National Pecan Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

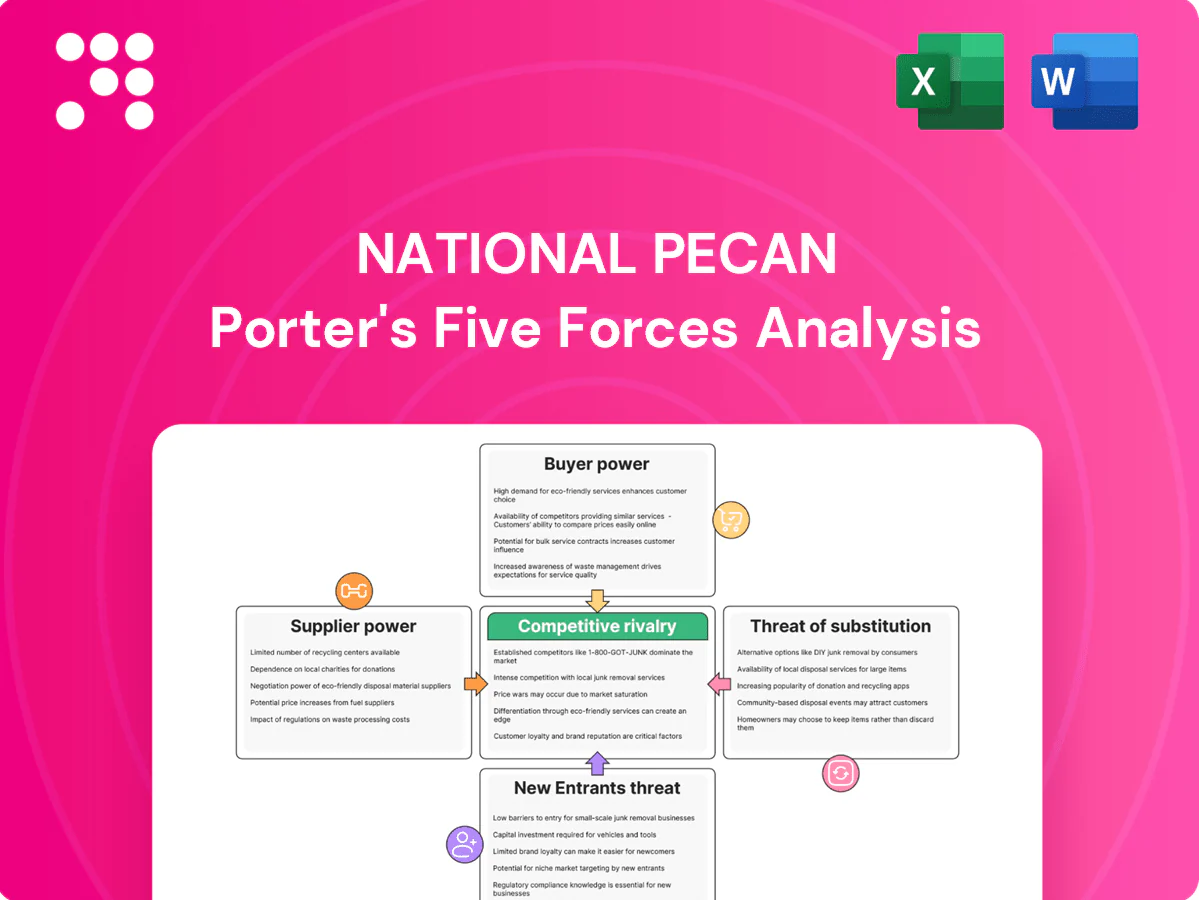

National Pecan faces moderate supplier power and seasonal input risks, while buyer concentration and price sensitivity heighten competitive pressure; substitutes and scale economies shape market rivalry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore National Pecan’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Vertical integration dampens grower leverage

Owning orchards and accumulated inventory reduces dependence on third-party growers, limiting supplier bargaining power; internal supply provides baseline volumes, tighter quality control and price-discovery advantages versus spot markets—important given U.S. pecan production was about 341 million pounds in 2023–24 per USDA—however integration cannot fully offset crop shortfalls in weak harvest years.

Fragmented grower base with regional concentration

National Pecan faces a fragmented grower base concentrated in Georgia, Texas, New Mexico and Mexico, with Mexico the world’s largest pecan producer, which dilutes individual supplier power. Regional weather events and disease outbreaks (drought, scab) can sharply tighten local supply and temporarily raise grower leverage. Cross-region sourcing and imports reduce hold-up risk, while long-term contracts and pool pricing smooth seasonal volatility.

Ag-input suppliers hold moderate influence

Ag-input costs (fertilizer, irrigation, labor, equipment) directly squeeze farm margins and nut costs; fertilizer prices in 2024 sit roughly 30–40% below 2022 peaks while labor costs have risen about 10–12% since 2020 to near $16–17/hr. Water constraints in key growing regions intermittently push irrigation costs higher. Brand availability limits sustained supplier pricing power, and Diamond Foods’ scale can secure 3–7% purchasing discounts.

Quality, certifications, and food safety as leverage points

Growers delivering specified sizes, 4–6% moisture and aflatoxin below the FDA action level of 20 ppb can command premiums; many buyers prefer <10 ppb for export markets, raising supplier leverage. Certifications such as GFSI-benchmarked schemes and GAP reduce buyer risk and shift bargaining power upstream, while NPC’s processing expertise standardizes kernels and narrows that edge. Supplier audits and support programs align incentives and stabilize contract terms.

- size/moisture control

- aflatoxin <20 ppb (FDA)

- GFSI/GAP risk reduction

- NPC processing standardization

- audits/support stabilize terms

Crop cyclicality and inventory carry influence pricing

Pecans show strong alternate-bearing and weather-driven yield swings, often producing 30–50% year-to-year volume variation, creating acute supply-driven price spikes that boost supplier leverage in short crops and shift bargaining power to processors in bumper years with carryover stock.

Strategic inventory carry and forward contracting/hedging (used across the industry) smooth negotiation outcomes, while vertical integration allows firms to buffer harvest timing and quality variability through processing and storage control.

- Supply swing: 30–50% yield variability

- Supplier leverage: heightened in short crops

- Processor leverage: increases with carryover inventory

- Risk mitigation: inventory, forward contracts, hedging, integration

Orchard ownership cuts supplier power; US pecan output ~341M lb 2023–24

Owning orchards and inventory lowers supplier power but cannot fully offset 30–50% yield swings; US pecan output was about 341M lb in 2023–24. Fragmented growers (GA, TX, NM, Mexico) dilute individual power, though short crops raise leverage. Input costs: fertilizer ~30–40% below 2022 peaks (2024), labor ~$16–17/hr; contracts and integration mitigate risk.

| Metric | Value |

|---|---|

| US production (2023–24) | 341M lb |

| Yield variability | 30–50% |

| Fertilizer (2024 vs 2022) | -30–40% |

| Labor (2024) | $16–17/hr |

What is included in the product

Concise Porter's Five Forces for National Pecan, identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces tailored to the National Pecan sector—quickly spot supplier power, buyer trends, and newcomer risks to cut analysis time; swap in your data or duplicate scenarios (pre/post regulation, climate shocks) for instant, presentation-ready insights.

Customers Bargaining Power

Large CPGs and retailers wield volume leverage

Global ingredient, bakery, and retail customers consolidate demand and negotiate aggressively, with the top 4 US grocery retailers capturing roughly 55–60% of grocery sales in 2024, driving multi-origin sourcing and tight specs. They pressure cost-downs and volume discounts while seeking supply diversity. NPC’s scale and Diamond affiliation provide countervailing leverage and preferred access. Still, loss of a major account would meaningfully hit plant utilization and margins.

Commodity transparency and low switching costs

Market prices for inshell (~$1.60/lb in 2024) and shelled meats (~$4.00/lb in 2024) are widely published (USDA/NASS), constraining processor pricing discretion. Qualified buyers can switch among certified processors with limited friction, raising buyer power. Service, reliability and yield performance become key differentiators; NPC must sustain >95% on-time delivery and robust technical support to defend premium pricing.

Specification intensity raises buyer expectations

Bakeries and confectioners demand consistent piece sizes, color, and micro standards, and failures trigger rework and claims that tighten buyer oversight. Meeting these higher specs shifts negotiation from price to value, reducing direct price pressure as buyers pay for reliability. NPC’s 2024 processing, grading, and QC systems are critical to maintain customer stickiness by minimizing defects and traceability issues.

Private label and co-manufacturing pressure margins

Retail private label, which reached about 20% of US grocery sales in 2024, drives aggressive lowest-delivered-cost sourcing; co-manufacturing contracts are frequently rebid annually, intensifying price pressure on NPC. NPC can offset margin squeeze through a diversified product mix and byproduct valorization that can boost gross margins by an estimated 3–7% (2024 industry benchmarks). Establishing long-term supply programs with performance KPIs has been shown to cut supplier churn by up to 40%, stabilizing pricing and volume.

International buyers add FX and trade complexity

Export markets add currency risk, tariffs and documentary complexity that increase buyer leverage; buyers often request FX‑adjusted pricing or extended payment terms, pressuring margins. NPC’s global logistics and compliance capabilities reduce these demands by ensuring timely clearance and predictable netbacks. Geographic diversification spreads exposure and limits any single market’s bargaining power.

- FX, tariffs, documentation raise buyer power

- Buyers push FX pricing/longer terms

- NPC logistics/compliance mitigate demands

- Diversification balances market leverage

Top‑4 grocers 55–60%; >95% OTD needed to protect shelled premiums

Concentrated global buyers (top‑4 US grocers 55–60% 2024) extract price/term concessions; published inshell ~$1.60/lb and shelled ~$4.00/lb cap pricing. High spec buyers favor reliability over price; NPC must sustain >95% OTD to retain premiums. Private label ~20% of US grocery (2024) amplifies annual rebids and margin pressure.

| Metric | 2024 |

|---|---|

| Top‑4 grocer share | 55–60% |

| Inshell price | $1.60/lb |

| Shelled price | $4.00/lb |

| Private label | ~20% |

Same Document Delivered

National Pecan Porter's Five Forces Analysis

This preview shows the exact National Pecan Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely what you'll get upon payment.

Go Beyond the Preview—Access the Full Strategic Report

National Pecan faces moderate supplier power and seasonal input risks, while buyer concentration and price sensitivity heighten competitive pressure; substitutes and scale economies shape market rivalry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore National Pecan’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Vertical integration dampens grower leverage

Owning orchards and accumulated inventory reduces dependence on third-party growers, limiting supplier bargaining power; internal supply provides baseline volumes, tighter quality control and price-discovery advantages versus spot markets—important given U.S. pecan production was about 341 million pounds in 2023–24 per USDA—however integration cannot fully offset crop shortfalls in weak harvest years.

Fragmented grower base with regional concentration

National Pecan faces a fragmented grower base concentrated in Georgia, Texas, New Mexico and Mexico, with Mexico the world’s largest pecan producer, which dilutes individual supplier power. Regional weather events and disease outbreaks (drought, scab) can sharply tighten local supply and temporarily raise grower leverage. Cross-region sourcing and imports reduce hold-up risk, while long-term contracts and pool pricing smooth seasonal volatility.

Ag-input suppliers hold moderate influence

Ag-input costs (fertilizer, irrigation, labor, equipment) directly squeeze farm margins and nut costs; fertilizer prices in 2024 sit roughly 30–40% below 2022 peaks while labor costs have risen about 10–12% since 2020 to near $16–17/hr. Water constraints in key growing regions intermittently push irrigation costs higher. Brand availability limits sustained supplier pricing power, and Diamond Foods’ scale can secure 3–7% purchasing discounts.

Quality, certifications, and food safety as leverage points

Growers delivering specified sizes, 4–6% moisture and aflatoxin below the FDA action level of 20 ppb can command premiums; many buyers prefer <10 ppb for export markets, raising supplier leverage. Certifications such as GFSI-benchmarked schemes and GAP reduce buyer risk and shift bargaining power upstream, while NPC’s processing expertise standardizes kernels and narrows that edge. Supplier audits and support programs align incentives and stabilize contract terms.

- size/moisture control

- aflatoxin <20 ppb (FDA)

- GFSI/GAP risk reduction

- NPC processing standardization

- audits/support stabilize terms

Crop cyclicality and inventory carry influence pricing

Pecans show strong alternate-bearing and weather-driven yield swings, often producing 30–50% year-to-year volume variation, creating acute supply-driven price spikes that boost supplier leverage in short crops and shift bargaining power to processors in bumper years with carryover stock.

Strategic inventory carry and forward contracting/hedging (used across the industry) smooth negotiation outcomes, while vertical integration allows firms to buffer harvest timing and quality variability through processing and storage control.

- Supply swing: 30–50% yield variability

- Supplier leverage: heightened in short crops

- Processor leverage: increases with carryover inventory

- Risk mitigation: inventory, forward contracts, hedging, integration

Orchard ownership cuts supplier power; US pecan output ~341M lb 2023–24

Owning orchards and inventory lowers supplier power but cannot fully offset 30–50% yield swings; US pecan output was about 341M lb in 2023–24. Fragmented growers (GA, TX, NM, Mexico) dilute individual power, though short crops raise leverage. Input costs: fertilizer ~30–40% below 2022 peaks (2024), labor ~$16–17/hr; contracts and integration mitigate risk.

| Metric | Value |

|---|---|

| US production (2023–24) | 341M lb |

| Yield variability | 30–50% |

| Fertilizer (2024 vs 2022) | -30–40% |

| Labor (2024) | $16–17/hr |

What is included in the product

Concise Porter's Five Forces for National Pecan, identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces tailored to the National Pecan sector—quickly spot supplier power, buyer trends, and newcomer risks to cut analysis time; swap in your data or duplicate scenarios (pre/post regulation, climate shocks) for instant, presentation-ready insights.

Customers Bargaining Power

Large CPGs and retailers wield volume leverage

Global ingredient, bakery, and retail customers consolidate demand and negotiate aggressively, with the top 4 US grocery retailers capturing roughly 55–60% of grocery sales in 2024, driving multi-origin sourcing and tight specs. They pressure cost-downs and volume discounts while seeking supply diversity. NPC’s scale and Diamond affiliation provide countervailing leverage and preferred access. Still, loss of a major account would meaningfully hit plant utilization and margins.

Commodity transparency and low switching costs

Market prices for inshell (~$1.60/lb in 2024) and shelled meats (~$4.00/lb in 2024) are widely published (USDA/NASS), constraining processor pricing discretion. Qualified buyers can switch among certified processors with limited friction, raising buyer power. Service, reliability and yield performance become key differentiators; NPC must sustain >95% on-time delivery and robust technical support to defend premium pricing.

Specification intensity raises buyer expectations

Bakeries and confectioners demand consistent piece sizes, color, and micro standards, and failures trigger rework and claims that tighten buyer oversight. Meeting these higher specs shifts negotiation from price to value, reducing direct price pressure as buyers pay for reliability. NPC’s 2024 processing, grading, and QC systems are critical to maintain customer stickiness by minimizing defects and traceability issues.

Private label and co-manufacturing pressure margins

Retail private label, which reached about 20% of US grocery sales in 2024, drives aggressive lowest-delivered-cost sourcing; co-manufacturing contracts are frequently rebid annually, intensifying price pressure on NPC. NPC can offset margin squeeze through a diversified product mix and byproduct valorization that can boost gross margins by an estimated 3–7% (2024 industry benchmarks). Establishing long-term supply programs with performance KPIs has been shown to cut supplier churn by up to 40%, stabilizing pricing and volume.

International buyers add FX and trade complexity

Export markets add currency risk, tariffs and documentary complexity that increase buyer leverage; buyers often request FX‑adjusted pricing or extended payment terms, pressuring margins. NPC’s global logistics and compliance capabilities reduce these demands by ensuring timely clearance and predictable netbacks. Geographic diversification spreads exposure and limits any single market’s bargaining power.

- FX, tariffs, documentation raise buyer power

- Buyers push FX pricing/longer terms

- NPC logistics/compliance mitigate demands

- Diversification balances market leverage

Top‑4 grocers 55–60%; >95% OTD needed to protect shelled premiums

Concentrated global buyers (top‑4 US grocers 55–60% 2024) extract price/term concessions; published inshell ~$1.60/lb and shelled ~$4.00/lb cap pricing. High spec buyers favor reliability over price; NPC must sustain >95% OTD to retain premiums. Private label ~20% of US grocery (2024) amplifies annual rebids and margin pressure.

| Metric | 2024 |

|---|---|

| Top‑4 grocer share | 55–60% |

| Inshell price | $1.60/lb |

| Shelled price | $4.00/lb |

| Private label | ~20% |

Same Document Delivered

National Pecan Porter's Five Forces Analysis

This preview shows the exact National Pecan Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely what you'll get upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

National Pecan faces moderate supplier power and seasonal input risks, while buyer concentration and price sensitivity heighten competitive pressure; substitutes and scale economies shape market rivalry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore National Pecan’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Vertical integration dampens grower leverage

Owning orchards and accumulated inventory reduces dependence on third-party growers, limiting supplier bargaining power; internal supply provides baseline volumes, tighter quality control and price-discovery advantages versus spot markets—important given U.S. pecan production was about 341 million pounds in 2023–24 per USDA—however integration cannot fully offset crop shortfalls in weak harvest years.

Fragmented grower base with regional concentration

National Pecan faces a fragmented grower base concentrated in Georgia, Texas, New Mexico and Mexico, with Mexico the world’s largest pecan producer, which dilutes individual supplier power. Regional weather events and disease outbreaks (drought, scab) can sharply tighten local supply and temporarily raise grower leverage. Cross-region sourcing and imports reduce hold-up risk, while long-term contracts and pool pricing smooth seasonal volatility.

Ag-input suppliers hold moderate influence

Ag-input costs (fertilizer, irrigation, labor, equipment) directly squeeze farm margins and nut costs; fertilizer prices in 2024 sit roughly 30–40% below 2022 peaks while labor costs have risen about 10–12% since 2020 to near $16–17/hr. Water constraints in key growing regions intermittently push irrigation costs higher. Brand availability limits sustained supplier pricing power, and Diamond Foods’ scale can secure 3–7% purchasing discounts.

Quality, certifications, and food safety as leverage points

Growers delivering specified sizes, 4–6% moisture and aflatoxin below the FDA action level of 20 ppb can command premiums; many buyers prefer <10 ppb for export markets, raising supplier leverage. Certifications such as GFSI-benchmarked schemes and GAP reduce buyer risk and shift bargaining power upstream, while NPC’s processing expertise standardizes kernels and narrows that edge. Supplier audits and support programs align incentives and stabilize contract terms.

- size/moisture control

- aflatoxin <20 ppb (FDA)

- GFSI/GAP risk reduction

- NPC processing standardization

- audits/support stabilize terms

Crop cyclicality and inventory carry influence pricing

Pecans show strong alternate-bearing and weather-driven yield swings, often producing 30–50% year-to-year volume variation, creating acute supply-driven price spikes that boost supplier leverage in short crops and shift bargaining power to processors in bumper years with carryover stock.

Strategic inventory carry and forward contracting/hedging (used across the industry) smooth negotiation outcomes, while vertical integration allows firms to buffer harvest timing and quality variability through processing and storage control.

- Supply swing: 30–50% yield variability

- Supplier leverage: heightened in short crops

- Processor leverage: increases with carryover inventory

- Risk mitigation: inventory, forward contracts, hedging, integration

Orchard ownership cuts supplier power; US pecan output ~341M lb 2023–24

Owning orchards and inventory lowers supplier power but cannot fully offset 30–50% yield swings; US pecan output was about 341M lb in 2023–24. Fragmented growers (GA, TX, NM, Mexico) dilute individual power, though short crops raise leverage. Input costs: fertilizer ~30–40% below 2022 peaks (2024), labor ~$16–17/hr; contracts and integration mitigate risk.

| Metric | Value |

|---|---|

| US production (2023–24) | 341M lb |

| Yield variability | 30–50% |

| Fertilizer (2024 vs 2022) | -30–40% |

| Labor (2024) | $16–17/hr |

What is included in the product

Concise Porter's Five Forces for National Pecan, identifying competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces tailored to the National Pecan sector—quickly spot supplier power, buyer trends, and newcomer risks to cut analysis time; swap in your data or duplicate scenarios (pre/post regulation, climate shocks) for instant, presentation-ready insights.

Customers Bargaining Power

Large CPGs and retailers wield volume leverage

Global ingredient, bakery, and retail customers consolidate demand and negotiate aggressively, with the top 4 US grocery retailers capturing roughly 55–60% of grocery sales in 2024, driving multi-origin sourcing and tight specs. They pressure cost-downs and volume discounts while seeking supply diversity. NPC’s scale and Diamond affiliation provide countervailing leverage and preferred access. Still, loss of a major account would meaningfully hit plant utilization and margins.

Commodity transparency and low switching costs

Market prices for inshell (~$1.60/lb in 2024) and shelled meats (~$4.00/lb in 2024) are widely published (USDA/NASS), constraining processor pricing discretion. Qualified buyers can switch among certified processors with limited friction, raising buyer power. Service, reliability and yield performance become key differentiators; NPC must sustain >95% on-time delivery and robust technical support to defend premium pricing.

Specification intensity raises buyer expectations

Bakeries and confectioners demand consistent piece sizes, color, and micro standards, and failures trigger rework and claims that tighten buyer oversight. Meeting these higher specs shifts negotiation from price to value, reducing direct price pressure as buyers pay for reliability. NPC’s 2024 processing, grading, and QC systems are critical to maintain customer stickiness by minimizing defects and traceability issues.

Private label and co-manufacturing pressure margins

Retail private label, which reached about 20% of US grocery sales in 2024, drives aggressive lowest-delivered-cost sourcing; co-manufacturing contracts are frequently rebid annually, intensifying price pressure on NPC. NPC can offset margin squeeze through a diversified product mix and byproduct valorization that can boost gross margins by an estimated 3–7% (2024 industry benchmarks). Establishing long-term supply programs with performance KPIs has been shown to cut supplier churn by up to 40%, stabilizing pricing and volume.

International buyers add FX and trade complexity

Export markets add currency risk, tariffs and documentary complexity that increase buyer leverage; buyers often request FX‑adjusted pricing or extended payment terms, pressuring margins. NPC’s global logistics and compliance capabilities reduce these demands by ensuring timely clearance and predictable netbacks. Geographic diversification spreads exposure and limits any single market’s bargaining power.

- FX, tariffs, documentation raise buyer power

- Buyers push FX pricing/longer terms

- NPC logistics/compliance mitigate demands

- Diversification balances market leverage

Top‑4 grocers 55–60%; >95% OTD needed to protect shelled premiums

Concentrated global buyers (top‑4 US grocers 55–60% 2024) extract price/term concessions; published inshell ~$1.60/lb and shelled ~$4.00/lb cap pricing. High spec buyers favor reliability over price; NPC must sustain >95% OTD to retain premiums. Private label ~20% of US grocery (2024) amplifies annual rebids and margin pressure.

| Metric | 2024 |

|---|---|

| Top‑4 grocer share | 55–60% |

| Inshell price | $1.60/lb |

| Shelled price | $4.00/lb |

| Private label | ~20% |

Same Document Delivered

National Pecan Porter's Five Forces Analysis

This preview shows the exact National Pecan Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use. What you see here is precisely what you'll get upon payment.