Navigator SWOT Analysis

Your Strategic Toolkit Starts Here

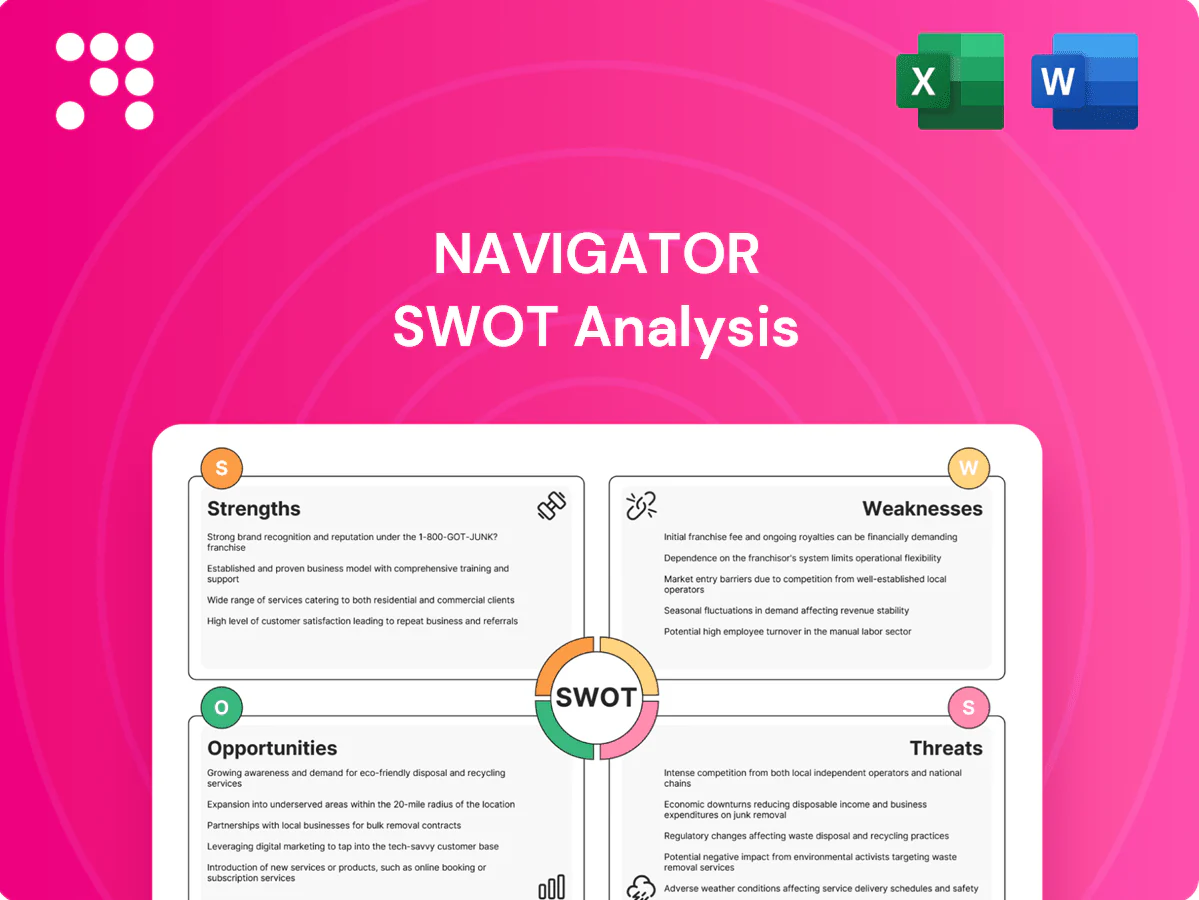

Discover Navigator's competitive edge and hidden risks with our full SWOT analysis—an investor-ready, research-backed report with actionable strategies and editable Word/Excel deliverables. Purchase the complete analysis to strategize confidently, present professionally, and seize growth opportunities.

Strengths

Diverse alt platform

Navigator’s diverse platform across private equity, hedge funds and credit reduces reliance on any single cycle and aligns with a market where global alternative assets topped roughly $17 trillion in 2024. This mix smooths fee revenues and helps dampen drawdowns through uncorrelated return streams. It also enables targeted cross-selling to institutions and HNWIs, strengthening client engagement and supporting durable relationships.

Global client reach

Navigator's global client reach leverages institutional and wealth channels across regions to widen the fundraising funnel, tapping into a market where global alternative assets AUM topped about $17 trillion by 2024. Geographic spread reduces exposure to local market shocks and supports larger fund launches, enabling scalable product rollouts. Broad distribution enhances brand recognition and pipeline visibility, improving odds for multi-region syndication and cross-border capital placement.

Recurring fee base

Management fees from locked-up vehicles provide a stable baseline cash flow, with typical private-equity-style management fees around 1.5% of AUM. Long-duration capital (fund lives commonly 7–10 years) improves planning and smooths investment pacing. Performance fees (carry commonly 20%) create significant upside in strong markets. This fee mix supports ongoing reinvestment and sustainable shareholder returns.

Manager services edge

Navigator’s embedded administrative and operational support ties it closely to underlying managers, creating vertical integration that McKinsey (2023) estimates can cut operating costs up to 25% and improve data transparency through unified systems.

Those integrated services deepen partnerships, with Deloitte (2024) noting integrated-servicing models can reduce client churn by ~30% and raise retention above industry averages; service stickiness thus forms a durable competitive moat.

- Operational cost reduction: McKinsey 2023 ~25%

- Churn reduction: Deloitte 2024 ~30%

- Higher retention: integrated-servicing > industry avg

Multi-manager sourcing

Multi-manager sourcing expands idea flow by tapping dozens of specialist managers, and as of 2024 institutional allocations to multi-manager sleeves represented an estimated 10–15% of alternative portfolios, increasing origination channels.

Flexible allocations let capital rotate to outperformers—median rebalancing windows are often 30–90 days—while spreading exposures across 8–12 managers reduces single-manager key-person risk.

The modular architecture speeds onboarding of new strategies, typically enabling pilot allocations within 30–90 days to capture emerging opportunities.

- Access: dozens of specialist managers

- Flexibility: rebalances in 30–90 days

- Risk: diversification across 8–12 managers

- Adaptability: pilot allocations in 30–90 days

Diversified alternatives platform taps $17T market, smoothing revenue via uncorrelated returns

Navigator’s diversified alternatives platform reduces cycle risk and taps a ~$17 trillion 2024 market, smoothing revenues via uncorrelated returns. Global distribution and multi-manager sourcing (10–15% of alt allocations) expand fundraising and origination. Integrated servicing boosts retention and cuts costs (McKinsey 2023 ~25%; Deloitte 2024 churn ~30%), while fee mix (mgmt ~1.5%, carry ~20%) underpins cash flow.

| Metric | Value |

|---|---|

| Global alt AUM (2024) | $17T |

| Mgmt fee | ~1.5% |

| Carry | ~20% |

| Cost reduction | ~25% (McKinsey 2023) |

| Churn reduction | ~30% (Deloitte 2024) |

What is included in the product

Provides a concise SWOT analysis of Navigator, outlining internal strengths and weaknesses and external opportunities and threats to assess the company’s strategic position, growth drivers, and key risks.

Offers a compact, editable Navigator SWOT matrix that accelerates cross-team alignment, simplifies stakeholder-ready presentations, and lets executives quickly update priorities for fast decision-making.

Weaknesses

Perf fee volatility

Carry and incentive fees, typically 20% of profits with common 8% hurdles, are highly cyclical and tied to market marks and exits. Quarterly revaluations and uneven exit pacing can swing reported earnings materially, complicating forecasting and valuation multiples. As a result, investors often apply valuation discounts of roughly 10–25% for fee volatility.

Opaque valuations

Private assets (global AUM >$12 trillion) rely heavily on models and lagged marks, with many funds publishing quarterly NAVs that can be 60–90 days stale. Limited transparency has driven sharper outflows in downturns, amplifying confidence erosion. NAV timing mismatches introduce noise across reported returns and performance attribution. Audit and valuation costs are structurally higher, often running in the 20–50 basis point range.

Manager concentration

Revenue may be concentrated in a few flagship managers or funds, with the top three managers often accounting for more than 50% of platform fees in comparable asset platforms; loss of one relationship can remove double-digit percent of AUM, key-person departures at partners elevate redemption and performance risk, and diversification across GPs remains incomplete.

Fee pressure risk

Institutions increasingly secure lower management fees and tougher hurdle rates; competition from mega-managers (combined AUM >$20 trillion in 2024) intensifies pricing pressure, causing blended fee rates to drift down and compress margins, forcing firms to defend profitability through scale and clear product differentiation.

- Rising institutional negotiations

- Pricing pressure from top managers

- Blended fee erosion over time

- Need scale + differentiation to protect margins

Regulatory burden

Multiple jurisdictions increase legal and compliance overhead, raising costs and time-to-market; EU rules like GDPR (fines up to 4% of global turnover) and the Digital Markets Act (up to 10% of turnover) exemplify material financial risk. Frequent compliance changes slow product launch cadence, reporting requirements strain operations and systems, and fines or remediation divert capital and talent from growth.

- Jurisdictional complexity raises costs

- Regulatory changes delay launches

- Reporting strains systems

- Fines/remediation divert resources

Fee volatility and lagged NAVs create 10–25% valuation discounts and redemption risk

Fee volatility (carry + incentive) drives 10–25% valuation discounts and quarterly marks create earnings swing; audit/valuation costs run ~20–50 bps. Private assets (global AUM >$12 trillion) use lagged NAVs (60–90 days), raising redemption risk and transparency concerns. Revenue concentration is high (top 3 managers >50% platform fees) while mega-managers (> $20T) pressure fees and margins.

| Metric | Value |

|---|---|

| Private assets AUM | > $12 trillion (2024) |

| Mega-managers AUM | > $20 trillion (2024) |

| Valuation discount | 10–25% |

| Audit/valuation costs | 20–50 bps |

| Top-3 fee concentration | > 50% |

| NAV staleness | 60–90 days |

| GDPR fine | up to 4% turnover |

| DMA fine | up to 10% turnover |

Preview Before You Purchase

Navigator SWOT Analysis

This preview is the actual Navigator SWOT analysis document you’ll receive upon purchase — no placeholders or samples, just the same professional, structured file. The excerpt below is taken directly from the full report, and buying unlocks the complete, editable version. Purchase now to download the entire, ready-to-use SWOT analysis.

Your Strategic Toolkit Starts Here

Discover Navigator's competitive edge and hidden risks with our full SWOT analysis—an investor-ready, research-backed report with actionable strategies and editable Word/Excel deliverables. Purchase the complete analysis to strategize confidently, present professionally, and seize growth opportunities.

Strengths

Diverse alt platform

Navigator’s diverse platform across private equity, hedge funds and credit reduces reliance on any single cycle and aligns with a market where global alternative assets topped roughly $17 trillion in 2024. This mix smooths fee revenues and helps dampen drawdowns through uncorrelated return streams. It also enables targeted cross-selling to institutions and HNWIs, strengthening client engagement and supporting durable relationships.

Global client reach

Navigator's global client reach leverages institutional and wealth channels across regions to widen the fundraising funnel, tapping into a market where global alternative assets AUM topped about $17 trillion by 2024. Geographic spread reduces exposure to local market shocks and supports larger fund launches, enabling scalable product rollouts. Broad distribution enhances brand recognition and pipeline visibility, improving odds for multi-region syndication and cross-border capital placement.

Recurring fee base

Management fees from locked-up vehicles provide a stable baseline cash flow, with typical private-equity-style management fees around 1.5% of AUM. Long-duration capital (fund lives commonly 7–10 years) improves planning and smooths investment pacing. Performance fees (carry commonly 20%) create significant upside in strong markets. This fee mix supports ongoing reinvestment and sustainable shareholder returns.

Manager services edge

Navigator’s embedded administrative and operational support ties it closely to underlying managers, creating vertical integration that McKinsey (2023) estimates can cut operating costs up to 25% and improve data transparency through unified systems.

Those integrated services deepen partnerships, with Deloitte (2024) noting integrated-servicing models can reduce client churn by ~30% and raise retention above industry averages; service stickiness thus forms a durable competitive moat.

- Operational cost reduction: McKinsey 2023 ~25%

- Churn reduction: Deloitte 2024 ~30%

- Higher retention: integrated-servicing > industry avg

Multi-manager sourcing

Multi-manager sourcing expands idea flow by tapping dozens of specialist managers, and as of 2024 institutional allocations to multi-manager sleeves represented an estimated 10–15% of alternative portfolios, increasing origination channels.

Flexible allocations let capital rotate to outperformers—median rebalancing windows are often 30–90 days—while spreading exposures across 8–12 managers reduces single-manager key-person risk.

The modular architecture speeds onboarding of new strategies, typically enabling pilot allocations within 30–90 days to capture emerging opportunities.

- Access: dozens of specialist managers

- Flexibility: rebalances in 30–90 days

- Risk: diversification across 8–12 managers

- Adaptability: pilot allocations in 30–90 days

Diversified alternatives platform taps $17T market, smoothing revenue via uncorrelated returns

Navigator’s diversified alternatives platform reduces cycle risk and taps a ~$17 trillion 2024 market, smoothing revenues via uncorrelated returns. Global distribution and multi-manager sourcing (10–15% of alt allocations) expand fundraising and origination. Integrated servicing boosts retention and cuts costs (McKinsey 2023 ~25%; Deloitte 2024 churn ~30%), while fee mix (mgmt ~1.5%, carry ~20%) underpins cash flow.

| Metric | Value |

|---|---|

| Global alt AUM (2024) | $17T |

| Mgmt fee | ~1.5% |

| Carry | ~20% |

| Cost reduction | ~25% (McKinsey 2023) |

| Churn reduction | ~30% (Deloitte 2024) |

What is included in the product

Provides a concise SWOT analysis of Navigator, outlining internal strengths and weaknesses and external opportunities and threats to assess the company’s strategic position, growth drivers, and key risks.

Offers a compact, editable Navigator SWOT matrix that accelerates cross-team alignment, simplifies stakeholder-ready presentations, and lets executives quickly update priorities for fast decision-making.

Weaknesses

Perf fee volatility

Carry and incentive fees, typically 20% of profits with common 8% hurdles, are highly cyclical and tied to market marks and exits. Quarterly revaluations and uneven exit pacing can swing reported earnings materially, complicating forecasting and valuation multiples. As a result, investors often apply valuation discounts of roughly 10–25% for fee volatility.

Opaque valuations

Private assets (global AUM >$12 trillion) rely heavily on models and lagged marks, with many funds publishing quarterly NAVs that can be 60–90 days stale. Limited transparency has driven sharper outflows in downturns, amplifying confidence erosion. NAV timing mismatches introduce noise across reported returns and performance attribution. Audit and valuation costs are structurally higher, often running in the 20–50 basis point range.

Manager concentration

Revenue may be concentrated in a few flagship managers or funds, with the top three managers often accounting for more than 50% of platform fees in comparable asset platforms; loss of one relationship can remove double-digit percent of AUM, key-person departures at partners elevate redemption and performance risk, and diversification across GPs remains incomplete.

Fee pressure risk

Institutions increasingly secure lower management fees and tougher hurdle rates; competition from mega-managers (combined AUM >$20 trillion in 2024) intensifies pricing pressure, causing blended fee rates to drift down and compress margins, forcing firms to defend profitability through scale and clear product differentiation.

- Rising institutional negotiations

- Pricing pressure from top managers

- Blended fee erosion over time

- Need scale + differentiation to protect margins

Regulatory burden

Multiple jurisdictions increase legal and compliance overhead, raising costs and time-to-market; EU rules like GDPR (fines up to 4% of global turnover) and the Digital Markets Act (up to 10% of turnover) exemplify material financial risk. Frequent compliance changes slow product launch cadence, reporting requirements strain operations and systems, and fines or remediation divert capital and talent from growth.

- Jurisdictional complexity raises costs

- Regulatory changes delay launches

- Reporting strains systems

- Fines/remediation divert resources

Fee volatility and lagged NAVs create 10–25% valuation discounts and redemption risk

Fee volatility (carry + incentive) drives 10–25% valuation discounts and quarterly marks create earnings swing; audit/valuation costs run ~20–50 bps. Private assets (global AUM >$12 trillion) use lagged NAVs (60–90 days), raising redemption risk and transparency concerns. Revenue concentration is high (top 3 managers >50% platform fees) while mega-managers (> $20T) pressure fees and margins.

| Metric | Value |

|---|---|

| Private assets AUM | > $12 trillion (2024) |

| Mega-managers AUM | > $20 trillion (2024) |

| Valuation discount | 10–25% |

| Audit/valuation costs | 20–50 bps |

| Top-3 fee concentration | > 50% |

| NAV staleness | 60–90 days |

| GDPR fine | up to 4% turnover |

| DMA fine | up to 10% turnover |

Preview Before You Purchase

Navigator SWOT Analysis

This preview is the actual Navigator SWOT analysis document you’ll receive upon purchase — no placeholders or samples, just the same professional, structured file. The excerpt below is taken directly from the full report, and buying unlocks the complete, editable version. Purchase now to download the entire, ready-to-use SWOT analysis.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Discover Navigator's competitive edge and hidden risks with our full SWOT analysis—an investor-ready, research-backed report with actionable strategies and editable Word/Excel deliverables. Purchase the complete analysis to strategize confidently, present professionally, and seize growth opportunities.

Strengths

Diverse alt platform

Navigator’s diverse platform across private equity, hedge funds and credit reduces reliance on any single cycle and aligns with a market where global alternative assets topped roughly $17 trillion in 2024. This mix smooths fee revenues and helps dampen drawdowns through uncorrelated return streams. It also enables targeted cross-selling to institutions and HNWIs, strengthening client engagement and supporting durable relationships.

Global client reach

Navigator's global client reach leverages institutional and wealth channels across regions to widen the fundraising funnel, tapping into a market where global alternative assets AUM topped about $17 trillion by 2024. Geographic spread reduces exposure to local market shocks and supports larger fund launches, enabling scalable product rollouts. Broad distribution enhances brand recognition and pipeline visibility, improving odds for multi-region syndication and cross-border capital placement.

Recurring fee base

Management fees from locked-up vehicles provide a stable baseline cash flow, with typical private-equity-style management fees around 1.5% of AUM. Long-duration capital (fund lives commonly 7–10 years) improves planning and smooths investment pacing. Performance fees (carry commonly 20%) create significant upside in strong markets. This fee mix supports ongoing reinvestment and sustainable shareholder returns.

Manager services edge

Navigator’s embedded administrative and operational support ties it closely to underlying managers, creating vertical integration that McKinsey (2023) estimates can cut operating costs up to 25% and improve data transparency through unified systems.

Those integrated services deepen partnerships, with Deloitte (2024) noting integrated-servicing models can reduce client churn by ~30% and raise retention above industry averages; service stickiness thus forms a durable competitive moat.

- Operational cost reduction: McKinsey 2023 ~25%

- Churn reduction: Deloitte 2024 ~30%

- Higher retention: integrated-servicing > industry avg

Multi-manager sourcing

Multi-manager sourcing expands idea flow by tapping dozens of specialist managers, and as of 2024 institutional allocations to multi-manager sleeves represented an estimated 10–15% of alternative portfolios, increasing origination channels.

Flexible allocations let capital rotate to outperformers—median rebalancing windows are often 30–90 days—while spreading exposures across 8–12 managers reduces single-manager key-person risk.

The modular architecture speeds onboarding of new strategies, typically enabling pilot allocations within 30–90 days to capture emerging opportunities.

- Access: dozens of specialist managers

- Flexibility: rebalances in 30–90 days

- Risk: diversification across 8–12 managers

- Adaptability: pilot allocations in 30–90 days

Diversified alternatives platform taps $17T market, smoothing revenue via uncorrelated returns

Navigator’s diversified alternatives platform reduces cycle risk and taps a ~$17 trillion 2024 market, smoothing revenues via uncorrelated returns. Global distribution and multi-manager sourcing (10–15% of alt allocations) expand fundraising and origination. Integrated servicing boosts retention and cuts costs (McKinsey 2023 ~25%; Deloitte 2024 churn ~30%), while fee mix (mgmt ~1.5%, carry ~20%) underpins cash flow.

| Metric | Value |

|---|---|

| Global alt AUM (2024) | $17T |

| Mgmt fee | ~1.5% |

| Carry | ~20% |

| Cost reduction | ~25% (McKinsey 2023) |

| Churn reduction | ~30% (Deloitte 2024) |

What is included in the product

Provides a concise SWOT analysis of Navigator, outlining internal strengths and weaknesses and external opportunities and threats to assess the company’s strategic position, growth drivers, and key risks.

Offers a compact, editable Navigator SWOT matrix that accelerates cross-team alignment, simplifies stakeholder-ready presentations, and lets executives quickly update priorities for fast decision-making.

Weaknesses

Perf fee volatility

Carry and incentive fees, typically 20% of profits with common 8% hurdles, are highly cyclical and tied to market marks and exits. Quarterly revaluations and uneven exit pacing can swing reported earnings materially, complicating forecasting and valuation multiples. As a result, investors often apply valuation discounts of roughly 10–25% for fee volatility.

Opaque valuations

Private assets (global AUM >$12 trillion) rely heavily on models and lagged marks, with many funds publishing quarterly NAVs that can be 60–90 days stale. Limited transparency has driven sharper outflows in downturns, amplifying confidence erosion. NAV timing mismatches introduce noise across reported returns and performance attribution. Audit and valuation costs are structurally higher, often running in the 20–50 basis point range.

Manager concentration

Revenue may be concentrated in a few flagship managers or funds, with the top three managers often accounting for more than 50% of platform fees in comparable asset platforms; loss of one relationship can remove double-digit percent of AUM, key-person departures at partners elevate redemption and performance risk, and diversification across GPs remains incomplete.

Fee pressure risk

Institutions increasingly secure lower management fees and tougher hurdle rates; competition from mega-managers (combined AUM >$20 trillion in 2024) intensifies pricing pressure, causing blended fee rates to drift down and compress margins, forcing firms to defend profitability through scale and clear product differentiation.

- Rising institutional negotiations

- Pricing pressure from top managers

- Blended fee erosion over time

- Need scale + differentiation to protect margins

Regulatory burden

Multiple jurisdictions increase legal and compliance overhead, raising costs and time-to-market; EU rules like GDPR (fines up to 4% of global turnover) and the Digital Markets Act (up to 10% of turnover) exemplify material financial risk. Frequent compliance changes slow product launch cadence, reporting requirements strain operations and systems, and fines or remediation divert capital and talent from growth.

- Jurisdictional complexity raises costs

- Regulatory changes delay launches

- Reporting strains systems

- Fines/remediation divert resources

Fee volatility and lagged NAVs create 10–25% valuation discounts and redemption risk

Fee volatility (carry + incentive) drives 10–25% valuation discounts and quarterly marks create earnings swing; audit/valuation costs run ~20–50 bps. Private assets (global AUM >$12 trillion) use lagged NAVs (60–90 days), raising redemption risk and transparency concerns. Revenue concentration is high (top 3 managers >50% platform fees) while mega-managers (> $20T) pressure fees and margins.

| Metric | Value |

|---|---|

| Private assets AUM | > $12 trillion (2024) |

| Mega-managers AUM | > $20 trillion (2024) |

| Valuation discount | 10–25% |

| Audit/valuation costs | 20–50 bps |

| Top-3 fee concentration | > 50% |

| NAV staleness | 60–90 days |

| GDPR fine | up to 4% turnover |

| DMA fine | up to 10% turnover |

Preview Before You Purchase

Navigator SWOT Analysis

This preview is the actual Navigator SWOT analysis document you’ll receive upon purchase — no placeholders or samples, just the same professional, structured file. The excerpt below is taken directly from the full report, and buying unlocks the complete, editable version. Purchase now to download the entire, ready-to-use SWOT analysis.