NatWest Group SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

NatWest Group’s resilient retail franchise, strong digital expansion, and solid capital position contrast with legacy cost pressures, regulatory scrutiny, and exposure to UK market cyclicality. Want the full picture—purchase the complete SWOT analysis for a research-backed, editable report and Excel tools to guide strategic decisions and investments.

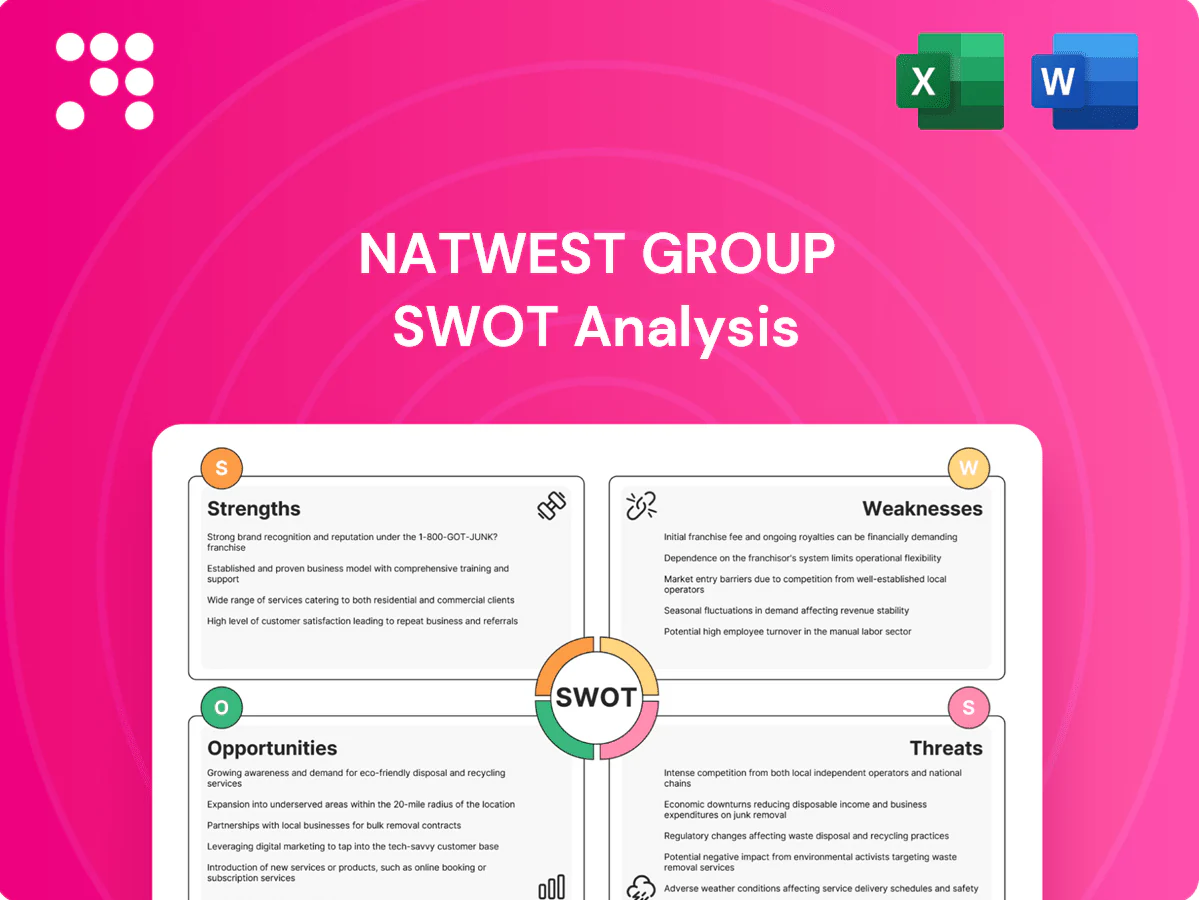

Strengths

Leading UK franchise

NatWest is a leading UK retail and commercial bank, with roughly 15% share of current accounts, about 16% share of mortgage balances and c.13% share of SME lending, underpinning strong scale across core markets. Its multichannel distribution—2,000+ branches, extensive digital platforms and dedicated relationship managers—delivers broad customer access. A stable, granular deposit base of c.£350bn supports funding resilience and gives pricing power to drive cross-sell.

Trusted core brands

NatWest Group's core brands—NatWest, Royal Bank of Scotland (founded 1727) and Ulster Bank (NI)—hold strong brand equity across retail, SME and corporate segments, supporting c.19 million customers. Long-standing relationships boost retention and lower acquisition costs through high lifetime value and cross-sell. Well-known brands facilitate corporate and institutional mandates, helping win mandates and capital markets roles. Brand strength underpins resilient fee income streams.

Diverse product suite

NatWest Group offers a full spectrum from retail and commercial banking to private banking and corporate finance, serving c.19 million customers (2024) across the UK and Ireland. Diversified revenue streams from mortgages, SME lending, wealth and markets reduce volatility across interest-rate and credit cycles. End-to-end product chains enable lifecycle cross-sell, delivering holistic solutions for individuals, SMEs and institutions.

Robust capital & liquidity

NatWest Group reports a strong CET1 ratio of 15.6%, a leverage ratio around 4.9% and an LCR near 190% (latest 2024/25 disclosures), comfortably above regulatory minima; these buffers support organic growth, buybacks/dividends and absorb credit shocks, underpinned by disciplined risk management and the ring-fenced UK retail structure.

- CET1 15.6%

- Leverage ~4.9%

- LCR ~190%

- Ring-fenced structure & disciplined risk

Digital at scale

Digital at scale: NatWest’s high mobile adoption (c.10m mobile customers) and 24/7 self-service plus efficient digital onboarding drive lower cost-to-serve and data-driven personalization; secure payments and instant lending decisions improve UX and act as differentiators, yielding lower churn and higher engagement.

- mobile: c.10m

- 24/7 self-service

- instant decisions

UK banking leader - c.19m customers, £350bn deposits

Market leader in UK retail/commercial banking with c.19m customers, ≈15% current-account share, ≈16% mortgage share and ≈13% SME lending share, supporting scale and cross-sell. Stable deposit base c.£350bn, CET1 15.6%, leverage ~4.9% and LCR ~190% provide strong capital/funding resilience. Digital at scale: c.10m mobile users, 24/7 self‑service and instant decisions lowering cost-to-serve.

| Metric | Value |

|---|---|

| Customers | c.19m |

| Deposits | c.£350bn |

| CET1 | 15.6% |

| LCR | ~190% |

| Mobile users | c.10m |

What is included in the product

Delivers a strategic overview of NatWest Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix for NatWest Group to quickly pinpoint strategic risks and opportunities, relieving analysis bottlenecks and enabling faster, aligned decision-making.

Weaknesses

UK concentration

NatWest remains heavily UK‑focused, with a mortgage book around £200bn within a UK mortgage market of roughly £1.6trn (2024), concentrating revenue and credit risk in the UK housing cycle. Limited geographic diversification versus global peers raises sensitivity to UK consumer confidence, Bank Rate (~5.25% mid‑2025) and house‑price swings, risking volatile earnings during domestic downturns.

Legacy IT complexity

Multi-decade core systems, tangled integration layers and accumulated technical debt force NatWest to absorb elevated change costs and higher operational risk during modernization, slowing feature rollout compared with nimble fintechs. Complexity has contributed to periodic outages and disproportionate remediation spend, attracting intensified regulatory scrutiny and requiring significant governance and capital allocation to stabilize platforms.

Residual reputational drag

Residual reputational drag stems from legacy issues dating back to the 2008 financial crisis, when RBS required a UK government bailout of about 45.5 billion pounds, and subsequent conduct matters have kept scrutiny elevated. Trust rebuilding remains slow among corporate and retail clients, sustaining higher regulatory intensity and adverse brand perception. That reputational cost encourages a cautious risk appetite, which can limit lending growth and margin expansion.

Margin sensitivity

Margin sensitivity: NatWest faces pressure on net interest margin from intensified competition, deposit migration into higher-rate savings and necessary savings repricing amid a Bank of England base rate near 5.25%, while caps on overdraft/fees and ring-fencing limit non‑interest income flexibility.

Mortgage price wars have compressed spreads, and earnings remain highly sensitive to the rate path and deposit beta—industry deposit betas seen around 40–60% amplify NIM volatility.

- Deposit migration increases funding costs

- Overdraft/fee caps and ring-fencing constrain revenues

- Mortgage spreads compressed by price competition

- Earnings sensitive to rate path and ~40–60% deposit beta

Cost base vs challengers

NatWest's extensive branch network and legacy compliance frameworks drive higher fixed costs compared with digital-only challengers that bypass physical overheads, producing materially higher unit costs in operations and customer servicing and pressuring margins. Ongoing efficiency programmes are required to protect RoE targets, forcing trade-offs between investing in growth initiatives and simplifying the operating model.

- branch footprint: hundreds of locations

- higher unit costs vs digital peers

- efficiency programmes needed to sustain RoE

- investment trade-off: growth vs simplification

UK-centric lender with ~£200bn mortgage book: rate sensitivity, legacy tech and reputational drag

NatWest is UK‑centric with ~£200bn mortgage book vs £1.6trn UK market (2024), concentrating credit/revenue risk to BOE rate (~5.25% mid‑2025) and house prices; legacy IT/tech debt raises change costs, outages and remediation spend; residual reputational drag from the £45.5bn RBS bailout and conduct issues sustains higher regulatory intensity; large branch footprint and fee caps pressure margins and RoE.

| Metric | Value |

|---|---|

| Mortgage book | ~£200bn (2024) |

| UK mortgage market | £1.6trn (2024) |

| BoE base rate | ~5.25% (mid‑2025) |

| RBS bailout | £45.5bn |

Preview Before You Purchase

NatWest Group SWOT Analysis

This is the actual SWOT analysis document for NatWest Group you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the entire in-depth, editable version. You're viewing a live preview of the real file, ready to download after checkout.

Dive Deeper Into the Company’s Strategic Blueprint

NatWest Group’s resilient retail franchise, strong digital expansion, and solid capital position contrast with legacy cost pressures, regulatory scrutiny, and exposure to UK market cyclicality. Want the full picture—purchase the complete SWOT analysis for a research-backed, editable report and Excel tools to guide strategic decisions and investments.

Strengths

Leading UK franchise

NatWest is a leading UK retail and commercial bank, with roughly 15% share of current accounts, about 16% share of mortgage balances and c.13% share of SME lending, underpinning strong scale across core markets. Its multichannel distribution—2,000+ branches, extensive digital platforms and dedicated relationship managers—delivers broad customer access. A stable, granular deposit base of c.£350bn supports funding resilience and gives pricing power to drive cross-sell.

Trusted core brands

NatWest Group's core brands—NatWest, Royal Bank of Scotland (founded 1727) and Ulster Bank (NI)—hold strong brand equity across retail, SME and corporate segments, supporting c.19 million customers. Long-standing relationships boost retention and lower acquisition costs through high lifetime value and cross-sell. Well-known brands facilitate corporate and institutional mandates, helping win mandates and capital markets roles. Brand strength underpins resilient fee income streams.

Diverse product suite

NatWest Group offers a full spectrum from retail and commercial banking to private banking and corporate finance, serving c.19 million customers (2024) across the UK and Ireland. Diversified revenue streams from mortgages, SME lending, wealth and markets reduce volatility across interest-rate and credit cycles. End-to-end product chains enable lifecycle cross-sell, delivering holistic solutions for individuals, SMEs and institutions.

Robust capital & liquidity

NatWest Group reports a strong CET1 ratio of 15.6%, a leverage ratio around 4.9% and an LCR near 190% (latest 2024/25 disclosures), comfortably above regulatory minima; these buffers support organic growth, buybacks/dividends and absorb credit shocks, underpinned by disciplined risk management and the ring-fenced UK retail structure.

- CET1 15.6%

- Leverage ~4.9%

- LCR ~190%

- Ring-fenced structure & disciplined risk

Digital at scale

Digital at scale: NatWest’s high mobile adoption (c.10m mobile customers) and 24/7 self-service plus efficient digital onboarding drive lower cost-to-serve and data-driven personalization; secure payments and instant lending decisions improve UX and act as differentiators, yielding lower churn and higher engagement.

- mobile: c.10m

- 24/7 self-service

- instant decisions

UK banking leader - c.19m customers, £350bn deposits

Market leader in UK retail/commercial banking with c.19m customers, ≈15% current-account share, ≈16% mortgage share and ≈13% SME lending share, supporting scale and cross-sell. Stable deposit base c.£350bn, CET1 15.6%, leverage ~4.9% and LCR ~190% provide strong capital/funding resilience. Digital at scale: c.10m mobile users, 24/7 self‑service and instant decisions lowering cost-to-serve.

| Metric | Value |

|---|---|

| Customers | c.19m |

| Deposits | c.£350bn |

| CET1 | 15.6% |

| LCR | ~190% |

| Mobile users | c.10m |

What is included in the product

Delivers a strategic overview of NatWest Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix for NatWest Group to quickly pinpoint strategic risks and opportunities, relieving analysis bottlenecks and enabling faster, aligned decision-making.

Weaknesses

UK concentration

NatWest remains heavily UK‑focused, with a mortgage book around £200bn within a UK mortgage market of roughly £1.6trn (2024), concentrating revenue and credit risk in the UK housing cycle. Limited geographic diversification versus global peers raises sensitivity to UK consumer confidence, Bank Rate (~5.25% mid‑2025) and house‑price swings, risking volatile earnings during domestic downturns.

Legacy IT complexity

Multi-decade core systems, tangled integration layers and accumulated technical debt force NatWest to absorb elevated change costs and higher operational risk during modernization, slowing feature rollout compared with nimble fintechs. Complexity has contributed to periodic outages and disproportionate remediation spend, attracting intensified regulatory scrutiny and requiring significant governance and capital allocation to stabilize platforms.

Residual reputational drag

Residual reputational drag stems from legacy issues dating back to the 2008 financial crisis, when RBS required a UK government bailout of about 45.5 billion pounds, and subsequent conduct matters have kept scrutiny elevated. Trust rebuilding remains slow among corporate and retail clients, sustaining higher regulatory intensity and adverse brand perception. That reputational cost encourages a cautious risk appetite, which can limit lending growth and margin expansion.

Margin sensitivity

Margin sensitivity: NatWest faces pressure on net interest margin from intensified competition, deposit migration into higher-rate savings and necessary savings repricing amid a Bank of England base rate near 5.25%, while caps on overdraft/fees and ring-fencing limit non‑interest income flexibility.

Mortgage price wars have compressed spreads, and earnings remain highly sensitive to the rate path and deposit beta—industry deposit betas seen around 40–60% amplify NIM volatility.

- Deposit migration increases funding costs

- Overdraft/fee caps and ring-fencing constrain revenues

- Mortgage spreads compressed by price competition

- Earnings sensitive to rate path and ~40–60% deposit beta

Cost base vs challengers

NatWest's extensive branch network and legacy compliance frameworks drive higher fixed costs compared with digital-only challengers that bypass physical overheads, producing materially higher unit costs in operations and customer servicing and pressuring margins. Ongoing efficiency programmes are required to protect RoE targets, forcing trade-offs between investing in growth initiatives and simplifying the operating model.

- branch footprint: hundreds of locations

- higher unit costs vs digital peers

- efficiency programmes needed to sustain RoE

- investment trade-off: growth vs simplification

UK-centric lender with ~£200bn mortgage book: rate sensitivity, legacy tech and reputational drag

NatWest is UK‑centric with ~£200bn mortgage book vs £1.6trn UK market (2024), concentrating credit/revenue risk to BOE rate (~5.25% mid‑2025) and house prices; legacy IT/tech debt raises change costs, outages and remediation spend; residual reputational drag from the £45.5bn RBS bailout and conduct issues sustains higher regulatory intensity; large branch footprint and fee caps pressure margins and RoE.

| Metric | Value |

|---|---|

| Mortgage book | ~£200bn (2024) |

| UK mortgage market | £1.6trn (2024) |

| BoE base rate | ~5.25% (mid‑2025) |

| RBS bailout | £45.5bn |

Preview Before You Purchase

NatWest Group SWOT Analysis

This is the actual SWOT analysis document for NatWest Group you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the entire in-depth, editable version. You're viewing a live preview of the real file, ready to download after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

NatWest Group’s resilient retail franchise, strong digital expansion, and solid capital position contrast with legacy cost pressures, regulatory scrutiny, and exposure to UK market cyclicality. Want the full picture—purchase the complete SWOT analysis for a research-backed, editable report and Excel tools to guide strategic decisions and investments.

Strengths

Leading UK franchise

NatWest is a leading UK retail and commercial bank, with roughly 15% share of current accounts, about 16% share of mortgage balances and c.13% share of SME lending, underpinning strong scale across core markets. Its multichannel distribution—2,000+ branches, extensive digital platforms and dedicated relationship managers—delivers broad customer access. A stable, granular deposit base of c.£350bn supports funding resilience and gives pricing power to drive cross-sell.

Trusted core brands

NatWest Group's core brands—NatWest, Royal Bank of Scotland (founded 1727) and Ulster Bank (NI)—hold strong brand equity across retail, SME and corporate segments, supporting c.19 million customers. Long-standing relationships boost retention and lower acquisition costs through high lifetime value and cross-sell. Well-known brands facilitate corporate and institutional mandates, helping win mandates and capital markets roles. Brand strength underpins resilient fee income streams.

Diverse product suite

NatWest Group offers a full spectrum from retail and commercial banking to private banking and corporate finance, serving c.19 million customers (2024) across the UK and Ireland. Diversified revenue streams from mortgages, SME lending, wealth and markets reduce volatility across interest-rate and credit cycles. End-to-end product chains enable lifecycle cross-sell, delivering holistic solutions for individuals, SMEs and institutions.

Robust capital & liquidity

NatWest Group reports a strong CET1 ratio of 15.6%, a leverage ratio around 4.9% and an LCR near 190% (latest 2024/25 disclosures), comfortably above regulatory minima; these buffers support organic growth, buybacks/dividends and absorb credit shocks, underpinned by disciplined risk management and the ring-fenced UK retail structure.

- CET1 15.6%

- Leverage ~4.9%

- LCR ~190%

- Ring-fenced structure & disciplined risk

Digital at scale

Digital at scale: NatWest’s high mobile adoption (c.10m mobile customers) and 24/7 self-service plus efficient digital onboarding drive lower cost-to-serve and data-driven personalization; secure payments and instant lending decisions improve UX and act as differentiators, yielding lower churn and higher engagement.

- mobile: c.10m

- 24/7 self-service

- instant decisions

UK banking leader - c.19m customers, £350bn deposits

Market leader in UK retail/commercial banking with c.19m customers, ≈15% current-account share, ≈16% mortgage share and ≈13% SME lending share, supporting scale and cross-sell. Stable deposit base c.£350bn, CET1 15.6%, leverage ~4.9% and LCR ~190% provide strong capital/funding resilience. Digital at scale: c.10m mobile users, 24/7 self‑service and instant decisions lowering cost-to-serve.

| Metric | Value |

|---|---|

| Customers | c.19m |

| Deposits | c.£350bn |

| CET1 | 15.6% |

| LCR | ~190% |

| Mobile users | c.10m |

What is included in the product

Delivers a strategic overview of NatWest Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix for NatWest Group to quickly pinpoint strategic risks and opportunities, relieving analysis bottlenecks and enabling faster, aligned decision-making.

Weaknesses

UK concentration

NatWest remains heavily UK‑focused, with a mortgage book around £200bn within a UK mortgage market of roughly £1.6trn (2024), concentrating revenue and credit risk in the UK housing cycle. Limited geographic diversification versus global peers raises sensitivity to UK consumer confidence, Bank Rate (~5.25% mid‑2025) and house‑price swings, risking volatile earnings during domestic downturns.

Legacy IT complexity

Multi-decade core systems, tangled integration layers and accumulated technical debt force NatWest to absorb elevated change costs and higher operational risk during modernization, slowing feature rollout compared with nimble fintechs. Complexity has contributed to periodic outages and disproportionate remediation spend, attracting intensified regulatory scrutiny and requiring significant governance and capital allocation to stabilize platforms.

Residual reputational drag

Residual reputational drag stems from legacy issues dating back to the 2008 financial crisis, when RBS required a UK government bailout of about 45.5 billion pounds, and subsequent conduct matters have kept scrutiny elevated. Trust rebuilding remains slow among corporate and retail clients, sustaining higher regulatory intensity and adverse brand perception. That reputational cost encourages a cautious risk appetite, which can limit lending growth and margin expansion.

Margin sensitivity

Margin sensitivity: NatWest faces pressure on net interest margin from intensified competition, deposit migration into higher-rate savings and necessary savings repricing amid a Bank of England base rate near 5.25%, while caps on overdraft/fees and ring-fencing limit non‑interest income flexibility.

Mortgage price wars have compressed spreads, and earnings remain highly sensitive to the rate path and deposit beta—industry deposit betas seen around 40–60% amplify NIM volatility.

- Deposit migration increases funding costs

- Overdraft/fee caps and ring-fencing constrain revenues

- Mortgage spreads compressed by price competition

- Earnings sensitive to rate path and ~40–60% deposit beta

Cost base vs challengers

NatWest's extensive branch network and legacy compliance frameworks drive higher fixed costs compared with digital-only challengers that bypass physical overheads, producing materially higher unit costs in operations and customer servicing and pressuring margins. Ongoing efficiency programmes are required to protect RoE targets, forcing trade-offs between investing in growth initiatives and simplifying the operating model.

- branch footprint: hundreds of locations

- higher unit costs vs digital peers

- efficiency programmes needed to sustain RoE

- investment trade-off: growth vs simplification

UK-centric lender with ~£200bn mortgage book: rate sensitivity, legacy tech and reputational drag

NatWest is UK‑centric with ~£200bn mortgage book vs £1.6trn UK market (2024), concentrating credit/revenue risk to BOE rate (~5.25% mid‑2025) and house prices; legacy IT/tech debt raises change costs, outages and remediation spend; residual reputational drag from the £45.5bn RBS bailout and conduct issues sustains higher regulatory intensity; large branch footprint and fee caps pressure margins and RoE.

| Metric | Value |

|---|---|

| Mortgage book | ~£200bn (2024) |

| UK mortgage market | £1.6trn (2024) |

| BoE base rate | ~5.25% (mid‑2025) |

| RBS bailout | £45.5bn |

Preview Before You Purchase

NatWest Group SWOT Analysis

This is the actual SWOT analysis document for NatWest Group you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the entire in-depth, editable version. You're viewing a live preview of the real file, ready to download after checkout.