Nay Elektrodom AS Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

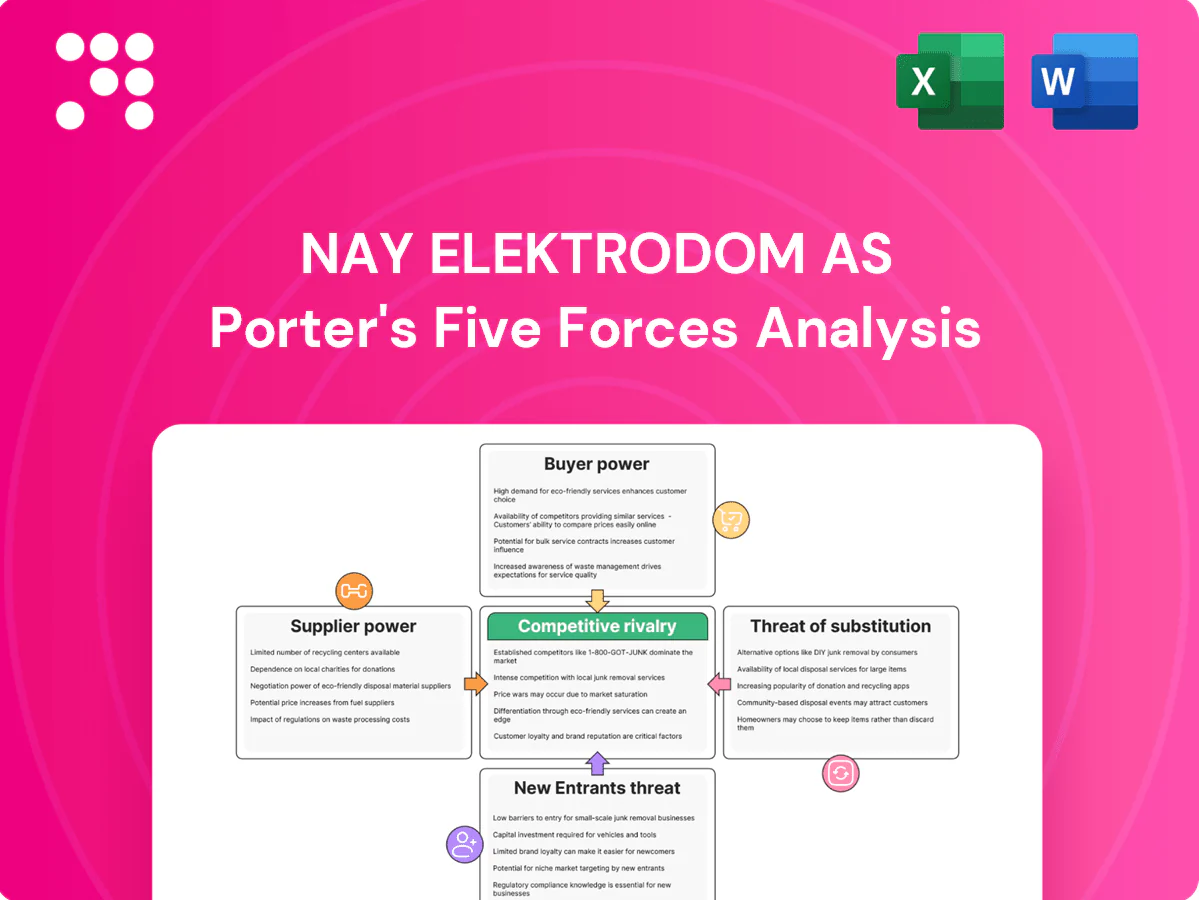

Nay Elektrodom AS faces moderate buyer power and intense rivalry from national retailers and e-commerce, while supplier influence is limited by brand diversity; threats from new entrants and substitutes are tempered by scale and logistics. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Nay Elektrodom AS.

Suppliers Bargaining Power

Global OEM concentration

Major categories at NAY rely on a few global brands—Samsung, Apple, LG, Bosch and HP—whose scale translates into leverage over pricing, allocation and marketing terms; Apple alone reported $383 billion revenue in FY2024, underscoring supplier clout. Limited product differentiation in retail increases brand power over shelf space and promotions. NAY mitigates this with multi-brand assortments and volume-based purchase commitments to secure better terms.

Distributor intermediation

Regional distributors between NAY and OEMs add margin layers—commonly 5–12% in CE channels in 2024—reducing NAY’s direct negotiating leverage and visibility into allocations. Building direct OEM accounts where feasible has been shown to improve net terms and exclusivity, often trimming costs by 1–3% and shortening lead times. Implementing dual-sourcing for key SKUs hedges allocation risk and has cut peak-season stockouts by roughly 25–35% in comparable retailers.

Supply chain constraints

Cyclic chip shortages and logistics bottlenecks in 2024 kept semiconductor lead times elevated (around 14 weeks) and shifted pricing power to suppliers, with allocation favoring large, multi-country buyers and pressuring domestic chains. NAY, serving Slovakia (5.4M population), benefits from national scale but remains modest versus pan-EU retailers. Early ordering and vendor-managed inventory (VMI) — shown to cut stockouts/inventory by ~20–30% — can soften shocks.

Brand-led MAP and promotions

OEMs enforce MAP, co-op budgets and promo calendars (co-op funds commonly 1–3% of retail sales in 2024), and NAY must comply to access hero SKUs and marketing funds, which constrains pricing flexibility on flagship products and compresses margin on promoted lines.

- MAP limits discounting

- Co-op funds 1–3% (2024)

- Access tied to compliance

- Private-label & service bundles recover margin

After-sales dependency

After-sales repairs and warranties for NAY Elektrodom rely on OEM parts and brand authorization, which gives suppliers leverage over turnaround times and reimbursement rates; as of 2024 major manufacturers maintain warranty authorization requirements across the Baltic retail channel. Strong service SLAs protect NAY’s reputation but tie repair workflows to OEM policies, while investment in certified service capacity reduces dependency and strengthens negotiating position.

- OEM authorization required

- Suppliers set turnaround/reimbursement

- Service SLAs protect brand

- Certified service investment = higher bargaining power

Supplier leverage, ~14-week chip lead times and 5-12% distributor margins

Suppliers (Samsung, Apple, LG, Bosch, HP) hold strong leverage—Apple revenue $383B (FY2024), MAP and co-op funds 1–3% limit NAY pricing; distributor layers add 5–12% margin. Chip lead times ~14 weeks (2024) favor large buyers; VMI/early ordering cuts stockouts ~20–30%. Certified service capacity improves NAY bargaining on warranties and turnarounds.

| Metric | 2024 |

|---|---|

| Apple rev | $383B |

| Distributor margin | 5–12% |

| Co-op/MAP | 1–3% |

| Chip LT | ~14w |

What is included in the product

Tailored Porter's Five Forces for Nay Elektrodom AS revealing competitive intensity, buyer/supplier power, threat of new entrants and substitutes, plus strategic barriers protecting its market position.

A concise one-sheet Porter's Five Forces summary for Nay Elektrodom—instantly visualize competitive pressure with a spider chart, customize force levels for shifting retail, supplier and regulatory dynamics, and drop directly into pitch decks or dashboards for fast decision-making.

Customers Bargaining Power

High price transparency

High price transparency in 2024 lets customers compare Alza, Datart, Mall and marketplace offers instantly, compressing gross margins on KVIs such as smartphones and TVs into low single-digit bands. Dynamic pricing engines and price-match policies are now standard expectations across retailers. Competitive differentiation shifts to availability, fulfillment speed and after-sales service.

Low switching costs

Low switching costs let shoppers pivot with a click as e-commerce captured 13.6% of EU retail in 2023 and Estonia records 92% internet use (Eurostat 2023), making loyalty fragile without tangible perks; NAY can anchor repeat purchases with loyalty programs, point-of-sale financing and bundle offers, while click-and-collect convenience lowers churn.

Service-sensitive segments

Service-sensitive segments wield higher bargaining power for Nay Elektrodom as installation, haul-away and extended warranties for large appliances justify premiums and limit pure price competition. Clear SLAs and next-day delivery—cited by 2024 consumer surveys as a top 3 purchase driver—increase perceived value and brand stickiness. Business customers additionally prioritize invoicing terms and post-sale technical support, shifting negotiations toward service levels rather than unit price.

Demand volatility and seasonality

Demand volatility around Black Friday, back-to-school and holiday peaks concentrates customer leverage as shoppers time purchases and expect steep discounts, forcing NAY to lock promotional stock and plan tiered offers well before peak windows to avoid stockouts and margin erosion. Deal-seeking behavior amplifies discount expectations, while targeted personalized offers on non-promoted lines help preserve margins and increase attachment rates.

- Peak events concentrate leverage

- Early promo inventory commitments

- Tiered offers reduce margin hit

- Personalization protects non-promoted margins

Product information abundance

Product information abundance sharply reduces information asymmetry: Statista 2024 found 85% of electronics shoppers consult reviews and specs before purchase, empowering customers to demand exact SKUs and features and narrowing upsell opportunities for Nay Elektrodom AS. Guided-selling tools and personalized recommendations can redirect choices toward higher-margin alternatives, while rich content and expert advice reclaim influence at the point of decision.

- Reviews/specs cut information asymmetry — 85% consult reviews (Statista 2024)

- Demand for specific SKUs limits generic upsell

- Guided selling drives margin capture

- Content/expert advice increases conversion influence

Price transparency and dynamic pricing squeeze margins; loyalty, personalization protect revenue

High price transparency and dynamic pricing (Statista 2024: 85% consult reviews) compress margins on KVIs; fast fulfillment and service drive loyalty. Low switching costs and rising e-commerce (EU ~14.8% 2024) increase customer leverage; loyalty programs, financing and bundles mitigate churn. Peak events amplify discount pressure; personalization and guided selling preserve margins.

| Metric | Value |

|---|---|

| Reviews consulted | 85% (Statista 2024) |

| EU e‑commerce | ~14.8% (2024) |

Preview Before You Purchase

Nay Elektrodom AS Porter's Five Forces Analysis

This preview shows the Nay Elektrodom AS Porter's Five Forces Analysis and is the exact document you'll receive upon purchase. It is fully formatted, professionally written, and ready for immediate use. No placeholders or samples—what you see is what you’ll download instantly.

A Must-Have Tool for Decision-Makers

Nay Elektrodom AS faces moderate buyer power and intense rivalry from national retailers and e-commerce, while supplier influence is limited by brand diversity; threats from new entrants and substitutes are tempered by scale and logistics. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Nay Elektrodom AS.

Suppliers Bargaining Power

Global OEM concentration

Major categories at NAY rely on a few global brands—Samsung, Apple, LG, Bosch and HP—whose scale translates into leverage over pricing, allocation and marketing terms; Apple alone reported $383 billion revenue in FY2024, underscoring supplier clout. Limited product differentiation in retail increases brand power over shelf space and promotions. NAY mitigates this with multi-brand assortments and volume-based purchase commitments to secure better terms.

Distributor intermediation

Regional distributors between NAY and OEMs add margin layers—commonly 5–12% in CE channels in 2024—reducing NAY’s direct negotiating leverage and visibility into allocations. Building direct OEM accounts where feasible has been shown to improve net terms and exclusivity, often trimming costs by 1–3% and shortening lead times. Implementing dual-sourcing for key SKUs hedges allocation risk and has cut peak-season stockouts by roughly 25–35% in comparable retailers.

Supply chain constraints

Cyclic chip shortages and logistics bottlenecks in 2024 kept semiconductor lead times elevated (around 14 weeks) and shifted pricing power to suppliers, with allocation favoring large, multi-country buyers and pressuring domestic chains. NAY, serving Slovakia (5.4M population), benefits from national scale but remains modest versus pan-EU retailers. Early ordering and vendor-managed inventory (VMI) — shown to cut stockouts/inventory by ~20–30% — can soften shocks.

Brand-led MAP and promotions

OEMs enforce MAP, co-op budgets and promo calendars (co-op funds commonly 1–3% of retail sales in 2024), and NAY must comply to access hero SKUs and marketing funds, which constrains pricing flexibility on flagship products and compresses margin on promoted lines.

- MAP limits discounting

- Co-op funds 1–3% (2024)

- Access tied to compliance

- Private-label & service bundles recover margin

After-sales dependency

After-sales repairs and warranties for NAY Elektrodom rely on OEM parts and brand authorization, which gives suppliers leverage over turnaround times and reimbursement rates; as of 2024 major manufacturers maintain warranty authorization requirements across the Baltic retail channel. Strong service SLAs protect NAY’s reputation but tie repair workflows to OEM policies, while investment in certified service capacity reduces dependency and strengthens negotiating position.

- OEM authorization required

- Suppliers set turnaround/reimbursement

- Service SLAs protect brand

- Certified service investment = higher bargaining power

Supplier leverage, ~14-week chip lead times and 5-12% distributor margins

Suppliers (Samsung, Apple, LG, Bosch, HP) hold strong leverage—Apple revenue $383B (FY2024), MAP and co-op funds 1–3% limit NAY pricing; distributor layers add 5–12% margin. Chip lead times ~14 weeks (2024) favor large buyers; VMI/early ordering cuts stockouts ~20–30%. Certified service capacity improves NAY bargaining on warranties and turnarounds.

| Metric | 2024 |

|---|---|

| Apple rev | $383B |

| Distributor margin | 5–12% |

| Co-op/MAP | 1–3% |

| Chip LT | ~14w |

What is included in the product

Tailored Porter's Five Forces for Nay Elektrodom AS revealing competitive intensity, buyer/supplier power, threat of new entrants and substitutes, plus strategic barriers protecting its market position.

A concise one-sheet Porter's Five Forces summary for Nay Elektrodom—instantly visualize competitive pressure with a spider chart, customize force levels for shifting retail, supplier and regulatory dynamics, and drop directly into pitch decks or dashboards for fast decision-making.

Customers Bargaining Power

High price transparency

High price transparency in 2024 lets customers compare Alza, Datart, Mall and marketplace offers instantly, compressing gross margins on KVIs such as smartphones and TVs into low single-digit bands. Dynamic pricing engines and price-match policies are now standard expectations across retailers. Competitive differentiation shifts to availability, fulfillment speed and after-sales service.

Low switching costs

Low switching costs let shoppers pivot with a click as e-commerce captured 13.6% of EU retail in 2023 and Estonia records 92% internet use (Eurostat 2023), making loyalty fragile without tangible perks; NAY can anchor repeat purchases with loyalty programs, point-of-sale financing and bundle offers, while click-and-collect convenience lowers churn.

Service-sensitive segments

Service-sensitive segments wield higher bargaining power for Nay Elektrodom as installation, haul-away and extended warranties for large appliances justify premiums and limit pure price competition. Clear SLAs and next-day delivery—cited by 2024 consumer surveys as a top 3 purchase driver—increase perceived value and brand stickiness. Business customers additionally prioritize invoicing terms and post-sale technical support, shifting negotiations toward service levels rather than unit price.

Demand volatility and seasonality

Demand volatility around Black Friday, back-to-school and holiday peaks concentrates customer leverage as shoppers time purchases and expect steep discounts, forcing NAY to lock promotional stock and plan tiered offers well before peak windows to avoid stockouts and margin erosion. Deal-seeking behavior amplifies discount expectations, while targeted personalized offers on non-promoted lines help preserve margins and increase attachment rates.

- Peak events concentrate leverage

- Early promo inventory commitments

- Tiered offers reduce margin hit

- Personalization protects non-promoted margins

Product information abundance

Product information abundance sharply reduces information asymmetry: Statista 2024 found 85% of electronics shoppers consult reviews and specs before purchase, empowering customers to demand exact SKUs and features and narrowing upsell opportunities for Nay Elektrodom AS. Guided-selling tools and personalized recommendations can redirect choices toward higher-margin alternatives, while rich content and expert advice reclaim influence at the point of decision.

- Reviews/specs cut information asymmetry — 85% consult reviews (Statista 2024)

- Demand for specific SKUs limits generic upsell

- Guided selling drives margin capture

- Content/expert advice increases conversion influence

Price transparency and dynamic pricing squeeze margins; loyalty, personalization protect revenue

High price transparency and dynamic pricing (Statista 2024: 85% consult reviews) compress margins on KVIs; fast fulfillment and service drive loyalty. Low switching costs and rising e-commerce (EU ~14.8% 2024) increase customer leverage; loyalty programs, financing and bundles mitigate churn. Peak events amplify discount pressure; personalization and guided selling preserve margins.

| Metric | Value |

|---|---|

| Reviews consulted | 85% (Statista 2024) |

| EU e‑commerce | ~14.8% (2024) |

Preview Before You Purchase

Nay Elektrodom AS Porter's Five Forces Analysis

This preview shows the Nay Elektrodom AS Porter's Five Forces Analysis and is the exact document you'll receive upon purchase. It is fully formatted, professionally written, and ready for immediate use. No placeholders or samples—what you see is what you’ll download instantly.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Nay Elektrodom AS faces moderate buyer power and intense rivalry from national retailers and e-commerce, while supplier influence is limited by brand diversity; threats from new entrants and substitutes are tempered by scale and logistics. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Nay Elektrodom AS.

Suppliers Bargaining Power

Global OEM concentration

Major categories at NAY rely on a few global brands—Samsung, Apple, LG, Bosch and HP—whose scale translates into leverage over pricing, allocation and marketing terms; Apple alone reported $383 billion revenue in FY2024, underscoring supplier clout. Limited product differentiation in retail increases brand power over shelf space and promotions. NAY mitigates this with multi-brand assortments and volume-based purchase commitments to secure better terms.

Distributor intermediation

Regional distributors between NAY and OEMs add margin layers—commonly 5–12% in CE channels in 2024—reducing NAY’s direct negotiating leverage and visibility into allocations. Building direct OEM accounts where feasible has been shown to improve net terms and exclusivity, often trimming costs by 1–3% and shortening lead times. Implementing dual-sourcing for key SKUs hedges allocation risk and has cut peak-season stockouts by roughly 25–35% in comparable retailers.

Supply chain constraints

Cyclic chip shortages and logistics bottlenecks in 2024 kept semiconductor lead times elevated (around 14 weeks) and shifted pricing power to suppliers, with allocation favoring large, multi-country buyers and pressuring domestic chains. NAY, serving Slovakia (5.4M population), benefits from national scale but remains modest versus pan-EU retailers. Early ordering and vendor-managed inventory (VMI) — shown to cut stockouts/inventory by ~20–30% — can soften shocks.

Brand-led MAP and promotions

OEMs enforce MAP, co-op budgets and promo calendars (co-op funds commonly 1–3% of retail sales in 2024), and NAY must comply to access hero SKUs and marketing funds, which constrains pricing flexibility on flagship products and compresses margin on promoted lines.

- MAP limits discounting

- Co-op funds 1–3% (2024)

- Access tied to compliance

- Private-label & service bundles recover margin

After-sales dependency

After-sales repairs and warranties for NAY Elektrodom rely on OEM parts and brand authorization, which gives suppliers leverage over turnaround times and reimbursement rates; as of 2024 major manufacturers maintain warranty authorization requirements across the Baltic retail channel. Strong service SLAs protect NAY’s reputation but tie repair workflows to OEM policies, while investment in certified service capacity reduces dependency and strengthens negotiating position.

- OEM authorization required

- Suppliers set turnaround/reimbursement

- Service SLAs protect brand

- Certified service investment = higher bargaining power

Supplier leverage, ~14-week chip lead times and 5-12% distributor margins

Suppliers (Samsung, Apple, LG, Bosch, HP) hold strong leverage—Apple revenue $383B (FY2024), MAP and co-op funds 1–3% limit NAY pricing; distributor layers add 5–12% margin. Chip lead times ~14 weeks (2024) favor large buyers; VMI/early ordering cuts stockouts ~20–30%. Certified service capacity improves NAY bargaining on warranties and turnarounds.

| Metric | 2024 |

|---|---|

| Apple rev | $383B |

| Distributor margin | 5–12% |

| Co-op/MAP | 1–3% |

| Chip LT | ~14w |

What is included in the product

Tailored Porter's Five Forces for Nay Elektrodom AS revealing competitive intensity, buyer/supplier power, threat of new entrants and substitutes, plus strategic barriers protecting its market position.

A concise one-sheet Porter's Five Forces summary for Nay Elektrodom—instantly visualize competitive pressure with a spider chart, customize force levels for shifting retail, supplier and regulatory dynamics, and drop directly into pitch decks or dashboards for fast decision-making.

Customers Bargaining Power

High price transparency

High price transparency in 2024 lets customers compare Alza, Datart, Mall and marketplace offers instantly, compressing gross margins on KVIs such as smartphones and TVs into low single-digit bands. Dynamic pricing engines and price-match policies are now standard expectations across retailers. Competitive differentiation shifts to availability, fulfillment speed and after-sales service.

Low switching costs

Low switching costs let shoppers pivot with a click as e-commerce captured 13.6% of EU retail in 2023 and Estonia records 92% internet use (Eurostat 2023), making loyalty fragile without tangible perks; NAY can anchor repeat purchases with loyalty programs, point-of-sale financing and bundle offers, while click-and-collect convenience lowers churn.

Service-sensitive segments

Service-sensitive segments wield higher bargaining power for Nay Elektrodom as installation, haul-away and extended warranties for large appliances justify premiums and limit pure price competition. Clear SLAs and next-day delivery—cited by 2024 consumer surveys as a top 3 purchase driver—increase perceived value and brand stickiness. Business customers additionally prioritize invoicing terms and post-sale technical support, shifting negotiations toward service levels rather than unit price.

Demand volatility and seasonality

Demand volatility around Black Friday, back-to-school and holiday peaks concentrates customer leverage as shoppers time purchases and expect steep discounts, forcing NAY to lock promotional stock and plan tiered offers well before peak windows to avoid stockouts and margin erosion. Deal-seeking behavior amplifies discount expectations, while targeted personalized offers on non-promoted lines help preserve margins and increase attachment rates.

- Peak events concentrate leverage

- Early promo inventory commitments

- Tiered offers reduce margin hit

- Personalization protects non-promoted margins

Product information abundance

Product information abundance sharply reduces information asymmetry: Statista 2024 found 85% of electronics shoppers consult reviews and specs before purchase, empowering customers to demand exact SKUs and features and narrowing upsell opportunities for Nay Elektrodom AS. Guided-selling tools and personalized recommendations can redirect choices toward higher-margin alternatives, while rich content and expert advice reclaim influence at the point of decision.

- Reviews/specs cut information asymmetry — 85% consult reviews (Statista 2024)

- Demand for specific SKUs limits generic upsell

- Guided selling drives margin capture

- Content/expert advice increases conversion influence

Price transparency and dynamic pricing squeeze margins; loyalty, personalization protect revenue

High price transparency and dynamic pricing (Statista 2024: 85% consult reviews) compress margins on KVIs; fast fulfillment and service drive loyalty. Low switching costs and rising e-commerce (EU ~14.8% 2024) increase customer leverage; loyalty programs, financing and bundles mitigate churn. Peak events amplify discount pressure; personalization and guided selling preserve margins.

| Metric | Value |

|---|---|

| Reviews consulted | 85% (Statista 2024) |

| EU e‑commerce | ~14.8% (2024) |

Preview Before You Purchase

Nay Elektrodom AS Porter's Five Forces Analysis

This preview shows the Nay Elektrodom AS Porter's Five Forces Analysis and is the exact document you'll receive upon purchase. It is fully formatted, professionally written, and ready for immediate use. No placeholders or samples—what you see is what you’ll download instantly.