Ningbo Huaxiang Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

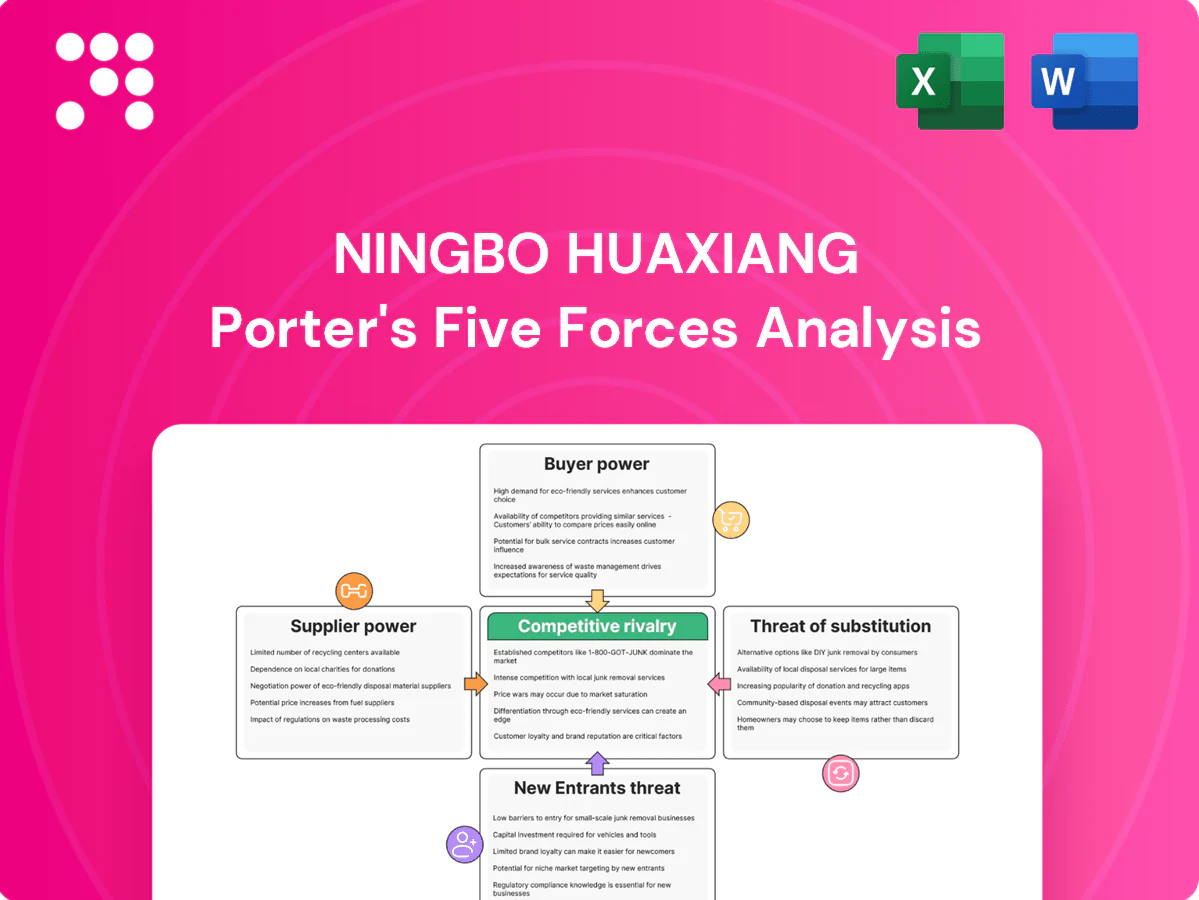

Ningbo Huaxiang faces moderate supplier power due to specialized port services, strong buyer negotiating leverage from major shippers, and elevated rivalry as regional terminals compete on price and capacity; barriers to entry are high but tech-enabled substitutes like inland hubs pose growing risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ningbo Huaxiang’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated resin and electronics sources

Key raw materials such as engineering plastics, coatings, LEDs and chips are sourced from a limited pool of qualified Tier 2 suppliers, and certification plus PPAP requirements typically delay supplier switching by 6–12 months in 2024. This concentration gives suppliers measurable price influence, especially during tight supply cycles. Ningbo Huaxiang's dual sourcing reduces exposure but does not fully eliminate supplier-driven cost or lead-time risk.

High tooling and mold dependence

Complex injection molds and automated painting lines are mission-critical and capital-intensive, with molds costing $50,000–$500,000 and painting lines requiring $2–8 million CAPEX (2024). Specialist tooling suppliers with proprietary capabilities often secure 10–20% price premia and preferred terms. Lead times of 16–30 weeks raise switching costs, and any delay can directly jeopardize program launch timelines.

Commodity price volatility passthrough

In 2024 oil-linked polymer and metal input swings increased cost volatility, pressuring Huaxiang’s margins; OEM contracts permit partial passthrough but typically with multi-month lag, while suppliers imposed surcharges when input spikes occurred, and these timing mismatches compressed reported profitability for the port operator.

Local cluster scale in China

China's dense supplier clusters around Ningbo deliver cost and logistics advantages, with Ningbo‑Zhoushan Port handling 1.31 billion tonnes and 34.49 million TEU in 2023, underpinning abundant local capacity that tempers supplier pricing power and fosters competition. Localization cuts freight and tariff exposure and proximity enables just-in-time reliability for Ningbo Huaxiang’s operations.

- Local capacity: high — reduces supplier leverage

- Logistics: lower freight/tariff risk

- Reliability: supports JIT

ESG and compliance tightening

Traceability, REACH and RoHS requirements and emerging recyclate-content rules sharply limit qualified suppliers; REACH lists over 24,000 registered substances (2024) and RoHS spans 10 product categories, narrowing the pool and modestly increasing supplier leverage. Audits and sustainability-data reporting raise supplier overheads and procurement costs. Non-compliance risk forces dependency on vetted partners, elevating switching costs.

- Traceability: digital product passports expanding in 2024

- REACH: >24,000 substances (2024)

- RoHS: 10 product categories

- Effect: smaller supplier pool → higher leverage

Supplier concentration 2024: tooling, lead times and regulation deepen pricing power

Supplier concentration in 2024 gives measurable pricing power—qualified Tier‑2 leads and certifications delay switching 6–12 months—while dual sourcing limits but does not remove cost/lead‑time risk. Capital‑intensive tooling (molds $50k–$500k; painting lines $2–8m) and 16–30 week lead times raise switching costs; input volatility and regulatory traceability (REACH >24,000 substances) further tighten supplier leverage.

| Factor | 2024 data |

|---|---|

| Supplier pool | Concentrated; switching 6–12 months |

| Tooling/CAPEX | Molds $50k–$500k; lines $2–8m |

| Lead times | 16–30 weeks |

| Port scale | Ningbo‑Zhoushan 1.31bn t; 34.49M TEU (2023) |

| Regulation | REACH >24,000 substances; RoHS 10 categories |

What is included in the product

Concise Porter’s Five Forces assessment of Ningbo Huaxiang highlighting competitive rivalry, supplier and buyer bargaining power, threats from new entrants and substitutes, and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Ningbo Huaxiang—instantly spot competitive pressures, supplier risks, and substitute threats to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Few large OEM customers

Global automakers and Tier 1 system integrators account for over 70% of Ningbo Huaxiang’s volumes in 2024, yet remain highly concentrated—top 5 OEMs represent roughly 40% of purchase demand; their scale delivers strong negotiating leverage. Vendor scorecards link volume tiers to price/quality, often adjusting unit pricing by 5–10% annually. High switching risk from qualification and tooling keeps pricing pressure persistent.

Platform lifecycle lock in

Design-in at program award secures multi-year volumes—industry platform awards averaged 3–7 years in 2024—giving Ningbo Huaxiang leverage. Buyers, however, demanded ~3% annual cost-downs in 2024, and engineering changes can reset commercial terms. Retaining awards requires strict performance and 100% PPAP FAI plus >95% on-time delivery.

Stringent quality and delivery terms

Stringent PPM targets (2024 industry benchmark ~50 PPM) plus warranty liabilities and JIT penalties shift quality and timing risk to suppliers. Buyers impose chargebacks for defects and delays (commonly clawbacks of 1–3% of shipment value), tightening supplier margins and increasing working capital needs. This escalates buyer power beyond price through operational and financial levers.

Global footprint expectations

OEMs in 2024 prefer suppliers that mirror their global footprints, narrowing eligible vendors and forcing port-linked capex to support multi-region operations; mandatory local content rules in key markets increase compliance costs, and large buyers leverage cross-border sourcing to extract price and service concessions.

- Global OEM follow-the-supplier demand

- Footprint limits vendor pool

- Local content compliance mandatory

- Buyers extract concessions via sourcing

Modular integration trend

OEMs and large Tier 1s increasingly bundle trims, lighting and electronics into modules, with module content share rising to about 40% of interior/lighting sourcing in 2024, boosting buyers' negotiating clout and compressing margins for single-scope suppliers. Smaller-scope vendors face disintermediation unless they move up the value chain. Huaxiang must offer integrated system solutions and demonstrate module-level cost and quality advantages to defend pricing.

- Higher buyer leverage: module share ~40% (2024)

- Risk: disintermediation of niche suppliers

- Defense: Huaxiang to pivot to system solutions

Buyer concentration >70%, top-5 OEMs ~40%, cost-downs ~3%

Buyers concentrate >70% volumes with top‑5 OEMs ≈40% in 2024, forcing 5–10% annual price tiers and ~3% mandated cost‑downs; qualification/tooling and 3–7y program awards keep switching costs high. Quality targets (~50 PPM) and chargebacks (1–3% shipment value) shift margin risk to suppliers; module share ≈40% raises disintermediation risk unless Huaxiang offers integrated systems.

| Metric | 2024 Value |

|---|---|

| Buyer concentration | >70% |

| Top‑5 OEM share | ~40% |

| Program length | 3–7 years |

| Annual cost‑down demand | ~3% |

| PPM benchmark | ~50 |

| Chargebacks | 1–3% shipment value |

| Module share | ~40% |

Full Version Awaits

Ningbo Huaxiang Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Ningbo Huaxiang you'll receive immediately after purchase—no placeholders or samples. The document displayed is the final, professionally formatted file ready for download and use the moment you buy. You’re viewing the actual deliverable, available instantly upon payment.

A Must-Have Tool for Decision-Makers

Ningbo Huaxiang faces moderate supplier power due to specialized port services, strong buyer negotiating leverage from major shippers, and elevated rivalry as regional terminals compete on price and capacity; barriers to entry are high but tech-enabled substitutes like inland hubs pose growing risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ningbo Huaxiang’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated resin and electronics sources

Key raw materials such as engineering plastics, coatings, LEDs and chips are sourced from a limited pool of qualified Tier 2 suppliers, and certification plus PPAP requirements typically delay supplier switching by 6–12 months in 2024. This concentration gives suppliers measurable price influence, especially during tight supply cycles. Ningbo Huaxiang's dual sourcing reduces exposure but does not fully eliminate supplier-driven cost or lead-time risk.

High tooling and mold dependence

Complex injection molds and automated painting lines are mission-critical and capital-intensive, with molds costing $50,000–$500,000 and painting lines requiring $2–8 million CAPEX (2024). Specialist tooling suppliers with proprietary capabilities often secure 10–20% price premia and preferred terms. Lead times of 16–30 weeks raise switching costs, and any delay can directly jeopardize program launch timelines.

Commodity price volatility passthrough

In 2024 oil-linked polymer and metal input swings increased cost volatility, pressuring Huaxiang’s margins; OEM contracts permit partial passthrough but typically with multi-month lag, while suppliers imposed surcharges when input spikes occurred, and these timing mismatches compressed reported profitability for the port operator.

Local cluster scale in China

China's dense supplier clusters around Ningbo deliver cost and logistics advantages, with Ningbo‑Zhoushan Port handling 1.31 billion tonnes and 34.49 million TEU in 2023, underpinning abundant local capacity that tempers supplier pricing power and fosters competition. Localization cuts freight and tariff exposure and proximity enables just-in-time reliability for Ningbo Huaxiang’s operations.

- Local capacity: high — reduces supplier leverage

- Logistics: lower freight/tariff risk

- Reliability: supports JIT

ESG and compliance tightening

Traceability, REACH and RoHS requirements and emerging recyclate-content rules sharply limit qualified suppliers; REACH lists over 24,000 registered substances (2024) and RoHS spans 10 product categories, narrowing the pool and modestly increasing supplier leverage. Audits and sustainability-data reporting raise supplier overheads and procurement costs. Non-compliance risk forces dependency on vetted partners, elevating switching costs.

- Traceability: digital product passports expanding in 2024

- REACH: >24,000 substances (2024)

- RoHS: 10 product categories

- Effect: smaller supplier pool → higher leverage

Supplier concentration 2024: tooling, lead times and regulation deepen pricing power

Supplier concentration in 2024 gives measurable pricing power—qualified Tier‑2 leads and certifications delay switching 6–12 months—while dual sourcing limits but does not remove cost/lead‑time risk. Capital‑intensive tooling (molds $50k–$500k; painting lines $2–8m) and 16–30 week lead times raise switching costs; input volatility and regulatory traceability (REACH >24,000 substances) further tighten supplier leverage.

| Factor | 2024 data |

|---|---|

| Supplier pool | Concentrated; switching 6–12 months |

| Tooling/CAPEX | Molds $50k–$500k; lines $2–8m |

| Lead times | 16–30 weeks |

| Port scale | Ningbo‑Zhoushan 1.31bn t; 34.49M TEU (2023) |

| Regulation | REACH >24,000 substances; RoHS 10 categories |

What is included in the product

Concise Porter’s Five Forces assessment of Ningbo Huaxiang highlighting competitive rivalry, supplier and buyer bargaining power, threats from new entrants and substitutes, and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Ningbo Huaxiang—instantly spot competitive pressures, supplier risks, and substitute threats to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Few large OEM customers

Global automakers and Tier 1 system integrators account for over 70% of Ningbo Huaxiang’s volumes in 2024, yet remain highly concentrated—top 5 OEMs represent roughly 40% of purchase demand; their scale delivers strong negotiating leverage. Vendor scorecards link volume tiers to price/quality, often adjusting unit pricing by 5–10% annually. High switching risk from qualification and tooling keeps pricing pressure persistent.

Platform lifecycle lock in

Design-in at program award secures multi-year volumes—industry platform awards averaged 3–7 years in 2024—giving Ningbo Huaxiang leverage. Buyers, however, demanded ~3% annual cost-downs in 2024, and engineering changes can reset commercial terms. Retaining awards requires strict performance and 100% PPAP FAI plus >95% on-time delivery.

Stringent quality and delivery terms

Stringent PPM targets (2024 industry benchmark ~50 PPM) plus warranty liabilities and JIT penalties shift quality and timing risk to suppliers. Buyers impose chargebacks for defects and delays (commonly clawbacks of 1–3% of shipment value), tightening supplier margins and increasing working capital needs. This escalates buyer power beyond price through operational and financial levers.

Global footprint expectations

OEMs in 2024 prefer suppliers that mirror their global footprints, narrowing eligible vendors and forcing port-linked capex to support multi-region operations; mandatory local content rules in key markets increase compliance costs, and large buyers leverage cross-border sourcing to extract price and service concessions.

- Global OEM follow-the-supplier demand

- Footprint limits vendor pool

- Local content compliance mandatory

- Buyers extract concessions via sourcing

Modular integration trend

OEMs and large Tier 1s increasingly bundle trims, lighting and electronics into modules, with module content share rising to about 40% of interior/lighting sourcing in 2024, boosting buyers' negotiating clout and compressing margins for single-scope suppliers. Smaller-scope vendors face disintermediation unless they move up the value chain. Huaxiang must offer integrated system solutions and demonstrate module-level cost and quality advantages to defend pricing.

- Higher buyer leverage: module share ~40% (2024)

- Risk: disintermediation of niche suppliers

- Defense: Huaxiang to pivot to system solutions

Buyer concentration >70%, top-5 OEMs ~40%, cost-downs ~3%

Buyers concentrate >70% volumes with top‑5 OEMs ≈40% in 2024, forcing 5–10% annual price tiers and ~3% mandated cost‑downs; qualification/tooling and 3–7y program awards keep switching costs high. Quality targets (~50 PPM) and chargebacks (1–3% shipment value) shift margin risk to suppliers; module share ≈40% raises disintermediation risk unless Huaxiang offers integrated systems.

| Metric | 2024 Value |

|---|---|

| Buyer concentration | >70% |

| Top‑5 OEM share | ~40% |

| Program length | 3–7 years |

| Annual cost‑down demand | ~3% |

| PPM benchmark | ~50 |

| Chargebacks | 1–3% shipment value |

| Module share | ~40% |

Full Version Awaits

Ningbo Huaxiang Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Ningbo Huaxiang you'll receive immediately after purchase—no placeholders or samples. The document displayed is the final, professionally formatted file ready for download and use the moment you buy. You’re viewing the actual deliverable, available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Ningbo Huaxiang faces moderate supplier power due to specialized port services, strong buyer negotiating leverage from major shippers, and elevated rivalry as regional terminals compete on price and capacity; barriers to entry are high but tech-enabled substitutes like inland hubs pose growing risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ningbo Huaxiang’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated resin and electronics sources

Key raw materials such as engineering plastics, coatings, LEDs and chips are sourced from a limited pool of qualified Tier 2 suppliers, and certification plus PPAP requirements typically delay supplier switching by 6–12 months in 2024. This concentration gives suppliers measurable price influence, especially during tight supply cycles. Ningbo Huaxiang's dual sourcing reduces exposure but does not fully eliminate supplier-driven cost or lead-time risk.

High tooling and mold dependence

Complex injection molds and automated painting lines are mission-critical and capital-intensive, with molds costing $50,000–$500,000 and painting lines requiring $2–8 million CAPEX (2024). Specialist tooling suppliers with proprietary capabilities often secure 10–20% price premia and preferred terms. Lead times of 16–30 weeks raise switching costs, and any delay can directly jeopardize program launch timelines.

Commodity price volatility passthrough

In 2024 oil-linked polymer and metal input swings increased cost volatility, pressuring Huaxiang’s margins; OEM contracts permit partial passthrough but typically with multi-month lag, while suppliers imposed surcharges when input spikes occurred, and these timing mismatches compressed reported profitability for the port operator.

Local cluster scale in China

China's dense supplier clusters around Ningbo deliver cost and logistics advantages, with Ningbo‑Zhoushan Port handling 1.31 billion tonnes and 34.49 million TEU in 2023, underpinning abundant local capacity that tempers supplier pricing power and fosters competition. Localization cuts freight and tariff exposure and proximity enables just-in-time reliability for Ningbo Huaxiang’s operations.

- Local capacity: high — reduces supplier leverage

- Logistics: lower freight/tariff risk

- Reliability: supports JIT

ESG and compliance tightening

Traceability, REACH and RoHS requirements and emerging recyclate-content rules sharply limit qualified suppliers; REACH lists over 24,000 registered substances (2024) and RoHS spans 10 product categories, narrowing the pool and modestly increasing supplier leverage. Audits and sustainability-data reporting raise supplier overheads and procurement costs. Non-compliance risk forces dependency on vetted partners, elevating switching costs.

- Traceability: digital product passports expanding in 2024

- REACH: >24,000 substances (2024)

- RoHS: 10 product categories

- Effect: smaller supplier pool → higher leverage

Supplier concentration 2024: tooling, lead times and regulation deepen pricing power

Supplier concentration in 2024 gives measurable pricing power—qualified Tier‑2 leads and certifications delay switching 6–12 months—while dual sourcing limits but does not remove cost/lead‑time risk. Capital‑intensive tooling (molds $50k–$500k; painting lines $2–8m) and 16–30 week lead times raise switching costs; input volatility and regulatory traceability (REACH >24,000 substances) further tighten supplier leverage.

| Factor | 2024 data |

|---|---|

| Supplier pool | Concentrated; switching 6–12 months |

| Tooling/CAPEX | Molds $50k–$500k; lines $2–8m |

| Lead times | 16–30 weeks |

| Port scale | Ningbo‑Zhoushan 1.31bn t; 34.49M TEU (2023) |

| Regulation | REACH >24,000 substances; RoHS 10 categories |

What is included in the product

Concise Porter’s Five Forces assessment of Ningbo Huaxiang highlighting competitive rivalry, supplier and buyer bargaining power, threats from new entrants and substitutes, and strategic levers to protect margins.

Clear one-sheet Porter's Five Forces for Ningbo Huaxiang—instantly spot competitive pressures, supplier risks, and substitute threats to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Few large OEM customers

Global automakers and Tier 1 system integrators account for over 70% of Ningbo Huaxiang’s volumes in 2024, yet remain highly concentrated—top 5 OEMs represent roughly 40% of purchase demand; their scale delivers strong negotiating leverage. Vendor scorecards link volume tiers to price/quality, often adjusting unit pricing by 5–10% annually. High switching risk from qualification and tooling keeps pricing pressure persistent.

Platform lifecycle lock in

Design-in at program award secures multi-year volumes—industry platform awards averaged 3–7 years in 2024—giving Ningbo Huaxiang leverage. Buyers, however, demanded ~3% annual cost-downs in 2024, and engineering changes can reset commercial terms. Retaining awards requires strict performance and 100% PPAP FAI plus >95% on-time delivery.

Stringent quality and delivery terms

Stringent PPM targets (2024 industry benchmark ~50 PPM) plus warranty liabilities and JIT penalties shift quality and timing risk to suppliers. Buyers impose chargebacks for defects and delays (commonly clawbacks of 1–3% of shipment value), tightening supplier margins and increasing working capital needs. This escalates buyer power beyond price through operational and financial levers.

Global footprint expectations

OEMs in 2024 prefer suppliers that mirror their global footprints, narrowing eligible vendors and forcing port-linked capex to support multi-region operations; mandatory local content rules in key markets increase compliance costs, and large buyers leverage cross-border sourcing to extract price and service concessions.

- Global OEM follow-the-supplier demand

- Footprint limits vendor pool

- Local content compliance mandatory

- Buyers extract concessions via sourcing

Modular integration trend

OEMs and large Tier 1s increasingly bundle trims, lighting and electronics into modules, with module content share rising to about 40% of interior/lighting sourcing in 2024, boosting buyers' negotiating clout and compressing margins for single-scope suppliers. Smaller-scope vendors face disintermediation unless they move up the value chain. Huaxiang must offer integrated system solutions and demonstrate module-level cost and quality advantages to defend pricing.

- Higher buyer leverage: module share ~40% (2024)

- Risk: disintermediation of niche suppliers

- Defense: Huaxiang to pivot to system solutions

Buyer concentration >70%, top-5 OEMs ~40%, cost-downs ~3%

Buyers concentrate >70% volumes with top‑5 OEMs ≈40% in 2024, forcing 5–10% annual price tiers and ~3% mandated cost‑downs; qualification/tooling and 3–7y program awards keep switching costs high. Quality targets (~50 PPM) and chargebacks (1–3% shipment value) shift margin risk to suppliers; module share ≈40% raises disintermediation risk unless Huaxiang offers integrated systems.

| Metric | 2024 Value |

|---|---|

| Buyer concentration | >70% |

| Top‑5 OEM share | ~40% |

| Program length | 3–7 years |

| Annual cost‑down demand | ~3% |

| PPM benchmark | ~50 |

| Chargebacks | 1–3% shipment value |

| Module share | ~40% |

Full Version Awaits

Ningbo Huaxiang Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Ningbo Huaxiang you'll receive immediately after purchase—no placeholders or samples. The document displayed is the final, professionally formatted file ready for download and use the moment you buy. You’re viewing the actual deliverable, available instantly upon payment.