NEC Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

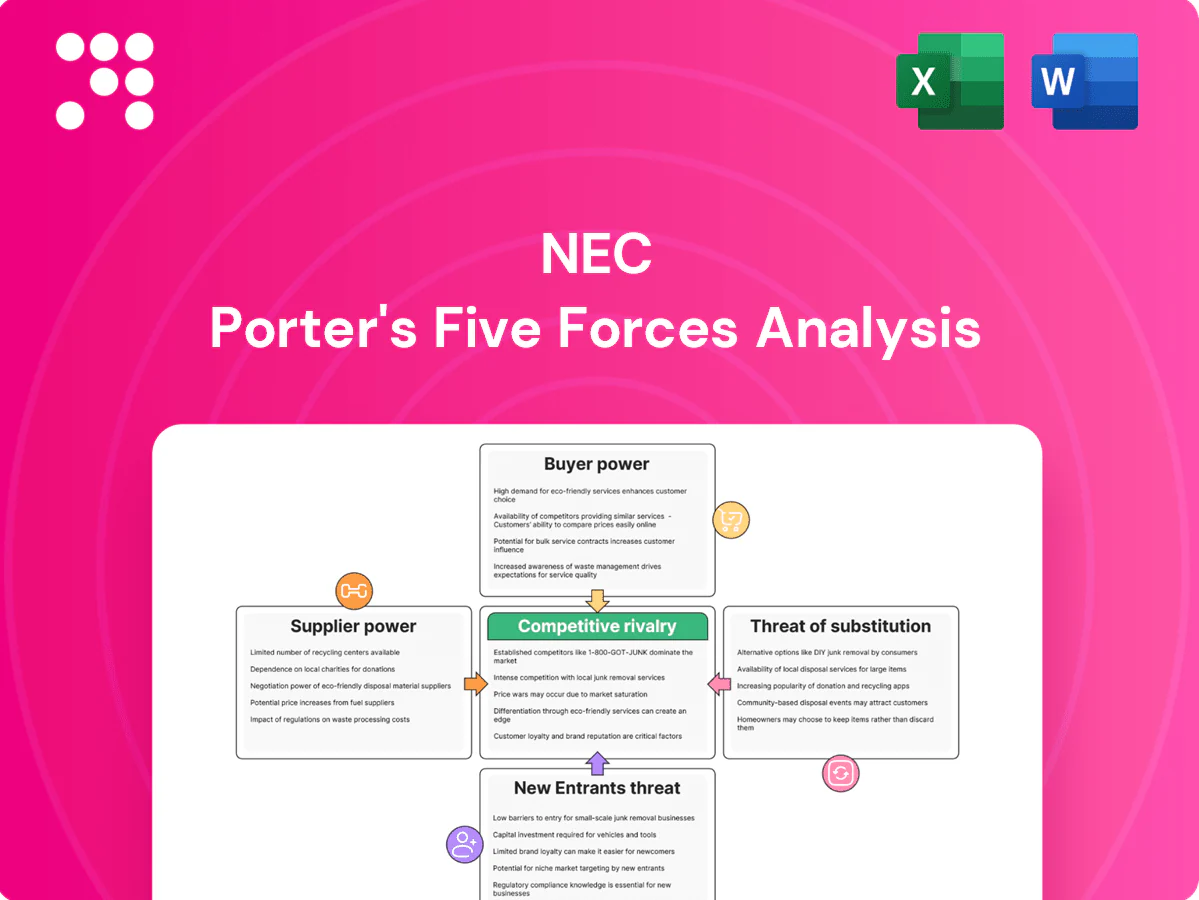

NEC's Porter's Five Forces snapshot highlights how supplier leverage, buyer power, rivalry, substitutes, and entry barriers shape its competitive edge and strategic risks; this brief only scratches the surface. Unlock the full report for force-by-force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialized component dependence

NEC depends on advanced semiconductors, optics and telecom-grade components where a few global suppliers dominate; TSMC alone held about 55% of global foundry revenue in 2024, concentrating pricing and lead-time risk. This supplier concentration can extend lead times and boost niche-part pricing. NEC mitigates via multi-sourcing and design-for-availability, but supply shocks can still ripple through systems-integration timelines.

Software and IP licensing

Critical software stacks, AI frameworks, and cybersecurity tools often require licensed IP; vendors with differentiated IP can command higher fees or restrictive terms, influencing NEC's margins. NEC negotiates enterprise agreements and builds in-house alternatives to reduce lock-in, with the global enterprise software market surpassing $600 billion in 2024. Open-source adoption helps balance bargaining power but increases integration effort and maintenance burden.

Cloud and network ecosystem partners

Partnerships with hyperscalers (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11% of global cloud market in 2024) and network technology allies are essential for NEC’s hybrid solutions but give partners leverage over product roadmaps and margins via certification and marketplace rules, often involving 20–30% marketplace fees. Co-selling can offset imbalances by enabling larger TAM deals, yet reliance on partner APIs and updates can shift control away from NEC.

Manufacturing and ODM relationships

For devices and displays NEC relies on large EMS/ODM partners; 2024 industry scale (contract manufacturing ~USD 550bn) lets suppliers demand premiums. Volume commitments and multi-year contracts secure capacity but reduce sourcing agility; quality, yield and logistics performance drive supplier leverage. Dual-sourcing and regional diversification (APAC/EU/North America) limit disruption and cost swings.

- Scale concentration: benefits suppliers

- Long-term deals: capacity vs flexibility

- Quality/yield = negotiation power

- Dual-source/regional mix reduces risk

Standards and interoperability constraints

Telecom and public-safety standards (3GPP ~18-month release cadence in 2024) restrict supplier substitution without costly revalidation; certification cycles typically span 12–24 months and revalidation can cost up to $1M, raising NEC’s switching costs. Suppliers meeting stringent standards command pricing latitude, often a 10–15% premium. NEC’s modular architectures aim to preserve swap-out options over time.

- Standards cadence: 3GPP ~18 months (2024)

- Certification cycle: 12–24 months

- Revalidation cost: up to $1M

- Supplier premium: ~10–15%

Supply concentration, hyperscaler fees and certification costs raise high switching risk

NEC faces concentrated suppliers (TSMC 55% foundry 2024), proprietary software vendors and hyperscalers (AWS 32%, Azure 23%, GCP 11% 2024) that raise costs and switching time; certification cycles 12–24 months and revalidation up to $1M increase switching costs. NEC uses multi-sourcing, modular design and partner agreements to mitigate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| TSMC | 55% foundry rev | Pricing/lead-time risk |

| Hyperscalers | AWS32%/Azure23%/GCP11% | Marketplace fees, roadmap leverage |

| Contract mfg | ~USD550bn | Capacity premiums |

| Certification | 12–24m / ~$1M | High switching cost |

What is included in the product

Tailored Porter's Five Forces analysis for NEC that uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and emerging threats to inform strategic decisions and investor materials.

A single-sheet NEC Porter's Five Forces summary with customizable pressure sliders and instant spider chart—simplifies competitive analysis for fast decisions and copy-ready slides.

Customers Bargaining Power

Large enterprise and government RFPs

Governments and large CSPs buy through competitive tenders with strict SLAs and penalties, forcing NEC to accept tight delivery and uptime commitments. Their scale drives aggressive pricing and demands for customization, while multi-year framework agreements (typically 3–5 years) compress margins but give predictable revenue. NEC defends value through security certifications, carrier-grade reliability, and systems integration capabilities. This mix raises customer bargaining power but preserves premium for differentiated solutions.

High switching costs, but savvy buyers

Integrated IT-network solutions embed deeply in operations, raising technical and organizational switching costs; NEC reported about 3.4 trillion yen in consolidated revenue for FY2023 (year to March 2024), underscoring scale. Buyers leverage pilot phases and proof-of-concepts to reduce asymmetry, yet even with lock-in they insist on service credits and roadmap commitments. NEC counters with lifecycle support and open interfaces to ease customer concerns.

Outcome-based and subscription models

Clients increasingly prefer OPEX, managed services and outcome-linked pricing, shifting risk to vendors and intensifying price scrutiny; IDC estimated the global managed services market at about $300B in 2024, reflecting this shift. Benchmarking across providers and transparent SLAs enhances buyer leverage and compresses margins. NEC bundles software, services and maintenance to stabilize ARPU and offset contract risk.

Security and compliance requirements

Public safety and critical infrastructure buyers increasingly mandate certifications such as ISO/IEC 27001, NIST CSF and SOC 2 plus regular audits, narrowing the pool of qualified vendors and partially softening buyer switching power. Compliance obligations allow buyers to demand tailored features at vendor expense, raising customization pressure. NEC’s long track record and certifications boost trust but increase cost-to-serve.

- Certifications: ISO/IEC 27001, NIST CSF, SOC 2

- Market effect: fewer qualified vendors → reduced buyer options

- Commercial impact: higher customization cost absorbed by vendors

Global alternatives and multi-vendor strategies

Clients often split awards among multiple vendors to avoid dependence, with multi-vendor sourcing now used by roughly half of large operators; international competitors enable cross-border price comparisons, driving continuous re-bidding and renegotiation. NEC leans on reference architectures and integration prowess to remain a preferred vendor in a global telecom equipment market ~140 billion USD in 2024.

- Multi-vendor adoption ~50%

- Global market ~140B USD (2024)

- Continuous re-bidding increases price pressure

- NEC advantage: reference architectures + integration

Tenders, strict SLAs and OPEX managed services ($300B) empower buyers

Large government and CSP buyers use competitive tenders, strict SLAs and multi‑year (3–5y) frameworks to pressure pricing and customization, raising customer bargaining power despite NEC’s security certifications and carrier-grade integration. OPEX/managed models (global managed services ≈ $300B 2024) increase price scrutiny; multi-vendor sourcing ~50% reduces lock‑in.

| Metric | Value |

|---|---|

| NEC FY2023 revenue | ¥3.4T |

| Managed services market 2024 | $300B |

| Telecom equip. market 2024 | $140B |

| Multi-vendor adoption | ~50% |

Preview Before You Purchase

NEC Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of NEC you'll receive after purchase—fully formatted and ready for use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. Instant download upon payment—no placeholders, mockups, or surprises.

A Must-Have Tool for Decision-Makers

NEC's Porter's Five Forces snapshot highlights how supplier leverage, buyer power, rivalry, substitutes, and entry barriers shape its competitive edge and strategic risks; this brief only scratches the surface. Unlock the full report for force-by-force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialized component dependence

NEC depends on advanced semiconductors, optics and telecom-grade components where a few global suppliers dominate; TSMC alone held about 55% of global foundry revenue in 2024, concentrating pricing and lead-time risk. This supplier concentration can extend lead times and boost niche-part pricing. NEC mitigates via multi-sourcing and design-for-availability, but supply shocks can still ripple through systems-integration timelines.

Software and IP licensing

Critical software stacks, AI frameworks, and cybersecurity tools often require licensed IP; vendors with differentiated IP can command higher fees or restrictive terms, influencing NEC's margins. NEC negotiates enterprise agreements and builds in-house alternatives to reduce lock-in, with the global enterprise software market surpassing $600 billion in 2024. Open-source adoption helps balance bargaining power but increases integration effort and maintenance burden.

Cloud and network ecosystem partners

Partnerships with hyperscalers (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11% of global cloud market in 2024) and network technology allies are essential for NEC’s hybrid solutions but give partners leverage over product roadmaps and margins via certification and marketplace rules, often involving 20–30% marketplace fees. Co-selling can offset imbalances by enabling larger TAM deals, yet reliance on partner APIs and updates can shift control away from NEC.

Manufacturing and ODM relationships

For devices and displays NEC relies on large EMS/ODM partners; 2024 industry scale (contract manufacturing ~USD 550bn) lets suppliers demand premiums. Volume commitments and multi-year contracts secure capacity but reduce sourcing agility; quality, yield and logistics performance drive supplier leverage. Dual-sourcing and regional diversification (APAC/EU/North America) limit disruption and cost swings.

- Scale concentration: benefits suppliers

- Long-term deals: capacity vs flexibility

- Quality/yield = negotiation power

- Dual-source/regional mix reduces risk

Standards and interoperability constraints

Telecom and public-safety standards (3GPP ~18-month release cadence in 2024) restrict supplier substitution without costly revalidation; certification cycles typically span 12–24 months and revalidation can cost up to $1M, raising NEC’s switching costs. Suppliers meeting stringent standards command pricing latitude, often a 10–15% premium. NEC’s modular architectures aim to preserve swap-out options over time.

- Standards cadence: 3GPP ~18 months (2024)

- Certification cycle: 12–24 months

- Revalidation cost: up to $1M

- Supplier premium: ~10–15%

Supply concentration, hyperscaler fees and certification costs raise high switching risk

NEC faces concentrated suppliers (TSMC 55% foundry 2024), proprietary software vendors and hyperscalers (AWS 32%, Azure 23%, GCP 11% 2024) that raise costs and switching time; certification cycles 12–24 months and revalidation up to $1M increase switching costs. NEC uses multi-sourcing, modular design and partner agreements to mitigate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| TSMC | 55% foundry rev | Pricing/lead-time risk |

| Hyperscalers | AWS32%/Azure23%/GCP11% | Marketplace fees, roadmap leverage |

| Contract mfg | ~USD550bn | Capacity premiums |

| Certification | 12–24m / ~$1M | High switching cost |

What is included in the product

Tailored Porter's Five Forces analysis for NEC that uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and emerging threats to inform strategic decisions and investor materials.

A single-sheet NEC Porter's Five Forces summary with customizable pressure sliders and instant spider chart—simplifies competitive analysis for fast decisions and copy-ready slides.

Customers Bargaining Power

Large enterprise and government RFPs

Governments and large CSPs buy through competitive tenders with strict SLAs and penalties, forcing NEC to accept tight delivery and uptime commitments. Their scale drives aggressive pricing and demands for customization, while multi-year framework agreements (typically 3–5 years) compress margins but give predictable revenue. NEC defends value through security certifications, carrier-grade reliability, and systems integration capabilities. This mix raises customer bargaining power but preserves premium for differentiated solutions.

High switching costs, but savvy buyers

Integrated IT-network solutions embed deeply in operations, raising technical and organizational switching costs; NEC reported about 3.4 trillion yen in consolidated revenue for FY2023 (year to March 2024), underscoring scale. Buyers leverage pilot phases and proof-of-concepts to reduce asymmetry, yet even with lock-in they insist on service credits and roadmap commitments. NEC counters with lifecycle support and open interfaces to ease customer concerns.

Outcome-based and subscription models

Clients increasingly prefer OPEX, managed services and outcome-linked pricing, shifting risk to vendors and intensifying price scrutiny; IDC estimated the global managed services market at about $300B in 2024, reflecting this shift. Benchmarking across providers and transparent SLAs enhances buyer leverage and compresses margins. NEC bundles software, services and maintenance to stabilize ARPU and offset contract risk.

Security and compliance requirements

Public safety and critical infrastructure buyers increasingly mandate certifications such as ISO/IEC 27001, NIST CSF and SOC 2 plus regular audits, narrowing the pool of qualified vendors and partially softening buyer switching power. Compliance obligations allow buyers to demand tailored features at vendor expense, raising customization pressure. NEC’s long track record and certifications boost trust but increase cost-to-serve.

- Certifications: ISO/IEC 27001, NIST CSF, SOC 2

- Market effect: fewer qualified vendors → reduced buyer options

- Commercial impact: higher customization cost absorbed by vendors

Global alternatives and multi-vendor strategies

Clients often split awards among multiple vendors to avoid dependence, with multi-vendor sourcing now used by roughly half of large operators; international competitors enable cross-border price comparisons, driving continuous re-bidding and renegotiation. NEC leans on reference architectures and integration prowess to remain a preferred vendor in a global telecom equipment market ~140 billion USD in 2024.

- Multi-vendor adoption ~50%

- Global market ~140B USD (2024)

- Continuous re-bidding increases price pressure

- NEC advantage: reference architectures + integration

Tenders, strict SLAs and OPEX managed services ($300B) empower buyers

Large government and CSP buyers use competitive tenders, strict SLAs and multi‑year (3–5y) frameworks to pressure pricing and customization, raising customer bargaining power despite NEC’s security certifications and carrier-grade integration. OPEX/managed models (global managed services ≈ $300B 2024) increase price scrutiny; multi-vendor sourcing ~50% reduces lock‑in.

| Metric | Value |

|---|---|

| NEC FY2023 revenue | ¥3.4T |

| Managed services market 2024 | $300B |

| Telecom equip. market 2024 | $140B |

| Multi-vendor adoption | ~50% |

Preview Before You Purchase

NEC Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of NEC you'll receive after purchase—fully formatted and ready for use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. Instant download upon payment—no placeholders, mockups, or surprises.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

NEC's Porter's Five Forces snapshot highlights how supplier leverage, buyer power, rivalry, substitutes, and entry barriers shape its competitive edge and strategic risks; this brief only scratches the surface. Unlock the full report for force-by-force ratings, visuals, and actionable insights to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialized component dependence

NEC depends on advanced semiconductors, optics and telecom-grade components where a few global suppliers dominate; TSMC alone held about 55% of global foundry revenue in 2024, concentrating pricing and lead-time risk. This supplier concentration can extend lead times and boost niche-part pricing. NEC mitigates via multi-sourcing and design-for-availability, but supply shocks can still ripple through systems-integration timelines.

Software and IP licensing

Critical software stacks, AI frameworks, and cybersecurity tools often require licensed IP; vendors with differentiated IP can command higher fees or restrictive terms, influencing NEC's margins. NEC negotiates enterprise agreements and builds in-house alternatives to reduce lock-in, with the global enterprise software market surpassing $600 billion in 2024. Open-source adoption helps balance bargaining power but increases integration effort and maintenance burden.

Cloud and network ecosystem partners

Partnerships with hyperscalers (AWS ~32%, Microsoft Azure ~23%, Google Cloud ~11% of global cloud market in 2024) and network technology allies are essential for NEC’s hybrid solutions but give partners leverage over product roadmaps and margins via certification and marketplace rules, often involving 20–30% marketplace fees. Co-selling can offset imbalances by enabling larger TAM deals, yet reliance on partner APIs and updates can shift control away from NEC.

Manufacturing and ODM relationships

For devices and displays NEC relies on large EMS/ODM partners; 2024 industry scale (contract manufacturing ~USD 550bn) lets suppliers demand premiums. Volume commitments and multi-year contracts secure capacity but reduce sourcing agility; quality, yield and logistics performance drive supplier leverage. Dual-sourcing and regional diversification (APAC/EU/North America) limit disruption and cost swings.

- Scale concentration: benefits suppliers

- Long-term deals: capacity vs flexibility

- Quality/yield = negotiation power

- Dual-source/regional mix reduces risk

Standards and interoperability constraints

Telecom and public-safety standards (3GPP ~18-month release cadence in 2024) restrict supplier substitution without costly revalidation; certification cycles typically span 12–24 months and revalidation can cost up to $1M, raising NEC’s switching costs. Suppliers meeting stringent standards command pricing latitude, often a 10–15% premium. NEC’s modular architectures aim to preserve swap-out options over time.

- Standards cadence: 3GPP ~18 months (2024)

- Certification cycle: 12–24 months

- Revalidation cost: up to $1M

- Supplier premium: ~10–15%

Supply concentration, hyperscaler fees and certification costs raise high switching risk

NEC faces concentrated suppliers (TSMC 55% foundry 2024), proprietary software vendors and hyperscalers (AWS 32%, Azure 23%, GCP 11% 2024) that raise costs and switching time; certification cycles 12–24 months and revalidation up to $1M increase switching costs. NEC uses multi-sourcing, modular design and partner agreements to mitigate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| TSMC | 55% foundry rev | Pricing/lead-time risk |

| Hyperscalers | AWS32%/Azure23%/GCP11% | Marketplace fees, roadmap leverage |

| Contract mfg | ~USD550bn | Capacity premiums |

| Certification | 12–24m / ~$1M | High switching cost |

What is included in the product

Tailored Porter's Five Forces analysis for NEC that uncovers competitive drivers, supplier/buyer power, entry barriers, substitutes, and emerging threats to inform strategic decisions and investor materials.

A single-sheet NEC Porter's Five Forces summary with customizable pressure sliders and instant spider chart—simplifies competitive analysis for fast decisions and copy-ready slides.

Customers Bargaining Power

Large enterprise and government RFPs

Governments and large CSPs buy through competitive tenders with strict SLAs and penalties, forcing NEC to accept tight delivery and uptime commitments. Their scale drives aggressive pricing and demands for customization, while multi-year framework agreements (typically 3–5 years) compress margins but give predictable revenue. NEC defends value through security certifications, carrier-grade reliability, and systems integration capabilities. This mix raises customer bargaining power but preserves premium for differentiated solutions.

High switching costs, but savvy buyers

Integrated IT-network solutions embed deeply in operations, raising technical and organizational switching costs; NEC reported about 3.4 trillion yen in consolidated revenue for FY2023 (year to March 2024), underscoring scale. Buyers leverage pilot phases and proof-of-concepts to reduce asymmetry, yet even with lock-in they insist on service credits and roadmap commitments. NEC counters with lifecycle support and open interfaces to ease customer concerns.

Outcome-based and subscription models

Clients increasingly prefer OPEX, managed services and outcome-linked pricing, shifting risk to vendors and intensifying price scrutiny; IDC estimated the global managed services market at about $300B in 2024, reflecting this shift. Benchmarking across providers and transparent SLAs enhances buyer leverage and compresses margins. NEC bundles software, services and maintenance to stabilize ARPU and offset contract risk.

Security and compliance requirements

Public safety and critical infrastructure buyers increasingly mandate certifications such as ISO/IEC 27001, NIST CSF and SOC 2 plus regular audits, narrowing the pool of qualified vendors and partially softening buyer switching power. Compliance obligations allow buyers to demand tailored features at vendor expense, raising customization pressure. NEC’s long track record and certifications boost trust but increase cost-to-serve.

- Certifications: ISO/IEC 27001, NIST CSF, SOC 2

- Market effect: fewer qualified vendors → reduced buyer options

- Commercial impact: higher customization cost absorbed by vendors

Global alternatives and multi-vendor strategies

Clients often split awards among multiple vendors to avoid dependence, with multi-vendor sourcing now used by roughly half of large operators; international competitors enable cross-border price comparisons, driving continuous re-bidding and renegotiation. NEC leans on reference architectures and integration prowess to remain a preferred vendor in a global telecom equipment market ~140 billion USD in 2024.

- Multi-vendor adoption ~50%

- Global market ~140B USD (2024)

- Continuous re-bidding increases price pressure

- NEC advantage: reference architectures + integration

Tenders, strict SLAs and OPEX managed services ($300B) empower buyers

Large government and CSP buyers use competitive tenders, strict SLAs and multi‑year (3–5y) frameworks to pressure pricing and customization, raising customer bargaining power despite NEC’s security certifications and carrier-grade integration. OPEX/managed models (global managed services ≈ $300B 2024) increase price scrutiny; multi-vendor sourcing ~50% reduces lock‑in.

| Metric | Value |

|---|---|

| NEC FY2023 revenue | ¥3.4T |

| Managed services market 2024 | $300B |

| Telecom equip. market 2024 | $140B |

| Multi-vendor adoption | ~50% |

Preview Before You Purchase

NEC Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of NEC you'll receive after purchase—fully formatted and ready for use. It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. Instant download upon payment—no placeholders, mockups, or surprises.