Nautilus Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Nautilus faces shifting competitive currents—moderate supplier leverage, evolving buyer expectations, and growing substitute threats as fitness tech and streaming content expand. This snapshot highlights key pressures and strategic implications for management and investors. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable recommendations.

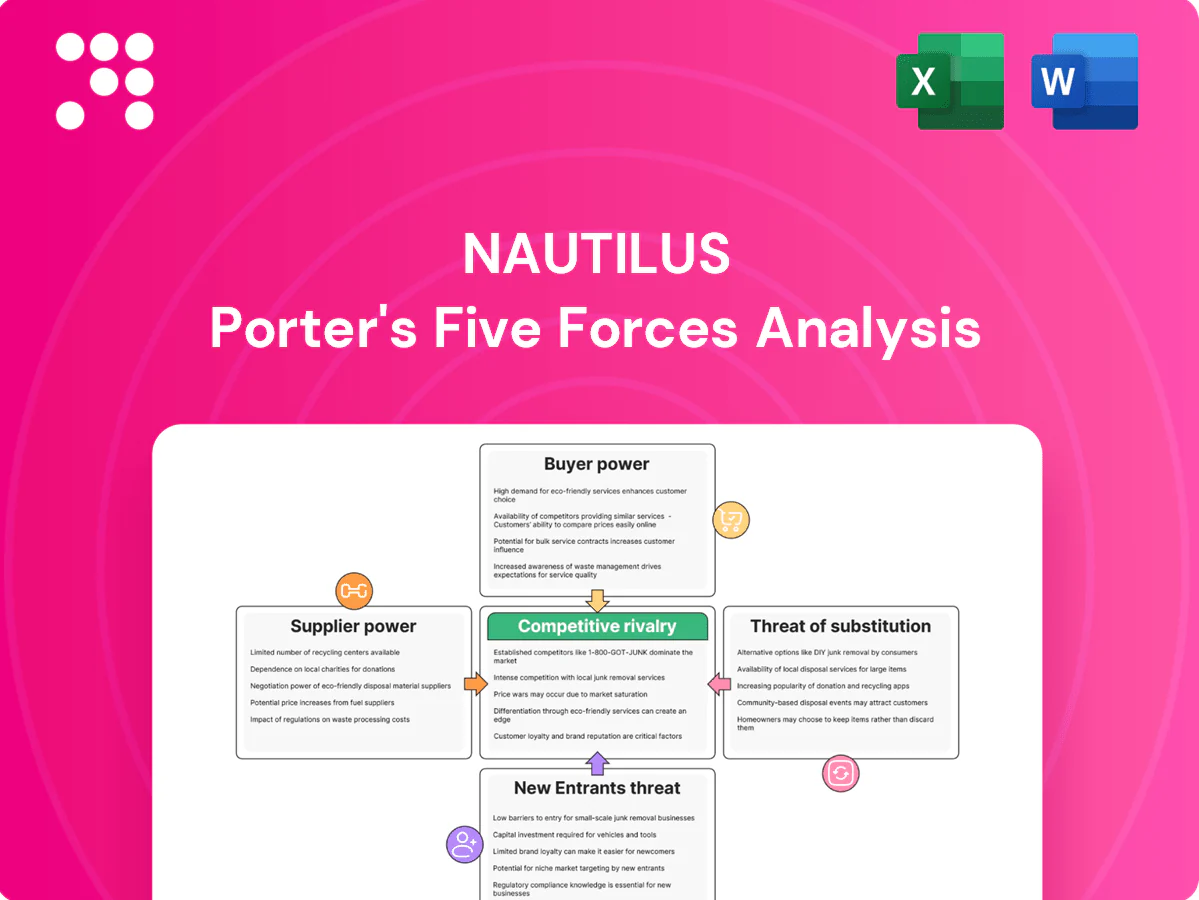

Suppliers Bargaining Power

Diverse component sources

Core parts such as steel frames, motors, electronics, plastics and consoles are sourced widely from global suppliers—limiting concentration risk as major manufacturing hubs in Asia and North America supply the bulk of these components. Alternative vendors across Asia and North America enable competitive bids, though firmware-integrated consoles and IoT modules narrow viable suppliers to a handful. Dual-sourcing and vendor qualification typically add months to lead times and can raise procurement costs by several percent.

Specialized electronics reliance

Connected-fitness products rely on sensors, displays, chips and connectivity modules that in 2024 faced constrained supply with component lead times commonly 12–20 weeks, raising supplier leverage. Firmware integration and regulatory certifications create high switching friction and lock-in when suppliers customize parts to Nautilus specs. Long lead times force higher inventory or pay expedite fees, squeezing margins and raising working-capital needs.

Contract manufacturing and tooling

Much Nautilus equipment is made by contract manufacturers, offering production flexibility but embedding significant tooling and mold commitments; switching factories requires retooling, QA validation and potential weeks of downtime. These factors create moderate supplier power via switching costs. Long-term supply agreements can reduce near-term risk, though they increase strategic lock-in over time.

Logistics and tariffs exposure

Ocean freight, port congestion and trade tariffs materially drive landed cost; Section 301 tariffs on China remain as high as 25%, and carriers/3PLs obtain leverage during capacity tightness, pushing spot premiums and rollovers. Diversifying lanes and nearshoring cut exposure but require quarters to years to implement. Fuel surcharges and compliance fees create additional cost variability.

- Tariffs: up to 25% Section 301

- Carrier leverage: spot/contract premium risk

- Mitigation: lane diversification, nearshoring (time‑consuming)

- Cost drivers: fuel surcharges, compliance fees

Brand-critical quality control

Equipment safety and durability define Nautilus brand value, making high-spec suppliers indispensable and elevating supplier bargaining power as failures drive returns and warranty costs that erode margins.

Dependence on proven vendors increased in 2024 after intensified quality scrutiny; vendor audits and strict SLAs are used to re-balance leverage and contain recall risk.

- High-spec suppliers: critical

- Failures → higher returns/warranty costs

- 2024: intensified vendor audits and SLAs

Dispersed parts, concentrated firmware — 12–20w, 25%

Suppliers of commoditized parts are broadly dispersed across Asia and North America, limiting concentration risk, but firmware-integrated consoles and IoT modules concentrate bargaining power in a few vendors. 2024 lead times of 12–20 weeks and Section 301 tariffs up to 25% raise costs and working-capital needs. Contract manufacturers and tooling lock-in create moderate switching costs and strategic supplier leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| Component lead times | 12–20 weeks | Inventory/cost pressure |

| Tariffs | Section 301 up to 25% | Higher landed cost |

| Firmware/IoT suppliers | Few viable vendors | Higher supplier power |

What is included in the product

Tailored Porter's Five Forces analysis for Nautilus that uncovers the key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. Identifies disruptive substitutes, emerging threats, and incumbent advantages with strategic commentary suitable for investor decks or internal strategy.

One-sheet Nautilus Porter's Five Forces simplifies strategic pain points with a clean, customizable summary and instant spider chart visualization for quick decision-making. Swap in your own data, duplicate scenarios, and integrate into decks or dashboards without macros—ready for non-finance users and boardroom use.

Customers Bargaining Power

Highly price-sensitive consumers

Highly price-sensitive home-fitness buyers compare across brands and models via transparent online pricing—about 70% of shoppers check multiple sites—while promotions, BNPL and seasonal discounts heavily influence timing; low switching costs raise buyer leverage, and reviews or limited-time deals can rapidly swing perceived value and purchase decisions.

Retail and marketplace leverage

Large channels like Amazon and specialty retailers command shelf space and search placement—Amazon held about 38% of US e-commerce in 2024—letting them pressure margins via typical ~15% referral fees, returns policies and co-op marketing. Online return rates hover near 16%, so losing a key channel hits volume and visibility hard; DTC eases but dependence stays meaningful.

Content and subscription churn

Digital fitness buyers can cancel or switch apps with minimal friction; industry data in 2024 shows typical monthly churn of about 5–7%, implying annualized churn often exceeds 40%. Content freshness and tight hardware integration (connected bikes/treadmills) materially affect retention and perceived value. High churn amplifies buyer power on pricing and features, while bundling JRNY with Nautilus hardware can partially reduce switching by increasing switching costs and stickiness.

Information-rich purchase journey

Reviews, influencer content and comparison sites have eroded information asymmetry; a 2024 survey found 92% of consumers consult reviews before buying, so defects or design trade-offs are spotted quickly. That transparency compresses pricing power and raises switch risk, making reputation management and rapid product iteration essential for Nautilus.

- Reviews: 92% consult (2024)

- Effect: compressed pricing power

- Priority: reputation management

- Priority: rapid iteration

Post-pandemic demand volatility

- Shift volatility: at-home vs gym

- Buyer leverage: discounts up to 30% (2024)

- Inventory risk: overhang increases bargaining power

- Mitigation: forecasting + dynamic pricing

Customers hold leverage: 92% read reviews, 70% compare; 30% discounts compress margins

Customers hold strong bargaining power: 70% compare multiple sites and 92% consult reviews, driving price sensitivity and rapid switching; Amazon’s 38% US e-commerce share (2024) and ~15% referral fees pressure margins. Returns ~16% and monthly churn 5–7% (annual >40%) amplify leverage; discounts reached 30% in 2024, while e‑commerce demand sat ~25% above 2019.

| Metric | 2024 Value |

|---|---|

| Compare multiple sites | 70% |

| Consult reviews | 92% |

| Amazon e‑commerce share | 38% |

| Return rate | ~16% |

| Monthly churn | 5–7% |

| Peak discounts | ~30% |

| E‑commerce vs 2019 | +25% |

Preview Before You Purchase

Nautilus Porter's Five Forces Analysis

This preview shows the exact Nautilus Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.

From Overview to Strategy Blueprint

Nautilus faces shifting competitive currents—moderate supplier leverage, evolving buyer expectations, and growing substitute threats as fitness tech and streaming content expand. This snapshot highlights key pressures and strategic implications for management and investors. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Diverse component sources

Core parts such as steel frames, motors, electronics, plastics and consoles are sourced widely from global suppliers—limiting concentration risk as major manufacturing hubs in Asia and North America supply the bulk of these components. Alternative vendors across Asia and North America enable competitive bids, though firmware-integrated consoles and IoT modules narrow viable suppliers to a handful. Dual-sourcing and vendor qualification typically add months to lead times and can raise procurement costs by several percent.

Specialized electronics reliance

Connected-fitness products rely on sensors, displays, chips and connectivity modules that in 2024 faced constrained supply with component lead times commonly 12–20 weeks, raising supplier leverage. Firmware integration and regulatory certifications create high switching friction and lock-in when suppliers customize parts to Nautilus specs. Long lead times force higher inventory or pay expedite fees, squeezing margins and raising working-capital needs.

Contract manufacturing and tooling

Much Nautilus equipment is made by contract manufacturers, offering production flexibility but embedding significant tooling and mold commitments; switching factories requires retooling, QA validation and potential weeks of downtime. These factors create moderate supplier power via switching costs. Long-term supply agreements can reduce near-term risk, though they increase strategic lock-in over time.

Logistics and tariffs exposure

Ocean freight, port congestion and trade tariffs materially drive landed cost; Section 301 tariffs on China remain as high as 25%, and carriers/3PLs obtain leverage during capacity tightness, pushing spot premiums and rollovers. Diversifying lanes and nearshoring cut exposure but require quarters to years to implement. Fuel surcharges and compliance fees create additional cost variability.

- Tariffs: up to 25% Section 301

- Carrier leverage: spot/contract premium risk

- Mitigation: lane diversification, nearshoring (time‑consuming)

- Cost drivers: fuel surcharges, compliance fees

Brand-critical quality control

Equipment safety and durability define Nautilus brand value, making high-spec suppliers indispensable and elevating supplier bargaining power as failures drive returns and warranty costs that erode margins.

Dependence on proven vendors increased in 2024 after intensified quality scrutiny; vendor audits and strict SLAs are used to re-balance leverage and contain recall risk.

- High-spec suppliers: critical

- Failures → higher returns/warranty costs

- 2024: intensified vendor audits and SLAs

Dispersed parts, concentrated firmware — 12–20w, 25%

Suppliers of commoditized parts are broadly dispersed across Asia and North America, limiting concentration risk, but firmware-integrated consoles and IoT modules concentrate bargaining power in a few vendors. 2024 lead times of 12–20 weeks and Section 301 tariffs up to 25% raise costs and working-capital needs. Contract manufacturers and tooling lock-in create moderate switching costs and strategic supplier leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| Component lead times | 12–20 weeks | Inventory/cost pressure |

| Tariffs | Section 301 up to 25% | Higher landed cost |

| Firmware/IoT suppliers | Few viable vendors | Higher supplier power |

What is included in the product

Tailored Porter's Five Forces analysis for Nautilus that uncovers the key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. Identifies disruptive substitutes, emerging threats, and incumbent advantages with strategic commentary suitable for investor decks or internal strategy.

One-sheet Nautilus Porter's Five Forces simplifies strategic pain points with a clean, customizable summary and instant spider chart visualization for quick decision-making. Swap in your own data, duplicate scenarios, and integrate into decks or dashboards without macros—ready for non-finance users and boardroom use.

Customers Bargaining Power

Highly price-sensitive consumers

Highly price-sensitive home-fitness buyers compare across brands and models via transparent online pricing—about 70% of shoppers check multiple sites—while promotions, BNPL and seasonal discounts heavily influence timing; low switching costs raise buyer leverage, and reviews or limited-time deals can rapidly swing perceived value and purchase decisions.

Retail and marketplace leverage

Large channels like Amazon and specialty retailers command shelf space and search placement—Amazon held about 38% of US e-commerce in 2024—letting them pressure margins via typical ~15% referral fees, returns policies and co-op marketing. Online return rates hover near 16%, so losing a key channel hits volume and visibility hard; DTC eases but dependence stays meaningful.

Content and subscription churn

Digital fitness buyers can cancel or switch apps with minimal friction; industry data in 2024 shows typical monthly churn of about 5–7%, implying annualized churn often exceeds 40%. Content freshness and tight hardware integration (connected bikes/treadmills) materially affect retention and perceived value. High churn amplifies buyer power on pricing and features, while bundling JRNY with Nautilus hardware can partially reduce switching by increasing switching costs and stickiness.

Information-rich purchase journey

Reviews, influencer content and comparison sites have eroded information asymmetry; a 2024 survey found 92% of consumers consult reviews before buying, so defects or design trade-offs are spotted quickly. That transparency compresses pricing power and raises switch risk, making reputation management and rapid product iteration essential for Nautilus.

- Reviews: 92% consult (2024)

- Effect: compressed pricing power

- Priority: reputation management

- Priority: rapid iteration

Post-pandemic demand volatility

- Shift volatility: at-home vs gym

- Buyer leverage: discounts up to 30% (2024)

- Inventory risk: overhang increases bargaining power

- Mitigation: forecasting + dynamic pricing

Customers hold leverage: 92% read reviews, 70% compare; 30% discounts compress margins

Customers hold strong bargaining power: 70% compare multiple sites and 92% consult reviews, driving price sensitivity and rapid switching; Amazon’s 38% US e-commerce share (2024) and ~15% referral fees pressure margins. Returns ~16% and monthly churn 5–7% (annual >40%) amplify leverage; discounts reached 30% in 2024, while e‑commerce demand sat ~25% above 2019.

| Metric | 2024 Value |

|---|---|

| Compare multiple sites | 70% |

| Consult reviews | 92% |

| Amazon e‑commerce share | 38% |

| Return rate | ~16% |

| Monthly churn | 5–7% |

| Peak discounts | ~30% |

| E‑commerce vs 2019 | +25% |

Preview Before You Purchase

Nautilus Porter's Five Forces Analysis

This preview shows the exact Nautilus Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Nautilus faces shifting competitive currents—moderate supplier leverage, evolving buyer expectations, and growing substitute threats as fitness tech and streaming content expand. This snapshot highlights key pressures and strategic implications for management and investors. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Diverse component sources

Core parts such as steel frames, motors, electronics, plastics and consoles are sourced widely from global suppliers—limiting concentration risk as major manufacturing hubs in Asia and North America supply the bulk of these components. Alternative vendors across Asia and North America enable competitive bids, though firmware-integrated consoles and IoT modules narrow viable suppliers to a handful. Dual-sourcing and vendor qualification typically add months to lead times and can raise procurement costs by several percent.

Specialized electronics reliance

Connected-fitness products rely on sensors, displays, chips and connectivity modules that in 2024 faced constrained supply with component lead times commonly 12–20 weeks, raising supplier leverage. Firmware integration and regulatory certifications create high switching friction and lock-in when suppliers customize parts to Nautilus specs. Long lead times force higher inventory or pay expedite fees, squeezing margins and raising working-capital needs.

Contract manufacturing and tooling

Much Nautilus equipment is made by contract manufacturers, offering production flexibility but embedding significant tooling and mold commitments; switching factories requires retooling, QA validation and potential weeks of downtime. These factors create moderate supplier power via switching costs. Long-term supply agreements can reduce near-term risk, though they increase strategic lock-in over time.

Logistics and tariffs exposure

Ocean freight, port congestion and trade tariffs materially drive landed cost; Section 301 tariffs on China remain as high as 25%, and carriers/3PLs obtain leverage during capacity tightness, pushing spot premiums and rollovers. Diversifying lanes and nearshoring cut exposure but require quarters to years to implement. Fuel surcharges and compliance fees create additional cost variability.

- Tariffs: up to 25% Section 301

- Carrier leverage: spot/contract premium risk

- Mitigation: lane diversification, nearshoring (time‑consuming)

- Cost drivers: fuel surcharges, compliance fees

Brand-critical quality control

Equipment safety and durability define Nautilus brand value, making high-spec suppliers indispensable and elevating supplier bargaining power as failures drive returns and warranty costs that erode margins.

Dependence on proven vendors increased in 2024 after intensified quality scrutiny; vendor audits and strict SLAs are used to re-balance leverage and contain recall risk.

- High-spec suppliers: critical

- Failures → higher returns/warranty costs

- 2024: intensified vendor audits and SLAs

Dispersed parts, concentrated firmware — 12–20w, 25%

Suppliers of commoditized parts are broadly dispersed across Asia and North America, limiting concentration risk, but firmware-integrated consoles and IoT modules concentrate bargaining power in a few vendors. 2024 lead times of 12–20 weeks and Section 301 tariffs up to 25% raise costs and working-capital needs. Contract manufacturers and tooling lock-in create moderate switching costs and strategic supplier leverage.

| Metric | 2024 value | Impact |

|---|---|---|

| Component lead times | 12–20 weeks | Inventory/cost pressure |

| Tariffs | Section 301 up to 25% | Higher landed cost |

| Firmware/IoT suppliers | Few viable vendors | Higher supplier power |

What is included in the product

Tailored Porter's Five Forces analysis for Nautilus that uncovers the key drivers of competition, buyer and supplier power, and market entry risks affecting pricing and profitability. Identifies disruptive substitutes, emerging threats, and incumbent advantages with strategic commentary suitable for investor decks or internal strategy.

One-sheet Nautilus Porter's Five Forces simplifies strategic pain points with a clean, customizable summary and instant spider chart visualization for quick decision-making. Swap in your own data, duplicate scenarios, and integrate into decks or dashboards without macros—ready for non-finance users and boardroom use.

Customers Bargaining Power

Highly price-sensitive consumers

Highly price-sensitive home-fitness buyers compare across brands and models via transparent online pricing—about 70% of shoppers check multiple sites—while promotions, BNPL and seasonal discounts heavily influence timing; low switching costs raise buyer leverage, and reviews or limited-time deals can rapidly swing perceived value and purchase decisions.

Retail and marketplace leverage

Large channels like Amazon and specialty retailers command shelf space and search placement—Amazon held about 38% of US e-commerce in 2024—letting them pressure margins via typical ~15% referral fees, returns policies and co-op marketing. Online return rates hover near 16%, so losing a key channel hits volume and visibility hard; DTC eases but dependence stays meaningful.

Content and subscription churn

Digital fitness buyers can cancel or switch apps with minimal friction; industry data in 2024 shows typical monthly churn of about 5–7%, implying annualized churn often exceeds 40%. Content freshness and tight hardware integration (connected bikes/treadmills) materially affect retention and perceived value. High churn amplifies buyer power on pricing and features, while bundling JRNY with Nautilus hardware can partially reduce switching by increasing switching costs and stickiness.

Information-rich purchase journey

Reviews, influencer content and comparison sites have eroded information asymmetry; a 2024 survey found 92% of consumers consult reviews before buying, so defects or design trade-offs are spotted quickly. That transparency compresses pricing power and raises switch risk, making reputation management and rapid product iteration essential for Nautilus.

- Reviews: 92% consult (2024)

- Effect: compressed pricing power

- Priority: reputation management

- Priority: rapid iteration

Post-pandemic demand volatility

- Shift volatility: at-home vs gym

- Buyer leverage: discounts up to 30% (2024)

- Inventory risk: overhang increases bargaining power

- Mitigation: forecasting + dynamic pricing

Customers hold leverage: 92% read reviews, 70% compare; 30% discounts compress margins

Customers hold strong bargaining power: 70% compare multiple sites and 92% consult reviews, driving price sensitivity and rapid switching; Amazon’s 38% US e-commerce share (2024) and ~15% referral fees pressure margins. Returns ~16% and monthly churn 5–7% (annual >40%) amplify leverage; discounts reached 30% in 2024, while e‑commerce demand sat ~25% above 2019.

| Metric | 2024 Value |

|---|---|

| Compare multiple sites | 70% |

| Consult reviews | 92% |

| Amazon e‑commerce share | 38% |

| Return rate | ~16% |

| Monthly churn | 5–7% |

| Peak discounts | ~30% |

| E‑commerce vs 2019 | +25% |

Preview Before You Purchase

Nautilus Porter's Five Forces Analysis

This preview shows the exact Nautilus Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical document.