North American Title Co. Business Model Canvas

Business Model Canvas for a Title Services Firm: Value, Partners, Monetization

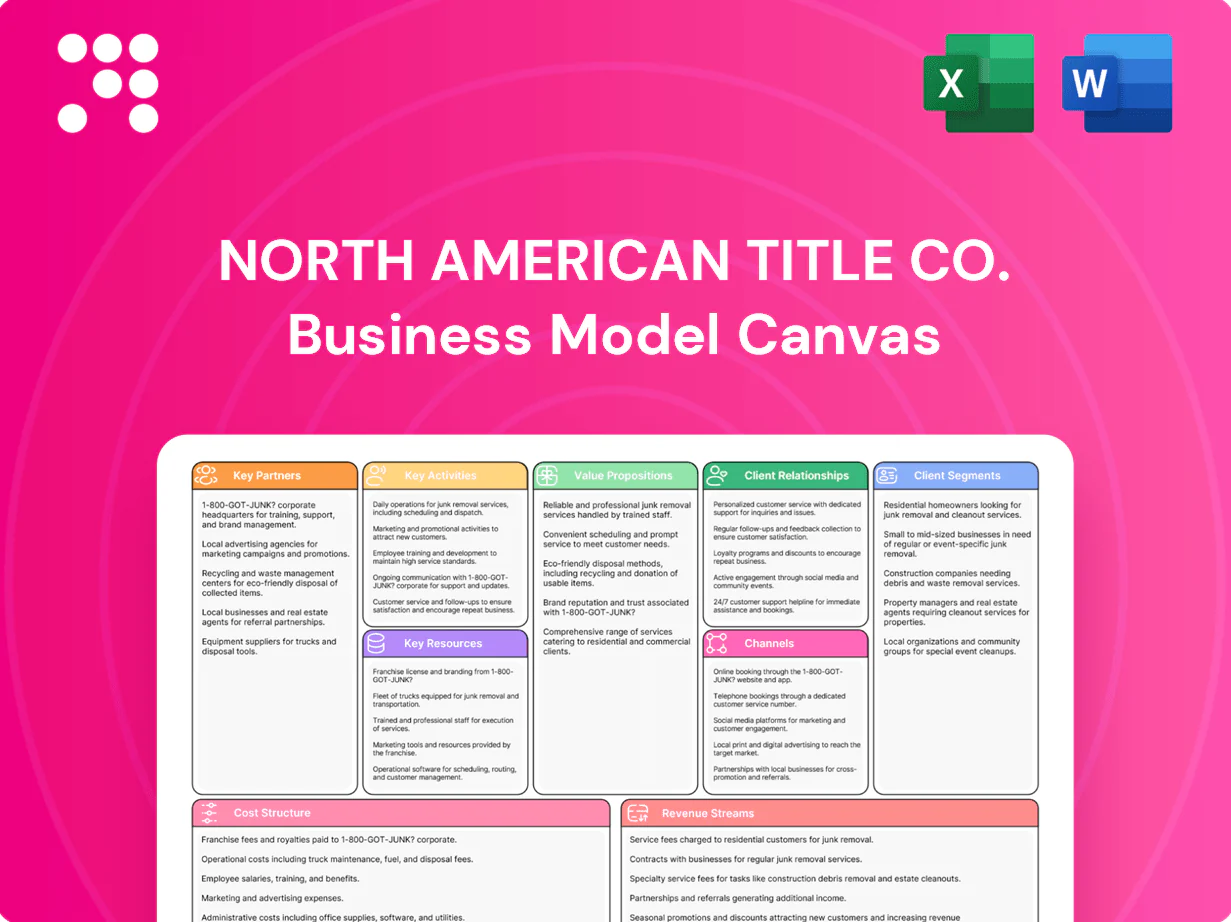

Unlock the full strategic blueprint behind North American Title Co.’s business model with our concise Business Model Canvas. This snapshot reveals how the company creates customer value, leverages key partnerships, and monetizes title services across markets. Ideal for investors, advisors, and founders seeking actionable, sector-specific insights—download the complete Word and Excel files to benchmark, adapt, and apply these proven strategies today.

Partnerships

Underwriters and reinsurance partners

Underwriters partner with reinsurers to spread risk on large commercial and aggregated residential portfolios, ceding portions of exposure to stabilize loss ratios and capital needs. In 2024 the U.S. title industry wrote roughly $11 billion in direct premiums, reinforcing the need for reinsurance to enable competitive pricing while preserving solvency. Ongoing actuarial collaboration refines retention thresholds and treaty terms based on loss modeling and capital stress tests.

Title agents and settlement providers

Independent and affiliated agents originate, close, and fund transactions on NATIC’s paper, supported by co-branded workflows, training, and audit programs that enforce compliance and quality. Preferred-agent networks accelerate throughput and expand geographic reach while performance dashboards provide real-time KPIs to guide appointments and remediation.

Data vendors and search firms

Public records aggregators, property data providers and search/exam partners supply the datasets that enable rapid, accurate title decisions; in 2024 API integrations reduced manual steps by up to 60% and cut error rates substantially. Firm SLAs (commonly 24–48 hour turnarounds) protect closing dates, while continuous data quality checks drove a roughly 30% improvement in curative outcomes.

Real estate and lender ecosystems

Relationships with mortgage lenders, brokers, builders and real estate brokerages drive referral flow and joint go-to-market initiatives focused on speed-to-close and certainty; pipeline visibility improves capacity planning and staffing. Compliance frameworks align with Fannie Mae/Freddie Mac seller/servicer requirements and CFPB/vendor management guidance in 2024.

- partners: lenders, brokers, builders, brokerages

- focus: speed-to-close, certainty

- ops: pipeline visibility → staffing

- compliance: Fannie/Freddie, CFPB standards (2024)

Regulatory and escrow banking partners

Regulatory and escrow banking partners — notably the 50 state Departments of Insurance plus DC, underwriter trade groups, and escrow banks — are critical stakeholders for North American Title Co. Robust banking partners are required for trust accounting, IOLTA compliance and cyber-wire controls. Proactive engagement with regulators reduces examination friction, while shared incident-response protocols and bank controls strengthen consumer protection.

- Regulators: 51 state/territorial DI bodies

- Banking: IOLTA & trust-account controls

- Risk: cyber-wire prevention & incident-response

- Trade groups: coordinated examiner engagement

Title partnerships cut manual steps 60%, boost curatives 30% and ensure 24–48h closings

Key partnerships—reinsurers, agents, data providers, lenders, regulators and escrow banks—enable risk transfer, distribution, data accuracy and closing certainty. 2024 metrics: US title direct premiums ~$11B; API integrations cut manual steps ~60% and curative rates improved ~30%; SLAs 24–48h; 51 state/territorial DI bodies engaged.

| Partner | Role | 2024 Metric |

|---|---|---|

| Reinsurers | Risk transfer | $11B industry premiums |

| Data/API | Accuracy/speed | -60% manual steps |

| Agents/Lenders | Distribution | SLA 24–48h |

| Regulators/Banks | Compliance/trust | 51 DI bodies |

What is included in the product

A comprehensive Business Model Canvas for North American Title Co. detailing customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks, with competitive advantages, linked SWOT insights and polished narrative ideal for presentations and investor discussions.

One-page business snapshot that relieves title industry complexity by condensing North American Title Co.'s strategy and operations into editable cells for fast team alignment and decision-making.

Activities

Title search and examination

Research chain of title, liens, encumbrances, and legal descriptions across jurisdictions to confirm a clear, insurable chain and flag jurisdictional exceptions. Standardize exam criteria to ensure consistent insurability judgments and surface curative actions early to keep closings on schedule. Maintain immutable audit trails to satisfy regulators and counterparties, retaining records 5–7 years per 2024 regulatory guidance.

Policy underwriting and issuance

Apply standardized underwriting guidelines to residential and commercial risks, assessing title defects, liens and survey issues to support issuance across varied transaction sizes; U.S. title insurers wrote roughly $16 billion in direct premiums in 2023. Price premiums by coverage limits, endorsements and transaction size, using rate filings and risk metrics to set fees. Issue owner’s and lender’s policies with appropriate exceptions and record/store policies and endorsements in secure electronic registries for claims handling and regulatory access.

Settlement, escrow, and disbursement

Coordinate closing documents, collect funds, and manage escrow safely, applying positive pay, dual control, and wire verification to prevent fraud and unauthorized transfers.

Disburse proceeds per signer instructions and applicable federal and state escrow laws, with all wire releases subject to dual confirmation.

Reconcile escrow accounts daily, and complete investigations and adjustments within 24 hours to meet fiduciary standards.

Claims handling and curative services

- Investigate and resolve

- Negotiate releases/pay losses/litigate

- Trend analysis to refine underwriting

- Transparent communication to preserve trust

Compliance, agent oversight, and cybersecurity

Conduct regular agent audits, licensing checks, and training while maintaining ALTA Best Practices and SOC controls; monitor cyber threats focused on payoff fraud and wire redirection and continuously update policies to align with evolving 2024 regulations.

- Agent audits, licensing, training

- ALTA Best Practices & SOC controls

- Monitor payoff fraud & wire redirection

- Policy updates for 2024 regulatory changes

Standardize underwriting; retain 5-7 year audit trails; dual-control escrow & 24h reconciliations

Research and exam title chains to ensure insurability and surface curatives; retain immutable audit trails 5–7 years per 2024 guidance. Apply standardized underwriting and pricing across residential/commercial risks (U.S. direct premiums ~$16B in 2023) and issue policies stored electronically. Manage escrow/closings with dual-control wires, daily reconciliations and 24-hour investigations; resolve claims via negotiation, payment or litigation.

| Metric | Value |

|---|---|

| U.S. direct premiums (2023) | $16B |

| Record retention | 5–7 years (2024) |

| Escrow reconciliation | Daily; investigations ≤24h |

| Wire releases | Dual confirmation |

Full Version Awaits

Business Model Canvas

The Business Model Canvas previewed here for North American Title Co. is the actual deliverable—not a mockup—and shows real content from the final file. When you purchase, you’ll receive this exact document with all sections included, ready to edit, present, or share. The full file is provided in editable Word and Excel formats for immediate download.

Business Model Canvas for a Title Services Firm: Value, Partners, Monetization

Unlock the full strategic blueprint behind North American Title Co.’s business model with our concise Business Model Canvas. This snapshot reveals how the company creates customer value, leverages key partnerships, and monetizes title services across markets. Ideal for investors, advisors, and founders seeking actionable, sector-specific insights—download the complete Word and Excel files to benchmark, adapt, and apply these proven strategies today.

Partnerships

Underwriters and reinsurance partners

Underwriters partner with reinsurers to spread risk on large commercial and aggregated residential portfolios, ceding portions of exposure to stabilize loss ratios and capital needs. In 2024 the U.S. title industry wrote roughly $11 billion in direct premiums, reinforcing the need for reinsurance to enable competitive pricing while preserving solvency. Ongoing actuarial collaboration refines retention thresholds and treaty terms based on loss modeling and capital stress tests.

Title agents and settlement providers

Independent and affiliated agents originate, close, and fund transactions on NATIC’s paper, supported by co-branded workflows, training, and audit programs that enforce compliance and quality. Preferred-agent networks accelerate throughput and expand geographic reach while performance dashboards provide real-time KPIs to guide appointments and remediation.

Data vendors and search firms

Public records aggregators, property data providers and search/exam partners supply the datasets that enable rapid, accurate title decisions; in 2024 API integrations reduced manual steps by up to 60% and cut error rates substantially. Firm SLAs (commonly 24–48 hour turnarounds) protect closing dates, while continuous data quality checks drove a roughly 30% improvement in curative outcomes.

Real estate and lender ecosystems

Relationships with mortgage lenders, brokers, builders and real estate brokerages drive referral flow and joint go-to-market initiatives focused on speed-to-close and certainty; pipeline visibility improves capacity planning and staffing. Compliance frameworks align with Fannie Mae/Freddie Mac seller/servicer requirements and CFPB/vendor management guidance in 2024.

- partners: lenders, brokers, builders, brokerages

- focus: speed-to-close, certainty

- ops: pipeline visibility → staffing

- compliance: Fannie/Freddie, CFPB standards (2024)

Regulatory and escrow banking partners

Regulatory and escrow banking partners — notably the 50 state Departments of Insurance plus DC, underwriter trade groups, and escrow banks — are critical stakeholders for North American Title Co. Robust banking partners are required for trust accounting, IOLTA compliance and cyber-wire controls. Proactive engagement with regulators reduces examination friction, while shared incident-response protocols and bank controls strengthen consumer protection.

- Regulators: 51 state/territorial DI bodies

- Banking: IOLTA & trust-account controls

- Risk: cyber-wire prevention & incident-response

- Trade groups: coordinated examiner engagement

Title partnerships cut manual steps 60%, boost curatives 30% and ensure 24–48h closings

Key partnerships—reinsurers, agents, data providers, lenders, regulators and escrow banks—enable risk transfer, distribution, data accuracy and closing certainty. 2024 metrics: US title direct premiums ~$11B; API integrations cut manual steps ~60% and curative rates improved ~30%; SLAs 24–48h; 51 state/territorial DI bodies engaged.

| Partner | Role | 2024 Metric |

|---|---|---|

| Reinsurers | Risk transfer | $11B industry premiums |

| Data/API | Accuracy/speed | -60% manual steps |

| Agents/Lenders | Distribution | SLA 24–48h |

| Regulators/Banks | Compliance/trust | 51 DI bodies |

What is included in the product

A comprehensive Business Model Canvas for North American Title Co. detailing customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks, with competitive advantages, linked SWOT insights and polished narrative ideal for presentations and investor discussions.

One-page business snapshot that relieves title industry complexity by condensing North American Title Co.'s strategy and operations into editable cells for fast team alignment and decision-making.

Activities

Title search and examination

Research chain of title, liens, encumbrances, and legal descriptions across jurisdictions to confirm a clear, insurable chain and flag jurisdictional exceptions. Standardize exam criteria to ensure consistent insurability judgments and surface curative actions early to keep closings on schedule. Maintain immutable audit trails to satisfy regulators and counterparties, retaining records 5–7 years per 2024 regulatory guidance.

Policy underwriting and issuance

Apply standardized underwriting guidelines to residential and commercial risks, assessing title defects, liens and survey issues to support issuance across varied transaction sizes; U.S. title insurers wrote roughly $16 billion in direct premiums in 2023. Price premiums by coverage limits, endorsements and transaction size, using rate filings and risk metrics to set fees. Issue owner’s and lender’s policies with appropriate exceptions and record/store policies and endorsements in secure electronic registries for claims handling and regulatory access.

Settlement, escrow, and disbursement

Coordinate closing documents, collect funds, and manage escrow safely, applying positive pay, dual control, and wire verification to prevent fraud and unauthorized transfers.

Disburse proceeds per signer instructions and applicable federal and state escrow laws, with all wire releases subject to dual confirmation.

Reconcile escrow accounts daily, and complete investigations and adjustments within 24 hours to meet fiduciary standards.

Claims handling and curative services

- Investigate and resolve

- Negotiate releases/pay losses/litigate

- Trend analysis to refine underwriting

- Transparent communication to preserve trust

Compliance, agent oversight, and cybersecurity

Conduct regular agent audits, licensing checks, and training while maintaining ALTA Best Practices and SOC controls; monitor cyber threats focused on payoff fraud and wire redirection and continuously update policies to align with evolving 2024 regulations.

- Agent audits, licensing, training

- ALTA Best Practices & SOC controls

- Monitor payoff fraud & wire redirection

- Policy updates for 2024 regulatory changes

Standardize underwriting; retain 5-7 year audit trails; dual-control escrow & 24h reconciliations

Research and exam title chains to ensure insurability and surface curatives; retain immutable audit trails 5–7 years per 2024 guidance. Apply standardized underwriting and pricing across residential/commercial risks (U.S. direct premiums ~$16B in 2023) and issue policies stored electronically. Manage escrow/closings with dual-control wires, daily reconciliations and 24-hour investigations; resolve claims via negotiation, payment or litigation.

| Metric | Value |

|---|---|

| U.S. direct premiums (2023) | $16B |

| Record retention | 5–7 years (2024) |

| Escrow reconciliation | Daily; investigations ≤24h |

| Wire releases | Dual confirmation |

Full Version Awaits

Business Model Canvas

The Business Model Canvas previewed here for North American Title Co. is the actual deliverable—not a mockup—and shows real content from the final file. When you purchase, you’ll receive this exact document with all sections included, ready to edit, present, or share. The full file is provided in editable Word and Excel formats for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas for a Title Services Firm: Value, Partners, Monetization

Unlock the full strategic blueprint behind North American Title Co.’s business model with our concise Business Model Canvas. This snapshot reveals how the company creates customer value, leverages key partnerships, and monetizes title services across markets. Ideal for investors, advisors, and founders seeking actionable, sector-specific insights—download the complete Word and Excel files to benchmark, adapt, and apply these proven strategies today.

Partnerships

Underwriters and reinsurance partners

Underwriters partner with reinsurers to spread risk on large commercial and aggregated residential portfolios, ceding portions of exposure to stabilize loss ratios and capital needs. In 2024 the U.S. title industry wrote roughly $11 billion in direct premiums, reinforcing the need for reinsurance to enable competitive pricing while preserving solvency. Ongoing actuarial collaboration refines retention thresholds and treaty terms based on loss modeling and capital stress tests.

Title agents and settlement providers

Independent and affiliated agents originate, close, and fund transactions on NATIC’s paper, supported by co-branded workflows, training, and audit programs that enforce compliance and quality. Preferred-agent networks accelerate throughput and expand geographic reach while performance dashboards provide real-time KPIs to guide appointments and remediation.

Data vendors and search firms

Public records aggregators, property data providers and search/exam partners supply the datasets that enable rapid, accurate title decisions; in 2024 API integrations reduced manual steps by up to 60% and cut error rates substantially. Firm SLAs (commonly 24–48 hour turnarounds) protect closing dates, while continuous data quality checks drove a roughly 30% improvement in curative outcomes.

Real estate and lender ecosystems

Relationships with mortgage lenders, brokers, builders and real estate brokerages drive referral flow and joint go-to-market initiatives focused on speed-to-close and certainty; pipeline visibility improves capacity planning and staffing. Compliance frameworks align with Fannie Mae/Freddie Mac seller/servicer requirements and CFPB/vendor management guidance in 2024.

- partners: lenders, brokers, builders, brokerages

- focus: speed-to-close, certainty

- ops: pipeline visibility → staffing

- compliance: Fannie/Freddie, CFPB standards (2024)

Regulatory and escrow banking partners

Regulatory and escrow banking partners — notably the 50 state Departments of Insurance plus DC, underwriter trade groups, and escrow banks — are critical stakeholders for North American Title Co. Robust banking partners are required for trust accounting, IOLTA compliance and cyber-wire controls. Proactive engagement with regulators reduces examination friction, while shared incident-response protocols and bank controls strengthen consumer protection.

- Regulators: 51 state/territorial DI bodies

- Banking: IOLTA & trust-account controls

- Risk: cyber-wire prevention & incident-response

- Trade groups: coordinated examiner engagement

Title partnerships cut manual steps 60%, boost curatives 30% and ensure 24–48h closings

Key partnerships—reinsurers, agents, data providers, lenders, regulators and escrow banks—enable risk transfer, distribution, data accuracy and closing certainty. 2024 metrics: US title direct premiums ~$11B; API integrations cut manual steps ~60% and curative rates improved ~30%; SLAs 24–48h; 51 state/territorial DI bodies engaged.

| Partner | Role | 2024 Metric |

|---|---|---|

| Reinsurers | Risk transfer | $11B industry premiums |

| Data/API | Accuracy/speed | -60% manual steps |

| Agents/Lenders | Distribution | SLA 24–48h |

| Regulators/Banks | Compliance/trust | 51 DI bodies |

What is included in the product

A comprehensive Business Model Canvas for North American Title Co. detailing customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks, with competitive advantages, linked SWOT insights and polished narrative ideal for presentations and investor discussions.

One-page business snapshot that relieves title industry complexity by condensing North American Title Co.'s strategy and operations into editable cells for fast team alignment and decision-making.

Activities

Title search and examination

Research chain of title, liens, encumbrances, and legal descriptions across jurisdictions to confirm a clear, insurable chain and flag jurisdictional exceptions. Standardize exam criteria to ensure consistent insurability judgments and surface curative actions early to keep closings on schedule. Maintain immutable audit trails to satisfy regulators and counterparties, retaining records 5–7 years per 2024 regulatory guidance.

Policy underwriting and issuance

Apply standardized underwriting guidelines to residential and commercial risks, assessing title defects, liens and survey issues to support issuance across varied transaction sizes; U.S. title insurers wrote roughly $16 billion in direct premiums in 2023. Price premiums by coverage limits, endorsements and transaction size, using rate filings and risk metrics to set fees. Issue owner’s and lender’s policies with appropriate exceptions and record/store policies and endorsements in secure electronic registries for claims handling and regulatory access.

Settlement, escrow, and disbursement

Coordinate closing documents, collect funds, and manage escrow safely, applying positive pay, dual control, and wire verification to prevent fraud and unauthorized transfers.

Disburse proceeds per signer instructions and applicable federal and state escrow laws, with all wire releases subject to dual confirmation.

Reconcile escrow accounts daily, and complete investigations and adjustments within 24 hours to meet fiduciary standards.

Claims handling and curative services

- Investigate and resolve

- Negotiate releases/pay losses/litigate

- Trend analysis to refine underwriting

- Transparent communication to preserve trust

Compliance, agent oversight, and cybersecurity

Conduct regular agent audits, licensing checks, and training while maintaining ALTA Best Practices and SOC controls; monitor cyber threats focused on payoff fraud and wire redirection and continuously update policies to align with evolving 2024 regulations.

- Agent audits, licensing, training

- ALTA Best Practices & SOC controls

- Monitor payoff fraud & wire redirection

- Policy updates for 2024 regulatory changes

Standardize underwriting; retain 5-7 year audit trails; dual-control escrow & 24h reconciliations

Research and exam title chains to ensure insurability and surface curatives; retain immutable audit trails 5–7 years per 2024 guidance. Apply standardized underwriting and pricing across residential/commercial risks (U.S. direct premiums ~$16B in 2023) and issue policies stored electronically. Manage escrow/closings with dual-control wires, daily reconciliations and 24-hour investigations; resolve claims via negotiation, payment or litigation.

| Metric | Value |

|---|---|

| U.S. direct premiums (2023) | $16B |

| Record retention | 5–7 years (2024) |

| Escrow reconciliation | Daily; investigations ≤24h |

| Wire releases | Dual confirmation |

Full Version Awaits

Business Model Canvas

The Business Model Canvas previewed here for North American Title Co. is the actual deliverable—not a mockup—and shows real content from the final file. When you purchase, you’ll receive this exact document with all sections included, ready to edit, present, or share. The full file is provided in editable Word and Excel formats for immediate download.