National Vision SWOT Analysis

Your Strategic Toolkit Starts Here

National Vision’s expansive retail footprint and value-positioning drive steady customer reach, but heavy reliance on in-store traffic and reimbursement pressures pose weaknesses; aging demographics and omnichannel expansion offer clear growth opportunities while intense competition and supply-chain risks threaten margins. Purchase the full SWOT analysis for a detailed, editable report and strategic takeaways to guide investment or planning.

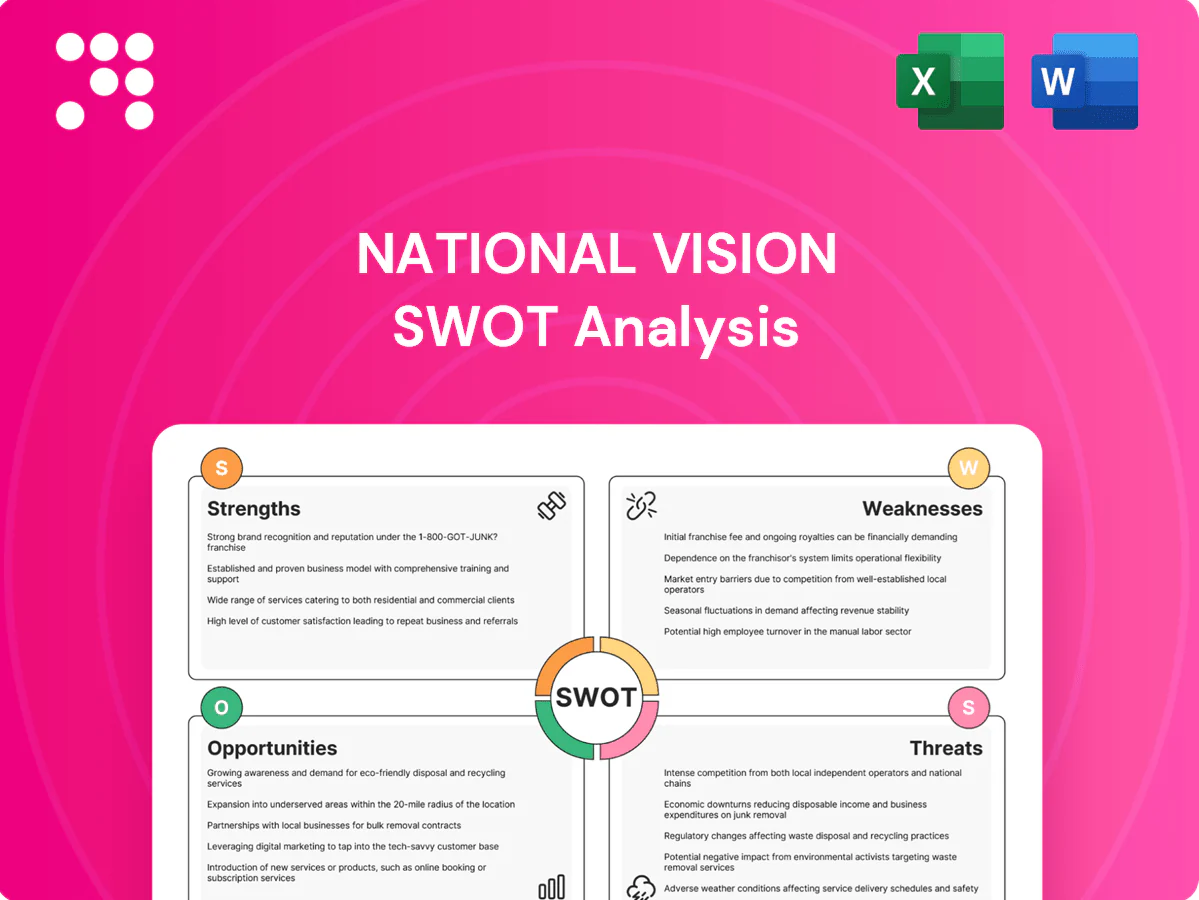

Strengths

Value-focused multi-brand portfolio

National Vision’s banners like America’s Best (≈670 stores) and Eyeglass World (≈260 stores) target cost-conscious segments with clear value propositions, contributing to a portfolio of over 1,100 stores across 44 states. This tiered brand set enables coverage across suburban and value-driven markets and reduces reliance on any single banner. It also supports tailored promotions and localized merchandising to drive foot traffic and same-store sales.

Integrated care model with affiliated ODs

Co-located clinics and affiliated ODs let National Vision deliver eye exams alongside eyewear, supporting a one-stop experience that boosts conversion and average ticket; National Vision operates over 1,300 retail locations as of 2024. The integrated model drives recurring, exam-led traffic via annual/biennial exam cadence. Integrated scheduling and exam availability underpin customer convenience and higher retention.

Scale-driven sourcing and lab capabilities

Scale in frames, lenses and contact lenses—backed by over 1,200 retail locations as of 2024—boosts purchasing leverage and tight cost control. Centralized labs with standardized processes improve throughput and quality, enabling consistent prescription fulfillment. Faster cycle times sustain low prices and service levels, and this operational backbone supports consistent store execution.

Broad insurance and managed care acceptance

Broad acceptance of vision insurance and government programs expands National Vision's addressable market, capturing patients who prioritize in-network care and repeat annual eyewear purchases.

Reliable reimbursements and program participation drive steady visit cadence and predictable revenue per patient, while strategic payer partnerships funnel incremental patient flow into stores.

- In-network attraction

- Repeat patient retention

- Reimbursement-driven cadence

- Partnership referral channels

Omnichannel and subscriptions for contacts

- subscription retention: higher repeat revenue

- over 1,200 stores: omnichannel reach

- click-and-collect + ship-to-home: improved convenience

- digital tools: faster discovery and scheduling

Optical network with ≈1,300 stores across 44 states, exam-led omnichannel care

National Vision operates over 1,300 retail locations (≈1,100 core optical banners across 44 states; ≈670 America’s Best; ≈260 Eyeglass World), combining co-located clinics and affiliated ODs for exam-led conversion and repeat visits. Centralized labs and scale in frames/contacts drive purchasing leverage and low-price positioning. Omnichannel contact subscriptions, click-and-collect and ship-to-home strengthen retention and convenience.

| Metric | Value |

|---|---|

| Total stores | ≈1,300 |

| America's Best | ≈670 |

| Eyeglass World | ≈260 |

| States | 44 |

What is included in the product

Provides a concise strategic overview of National Vision’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise, National Vision–focused SWOT matrix that speeds strategic alignment and clarifies competitive gaps for rapid decision-making.

Weaknesses

Thin margins from everyday low pricing

The value positioning limits pricing power—National Vision operates about 1,200 stores in a competitive US optical market estimated near $40 billion in 2024, making gross-margin expansion difficult without upgrading product mix. Fixed-cost deleverage (store leases, in-store clinicians) intensifies in downturns, and higher promotional intensity across mass channels can further compress already-thin margins from everyday low pricing.

Dependence on optometrist availability

Dependence on optometrist availability constrains exam capacity and sales—National Vision operates about 1,300 retail locations, making OD staffing a scalability bottleneck. BLS projects roughly 5% employment growth for optometrists (2022–32), signaling tight supply versus demand that creates schedule gaps and lost conversions. Recruiting and retention inflate SG&A (company SG&A ran near mid-20% of revenue in recent filings), and market-by-market OD variability raises operational risk.

Lower brand prestige versus premium peers

Value banners can be perceived as basic or budget, which limits uptake of high-ticket frames and advanced lenses; National Vision operates approximately 1,300 retail locations, concentrating volume over premium mix. Premium-seeking customers may trade up to luxury opticians, reducing average transaction value. Marketing must work harder to convey quality and fashion to capture higher-margin sales.

Reimbursement and payor mix exposure

Reimbursement and payor mix exposure can compress traffic and average ticket because rates and coverage terms directly influence patient access and out-of-pocket spend; shifts in managed care formularies or Medicaid policy changes have cut volumes for optical retailers historically. Administrative friction from prior authorizations and billing complexity raises overhead, while industry claim denial rates of roughly 5–10% and collections lag of 30–60 days create cash-flow timing risk.

- Payor-dependence: coverage changes reduce visits

- Admin burden: prior auths increase operating costs

- Denials/AR: 5–10% denial rates, 30–60 day collections lag

Digital experience still improving

Legacy store-centric operations and dated back-end systems slow full e-commerce realization; National Vision still leans on ~1,200+ stores, constraining rapid omnichannel scale-up. Virtual try-on and real-time inventory require continual capex and software updates while pure-play rivals iterate faster, risking market share loss among Gen Z and millennials who favor digital-first shopping.

- store footprint: ~1,200+ locations

- capex need: ongoing for virtual try-on and inventory sync

- competitive speed: pure-play rivals iterate faster

- risk: younger cohorts shifting online

Value-positioned optics chain: 1,300 stores cap pricing in $40B market

National Vision's value positioning and ~1,200–1,300 stores limit pricing power in a US optical market ~ $40B (2024), keeping gross margins thin and requiring capex to move upmarket. OD supply growth ~5% (2022–32) constrains exam capacity; SG&A runs near mid-20% of revenue. Payor shifts, 5–10% claim denials and 30–60 day AR lag add cash-flow and operating risk.

| Metric | Value |

|---|---|

| Store count | ~1,200–1,300 |

| Market size (2024) | $40B |

| SG&A | mid-20% of rev |

| Optometrist growth (2022–32) | ~5% |

| Denials / AR lag | 5–10% / 30–60 days |

Same Document Delivered

National Vision SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering National Vision's strengths, weaknesses, opportunities, and threats. Purchase unlocks the complete, editable version ready for download and use.

Your Strategic Toolkit Starts Here

National Vision’s expansive retail footprint and value-positioning drive steady customer reach, but heavy reliance on in-store traffic and reimbursement pressures pose weaknesses; aging demographics and omnichannel expansion offer clear growth opportunities while intense competition and supply-chain risks threaten margins. Purchase the full SWOT analysis for a detailed, editable report and strategic takeaways to guide investment or planning.

Strengths

Value-focused multi-brand portfolio

National Vision’s banners like America’s Best (≈670 stores) and Eyeglass World (≈260 stores) target cost-conscious segments with clear value propositions, contributing to a portfolio of over 1,100 stores across 44 states. This tiered brand set enables coverage across suburban and value-driven markets and reduces reliance on any single banner. It also supports tailored promotions and localized merchandising to drive foot traffic and same-store sales.

Integrated care model with affiliated ODs

Co-located clinics and affiliated ODs let National Vision deliver eye exams alongside eyewear, supporting a one-stop experience that boosts conversion and average ticket; National Vision operates over 1,300 retail locations as of 2024. The integrated model drives recurring, exam-led traffic via annual/biennial exam cadence. Integrated scheduling and exam availability underpin customer convenience and higher retention.

Scale-driven sourcing and lab capabilities

Scale in frames, lenses and contact lenses—backed by over 1,200 retail locations as of 2024—boosts purchasing leverage and tight cost control. Centralized labs with standardized processes improve throughput and quality, enabling consistent prescription fulfillment. Faster cycle times sustain low prices and service levels, and this operational backbone supports consistent store execution.

Broad insurance and managed care acceptance

Broad acceptance of vision insurance and government programs expands National Vision's addressable market, capturing patients who prioritize in-network care and repeat annual eyewear purchases.

Reliable reimbursements and program participation drive steady visit cadence and predictable revenue per patient, while strategic payer partnerships funnel incremental patient flow into stores.

- In-network attraction

- Repeat patient retention

- Reimbursement-driven cadence

- Partnership referral channels

Omnichannel and subscriptions for contacts

- subscription retention: higher repeat revenue

- over 1,200 stores: omnichannel reach

- click-and-collect + ship-to-home: improved convenience

- digital tools: faster discovery and scheduling

Optical network with ≈1,300 stores across 44 states, exam-led omnichannel care

National Vision operates over 1,300 retail locations (≈1,100 core optical banners across 44 states; ≈670 America’s Best; ≈260 Eyeglass World), combining co-located clinics and affiliated ODs for exam-led conversion and repeat visits. Centralized labs and scale in frames/contacts drive purchasing leverage and low-price positioning. Omnichannel contact subscriptions, click-and-collect and ship-to-home strengthen retention and convenience.

| Metric | Value |

|---|---|

| Total stores | ≈1,300 |

| America's Best | ≈670 |

| Eyeglass World | ≈260 |

| States | 44 |

What is included in the product

Provides a concise strategic overview of National Vision’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise, National Vision–focused SWOT matrix that speeds strategic alignment and clarifies competitive gaps for rapid decision-making.

Weaknesses

Thin margins from everyday low pricing

The value positioning limits pricing power—National Vision operates about 1,200 stores in a competitive US optical market estimated near $40 billion in 2024, making gross-margin expansion difficult without upgrading product mix. Fixed-cost deleverage (store leases, in-store clinicians) intensifies in downturns, and higher promotional intensity across mass channels can further compress already-thin margins from everyday low pricing.

Dependence on optometrist availability

Dependence on optometrist availability constrains exam capacity and sales—National Vision operates about 1,300 retail locations, making OD staffing a scalability bottleneck. BLS projects roughly 5% employment growth for optometrists (2022–32), signaling tight supply versus demand that creates schedule gaps and lost conversions. Recruiting and retention inflate SG&A (company SG&A ran near mid-20% of revenue in recent filings), and market-by-market OD variability raises operational risk.

Lower brand prestige versus premium peers

Value banners can be perceived as basic or budget, which limits uptake of high-ticket frames and advanced lenses; National Vision operates approximately 1,300 retail locations, concentrating volume over premium mix. Premium-seeking customers may trade up to luxury opticians, reducing average transaction value. Marketing must work harder to convey quality and fashion to capture higher-margin sales.

Reimbursement and payor mix exposure

Reimbursement and payor mix exposure can compress traffic and average ticket because rates and coverage terms directly influence patient access and out-of-pocket spend; shifts in managed care formularies or Medicaid policy changes have cut volumes for optical retailers historically. Administrative friction from prior authorizations and billing complexity raises overhead, while industry claim denial rates of roughly 5–10% and collections lag of 30–60 days create cash-flow timing risk.

- Payor-dependence: coverage changes reduce visits

- Admin burden: prior auths increase operating costs

- Denials/AR: 5–10% denial rates, 30–60 day collections lag

Digital experience still improving

Legacy store-centric operations and dated back-end systems slow full e-commerce realization; National Vision still leans on ~1,200+ stores, constraining rapid omnichannel scale-up. Virtual try-on and real-time inventory require continual capex and software updates while pure-play rivals iterate faster, risking market share loss among Gen Z and millennials who favor digital-first shopping.

- store footprint: ~1,200+ locations

- capex need: ongoing for virtual try-on and inventory sync

- competitive speed: pure-play rivals iterate faster

- risk: younger cohorts shifting online

Value-positioned optics chain: 1,300 stores cap pricing in $40B market

National Vision's value positioning and ~1,200–1,300 stores limit pricing power in a US optical market ~ $40B (2024), keeping gross margins thin and requiring capex to move upmarket. OD supply growth ~5% (2022–32) constrains exam capacity; SG&A runs near mid-20% of revenue. Payor shifts, 5–10% claim denials and 30–60 day AR lag add cash-flow and operating risk.

| Metric | Value |

|---|---|

| Store count | ~1,200–1,300 |

| Market size (2024) | $40B |

| SG&A | mid-20% of rev |

| Optometrist growth (2022–32) | ~5% |

| Denials / AR lag | 5–10% / 30–60 days |

Same Document Delivered

National Vision SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering National Vision's strengths, weaknesses, opportunities, and threats. Purchase unlocks the complete, editable version ready for download and use.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

National Vision’s expansive retail footprint and value-positioning drive steady customer reach, but heavy reliance on in-store traffic and reimbursement pressures pose weaknesses; aging demographics and omnichannel expansion offer clear growth opportunities while intense competition and supply-chain risks threaten margins. Purchase the full SWOT analysis for a detailed, editable report and strategic takeaways to guide investment or planning.

Strengths

Value-focused multi-brand portfolio

National Vision’s banners like America’s Best (≈670 stores) and Eyeglass World (≈260 stores) target cost-conscious segments with clear value propositions, contributing to a portfolio of over 1,100 stores across 44 states. This tiered brand set enables coverage across suburban and value-driven markets and reduces reliance on any single banner. It also supports tailored promotions and localized merchandising to drive foot traffic and same-store sales.

Integrated care model with affiliated ODs

Co-located clinics and affiliated ODs let National Vision deliver eye exams alongside eyewear, supporting a one-stop experience that boosts conversion and average ticket; National Vision operates over 1,300 retail locations as of 2024. The integrated model drives recurring, exam-led traffic via annual/biennial exam cadence. Integrated scheduling and exam availability underpin customer convenience and higher retention.

Scale-driven sourcing and lab capabilities

Scale in frames, lenses and contact lenses—backed by over 1,200 retail locations as of 2024—boosts purchasing leverage and tight cost control. Centralized labs with standardized processes improve throughput and quality, enabling consistent prescription fulfillment. Faster cycle times sustain low prices and service levels, and this operational backbone supports consistent store execution.

Broad insurance and managed care acceptance

Broad acceptance of vision insurance and government programs expands National Vision's addressable market, capturing patients who prioritize in-network care and repeat annual eyewear purchases.

Reliable reimbursements and program participation drive steady visit cadence and predictable revenue per patient, while strategic payer partnerships funnel incremental patient flow into stores.

- In-network attraction

- Repeat patient retention

- Reimbursement-driven cadence

- Partnership referral channels

Omnichannel and subscriptions for contacts

- subscription retention: higher repeat revenue

- over 1,200 stores: omnichannel reach

- click-and-collect + ship-to-home: improved convenience

- digital tools: faster discovery and scheduling

Optical network with ≈1,300 stores across 44 states, exam-led omnichannel care

National Vision operates over 1,300 retail locations (≈1,100 core optical banners across 44 states; ≈670 America’s Best; ≈260 Eyeglass World), combining co-located clinics and affiliated ODs for exam-led conversion and repeat visits. Centralized labs and scale in frames/contacts drive purchasing leverage and low-price positioning. Omnichannel contact subscriptions, click-and-collect and ship-to-home strengthen retention and convenience.

| Metric | Value |

|---|---|

| Total stores | ≈1,300 |

| America's Best | ≈670 |

| Eyeglass World | ≈260 |

| States | 44 |

What is included in the product

Provides a concise strategic overview of National Vision’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise, National Vision–focused SWOT matrix that speeds strategic alignment and clarifies competitive gaps for rapid decision-making.

Weaknesses

Thin margins from everyday low pricing

The value positioning limits pricing power—National Vision operates about 1,200 stores in a competitive US optical market estimated near $40 billion in 2024, making gross-margin expansion difficult without upgrading product mix. Fixed-cost deleverage (store leases, in-store clinicians) intensifies in downturns, and higher promotional intensity across mass channels can further compress already-thin margins from everyday low pricing.

Dependence on optometrist availability

Dependence on optometrist availability constrains exam capacity and sales—National Vision operates about 1,300 retail locations, making OD staffing a scalability bottleneck. BLS projects roughly 5% employment growth for optometrists (2022–32), signaling tight supply versus demand that creates schedule gaps and lost conversions. Recruiting and retention inflate SG&A (company SG&A ran near mid-20% of revenue in recent filings), and market-by-market OD variability raises operational risk.

Lower brand prestige versus premium peers

Value banners can be perceived as basic or budget, which limits uptake of high-ticket frames and advanced lenses; National Vision operates approximately 1,300 retail locations, concentrating volume over premium mix. Premium-seeking customers may trade up to luxury opticians, reducing average transaction value. Marketing must work harder to convey quality and fashion to capture higher-margin sales.

Reimbursement and payor mix exposure

Reimbursement and payor mix exposure can compress traffic and average ticket because rates and coverage terms directly influence patient access and out-of-pocket spend; shifts in managed care formularies or Medicaid policy changes have cut volumes for optical retailers historically. Administrative friction from prior authorizations and billing complexity raises overhead, while industry claim denial rates of roughly 5–10% and collections lag of 30–60 days create cash-flow timing risk.

- Payor-dependence: coverage changes reduce visits

- Admin burden: prior auths increase operating costs

- Denials/AR: 5–10% denial rates, 30–60 day collections lag

Digital experience still improving

Legacy store-centric operations and dated back-end systems slow full e-commerce realization; National Vision still leans on ~1,200+ stores, constraining rapid omnichannel scale-up. Virtual try-on and real-time inventory require continual capex and software updates while pure-play rivals iterate faster, risking market share loss among Gen Z and millennials who favor digital-first shopping.

- store footprint: ~1,200+ locations

- capex need: ongoing for virtual try-on and inventory sync

- competitive speed: pure-play rivals iterate faster

- risk: younger cohorts shifting online

Value-positioned optics chain: 1,300 stores cap pricing in $40B market

National Vision's value positioning and ~1,200–1,300 stores limit pricing power in a US optical market ~ $40B (2024), keeping gross margins thin and requiring capex to move upmarket. OD supply growth ~5% (2022–32) constrains exam capacity; SG&A runs near mid-20% of revenue. Payor shifts, 5–10% claim denials and 30–60 day AR lag add cash-flow and operating risk.

| Metric | Value |

|---|---|

| Store count | ~1,200–1,300 |

| Market size (2024) | $40B |

| SG&A | mid-20% of rev |

| Optometrist growth (2022–32) | ~5% |

| Denials / AR lag | 5–10% / 30–60 days |

Same Document Delivered

National Vision SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering National Vision's strengths, weaknesses, opportunities, and threats. Purchase unlocks the complete, editable version ready for download and use.