlock the full strategic picture. Purchase the complete SWOT analysis for a research-backed, editable report with financial context and tactical recommendations to inform investor, advisor, or executive decisions.

Strengths

Deep T&D expertise

Decades of specialization in transmission, distribution and substations produce repeatable execution playbooks that lower field variance and commissioning risk. Proven field procedures reduce rework, outages and schedule slippage, supporting utility-focused reliability metrics such as SAIDI and SAIFI. That operational rigor drives measurable quality performance and enables higher win rates on complex, schedule-critical contracts.

Cross-border footprint

Operations across Canada and the U.S. diversify revenue and regulatory exposure, with NAPEC serving multiple provinces and states and a roughly 70/30 US‑to‑Canada revenue mix in 2024. The network provides proximity to major utility service territories covering key urban load centers. Cross‑border scale improves fleet utilization and crew deployment, supporting over 1,000 field personnel. It enhances bid credibility on multi‑jurisdiction programs.

Diversified service mix

NAPEC’s capabilities across line construction, maintenance, storm response, substations, public lighting and traffic systems smooth revenue volatility and enable bundled bids and multiyear master service agreements; municipal lighting and traffic work benefit from stable public-sector demand, with LED conversions typically cutting energy use 40–60%, supporting recurring retrofit and maintenance spend.

Long-term utility relationships

Long-term MSAs and recurring maintenance give NAPEC strong backlog visibility and predictable revenue, with utilities prioritizing safety, reliability and outage minimization which increases contract stickiness. Robust past-performance records enable negotiated scopes and streamlined change orders, lowering bid costs and stabilizing crew utilization across peak and off-peak cycles.

- MSAs underpin backlog visibility

- Utility emphasis on safety/reliability boosts retention

- Historical performance eases change orders

- Lower sales costs, steadier crew utilization

Safety and compliance culture

NAPEC's utility-grade safety programs lower incident risk and insurance exposure by aligning operations with OSHA, DOT and NERC standards, supporting bids for high-voltage projects; strong compliance reduces regulatory delays and claims. Credible safety records are a contractual prerequisite for utility and DOT work and differentiate NAPEC in prequalification screens.

- Utility-grade safety reduces incidents and insurance exposure

- Compliance with OSHA, DOT, NERC

- Safety records required for high-voltage work

- Differentiator in prequalification

Utility specialists — 70:30 US:CA, 1,000+ crews, 40–60% LED savings

Decades of utility-focused specialization yield repeatable execution, higher win rates on complex projects, and lower commissioning risk. Cross‑border scale (2024 revenue ~70/30 US:Canada) and >1,000 field personnel improve fleet utilization and bid credibility. Diversified services (line, substations, lighting) and long MSAs smooth volatility; LED work cuts energy 40–60% supporting recurring demand.

| Metric | 2024 |

|---|---|

| US:Canada revenue mix | 70:30 |

| Field personnel | >1,000 |

| LED energy reduction | 40–60% |

| Service lines | Line, substation, storm, lighting, traffic |

What is included in the product

Delivers a strategic overview of NAPEC’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and guide strategic decision-making.

Provides a concise, editable NAPEC SWOT matrix for fast strategy alignment and easy updates, helping teams quickly identify and relieve policy, regulatory, and operational pain points.

Weaknesses

Project margin volatility

Unit-price and lump-sum contracts expose NAPEC to execution risk, transferring cost overruns to the firm. Weather delays, permitting holdups and change-order friction routinely erode margins. Industry net margins are low single-digit, typically 1–4% in pipeline and energy construction. Small productivity misses of 1–3% can materially eliminate profitability.

Capital-intensive operations

Specialized fleets, tooling, and recurrent training force ongoing capex; fleet refreshes often require hundreds of millions in outlay. Idle equipment in shoulder seasons can cut utilization by roughly 15–25%, dragging returns. Depreciation and maintenance commonly consume about 10–15% of operating cash flow. Refresh cycles may clash with market slowdowns, amplifying liquidity strain.

Client concentration

Revenue is highly concentrated among a handful of large utilities and municipalities, exposing NAPEC to client-specific volatility. Rebid risk on MSAs creates step-down scenarios that can erode margins and contract volume. Pricing leverage tends to favor incumbents and larger primes, limiting NAPEC’s negotiating power. Loss of a top client would meaningfully reduce backlog and utilization.

Labor constraints

- Scarce specialists

- 3–4 year pipelines

- Training >$20,000

- Wages +~7% (2022–24)

- Union scheduling limits

Brand transition to NRB

Post-acquisition rebranding to NRB risks diluting NAPEC legacy recognition and client recall, with procurement databases and prequal lists commonly lagging updates by 30–90 days. Mixed branding complicates referrals and past-performance validation, creating compliance gaps, and adds integration overhead that can extend IT and HR alignment timelines by an estimated 20–40%.

- Brand dilution: legacy recognition loss

- Procurement lag: 30–90 days

- Referrals/validation: mixed-brand gaps

- Integration overhead: +20–40% timelines

Low 1-4% margins + 15-25% idle, rising wages +7% squeeze liquidity

Unit-price contracts, weather/permitting delays and 1–4% industry margins make 1–3% productivity misses fatal; equipment capex (hundreds $M) and 15–25% seasonal idle reduce returns; revenue concentration to few clients and rebid risk threaten backlog and utilization; labor shortages (3–4yr apprenticeships, >$20k training), wages +7% (2022–24) and brand/integration lags (30–90d, +20–40% timelines) amplify liquidity strain.

| Metric | Value |

|---|---|

| Industry margins | 1–4% |

| Idle utilization | 15–25% |

| Depreciation/Opex | 10–15% OCF |

| Training | >$20,000 |

| Wage inflation | +7% (2022–24) |

| Procurement lag | 30–90 days |

| Integration timeline | +20–40% |

Same Document Delivered

NAPEC SWOT Analysis

This is the actual NAPEC SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing the real file and will download the identical, full document after checkout.